Hi, Please can somebody point me in the right direction, I would like code to pause the system till next open when a loss is booked after a stoploss is hit, Thanks.

There you go:

Once TradeON = 1

If TradeON = 0 then

TradeON = 1

Endif

If StrategyProfit < StrategyProfit[1] then

TradeON = 0

Endif

.

.

If MyLongConditions and TradeON Then

Buy 1 Contract at Market

Endif

.

.

If MyShortConditions and TradeON Then

Buy 1 Contract at Market

Endif

.

.

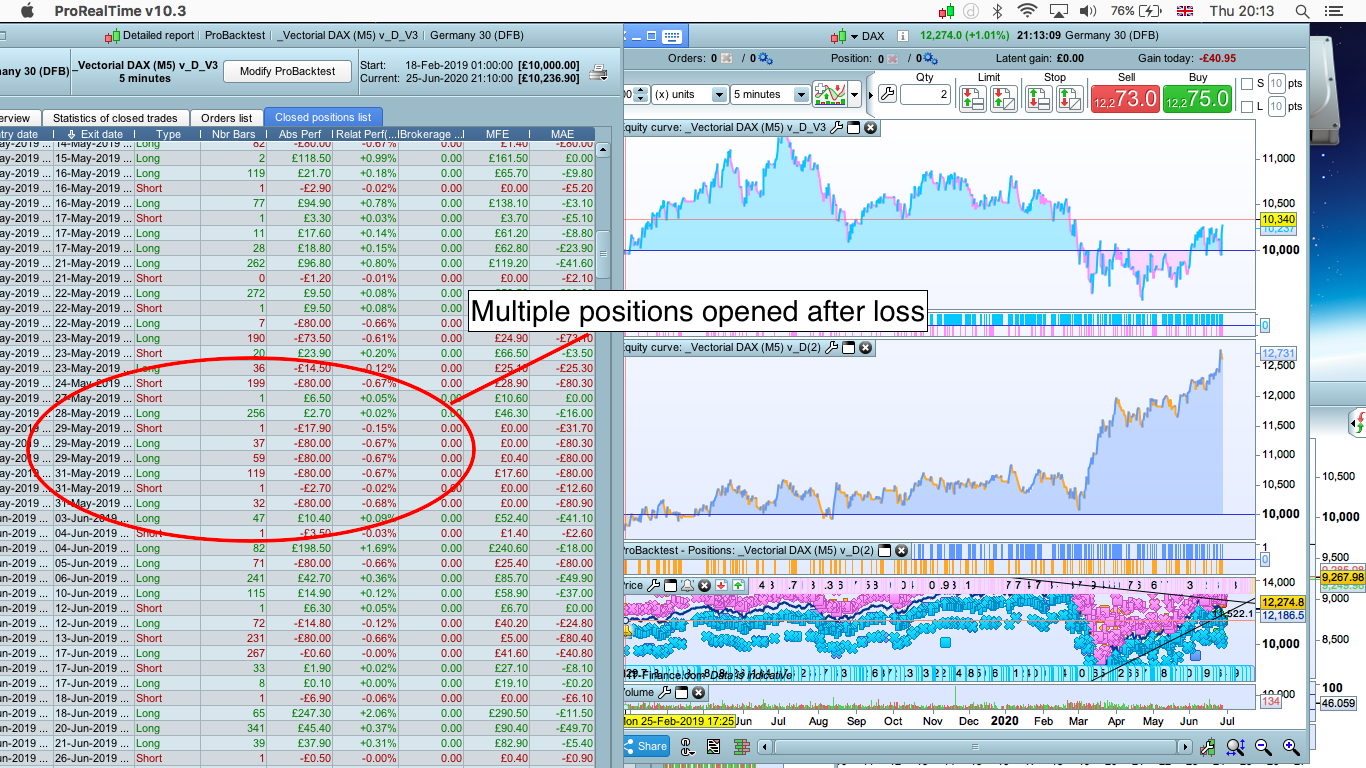

Hi Robert,

I made an attempt at inserting the code but it is not performing as expected still multiple losses on same day. D2 is the original equity curve before code was inserted please take a look at the code thanks.

// M5

// SPREAD 1.5

// by BALMORA 74 – FEBRUARY 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//VARIABLES

CtimeA = time >= 080000 and time <= 180000

CtimeB = time >= 080000 and time <= 180000

// TAILLE DES POSITIONS

ONCE PositionSizeLong = 1

ONCE PositionSizeShort = 1

//STRATEGIE

//VECTEUR = CALCUL DE L’ANGLE

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CondBuy1 = ANGLE >= 45

CondSell1 = ANGLE <= – 37

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 20

ONCE nbChandelierB = 35

lag = 5

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CondBuy2 = (pente > trigger) AND (pente < 0)

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

Once TradeON = 1

If TradeON = 0 then

TradeON = 1

Endif

If StrategyProfit < StrategyProfit[1] then

TradeON = 0

Endif

If condbuy and TradeON Then

Buy 1 Contract at Market

Endif

If condsell and TradeON Then

Buy 1 Contract at Market

Endif

//ENTREES EN POSITION

CONDBUY = CondBuy1 and CondBuy2 and CTimeA

CONDSELL = CondSell1 and CondSell2 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSizeLong contract at market

SET STOP %LOSS 1.3

SET STOP pLOSS 80

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSizeShort contract at market

SET STOP %LOSS 1.3

SET STOP pLOSS 80

ENDIF

//VARIABLES STOP SUIVEUR

ONCE trailingStopType = 1 // Trailing Stop – 0 OFF, 1 ON

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//———————————————-

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE – MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

IF ONMARKET AND DAYOFWEEK=5 AND TIME>=210000 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

You asked to wait 1 bar, that’s what it’s doing.

If you want to pause the whole day then replace line 2 of my code with

If IntraDayBarIndex = 0 then

Please, always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read.

Thank you 🙂

// ROBOT VECTORIAL DAX

// M5

// SPREAD 1.5

// by BALMORA 74 - FEBRUARY 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//VARIABLES

CtimeA = time >= 080000 and time <= 180000

CtimeB = time >= 080000 and time <= 180000

// TAILLE DES POSITIONS

ONCE PositionSizeLong = 1

ONCE PositionSizeShort = 1

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CondBuy1 = ANGLE >= 45

CondSell1 = ANGLE <= - 37

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 20

ONCE nbChandelierB = 35

lag = 5

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CondBuy2 = (pente > trigger) AND (pente < 0)

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

Once TradeON = 1

IF IntraDayBarIndex = 0 THEN

TradeON = 1

Endif

If StrategyProfit < StrategyProfit[1] then

TradeON = 0

Endif

If CONDBUY and TradeON Then

Buy 1 Contract at Market

Endif

If CONDSELL and TradeON Then

Buy 1 Contract at Market

Endif

//ENTREES EN POSITION

CONDBUY = CondBuy1 and CondBuy2 and CTimeA and TradeON

CONDSELL = CondSell1 and CondSell2 and CtimeB and TradeON

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSizeLong contract at market

SET STOP %LOSS 1.3

SET STOP pLOSS 80

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSizeShort contract at market

SET STOP %LOSS 1.3

SET STOP pLOSS 80

ENDIF

//VARIABLES STOP SUIVEUR

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

IF ONMARKET AND DAYOFWEEK=5 AND TIME>=210000 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

Hi Robert, Thanks I made the suggested replacement and I am still getting subsequent trades opening that day, thanks for your help.

You did not add TradeON to your conditions (line 10 and 15 in my code).

Add it to your lines 67 and 75.

My first code was made to wait ONE bar, while my next suggestions was to wait ONE day (till new day opens).

The code still dont work.

It’s beacause STRATEGYPROFIT (like ONMARKET, etc…) take a bar to be able to update its status, so when you do Stop & Reverse ProOrder can’t know whether there was a gain or a loss.

To achieve the correct result you should add

and Not OnMarket

to your conditions to enter a trade.

In case you want to do Stop & Reverse you need to take note of that and accept that you will probably suffer TWO losses before there’s a temporary stop.

At line 52 and 57 you always use BUY both for long and short conditions, is that intentional?

Ok Roberto, el código es bueno, thanks.

But, other problem.

If cumulateórders = true, the Code no function.

If you use and Not OnMarket it will not work!