Alco

AlcoParticipant

Senior

Hi guys,

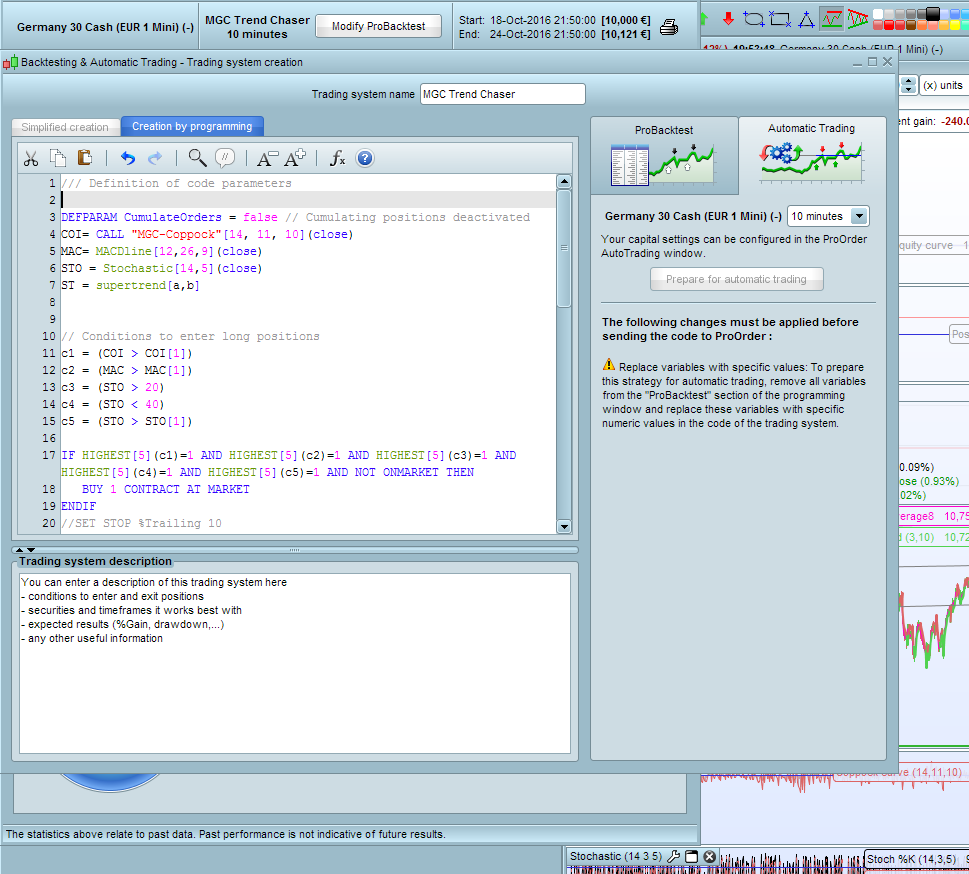

I’ve a problem with testing MGC Trend Chaser in demo. This is the code I am using:

/// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

COI= CALL "MGC-Coppock"[14, 11, 10](close)

MAC= MACDline[12,26,9](close)

STO = Stochastic[14,5](close)

ST = supertrend[a,b]

// Conditions to enter long positions

c1 = (COI > COI[1])

c2 = (MAC > MAC[1])

c3 = (STO > 20)

c4 = (STO < 40)

c5 = (STO > STO[1])

IF HIGHEST[5](c1)=1 AND HIGHEST[5](c2)=1 AND HIGHEST[5](c3)=1 AND HIGHEST[5](c4)=1 AND HIGHEST[5](c5)=1 AND NOT ONMARKET THEN

BUY 1 CONTRACT AT MARKET

ENDIF

//SET STOP %Trailing 10

// Conditions to exit long positions

//c6 = (COI< COI[1])

//c7 = (MAC< MAC[1])

//c8 = (STO < 80)

//c9 = (STO > 60)

//c10 = (STO < STO[1])

//IF HIGHEST[5](c6)=1 AND HIGHEST[5](c7)=1 AND HIGHEST[5](c8)=1 AND HIGHEST[5](c9)=1 AND HIGHEST[5](c10)=1 THEN

IF Close CROSSES UNDER ST THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

c11 = (COI< COI[1])

c12 = (MAC< MAC[1])

c13 = (STO < 80)

c14 = (STO > 60)

c15 = (STO < STO[1])

IF HIGHEST[5](c11)=1 AND HIGHEST[5](c12)=1 AND HIGHEST[5](c13)=1 AND HIGHEST[5](c14)=1 AND HIGHEST[5](c15)=1 AND NOT ONMARKET THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//SET STOP %Trailing 10

// Conditions to exit short positions

//c16 = (COI> COI[1])

//c17 = (MAC> MAC[1])

//c18 = (STO > 20)

//c19 = (STO < 40)

//c20 = (STO > STO[1])

//IF HIGHEST[5](c16)=1 AND HIGHEST[5](c17)=1 AND HIGHEST[5](c18)=1 AND HIGHEST[5](c19)=1 AND HIGHEST[5](c20)=1 THEN

IF close CROSSES OVER ST THEN

EXITSHORT AT MARKET

ENDIF

I’m getting the following error (see yellow triangle in pdf).

I do not understand what to change in the code. Could someone help me?

Thanks,

Alco

You have not defined variables a and b.

ST = supertrend[a,b]

AlcoParticipant

Senior

@arcane,

I think I need probuilder for that, or I don’t understand how to define them. I can not change the code for some reason.

Is it maybe possible to give me the code where you define st?

Kind regards,

Alco

Good work! How is the code going inProOrder?

AlcoParticipant

Senior

Hi Mike,

I tested in backtest the PRT code written in my first post. I got great results each day. I only tested it day by day. I had the best results in 10 min charts. So I wanted to test it in demo and got the error. I noticed that I used the wrong code. The code without MM. So I replaced it with this code

/// Definition of code parameters

defparam preloadbars = 3000

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

COI= WEIGHTEDAVERAGE[14](ROC[11] +ROC[10])

MAC= MACDline[12,26,9]

STO = Stochastic[14,5]

once RRreached = 0

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 5 //whole account risk in percent%

amount = 1 //lot amount to open each trade

rr = rr //risk reward ratio (set to 0 disable this function)

//dynamic step grid

minSTEP = 5 //minimal step of the grid

maxSTEP = 20 //maximal step of the grid

ATRcurrentPeriod = 5 //recent volatility 'instant' period

ATRhistoPeriod = 100 //historical volatility period

ATR = averagetruerange[ATRcurrentPeriod]

histoATR= highest[ATRhistoPeriod](ATR)

resultMAX = MAX(minSTEP*pipsize,histoATR - ATR)

resultMIN = MIN(resultMAX,maxSTEP*pipsize)

gridstep = (resultMIN)

// Conditions to enter long positions

c1 = (COI > COI[1])

c2 = (MAC > MAC[1])

c3 = (STO > 20)

c4 = (STO < 40)

c5 = (STO > STO[1])

// Conditions to enter short positions

c11 = (COI< COI[1])

c12 = (MAC< MAC[1])

c13 = (STO < 80)

c14 = (STO > 60)

c15 = (STO < STO[1])

//first trade whatever condition

if NOT ONMARKET AND HIGHEST[5](c1)=1 AND HIGHEST[5](c2)=1 AND HIGHEST[5](c3)=1 AND HIGHEST[5](c4)=1 AND HIGHEST[5](c5)=1 then //close>close[1]

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND HIGHEST[5](c11)=1 AND HIGHEST[5](c12)=1 AND HIGHEST[5](c13)=1 AND HIGHEST[5](c14)=1 AND HIGHEST[5](c15)=1 then //close<close[1]

SELLSHORT amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep*pipsize then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize

//actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*sd

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//GRAPH floatingprofit as "float"

//GRAPH RRreached as "rr"

//GRAPH floatingprofit as "floating profit"

//GRAPH BBfloatingprofit as "BB Floating Profit"

//GRAPH positionprice-mindistancetoclose

//GRAPH moneyrisk

//GRAPH onepointvaluebasket

//GRAPH gridstep

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

EXITSHORT AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

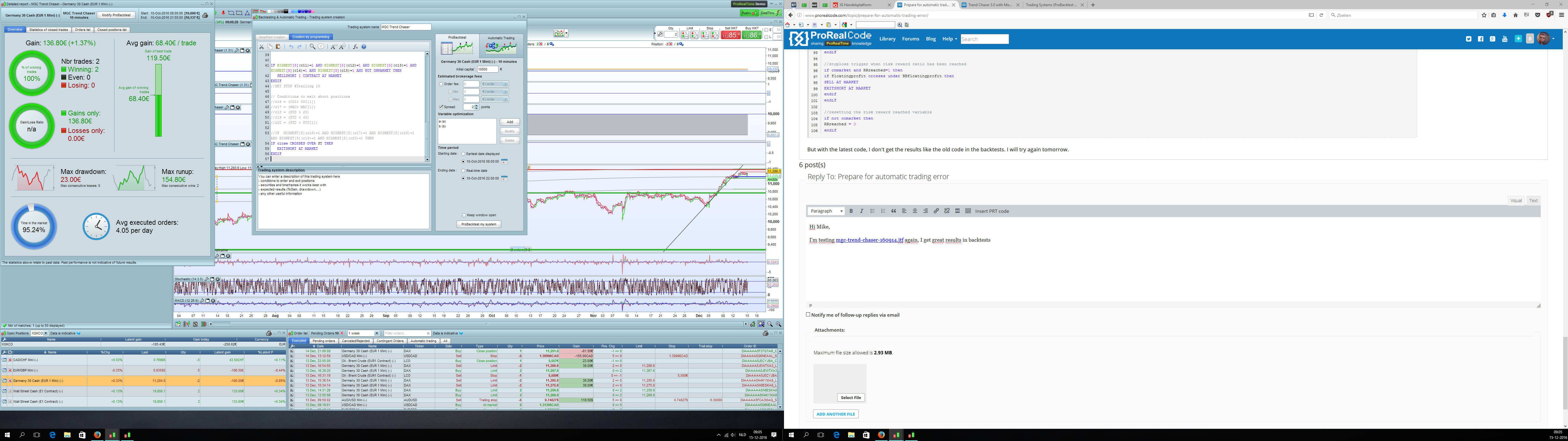

But with the latest code, I don’t get the results like the old code in the backtests. I will try again tomorrow.

AlcoParticipant

Senior

Hi Mike,

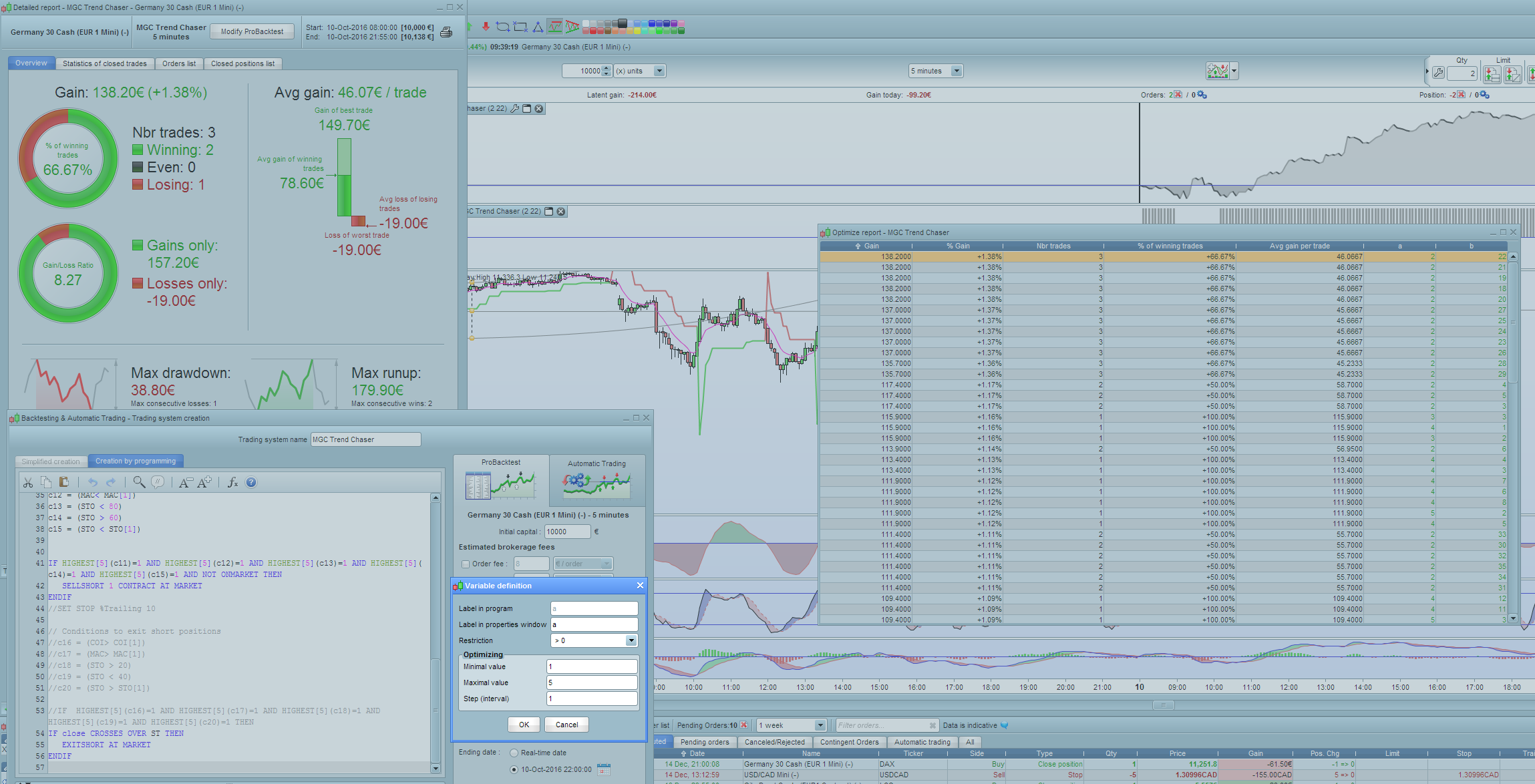

I’m testing mgc-trend-chaser-160914.itf again, I get great results in backtests for each day. But I know, before I can try it in demo, I need to optimize the supertrend variable a,b. But when I optimize the variable, like 1,4 or 2,8. Whatever I do, the results are not as good as before the optimizing. What configuration do I need, to get the same results if I optimize the supertrend for demo?

AlcoParticipant

Senior

I think the program uses the default setting before defining variable a,b. Please correct me if im wrong.

AlcoParticipant

Senior

I see an optimize report to define a,b. minimal and maximal value for a = 1-5 and 1-40 for b. So it is never possible to replicate the backtests because you only could choose 1 minimal and 1 maximal value?

Sorry but I don’t understand your problem 🙂

Once you have found the optimised parameters that suit your needs (best results, low drawdown, etc.), you’ll have to write it directly into the code and delete the optimisation variables of the probacktest window.

In any case, the variables values that are set into the code are priority to the ones of the optimisation variables window.

AlcoParticipant

Senior

Ok I try to explain it again Nicolas,

The first thing I did was testing this code

/// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

COI= CALL "MGC-Coppock"[14, 11, 10](close)

MAC= MACDline[12,26,9](close)

STO = Stochastic[14,5](close)

ST = supertrend[a,b]

// Conditions to enter long positions

c1 = (COI > COI[1])

c2 = (MAC > MAC[1])

c3 = (STO > 20)

c4 = (STO < 40)

c5 = (STO > STO[1])

IF HIGHEST[5](c1)=1 AND HIGHEST[5](c2)=1 AND HIGHEST[5](c3)=1 AND HIGHEST[5](c4)=1 AND HIGHEST[5](c5)=1 AND NOT ONMARKET THEN

BUY 1 CONTRACT AT MARKET

ENDIF

//SET STOP %Trailing 10

// Conditions to exit long positions

//c6 = (COI< COI[1])

//c7 = (MAC< MAC[1])

//c8 = (STO < 80)

//c9 = (STO > 60)

//c10 = (STO < STO[1])

//IF HIGHEST[5](c6)=1 AND HIGHEST[5](c7)=1 AND HIGHEST[5](c8)=1 AND HIGHEST[5](c9)=1 AND HIGHEST[5](c10)=1 THEN

IF Close CROSSES UNDER ST THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

c11 = (COI< COI[1])

c12 = (MAC< MAC[1])

c13 = (STO < 80)

c14 = (STO > 60)

c15 = (STO < STO[1])

IF HIGHEST[5](c11)=1 AND HIGHEST[5](c12)=1 AND HIGHEST[5](c13)=1 AND HIGHEST[5](c14)=1 AND HIGHEST[5](c15)=1 AND NOT ONMARKET THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//SET STOP %Trailing 10

// Conditions to exit short positions

//c16 = (COI> COI[1])

//c17 = (MAC> MAC[1])

//c18 = (STO > 20)

//c19 = (STO < 40)

//c20 = (STO > STO[1])

//IF HIGHEST[5](c16)=1 AND HIGHEST[5](c17)=1 AND HIGHEST[5](c18)=1 AND HIGHEST[5](c19)=1 AND HIGHEST[5](c20)=1 THEN

IF close CROSSES OVER ST THEN

EXITSHORT AT MARKET

ENDIF

Results where great in 5min and 10min time frames. But to use it in demo I got an error, because I didnt define: ST= supertrend [a,b]

After defining a and b, the results are bad. So I want to create the same results before the optimization.

Hi @Alco,

Sorry I have been off the air since early December.

The a and b variable are for optimising. I suggest you set ‘a’ at 1 to 10 with 2 step and ‘b’ at 5 to 40 with 5 step for faster optimisation. If the final results are close to either beginning or end, then adjust the variables until the result is somewhere in the middle of your beginning and end variables.

The next problem is that you have to have the MGC-Coppock defined in your platform so it can be called from your code. Better to substitute this for it “COI= WEIGHTEDAVERAGE[14](ROC[11] +ROC[10])”.

Now a word of warning, both codes with and without money management are quite complex with lots of variables. If you get a spectacular result in back-testing, it does not mean that you will get the same result in ProOrder. You need to forward test in ProOrder in demo mode for some time to be sure the code will produce a satisfactory result when run live.

If you read @cfta posts, you will find a good strategy for running ProOrder live.

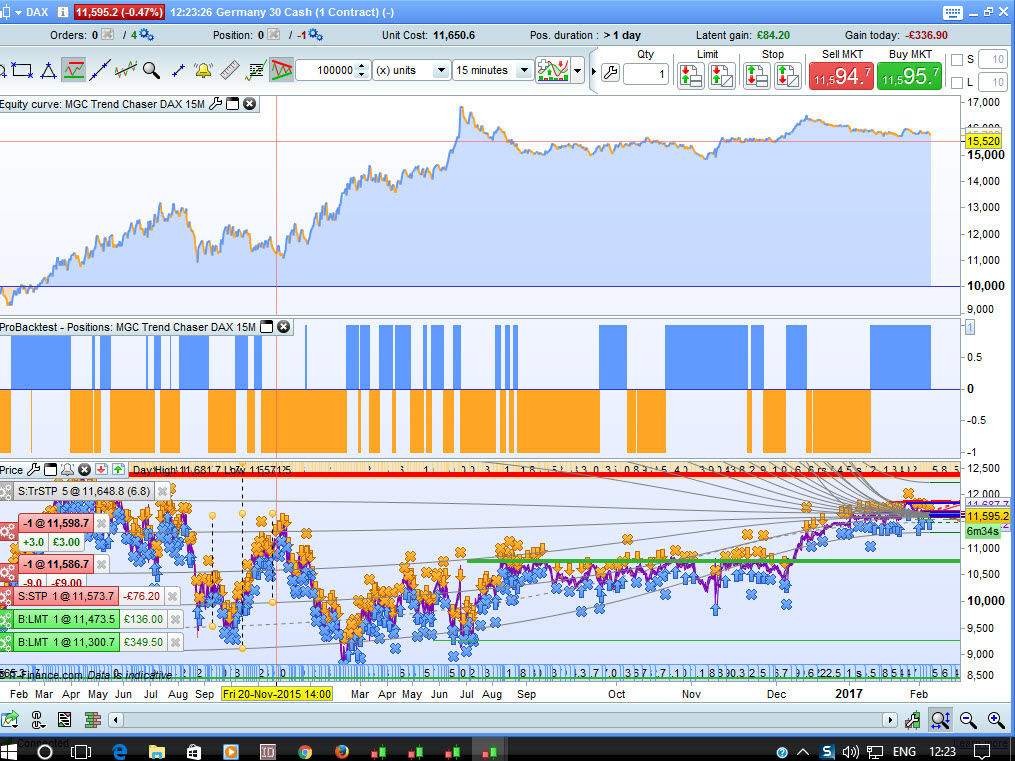

Hi Alco

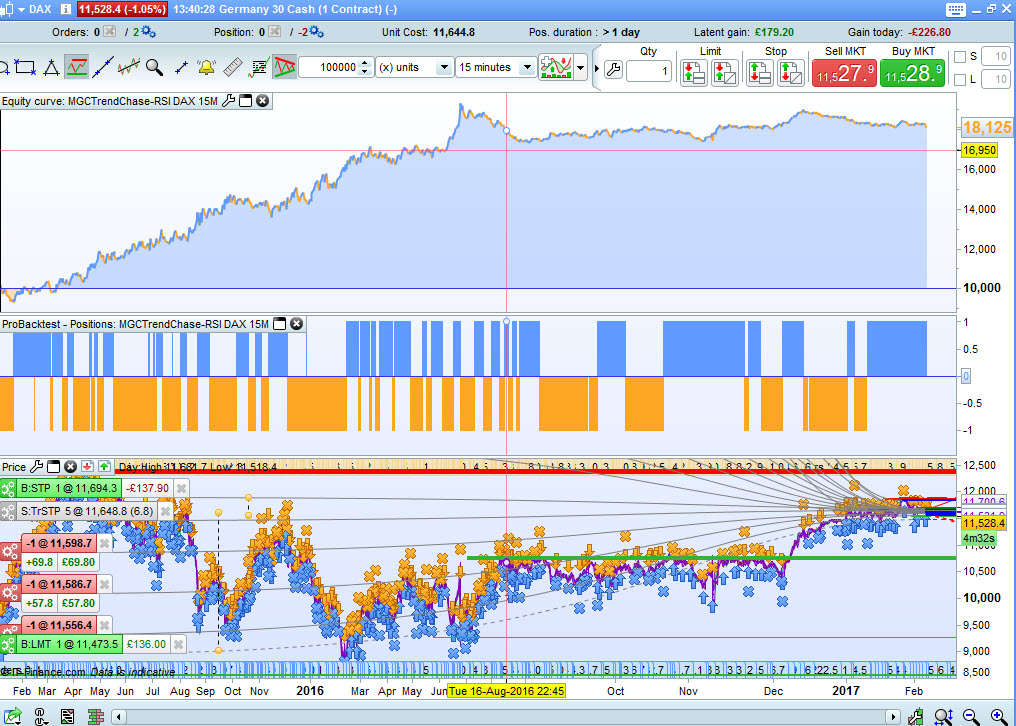

I note you say … I get great results in backtests for each day … and then you say you … results are not as good as before the optimizing? Also you provide a screen shot with good results for 1 day.

I’m confused, but would like to help, I hope I learn something while helping. I’m sure you know … if you optimise for 1 day then those optimised values will give highest profit that day or another day exactly the same (maybe never happen.).

Anyway, I couldn’t resist so attached is 100000 x 15M @ spread 2 on DAX with values ST = supertrend[6,25]. I’m setting it going on Demo Forward test right now.

Cheers

GraHal

Edit: Attached MGC 2 with better curve / more profit using code with the following amendments

(Apologies Mods, Insert PRT Code button not visible)

IF Close CROSSES UNDER ST or RSI[14](close) < 22 THEN

SELL AT MARKET

ENDIF

IF close CROSSES OVER ST or RSI[14](close) > 74 THEN

EXITSHORT AT MARKET

ENDIF

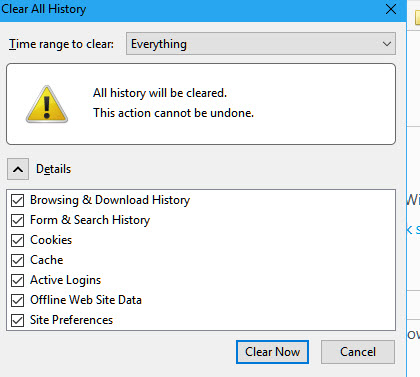

@GraHal, what is your computer screen resolution please? the button is not available below a certain proportion to avoid problem with mobile/tablet…

Hi Nicolas

Due to not wanting to wear glasses and to give large font / text size … my screen resolution is 1024 x 768.

I can see the insert PRT button if I clear everything out as attached, but if I have loads of tabs open on other tasks then I not want to ‘clear all’ at that point.

I just deleted ‘all cookies associated with this PRC site’ (only) and I then had to log back in, but still the Inser PRT Code is not visible.

Cheers

GraHal