Ça vous dit de créer un groupe What’s app tous les 3 ? ☺️

Top fifi ! il faut que je demande à Nicolas c’est ça pour obtenir les numéros et adresse mails ?

defparam cumulateorders = false

once longtrading= 1

once shorttrading= 1

n = 1

m = 3

l = 90

//Robustness Tester

once j = 0

once flag = 1

if flag = 1 then

j = j + 1

if j > 1 then

flag = -1

j = j - 1

endif

endif

if flag = -1 then

j = j - 1

if j = 0 then

j = j + 1

flag = 1

endif

endif

tradeon = 1

if opendate >= 20000101 then

if barindex mod 1 = 0 or barindex mod 1 = j then

tradeon = 1

endif

endif

// Heuristics Algorithm Start

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EnDif

StartingValue = 140

ResetPeriod = 26 //Specify no of months after which to reset optimization

Increment = 20

MaxIncrement = 3 //Limit of no of increments either up or down

Reps = 22 //Number of trades to use for analysis

MaxValue = 320 //Maximum allowed value

MinValue = increment //Minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm End

cs= summation[n](close>open) = n

cs = cs and close>bollingerup[valuex](close) and close>dlow(2)

cl= summation[m](close<open) = m

cl = cl and close<bollingerdown[valuex](close) and close<Dhigh(2)

size = 2

//entry conditions

if shorttrading then

if cs and tradeon then

sellshort size contract at market

endif

endif

if longtrading then

if cl and tradeon then

buy size contract at market

endif

endif

//exit conditions

if shortonmarket and close<average[l](close) then

exitshort at market

endif

if longonmarket and close>average[l](close) then

sell at market

endif

// Stop and target

SET TARGET pPROFIT 50

StartBreakeven = 30 // How much pips/points in gain to activate the Breakeven function?

PointsToKeep = 0 // How much pips/points to keep in profit above of below our entry price when the Breakeven is activated (beware of spread)

// Reset the BreakevenLevel when no trade are on market

IF NOT ONMARKET THEN

BreakevenLevel=0

ENDIF

// Test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

// Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

SELL AT BreakevenLevel STOP

ENDIF

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

EXITSHORT AT BreakevenLevel STOP

ENDIF

Bonjour les amis ,

je suis un peu dépassé entre la première version de Vanosi du testeur de robustesse avec une variable entre 1et 22, le glisser sur le fichier excel et la toute dernière avec tradeon.

Voici une stratégie ( pour avoir un cas concret) avec la dernière version du testeur de robustesse et également le Ealerning PRT qui est intéressant pour mettre à jour des variables dans la stratégie.

Comment fonctionne cette nouvelle version tradeon ( testeur de robustesse) ?

Avez vous essayez l’algo machine learning également ?

Merci pour votre aide

Florian

thanked this post

bonsoir @Florian,

j’avais pas vu ton message

dans le test de robustest il te manque des fichiers

Hello Florian

pour l’instant, j’ai essayé avec une valeur en backtest pour modifier en dynamique le trailing profit.. j’attends de voir en démo (sur 1S, pas très significatif 200.000 candles 😉 …)

On va dire que ce topic est animé 🙂 mais j’ai pas trop le temps de m’y consacrer… j’essaie de faire fonctionner déjà une stratégie en 1S.. Si ok, j’appliquerai la méthode

pour l’instant je touche du bois 😉

Hello,

Et bien bon courage pour du 1 seconde ! Depuis le début du confinement je suis sur le PC jour et nuit je commence à être sec ! 😂

J’ai enfin réussi à lancer une nouvelle stratégie aujourd’hui sur le DJI ! Une première je suis passé en 5 min et premier trade gagnant ce jour ☺️

Je lance en complément un nouveau projet.

Je travail sur un nouvel algorithme qui je peux adapter pour gérer mes assurances-vie. L’idée est d’avoir un screener sur les indices majeurs, les commodities : GOLD, Brent, enfin les grandes classes d’actifs et zone géographique ( US, Europe, Asie, émergents). J’ai pas mal d’ETF dans mon assurance vie et des fonds purs par pays.

– FF China focus

– Germany fund

– etc…

Si vous avez ce que je recherche dans les cartons également je suis preneur. ( si ça peut me libérer du temps pour travailler les stratégies en 5 mins). Je pense c’est une stratégie qui peut finir dans les cartons car il y peux de signaux pour des mecs comme nous mais au final c’est ce que je recherche.

En moyenne 3 a 5 positions dans l’année par sous jacent c’est très bien.

Dans mon idée je suis partie sur un Time frame : 2 jours pour éviter d’avoir trop de position dans l’année. En effet en assurance-vie et sur mon contrat de Capitalisation j’ai les délais d’arbitrages et de prise d’effet à J+1 a j+2 c’est pourquoi j’ai pris TF 2 jours.

Les meilleurs indicateurs en swing trading j’ai remarqué :

SMA 4, 10 et 20 jours

EmA 5 a clôture et ouverture Croisement MACD

Fractals 3 ou 5 candles QQE

TDI

RSI

SAR

Stochastique

ADX

Évidement je vais alléger c’est juste mon brainstorming.

A +

Florian

bonsoir florian

c’est le problème des forums et il y a des personnes qui sont la que pour recuperer.

il y a un autre qui ce permet de dire que c’est de la m****

Salut Florian

toutes les bonnes idées sont à prendre 😉

pour mon pea,pee, mes ass vie, j’utilise principalement le tracé pour identifier les zones support/résistance et les bougies. En daily et hebdo

J’utilise aussi assez fréquemment après tendance baissière puis contraction, une bollinger/grosse bougie cassant bbup/ gros volume pour identifier le bon moment. Après je fais du pyramidage..

Et il faut pas se le cacher, pour l’instant, et malheureusement, c’est bien le buy & hold qui est le plus efficace pour moi. Le trading auto, c’est pour l’instant un joujou.. j’ai pas encore trouvé le graal ultime pour mon compte live.. (malgré le temps passé 🙂 ) .. Je ferai peut-être mon fainéant en achetant la solution miracle tant attendue sur le marketplace ! lol

Comme dit Fifi, ^^, y’en a faudrait leur filer tous les fichiers itf possibles 😉 y’en a qui les balancent direct en live avec 10 contrats ! 😀

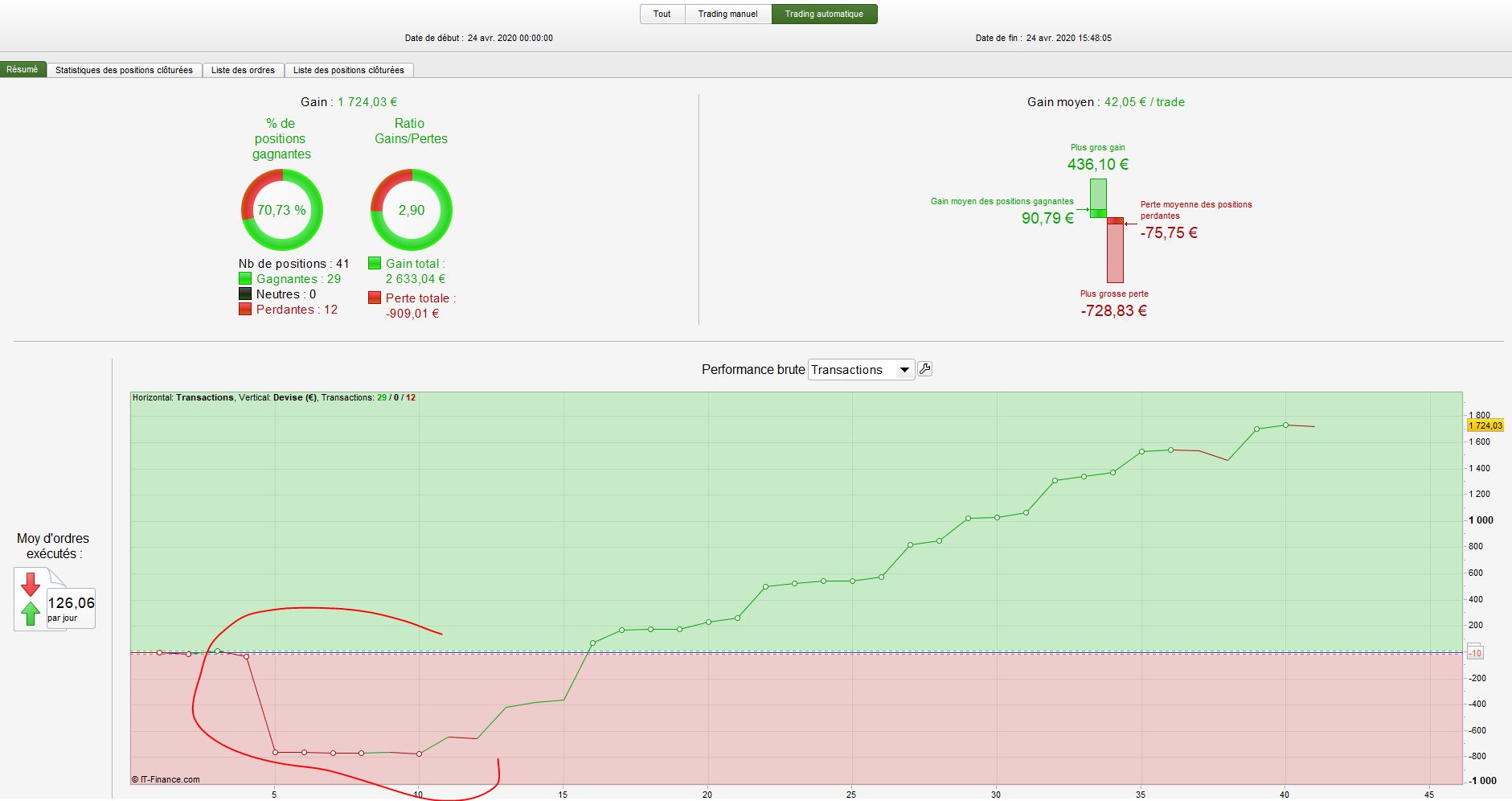

Bilan du jour, après modif de mes 3 algos candle ..

bon, petite truc que je dois régler, un des algos pendant les bougies daily qui deviennent indécises durant la journée, l’algo fait systématique 3 à 4 pertes puis de nouveau gain… faut encore des trades dans le mois pour confirmer ce biais.. … sinon je vais gérer ca simplement en diminuant le pos size dès qu’il commence à perdre

la version pullback prend short après comptage des red sur 1s.. je vais introduire le comptage des bougies petites mèches ou grandes mèches pour vérifier. Si indécision, je prends pas le short..

Tiens, ca faisait longtemps… il ne m’a pas pris mon image en upload… arff

et c’est pas mal ,

tu fini dans le vert c’est le principale

et c’est pas mal ,

tu fini dans le vert c’est le principale

Attends Fifi, la journée est pas terminée 🙂