I do not wish to be misled by a so-called belief in the recurrence of numbers designating empirical periods that no one could challenge. I do not think 27 is different from 26. The only difference is that the majority of market participants use the same thing, that’s all. It would then be enough to act like a sheep and follow the pack to verify that a period is more adequate than another one.

So I think you’re right, but there’s no divine force acting on market prices to induce the fact that one period is much more effective than another, it’s only human behavior Which makes today a RSI of period 14 is more adequate than another one of period 10. Of course this is especially true on instruments specially traded.

But this is not the subject of discussion, and it is useless to embark on philosophical discussions on this subject 🙂

@nicolas I agree, a number is but a number. However certain numbers are definitely more ‘interesting’ than others. Case in point being Fibonacci sequences (pure mathematical genius). People drive the behavior of markets and people are for some reason just more attracted to some numbers rather than other (for whichever reason). And because of that, they can be leveraged in financial markets (hence why I suspect Goichi Hosada spent so many years studying it).

Okay so maybe just to keep this thread alive, here is one of the initial strategies I experimented with, although it doesn’t qualify according to my initial criteria it did help me to realize that a RSI 2 strategy on it’s own is not enough. Also this strategy has a variable ‘z’ that needs to be optimized. It did yield ‘decent’ results (attached with spread of 20) on my local market though. However I have ventured on from here by at the same time simplifying my use of the RSI 2 period and adding the ‘aha’ ingredient that finally got it completely market neutral.

possize = 2

MA = Average[100](close)

RS2 = RSI[2](close)

ATR = AverageTrueRange[2](close)

once Long = 0

once Short = 0

If Long >= 1 Then

Short = 0

ElsIf Short >= 1 Then

Long = 0

EndIF

If Long = 1 or Short = 1 Then

z = 9

ElsIf Long = 2 or Short = 2 Then

z = 6

EndIf

If close > MA and RS2 < 5 and Long = 0 Then

Long = 1

LC = close //close at point of RSI oversold

ElsIf close < MA and RS2 > 95 and Short = 0 Then

Short = 1

SC = close //close at point of RSI overbought

EndIf

PSH = high[1] //Previous Swing High

PSL = low[1] //Previous Swing Low

For i = 2 to z

If close[i] > PSH Then

PSH = close[i]

ElsIf close[i] < PSL Then

PSL = close[i]

EndIf

Next

If Long = 1 and close > PSH Then

Long = 2

ElsIf Short = 1 and close < PSL Then

Short = 2

EndIF

If countofposition = 0 and close > MA and Long = 2 and RS2[1] < 5 and RS2 > 5 and close > LC Then

Buy possize contract at market

LE = 0 //Long Exit Counter set to 0

EndIf

If countofposition = 0 and close < MA and Short = 2 and RS2[1] > 95 and RS2 < 95 and close < SC Then

Sellshort possize contract at market

SE = 0 //Short Exit Counter set to 0

EndIf

If longonmarket and RS2 > 95 and LE = 0 Then

LE = 1

ElsIf shortonmarket and RS2 < 5 and SE = 0 Then

SE = 1

EndIf

If (longonmarket and LE = 1 and close < PSL) or (close < close[1] - ATR and RS2 < 5) Then

Sell at market

Long = 0

ElsIf (shortonmarket and SE = 1 and close > PSH) or (close > close[1] + ATR and RS2 > 95) Then

Exitshort at market

Short = 0

EndIf

So the only optimized variable is “z”, as the period lookback to find breakout of previous swing high/low?

I made a quick optimization myself on the french CAC40 index, and on 200k bars. Results was not bad (1 hour chart), but not so steady as the one you get with SAF40.

The classic RSI 2 periods strategy is built upon the assumption that market is mean reverting (in a bullish trend and in a daily timeframe), why do you think it is still the case on intraday charts and with a potentiel “universality”?

@nicolas you pose a fair question for which I cannot provide a fair answer 🙂 I think for everyone’s sake I am just going to go ahead and post my Universal Strategy to the library (I think you are going to like it!) – Simple yet it works on all markets

Nice! I am impatient that you post it! thank you!

@nicolas I have submitted the strategy to the library. As soon as it is posted I will add some comments with regards to it’s market dynamics. I.e. how it can theoretically perform in both ranging and trending markets by means of either Bollinger breakouts (Trending) or Bollinger reversals (Ranging). I used the CAC40 and ZAF40 as examples, both on which it will outperform the index while decreasing drawdown completely un-optimized. Even keeping the trading times the same! I found 01h00 to 18h00 (UCT +2) to work well on both markets.

Thanks, I’ll have a look this evening or by tomorrow morning.

@pepsmile @wing @inertia @grahal the strategy has been posted to the library:

Universal Strategy

You are welcome to have a look, would be interesting to see any modifications to make it even better on ‘all’ markets.

I have an suspicion that we can definitely do some work on the stop.

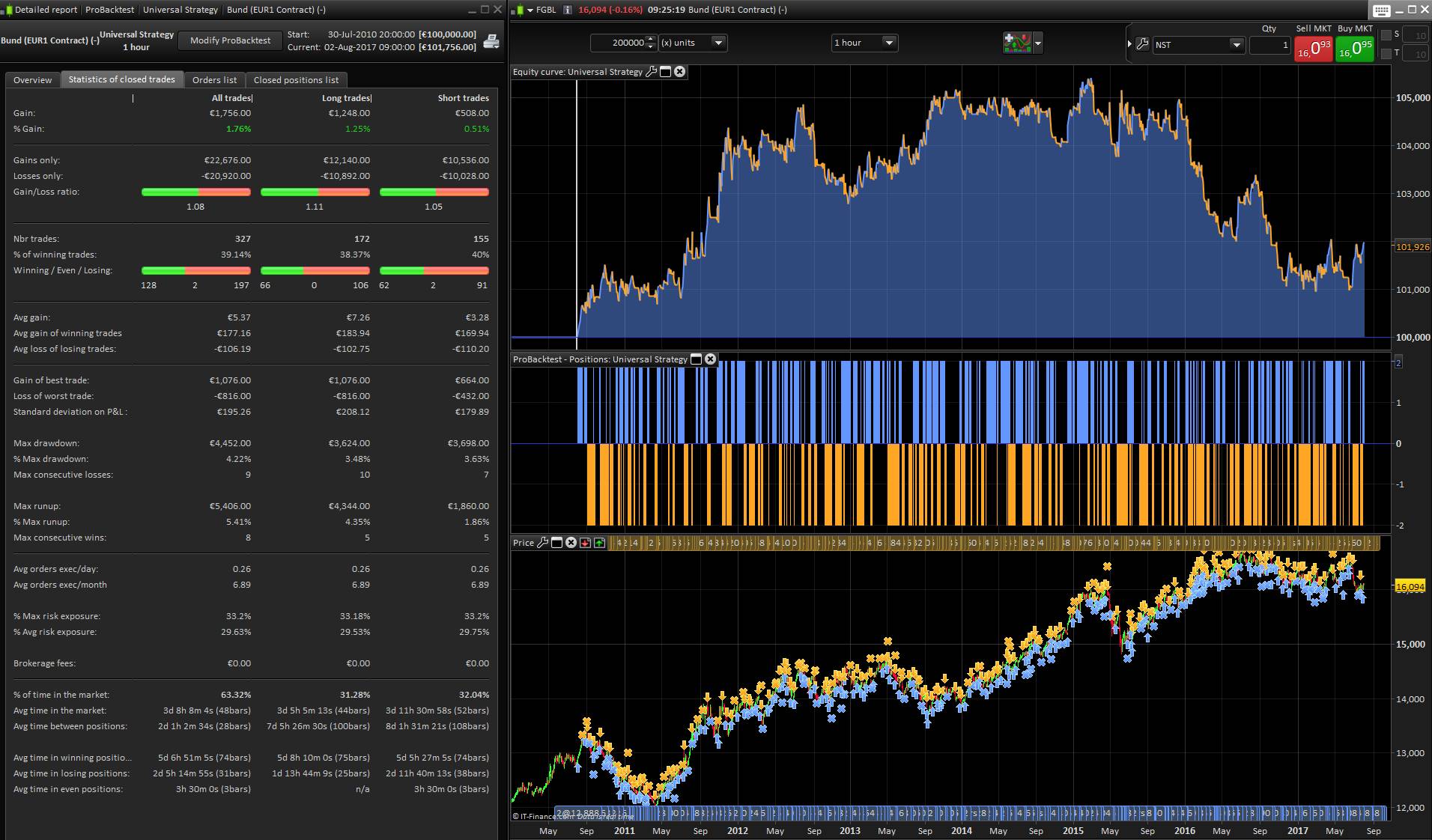

PFA the “Universal strategy” results (rough ones with same settings in 1 hour timeframe) for Bund (5 pts spread) and DAX (2 pts spread). I have not change anything for the time schedules. Test are made as far possible with tick-by-tick backtest.

Your thought about incorporate a trailing stop would mean to have also a universal setting for all possible instrument, so trailing the profit on price only is not an option IMO. Any other idea apart the classic ATR value? 🙂

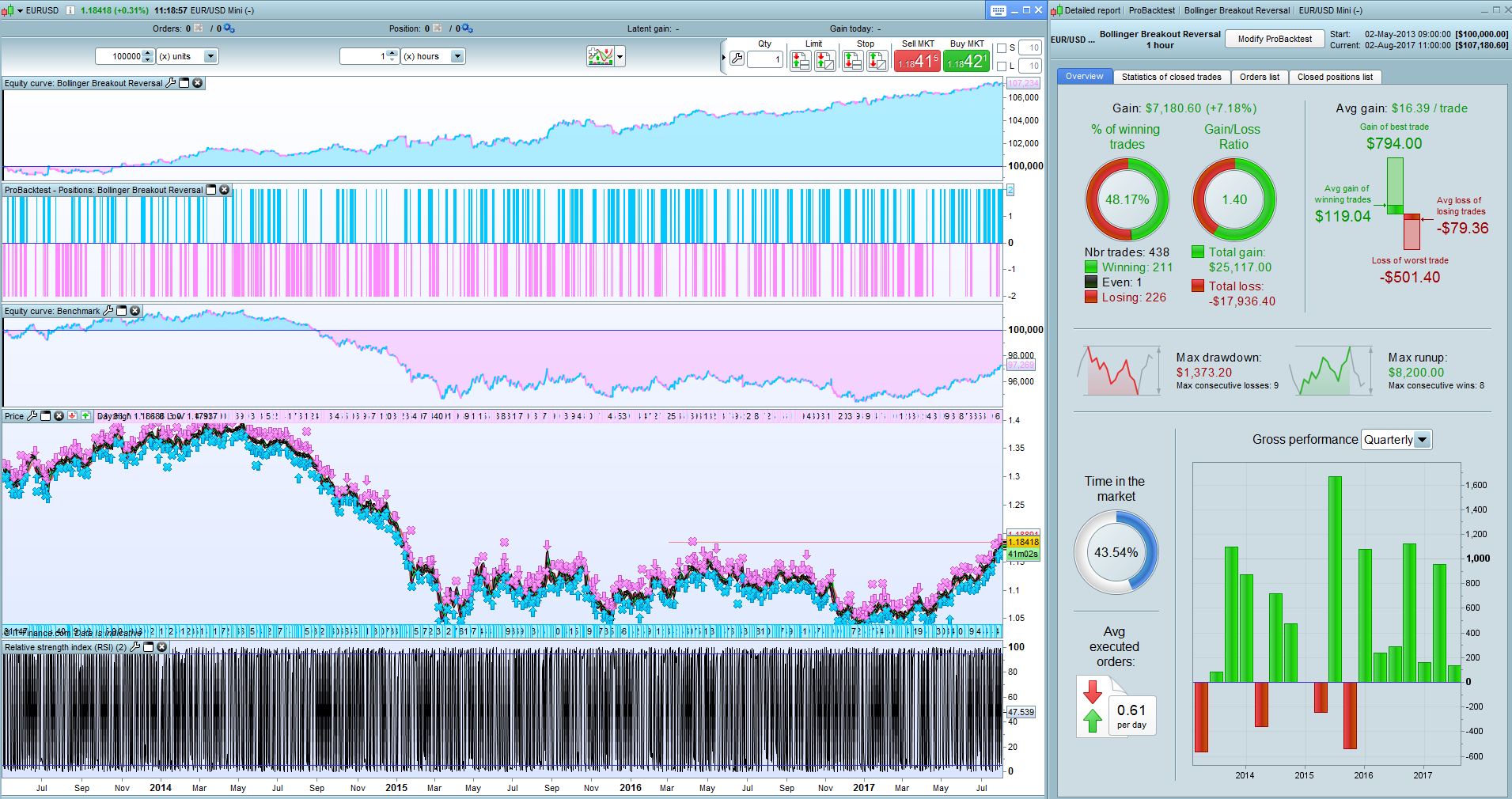

@nicolas attached EUR/USD with lastest modification (posted in library) to Stop. Definitely feel there are more room for improvement especially on the exit side.

Attached the latest version of code with modification to the stop.

Okay so on the topic of improving the stop even further I have started experimenting on distinguishing between Entry on a Bollinger breakout (BB = 1) vs. Entry on Bollinger Reversal (BB =0) by allocating the variable called BB and then using this variable to assign separate exit criteria. So far this is yielding positive results. Will post the updated file with some backtests when done.

Hi!

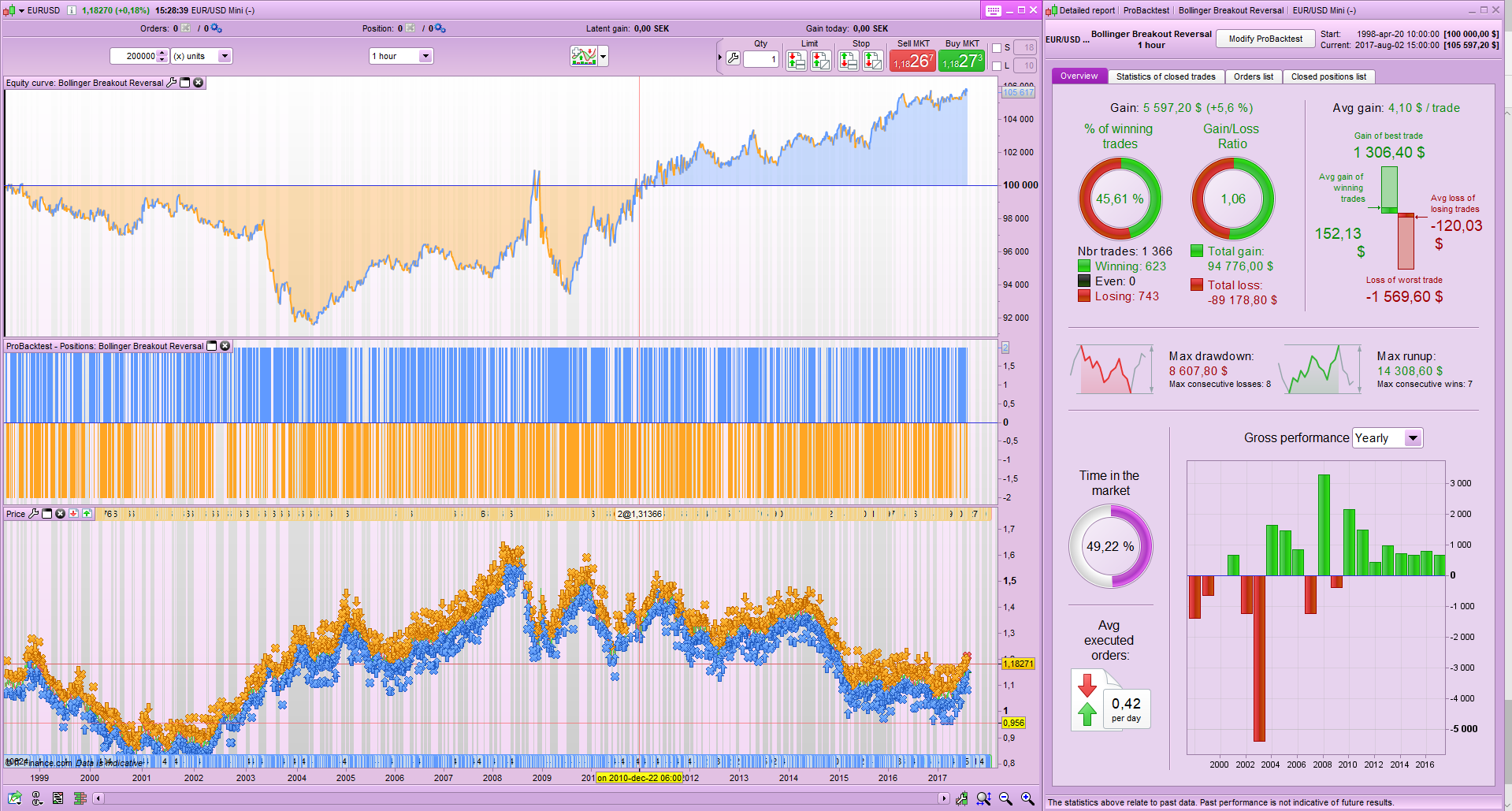

Here is EUR/USD on ig with 200k bars.

Regards

Henrik

@Hendrik interesting, did you optimize the trading time filter to take into account your timezone? Glad to see it is still outperforming Buy and Hold over 200k though.

I am actually making good progress with the modifications, going through each trade and looking for logical improvements.

Will really appreciate it if you will run the same test with the modified version that I will hopefully post tonight.