Merci Nicolas,

le code se comporte en effet bien différemment!

je vais continuer à conditionner pour éviter les faux signaux.

Grand Merci

Merci Nicolas,

Fonctionne très bien pour chaque UT.

La stratégie est maintenant Opérationnelle et Fonctionnelle…

Slts

Bonne nouvelle, et bonne continuation ! 😉

Bonjour Fantasio peux tu montrer ton code rectifié entièrement que je comprenne bien

timeframe(15 minute)

MMA100A15 = ExponentialAverage[100](close)

MMA300A15 = ExponentialAverage[300](close)

MMA600A15 = ExponentialAverage[600](close)

MMA1000A15 = ExponentialAverage[1000](Close)

BuyConditionA = (Close > MMA100A15) and (Close > MMA300A15) and (Close > MMA600A15) and (Close > MMA1000A15)

if BuyConditionA then

xA = BuyConditionA

endif

//déclare la stratégie dans l'UT 5 minutes

timeframe(5 minute)

MMA100A5 = ExponentialAverage[100](close)

MMA300A5 = ExponentialAverage[300](close)

MMA600A5 = ExponentialAverage[600](close)

MMA1000A5 = ExponentialAverage[1000](Close)

BuyConditionB = (Close > MMA100A5) and (Close > MMA300A5) and (Close > MMA600A5) and (Close > MMA1000A5)

if BuyConditionB then

yA = BuyConditionB

endif

Voici un morceau du code rectifié…. et de cette manière, les variable sont bien lues dans Chaque UT Correspondante 🙂

De cette manière tu obtiens les convergences recherchées.

Je vais faire tourner la stratégie un moment en réel pour m’assurer que ça me donne les mêmes résultat qu’en BackTest….le WALKFORWARD fonctionne bien de 10/80 à 50/50…donc il n’y a pas de raison que ça n’aille pas….

je dois intégrer quelques conditions pour améliorer mon ratio Gain/Perte

je vous tiendrez informé.

Slts

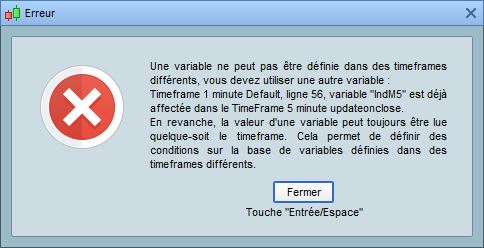

PRT V11 affiche un message d’erreur explicite dans ce cas. Toutes les variables définies dans un timeframe ne peuvent être redéfinies dans un autre timeframe

Le code total d’origine de fantasio ici https://www.prorealcode.com/topic/probleme-multiframe-sur-3-unites-de-temps/#post-132464 devient par exemple

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

//DEFPARAM FLATBEFORE = 091500

//DEFPARAM FLATAFTER = 154500

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

//Indicateurs de tendance

Pivot = (DHigh(1) + DLow(1) + DClose(1) + DOpen(0))/4

//Indicateurs de prise de positions

//Position acheteuse

//declare the strategy on the 15 minutes timeframe

timeframe(15 minute, updateonclose)

MMA100M15 = (ExponentialAverage[100](close))

MMA300M15 = (ExponentialAverage[300](close))

MMA600M15 = (ExponentialAverage[600](close))

MMA1000M15 = (ExponentialAverage[1000](close))

IndM15 = RSI[7](Close)

xM15 = 0.1 * (IndM15 - 50)

yM15 = (EXP (2 * xM15) - 1) / (EXP (2 * xM15) + 1)

zM15 = 50 * (yM15 + 1)

TimeM15aa = Close > MMA100M15

TimeM15ab = Close > MMA300M15

TimeM15ac = Close > MMA600M15

TimeM15ad = Close > MMA1000M15

TimeM15ae = zM15 < 38.2

buyconditionM15 = (TimeM15aa and TimeM15ab and TimeM15ac and TimeM15ad and TimeM15ae)

//declare the strategy on the 5 minutes timeframe

timeframe(5 minute, updateonclose)

MMA100M5 = (ExponentialAverage[100](close))

MMA300M5 = (ExponentialAverage[300](close))

MMA600M5 = (ExponentialAverage[600](close))

MMA1000M5 = (ExponentialAverage[1000](close))

IndM5 = RSI[7](Close)

xM5 = 0.1 * (IndM5 - 50)

yM5 = (EXP (2 * xM5) - 1) / (EXP (2 * xM5) + 1)

zM5 = 50 * (yM5 + 1)

TimeM5aa = Close > MMA100M5

TimeM5ab = Close > MMA300M5

TimeM5ac = Close > MMA600M5

TimeM5ad = Close > MMA1000M5

TimeM5ae = zM5 < 38.2

buyconditionM5 = (TimeM5aa and TimeM5ab and TimeM5ac and TimeM5ad and TimeM5ae)

//declare the strategy on the 1 minutes Default

timeframe(1 minute, Default)

MMA100Dft = (ExponentialAverage[100](close))

MMA300Dft = (ExponentialAverage[300](close))

MMA600Dft = (ExponentialAverage[600](close))

MMA1000Dft = (ExponentialAverage[1000](close))

IndDft = RSI[7](Close)

xDft = 0.1 * (IndDft - 50)

yDft = (EXP (2 * xDft) - 1) / (EXP (2 * xDft) + 1)

zDft = 50 * (yDft + 1)

TimeM1aa = Close > Pivot

TimeM1ab = Close > MMA100Dft

TimeM1ac = Close > MMA300Dft

TimeM1ad = Close > MMA600Dft

TimeM1ae = Close > MMA1000Dft

TimeM1af = zDft < 38.2

buyconditiondft = (TimeM1aa and TimeM1ab and TimeM1ac and TimeM1ad and TimeM1ae and TimeM1af)

if (buyconditionM15 and buyconditionM5 and buyconditionDft) and not daysForbiddenEntry then

buy 0.3 share at market

endif

//Position Vendeuse

//declare the strategy on the 15 minutes timeframe

timeframe(15 minute, updateonclose)

TimeM15va = Close < MMA100M15

TimeM15vb = Close < MMA300M15

TimeM15vc = Close < MMA600M15

TimeM15vd = Close < MMA1000M15

TimeM15ve = zM15 > 61.8

sellconditionM15 = (TimeM15va and TimeM15vb and TimeM15vc and TimeM15vd and TimeM15ve)

//declare the strategy on the 5 minutes timeframe

timeframe(5 minute, updateonclose)

TimeM5va = Close < MMA100M5

TimeM5vb = Close < MMA300M5

TimeM5vc = Close < MMA600M5

TimeM5vd = Close < MMA1000M5

TimeM5ve = zM5 > 61.8

sellconditionM5 = (TimeM5va and TimeM5vb and TimeM5vc and TimeM5vd and TimeM5ve)

//declare the strategy on the 1 minutes Default

timeframe(1 minute, Default)

TimeM1va = Close < Pivot

TimeM1vb = Close < MMA100Dft

TimeM1vc = Close < MMA300Dft

TimeM1vd = Close < MMA600Dft

TimeM1ve = Close < MMA1000Dft

TimeM1vf = zDft > 61.8

sellconditionDft = (TimeM1va and TimeM1vb and TimeM1vc and TimeM1vd and TimeM1ve and TimeM1vf)

if (sellconditionM15 and sellconditionM5 and sellconditionDft) and not daysForbiddenEntry then

sellshort 0.3 share at market

endif

//************************************************************************

//Stop Loss & Trailing function

SET STOP LOSS 27

trailingstart = 27 //trailing will start @trailinstart points profit

trailingstep = 9 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND close-tradeprice(1)>trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL > 0 AND close-newSL>trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND tradeprice(1)-close>trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL > 0 AND newSL-close>trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

Graphonprice pivot

Graphonprice MMA100M15

Graphonprice MMA300M15

Graphonprice MMA600M15

Graphonprice MMA1000M15

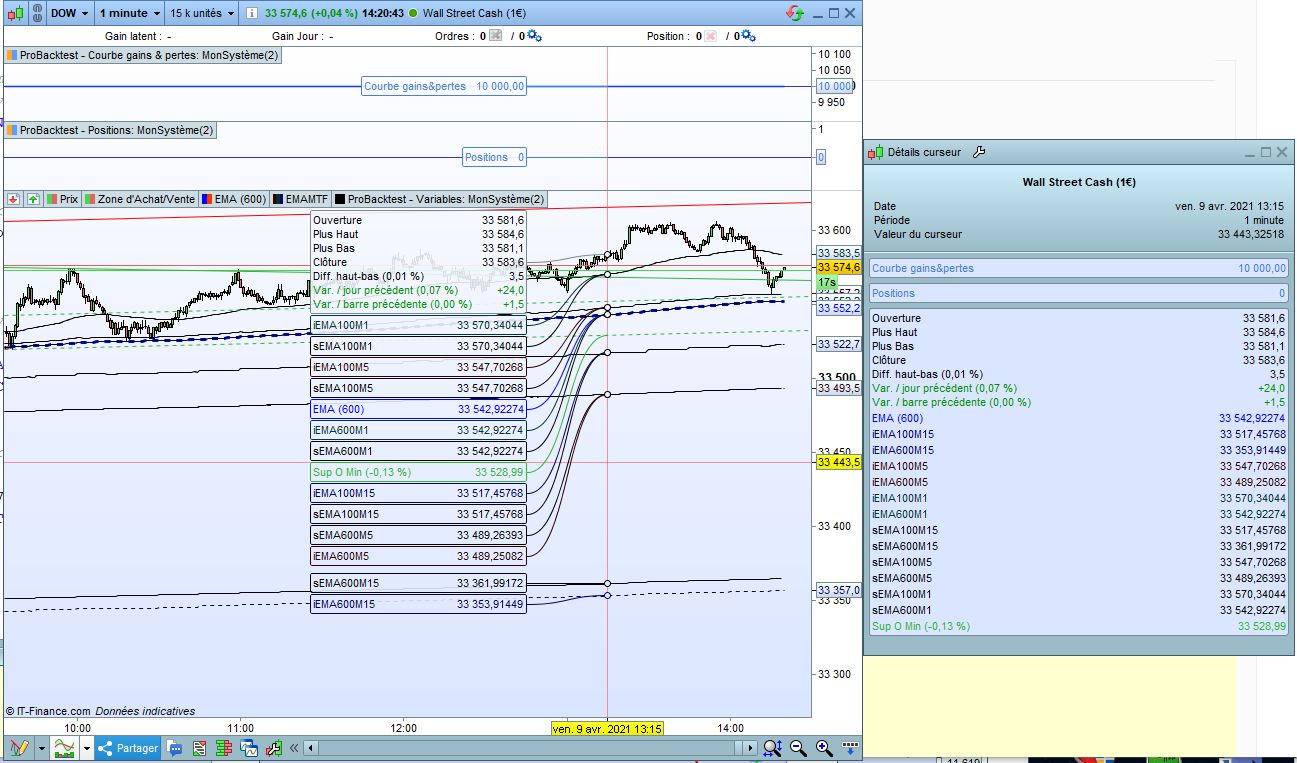

Cela dit, je pense avoir trouvé un problème de calcul car j’ai fait un indicateur qui calcule les moyennes mobiles en timeframe 15 minutes et 5 minutes sur le graphe, et les valeurs ne correspondent pas avec celles du back-test. Aucun problème pour l’EMA 100 mais des problèmes sur les calculs d’EMA sur ces périodes plus longues. Pour faire simple j’ai fait une stratégie très courte et un indicateur très court aussi qui permet de montrer le problème de calcul entre la stratégie PRT et l’indicateur

timeframe(15 minute)

MMA100M15 = (ExponentialAverage[100](close))

MMA600M15 = (ExponentialAverage[600](close))

timeframe(5 minute)

MMA100M5 = (ExponentialAverage[100](close))

MMA600M5 = (ExponentialAverage[600](close))

timeframe(1 minute)

MMA100M1 = (ExponentialAverage[100](close))

MMA600M1 = (ExponentialAverage[600](close))

return MMA100M15 as "iEMA100M15", MMA600M15 as "iEMA600M15", MMA100M5 as "iEMA100M5", MMA600M5 as "iEMA600M5", MMA100M1 as "iEMA100M1", MMA600M1 as "iEMA600M1"

Et sur la stratégie,

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

timeframe(15 minute)

MMA100M15 = (ExponentialAverage[100](close))

MMA600M15 = (ExponentialAverage[600](close))

timeframe(5 minute)

MMA100M5 = (ExponentialAverage[100](close))

MMA600M5 = (ExponentialAverage[600](close))

timeframe(1 minute)

MMA100M1 = (ExponentialAverage[100](close))

MMA600M1 = (ExponentialAverage[600](close))

Graphonprice MMA100M15 as "sEMA100M15"

Graphonprice MMA600M15 as "sEMA600M15"

Graphonprice MMA100M5 as "sEMA100M5"

Graphonprice MMA600M5 as "sEMA600M5"

Graphonprice MMA100M1 as "sEMA100M1"

Graphonprice MMA600M1 as "sEMA600M1"

VosConditions = 0

// généré automatiquement par PRT

// Conditions pour ouvrir une position acheteuse

IF NOT LongOnMarket AND VosConditions THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

// Conditions pour fermer une position acheteuse

If LongOnMarket AND VosConditions THEN

SELL AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

IF NOT ShortOnMarket AND VosConditions THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

// Conditions pour fermer une position en vente à découvert

IF ShortOnMarket AND VosConditions THEN

EXITSHORT AT MARKET

ENDIF

// Stops et objectifs : entrez vos stops et vos objectifs ici

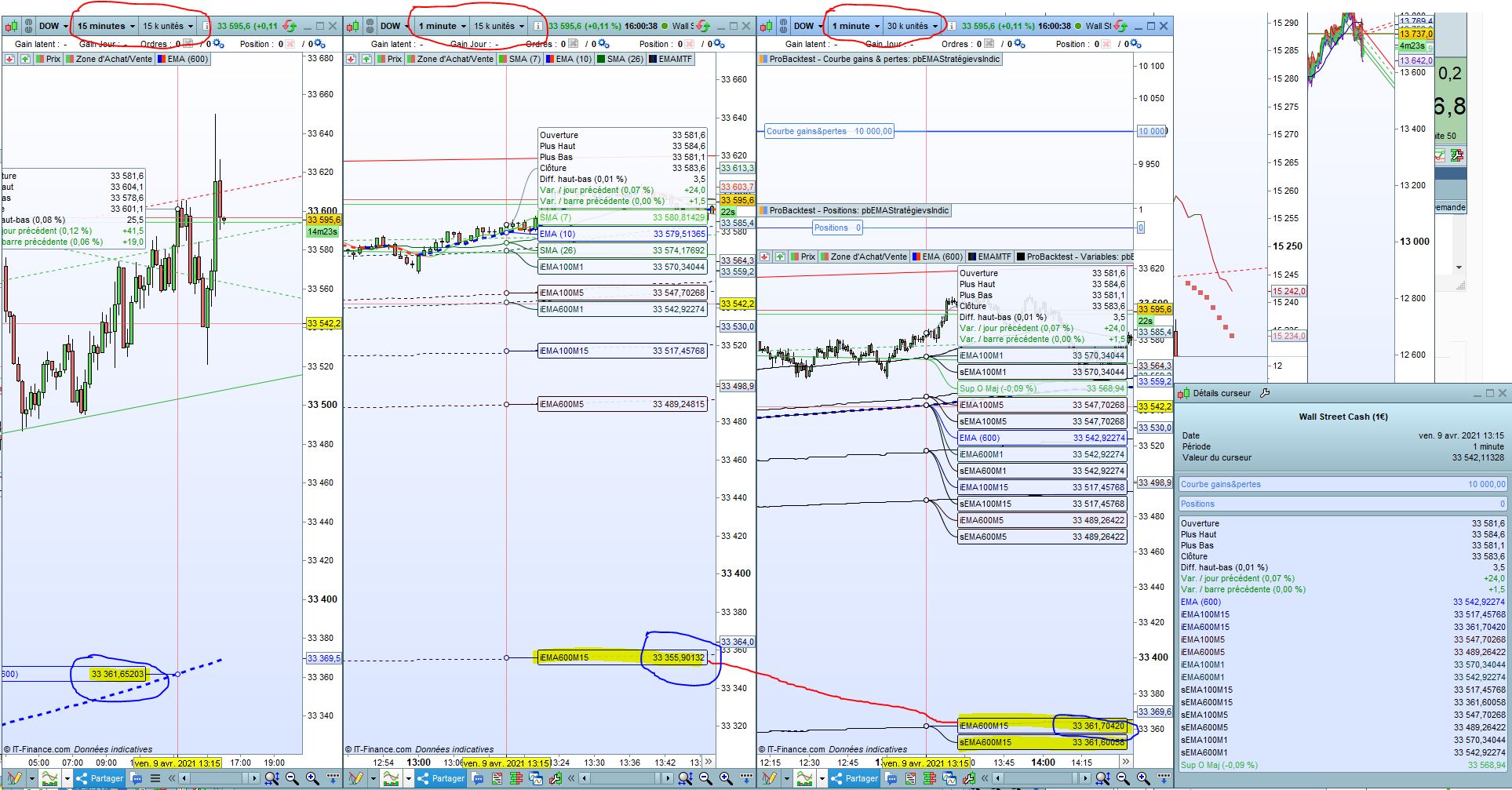

les chiffres sont différérents pour les EMA de 600 prériodes en UT M5 et UT M15. Le backtest prend toutes les dates affichées (pas de différence sur la date de début par exemple).

Nicolas tu confirmes le problème ?

Voici les ITF pour reproduire le problème :

J’ai trouvé le problème qui me semble être un bug dans le mode timeframe d’un indicateur PRT à première vue, pour avoir un calcul qui se rapproche de la réalité sur le graphique 1 minute, il faut afficher beaucoup d’unités (beaucoup plus qu’il n’en faudrait a priori pour calculer une EMA de 600 en UT 15 minutes sur un graphique 1 minute). même avec 20 k unités affichées en 1 minute, le calcul de l’EMA 600 sur un timeframe de 15 minutes est faux…

J’ai posté dans le forum anglais https://www.prorealcode.com/topic/multi-timeframe-mtf-indicators-for-prorealtime/page/4/#post-166630

Y-a-t-il une explication à ce problème ?

Oui je suis d’accord sur le principe de l’EMA mais la différence est assez sérieuse.

Ca veut dire qu’il faut se méfier des calculs récursifs longs entre indicateurs et stratégie de back test sur PRT.

Bonjour Fantasio

J’ai vu votre demande auprès de Nicolas, et je m’aperçois que je recherche quelque chose qui est très similaire et je me suis dit que peut-être, vous pourriez m’aider :

Je recherche un programme qui permet de collecter le RSI en timeframe 1mn, 5mn, et 15mn et d’afficher le résultat sur un petit coin d’écran

Auriez vous une idée ?

Merci pour votre retour