Since we have really limited backtest data on 10s timeframe: would it be an idea to optimise every 2 days, pick 10 results then take an average over a week or month? Or optimise daily and take an average after a couple of weeks?

Any thoughts on how to get an average optimised value on this timeframe that might actually work?

@snuckle would you mind sharing your version here?

i just replaced your indicator with this one.

your idea on getting an average over a couple of weeks is not a bad idea, maybe reoptimize after 1 week and keep the first still live and see how the new one performs

and at the same time take an average of the first optimization and the second and at the end have 3 running at the same time

Paul

PaulParticipant

Master

thnx. I’ve got a snippet I added to a rough version, i’am unsure how useful it will be.

What it does i.e. for long, it shows the buy signals you miss when you’re in a long positionposition, So it doesn’t count the signal when the position is opened, only the buysignals when longonmarket.

It does also calculated cumulative those signals which total could go up quite rapidly.

In general the higher the amount of cumulative signals, is not a good sign for robustness.

for testing if interested.

conbuy=buysignal

condsell=sellsignal

// show signals

once showsignals=1

if showsignals then

once count1l=0

once count1s=0

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

count2l=0

count2s=0

endif

if longonmarket then

if condbuy then

count1l=count1l+1

count2l=count2l+1

endif

endif

if shortonmarket then

if condsell then

count1s=count1s-1

count2s=count2s-1

endif

endif

graph count1l as "long signals in position cumulative"

graph count2l as "long signals in position"

graph count1s coloured(255,0,0,255) as "short signals in position cumulative"

graph count2s coloured(255,0,0,255) as "short signals in position"

endif

Link to above added as Log 263 to here …

Snippet Link Library

@paul by implementing your snippet, do we need to change cumulateorders= true? I was experimenting with cumulate orders = true in my code as you can see but failed to get more positive results. I think it would be worth taking a look at implementing some reversal code to exit trades as I think the current one isn’t performing very well.

PaulParticipant

Master

do we need to change cumulateorders= true

no because although it hits the same points, I wanted to optimise a strategy normally with 1 position, but still have visible the missed signals & the totals.

I’am not a fan of reversal because it cover ups the fact that the original signal was poor.

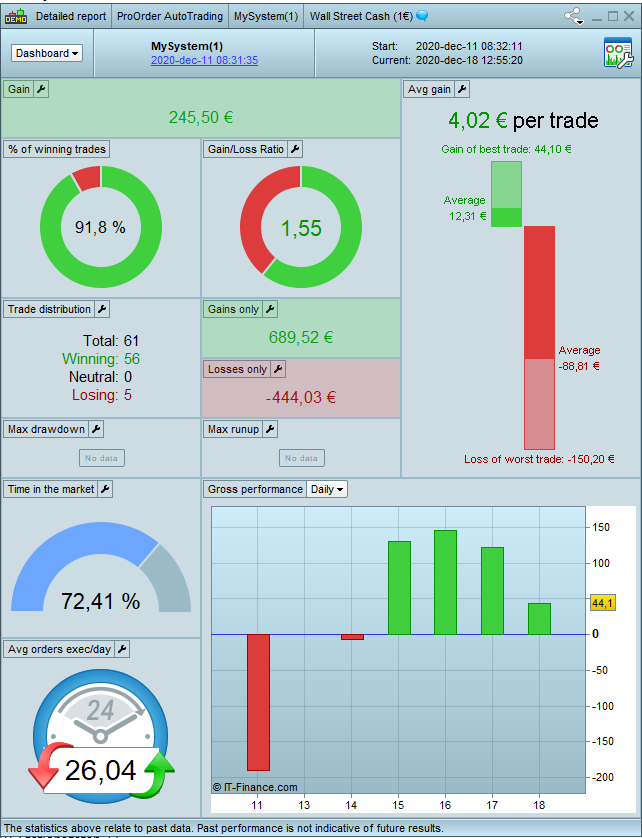

Results from first optimization on 70/30 WF have now been live for one week, seems ok so far.

did a new optimization on 70/30 WF and will be running it live simultaniously to this one and see if the first one fades or not.

If not too complicated

Maybe snucke would prefer to share his version of the .itf with us all?

Be easier than typing instructions etc??

Hi snucke and everyone else, how do you ensure that the minimum stop distance isn’t violated? I’m on IG and I’ve been trying a few different versions but the algorithm fails because the minimum stop distance of 6 pips isn’t respected. Thanks in advance for any tips regarding this.

IG minimum stop distance on the DJ is 10

Right, my bad. Any idea of how to configure this in the code?

EDIT: This restriction applies to the stop orders as well right?

This is my attempt at respecting the stop distance, it was added in the end of the stop loss code in snuckes latest version of this. I’m putting it on demo again to see if it works.

if newSL > 0 then //and abs(newSL-tradeprice) < stopRoom then

if newSL-tradeprice > 0 and newSL-tradeprice < stopRoom then

newSL = newSL + (stopRoom-(newSL-tradeprice))

elsif newSL-tradeprice < 0 and newSL-tradeprice > -stopRoom then

newSL = newSL - (stopRoom+(newSL-tradeprice))

endif

endif