Hi everyone, after taking a break for a while, I’m back to jot down a few more ideas during my free time. Since I’m a bit rusty, I would like some help in converting some elements into a code that I will then assemble and share with you if it’s decent.

First code: Identify an increase/decrease of x percent in a stock during the past y days;

Second code: Enter short during the breakdown of the opening range low if the candle is red/Enter long during the breakout of the opening range high if the candle is green;

Third code: Open a position when the price, after crossing over or under the VWAP, fails and bounces back.

Thanks!

JS

JSParticipant

Veteran

Hi @Francesco,

Here is the first code…

Period = y //y days

Gain = x // x%

Increase = 0

Decrease = 0

If (Close - Close[y]) / Close[y] * 100 >= x then

Increase = 1

ElsIf (Close - Close[y]) / Close[y] * 100 <= x then

Decrease = 1

EndIf

JSParticipant

Veteran

If (Close – Close[y]) / Close[y] * 100 >= x then

Increase = 1

ElsIf (Close – Close[y]) / Close[y] * 100 <= –x then

Decrease = 1

EndIf

I suggest to modify the code as follows, to make sure both variables are always different:

If (Close – Close[y]) / Close[y] * 100 >= x then

Increase = 1

Decrease = 0

ElsIf (Close – Close[y]) / Close[y] * 100 <= –x then

Increase = 0

Decrease = 1

EndIf

Thank you guys!

For the second request, could something like this work? (the time refers to NASDAQ opening hours)

// Entry Conditions

if time>= 153000 and time <= 153500 then

if time= 153000 then

dailyhigh= high

dailylow= low

endif

if high> dailyhigh then

dailyhigh= high

endif

if low< dailylow then

dailylow = low

endif

endif

cl= close crosses over dailyhigh

cs= close crosses under dailylow

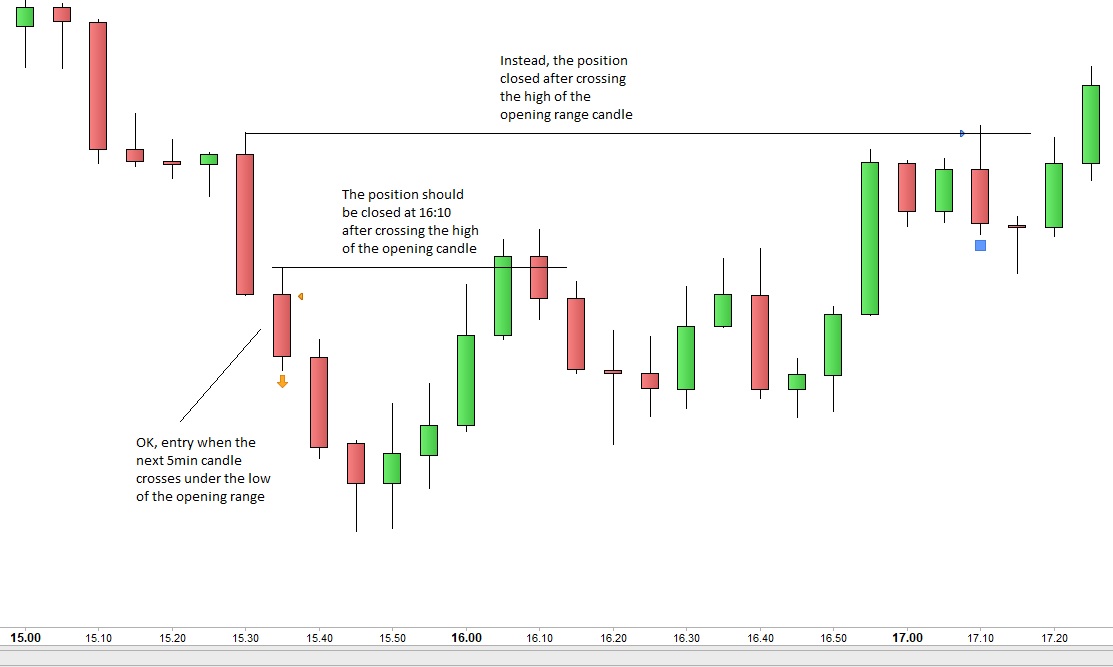

Seems not to work properly… i’ll explain better with the attached image, an example of a long setup.

Is this possible to code?

JSParticipant

Veteran

When I use Time >=153000 the high and Low of the previous candle is used, hence Time >= 153500…

DefParam CumulateOrders=False

TimeFrame(5 minutes, UpDateOnClose)

Once HighEntry=0

Once LowEntry=0

If Time >= 153500 and Time <= 154000 and NOT OnMarket then

If Time = 153500 then

HighEntry = High

LowEntry = Low

EndIf

If (HighEntry + LowEntry) <> 0 then

Buy 1 contract at HighEntry STOP

SellShort 1 contract at LowEntry STOP

EndIf

EndIf

It seems to open the positions correctly now! But i’m still missing on how to put the stop loss on the high/low of the entry candle.

Also in your example

@js the postion should be closed at 15:55 after crossing under the low of the entry candle.

Any suggestion? Current code version below:

// Entry Conditions

once highentry=0

once lowentry=0

if time= 153000 then

highentry=high

lowentry=low

endif

cl=close crosses over highentry

cs=close crosses under lowentry

// Time Conditions

t=time>=153500 and time< 154000

// Enter Long

if not onmarket and cl and t then

buy n contract at market

endif

// Enter Short

if not onmarket and cs and t then

sellshort n contract at market

endif

I implemented the following code and it seems that i’m getting closer

// Entry Conditions

if time=153000 then

highentry=high

lowentry=low

endif

cl=close crosses over highentry

cs=close crosses under lowentry

// Time Conditions

t=time>=153500 and time<154000

// Stop Loss Conditions

sll=abs(close-low)

sls=abs(close-high)

// Enter Long

if not onmarket and cl and t then

buy n contract at market

set stop loss sll

endif

// Enter Short

if not onmarket aand cs and t then

sellshort n contract at market

set stop loss sls

endif

But as you can see in the image attached, the position is closed when crossing the high of the opening range candle and not when crossing the high of the candle where the position was opened

Ok i think i managed to solve the issue changing with:

// Stop Loss Conditions

sll=abs(close[2]-low)

sls=abs(close[2]-high)

But looking at the backtests, putting the stop loss on the high/low of the opening range candle (so at the daily high/low) instead of the candle where the position was opened (as i wanted to during last posts) seems more effective for gains.

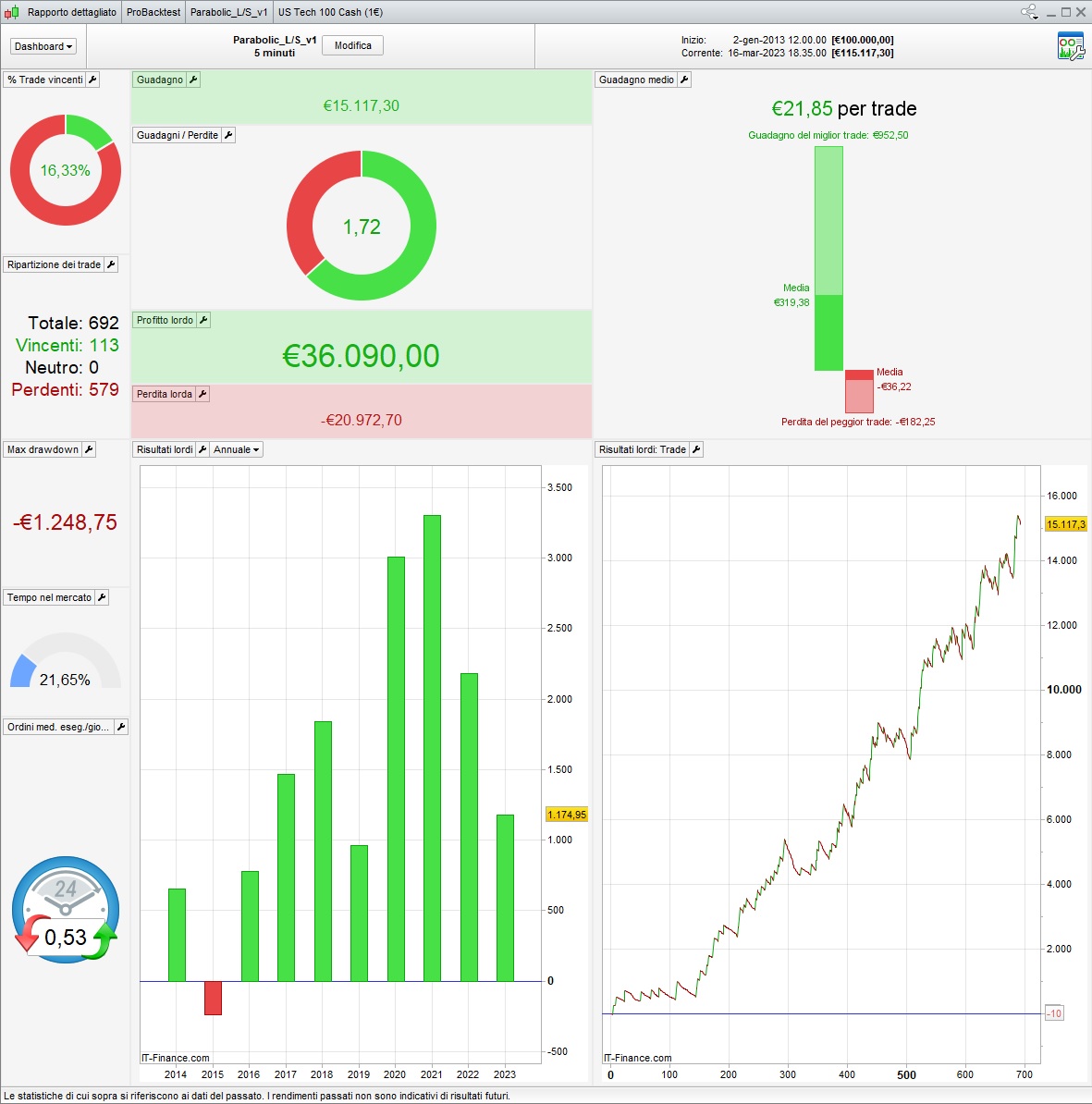

Below the first version of the system (i’m still figuring out if it’s necessary to implement the VWAP condition) on NASDAQ 5M – 1.5 Contracts (939€ atm)

// Parabolic Long/Short v1 by Francesco

// ProRealCode.com - 20230316

// NASDAQ - 5M

// Setup

defparam cumulateorders=false

n=1.5

once long=1

once short=1

timeframe (1 day)

// Filter

x=3

if (close-close[1])/close*100>=x then

increase=1

decrease=0

elsif (close-close[1])/close*100<=-x then

increase=0

decrease=1

endif

timeframe (default)

// Entry Conditions

if time=153000 then

highentry=high

lowentry=low

endif

cl=close crosses over highentry

cs=close crosses under lowentry

// Time Conditions

t=time>=153500 and time<154000

// Stop Loss Conditions

sll=abs(close-low)

sls=abs(close-high)

// Enter Long

if long then

if not onmarket and decrease=1 and cl and t then

buy n contract at market

set stop loss sll

endif

endif

// Enter Short

if short then

if not onmarket and increase=1 and cs and t then

sellshort n contract at market

set stop loss sls

endif

endif

// Trailing Stop

trailingstart=200

trailingstep=5

If not onmarket then

newsl=0

endif

if longonmarket then

if newsl=0 and close-tradeprice(1)>=trailingstart*pipsize then

newsl=tradeprice(1)+trailingstep*pipsize

endif

if newsl>0 and close-newsl>=trailingstep*pipsize then

newsl=newSL+trailingstep*pipsize

endif

endif

if shortonmarket then

if newsl=0 and tradeprice(1)-close>=trailingstart*pipsize then

newsl=tradeprice(1)-trailingstep*pipsize

endif

if newsl>0 and newSL-close>=trailingstep*pipsize then

newsl=newsl-trailingstep*pipsize

endif

endif

if newsl>0 then

sell at newsl stop

exitshort at newsl stop

endif

Few details about the system:

- Entirely based on price action

- Pretty easy to optimize (just 1 value to edit)

- No optimization needed for stop loss, just play with the trailing stop

- Running just the Long version drastically decreases drawdown but generates less gains

Please find attached a 10y backtest; feel free to give your contribution