Is that with 6m in the top TF?

6 months?

Yes back to 17 Oct 2019.

if it didn’t keep crashing on me.

Have you exported those 300 Systems from the backtest window yet??

My platform used to crash loads, but hasn’t for as long as I can remember … well perhaps once in 12 months! 🙂

6 months?

No, 6 minutes, in the other TF? or is it all set to default?

I cleared about half, but it’s so tedious. Now I’m cursing for not being able to export them all at once. We’re just moving a bunch of files, can’t see why it has to be one at a time.

can’t see why it has to be one at a time

I agree … it’s like stepping back in time to when computers were unfriendly!?

Wait until you try and clear the Auto-Trading window … it’s even worse … Copy, paste into backtesting window, add the title then save THEN export!!!

Pity PRT don’t sort it so ALL .itf’s are stored on a central repository then we can access from any Account … Real and Demo SB and CFD etc.

These are the sort of things I was hoping would be a feature of v11 but it seems not!? Loads of bells and whistles, but not much that make our lives easier??

No, 6 minutes, in the other TF?

Ha! The other Timeframe is / was already at default … I’m sure I only set the 10 seconds to default.

I just downloaded the file I posted. Does yours look like this?

TIMEFRAME(1 minutes)// try 2 or 3x default TF

ST1 = SuperTrend[3,10]

cnd1 = (close > ST1)

cnd2 = (close < ST1)

mx1 = average[25,7](close)

cnd3 = mx1 > mx1[1]

cnd4 = mx1 < mx1[1]

TIMEFRAME(default)

ST2 = SuperTrend[3,10]

cnd5 = (close > ST2)

cnd6 = (close < ST2)

If you want to run it at 2min prob better results changing the 1min to 6min … or wait a couple of days and I’ll try to post something that’s actually made for 2m.

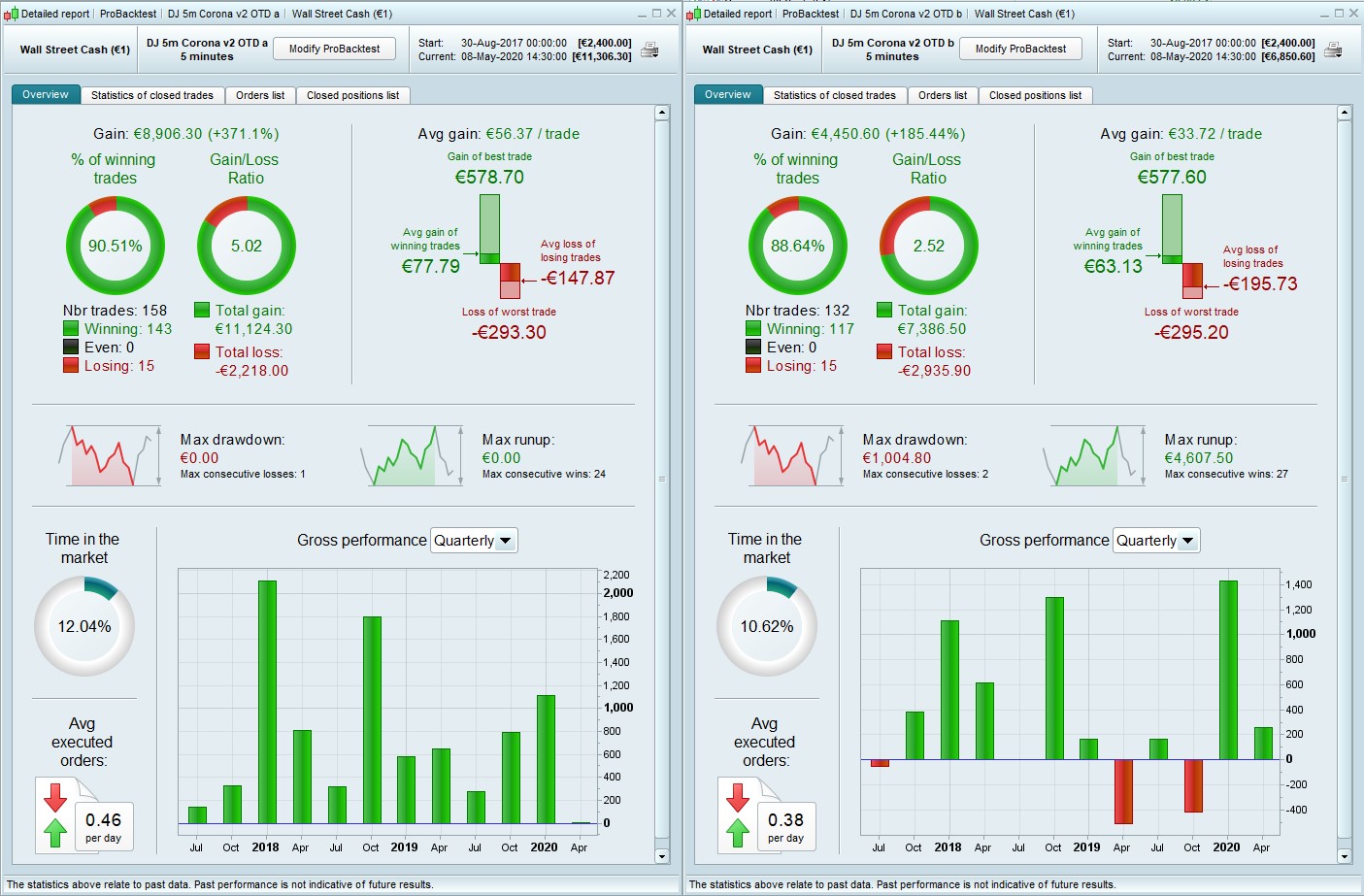

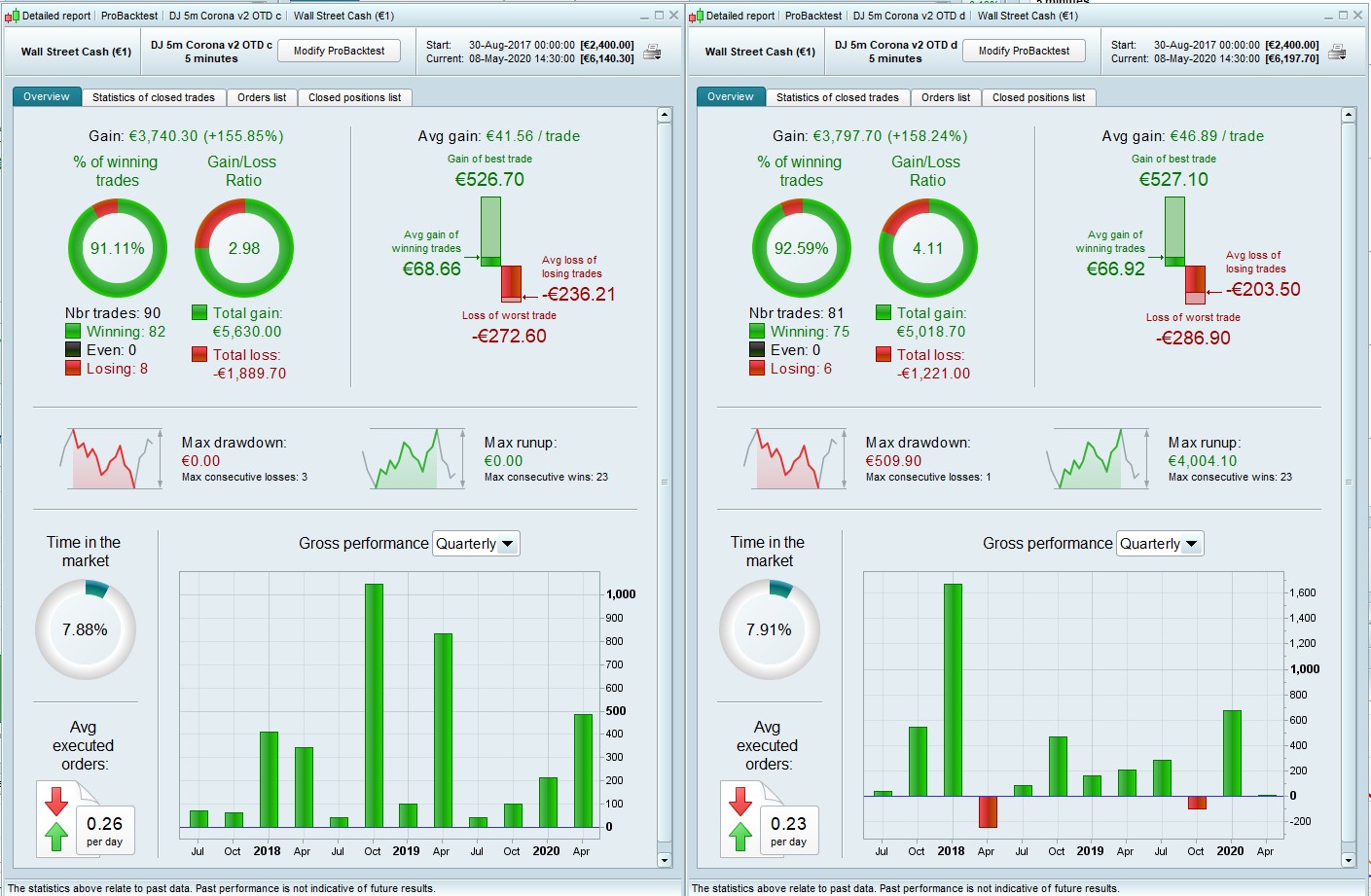

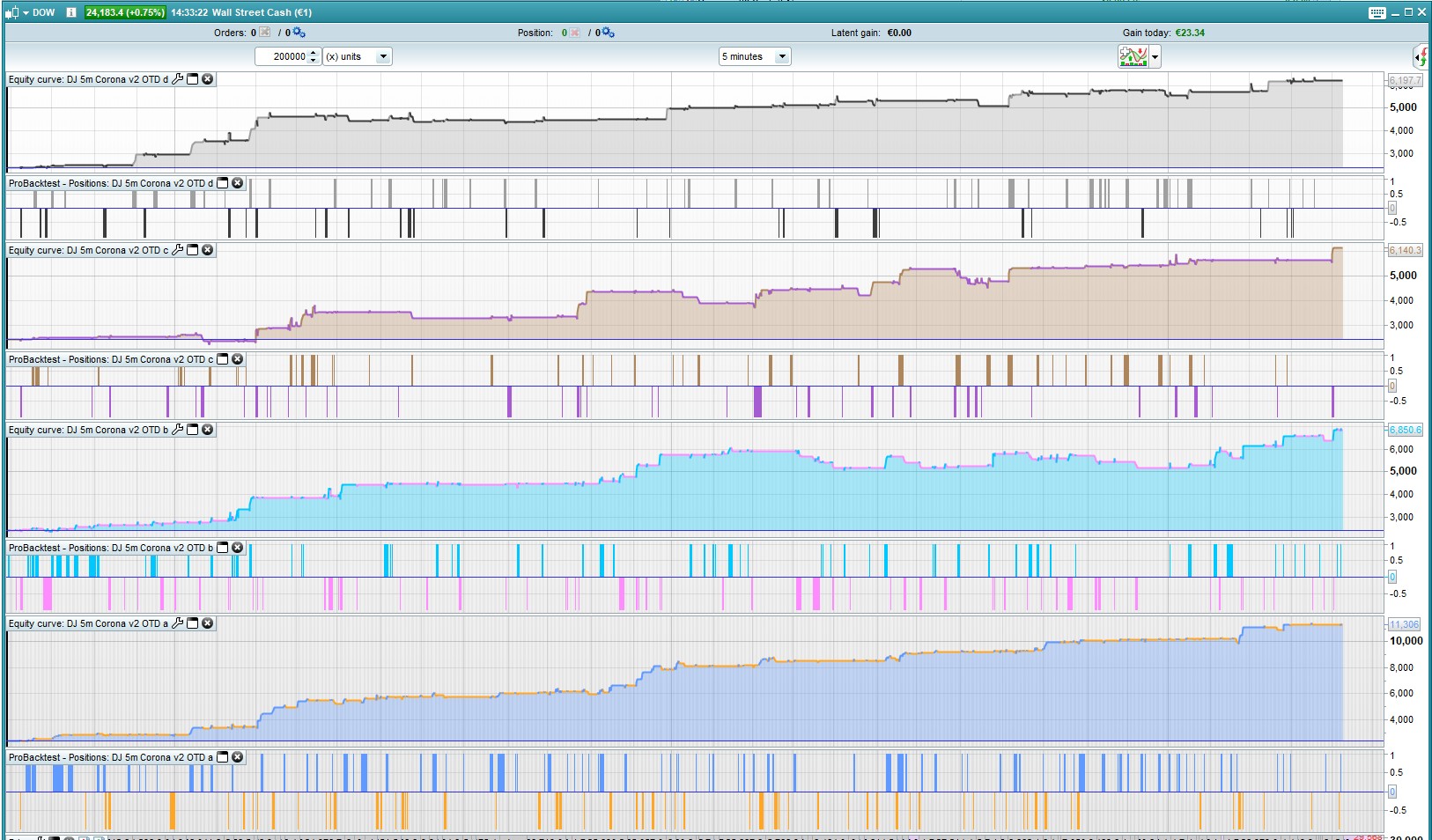

New improved DJ 5m Corona … just when you thought it was safe to go outside. Exchanged one Supertrend for Parabolic SAR, added Hull MA.

I have been steadily trying to avoid the temptation to optimise everything. For years I tried to optimise my wife. You can imagine how well that went. So this version has precisely zero optimisation. All the values were set in advance, either at traditional defaults, or because they seem sensible regardless of the curve. The only variation is the crossing pair of MAs, as selected by @Jan’s program. Everything else stays the same, 4 variations each doing one trade per day. No idea if this makes sense theoretically, but so far the numbers look good.

The trailing step is set to minimum to keep a position in play as long as poss and hopefully get to the TP. If that seems too slow then .004 (approx 1pt) also works well.

For years I tried to optimise my wife. You can imagine how well that went

Haha … it’s a pity there is no Appreciate the Joke / similar button on here as we need a bit of humour now and again!!

Wow System sounds good … minimum / nil optimisation and still in profit … this could be the one!!!!

optimising your wife actually sounds pretty creepy if you think about it too long … so let’s not.

Still working on a 2m version, also looks promising in spite of the short back test.

Sorry @nonetheless what is the difference between a b c d versions?

Also, you said they not perform good in robustness test; is the same for these new versions?

the difference between a b c d versions?

They each work in a different time slot, approx 90mins each. I thought this could be worth trying as a way of incorporating variations within one overarching concept. The results are far better than running any one of them without the OTD setting.

I didn’t even look at VRT, can’t see what I would learn by randomising an algo that makes one trade per day, and is almost never still open the next day. That is the trade you’re going to get, so I’m not too interested in the ones I cannot possibly ever get. WF is very good.

@nonetheless I missed maybe something but I did’nt get the same result on my backtests.

Even with optimisation of the 2 variables.

Did you do something else ?

Hehehe!! “For years I tried to optimise my wife…”. Lucky you! Be glad it’s not the other way around. My wife has tried to optimize me in every possible way…the result?! A Curvy non Fit man.

Anyway, keep up the good work! I really appreciate everything you Jedi-coders share with the community! (yeh, yeh…I’m a Star Wars fan, I know)…

@scooby did you change the time settings for France? + 1 hour

I really appreciate everything you Jedi-coders share with the community

More than happy to share stuff but in the spirit of full transparency, I ain’t no Jedi coder by a long chalk and wouldn’t want anyone to think I was. I’ve been day-trading for years so I know a thing or 2 about technical analysis but only started coding a few months ago. I’m just a bumbler with a lot of time on his hands. It’s guys like @Paul, @Fifi743, @JuanJ (+ all the moderators obviously) who are the true wizards here.

V best of luck! 🖖

and of course @Jan who did most of the work for this algo – thanks again!