I’m back experimenting in renko-land. I think there’s potential in this. Has anyone experimented with running simultaneous strategies with different box sizes? I.e, backtest show a nice equity curve with box size 50, then launch 5 strategies with small lot size at renko box 40, 45, 50, 55, 60? one could experiment with different trailing stop settings on each strategy too to diversify further. I get a really nice equity curve with Doctrading “Pure Renko” strategy. I still believe that having a dynamic box size is better but haven’t yet figured it out. Maybe if one look at the relationship between a moving average and the daily price with a multiplier?

I will launch some bots in demo and will let you know what the results are.

As always, any ideas would be welcome.

I been experience 0.1 % setting with 10MA. If 2 boxes crosses over MA entry buy order! stop loss below 2 boxes. Short for vice versa.

for me, it’s a waste of time the renko. But enjoy for your studies.. 😉

Any strategy with a low risk/reward ratio and/or without a proper money management will fail. I know people who are doing very well with Renko trading.

Nicolas,

Manual trading with renko or automatic strategy ? I’m curious to see anybody with profits on live account with an automatic strategy

Both. Why curious? Whatever the price representation, it all depends of the strategy 😉

Currently testing this Renko strategy out. Too early to say but so far it’s working well.

Peux tu partager le code de ta stratégie ?

Merci d’avance

Can you share the code of your strategy?

thank you in advance

Only post in the language of the forum that you are posting in. For example English only in the English speaking forums and French only in the French speaking forums.

Thank you 🙂

@Fab28 I’m using a custom trend indicator bought from one of the guys here on the forum so the code won’t work unless you have that indicator. If I can adapt the strategy with supertrend I can post it here but at the moment it’s relying on this indicator.

Paul

PaulParticipant

Master

still interresting even without the indicator but how does yor code do live?

That looks interesting. Can you say which custom indicator, am curious to take a look?

Thanks,

S

Hi @Paul and @samsampop

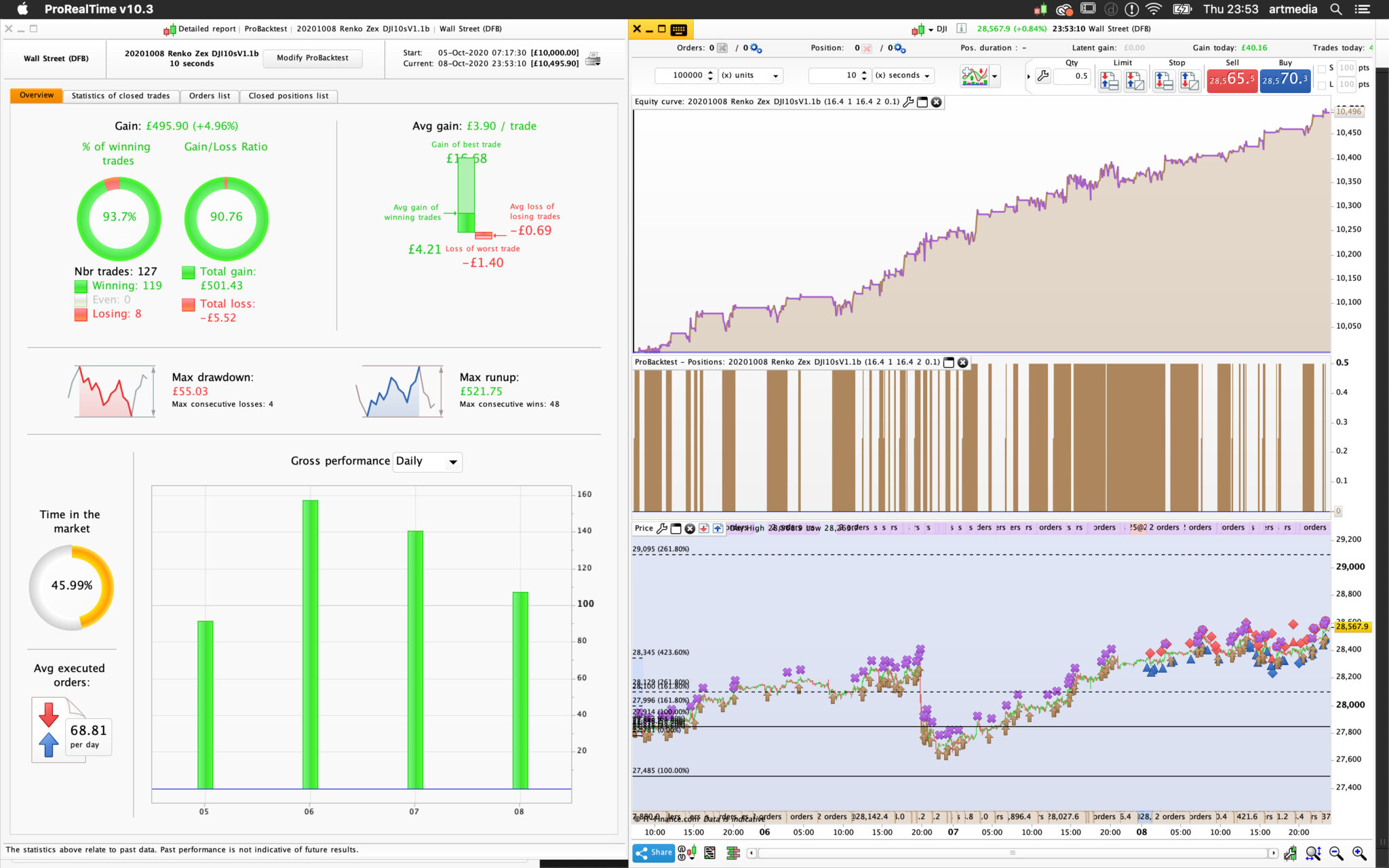

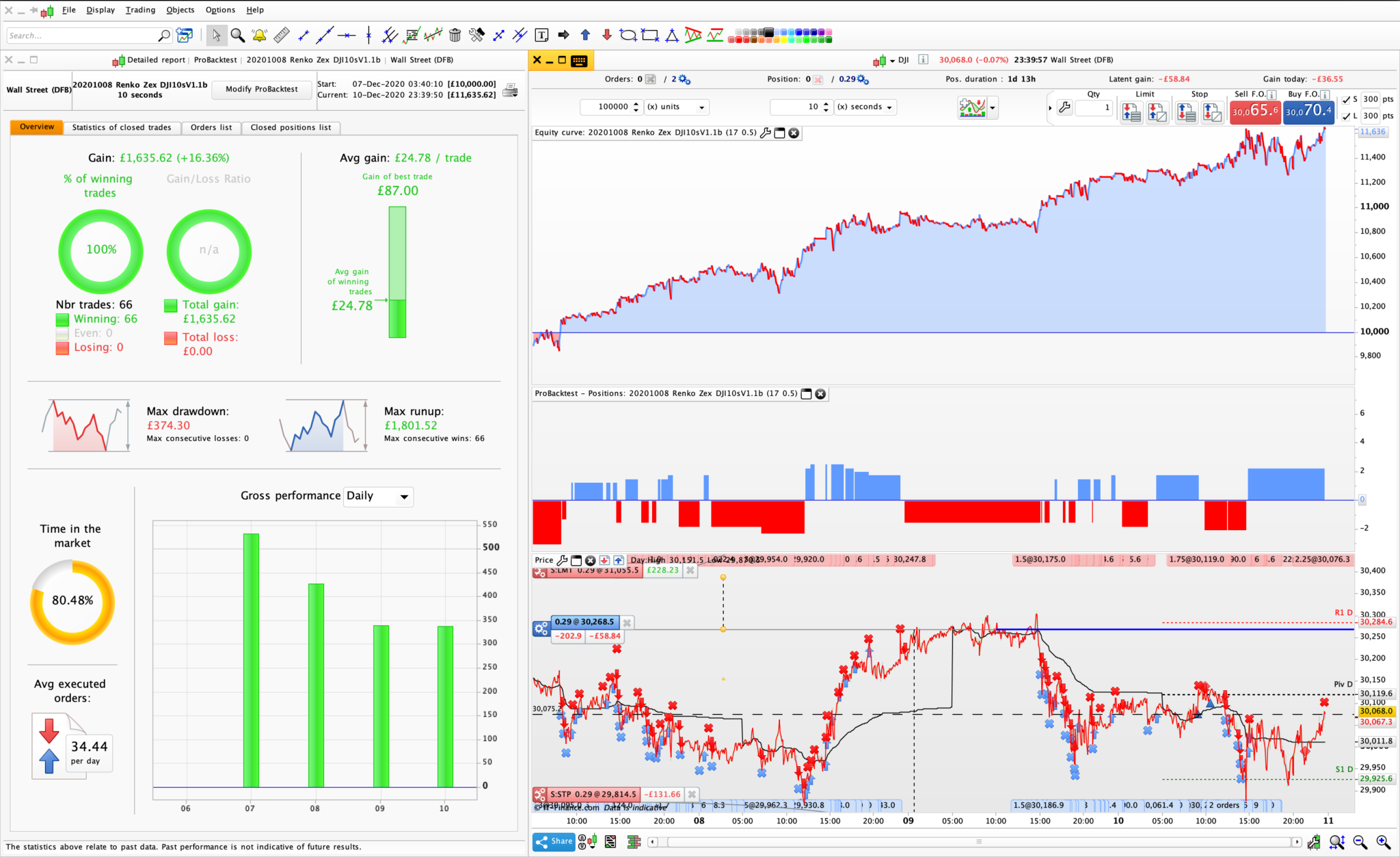

Sorry, I haven’t been very active recently. I revisited this code and it seems to have some potential. With minimal optimisation it still produces a good back test. It breaks all the rules, too many parameters, too little historic data etc. But I’m still interested in this kind of automatic scalping strategies. Any ideas would be welcome. The custom indicator (Perfect Trend Filter) is made by @aleale from his website.

defparam cumulateorders = false

// MM start

equity = 1000+STRATEGYPROFIT

risk=0.3

TF=15

if OpenDayofWeek = 0 then

//OkToTrade = 0

elsif OpenDayofWeek = 1 then // Monday

DailyRange=max(abs(Dhigh(2)-Dlow(2)),max(abs(Dhigh(2)-Dclose(3)),abs(Dlow(2)-Dclose(3))))

elsif OpenDayofWeek = 2 then // Tuesday

DailyRange=max(abs(Dhigh(1)-Dlow(1)),max(abs(Dhigh(1)-Dclose(3)),abs(Dlow(1)-Dclose(3))))

else

DailyRange=max(abs(Dhigh(1)-Dlow(1)),max(abs(Dhigh(1)-Dclose(2)),abs(Dlow(1)-Dclose(2))))

endif

DailyRange=max(abs(Dhigh(0)-Dlow(0)),DailyRange)

DailyATR=wilderaverage[20*TF](DailyRange)

a = (equity*risk)/(DailyATR)

t = a * 100

x = 0

// .25 decimal position sizes

incrementsize = 25

while x < t do

x = x + incrementsize

if x > t then

if x - t > incrementsize/2 then

x = x - incrementsize

endif

PositionSize = (x/100)

break

endif

wend

//once positionsize = 0.2

timeframe (1 minute)

//12:1 filter by Vonasi

Period = 12

Divider = 2

Filter = (close - open[Period - 1]) - (close - open[(Period / Divider) - 1])

if filter > 0 then

bull = 1

else

bull = 0

endif

if filter < 0 then

bear =1

else

bear = 0

endif

//12:1 filter end

timeframe (2 minutes)

trendfilter, ignored = CALL "$AT.IT Perfect Trend Filter"[4, 0]

if close > trendfilter then

trend = 1

else

trend = -1

endif

// ZEX indicator

timeframe (1 minute)

a1=SMI[20,6,5](close)

b1=triangularaverage[5](a1)

zex1=1.618*(a1-b1)

//

//timeframe (30 seconds)

//a2=SMI[12,6,5](close)

//b2=triangularaverage[5](a2)

//zex2=1.682*(a2-b2)

//

//timeframe (20 seconds)

//a3=SMI[12,6,5](close)

//b3=triangularaverage[5](a3)

//zex3=1.682*(a3-b3)

timeframe (Default)

//renko code

boxsize = 17 //17.1

volumesize=average[21](volume)*10

volumesum = volumesum+volume

once renkoMax = ROUND(close / boxSize) * boxSize

once renkoMin = renkoMax - boxSize

IF high > renkoMax + boxSize and volumesum-lastvolume>=volumesize THEN

WHILE high > renkoMax + boxSize

renkoMax = renkoMax + boxSize

renkoMin = renkoMin + boxSize

lastvolume = volumesum

WEND

ELSIF low < renkoMin - boxSize and volumesum-lastvolume>=volumesize THEN

WHILE low < renkoMin - boxSize

renkoMax = renkoMax - boxSize

renkoMin = renkoMin - boxSize

lastvolume = volumesum

WEND

ENDIF

// trend filter

if trend=1 and bull and zex1 > 0 then

buysignal = 1

else

buysignal = 0

endif

if trend=-1 and bear and zex1 < 0 then

sellsignal = 1

else

sellsignal = 0

endif

//entry conditions

if not onmarket and buysignal then

buy positionsize contract at renkoMax + boxSize stop

elsif not onmarket and sellsignal then

sellshort positionsize contract at renkoMin - boxSize stop

endif

fastrsi = rsi[2]

maxposition=positionsize*2

if countofposition<=maxposition then

if longonmarket and fastrsi crosses under 30 then

buy positionsize contract at market

endif

if shortonmarket and fastrsi crosses over 70 then

sellshort positionsize contract at market

endif

endif

// stop loss

MaxStopValue = round(equity*risk)

set stop ploss maxstopvalue

//// close long position when price reverses

//if longonmarket and trend=-1 and bear=1 then

//longexit2 = 1

//else

//longexit2 = 0

//endif

//

//// close short position when price reverses

//if shortonmarket and trend=1 and bull=1 then

//shortexit2 = 1

//else

//shortexit2 = 0

//endif

//

//

//if longonmarket and longexit2=1 then

//sell positionsize contract at market

//sellshort positionsize contract at market

//longexit2=0

//endif

//

//if shortonmarket and shortexit2=1 then

//exitshort positionsize contract at market

//buy positionsize contract at market

//shortexit2=0

//endif

//

//if longonmarket and sellsignal then

//sell at market

//buy positionsize contract at market

//endif

//

//if shortonmarket and buysignal then

//sellshort at market

//buy positionsize contract at market

//endif

//

timeframe (Default)

//trailing stop function

trailingstart = 13 //15.7 //trailing will start @trailinstart points profit

trailingstep = 2.9 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

timeframe (20 seconds)

// reversal exit

once longexit =1

once shortexit=1

if longexit then

if longonmarket then

minrangedistL=1

cl1=close<open and close[1]<open[1] and close[2]<open[2]

cl2=(close=low or close[1]=low[1] or close[2]=low[2])

cl3=(range>(close/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL)

if cl1 and cl2 and cl3 then

sell at market

sellshort positionsize contract at market

endif

endif

endif

if shortexit then

if shortonmarket then

minrangedistS=1

cs1=close>open and close[1]>open[1] and close[2]>open[2]

cs2=(close=high or close[1]=high[1] or close[2]=high[2])

cs3=(range>(close/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS)

if cs1 and cs2 and cs3 then

exitshort at market

buy positionsize contract at market

endif

endif

endif

// Friday 22:00 Close ALL operations.

IF DayOfWeek = 5 AND time = 214500 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

set stop %loss 0.5

thanked this post

Might you share the .itf containing the Indicator please?

i think he mentioned that its been bought by ALE, GraHal

i applied another trendfilter with 70/30 WF and got almost identical results.

so i guess any trendfilter works, for better or worse 🙂