I’ve been trying to amalgamate the codes I posted here #130635 as one itf, with cumulateorders =true and without the OTD condition, something like this:

If time >=143000 and time <160500 then

MAType = 54

MATypeV2 = 14

else

if time >=160500 and time <174500 then

MAType = 7

MATypeV2 = 36

else

if time >=174500 and time <192000 then

MAType = 2

MATypeV2 = 63

else

if time >=192000 and time <210000 then

MAType = 69

MATypeV2 = 7

endif

endif

endif

endif

Results are mixed, mainly because without the OTD (one trade per day) it allows multiple positions to be opened in each time slot. Is there a way to code this so as to have multiple positions, but max one from each time slot?

Hi, not sure but maybe something like this ?

if time=000000 then

count1=0

count2=0

count3=0

count4=0

endif

If time >=143000 and time <160500 then

MAType = 54

MATypeV2 = 14

condbuy1=... and count1=0

if condbuy1 then

buy at market

count1=count1+1

endif

else

...

Hi @Roger, is this what you meant?

if time=000000 then

count1=0

count2=0

count3=0

count4=0

endif

//conditions to enter long

If time >=143000 and time <160500 then

MAType = 54

MATypeV2 = 14

if wAFR > wAFRv2 and wAFR[1] < wAFRv2[1] and CndB and count1=0 then

buy positionsize shares AT MARKET

count1=count1+1

endif

else

If time >=160500 and time <174500 then

MAType = 7

MATypeV2 = 36

if wAFR > wAFRv2 and wAFR[1] < wAFRv2[1] and CndB and count2=0 then

buy positionsize shares AT MARKET

count2=count2+1

endif

else

If time >=174500 and time <192000 then

MAType = 2

MATypeV2 = 63

if wAFR > wAFRv2 and wAFR[1] < wAFRv2[1] and CndB and count3=0 then

buy positionsize shares AT MARKET

count3=count3+1

endif

else

If time >=192000 and time <210000 then

MAType = 69

MATypeV2 = 7

if wAFR > wAFRv2 and wAFR[1] < wAFRv2[1] and CndB and count4=0 then

buy positionsize shares AT MARKET

count4=count4+1

endif

endif

endif

endif

endif

//conditions to enter short

If time >=143000 and time <160500 then

MAType = 54

MATypeV2 = 14

if wAFR < wAFRv2 and wAFR[1] > wAFRv2[1] and CndS and count1=0 then

sellshort positionsize shares AT MARKET

count1=count1+1

endif

else

If time >=160500 and time <174500 then

MAType = 7

MATypeV2 = 36

if wAFR < wAFRv2 and wAFR[1] > wAFRv2[1] and CndS and count2=0 then

sellshort positionsize shares AT MARKET

count2=count2+1

endif

else

If time >=174500 and time <192000 then

MAType = 2

MATypeV2 = 63

if wAFR < wAFRv2 and wAFR[1] > wAFRv2[1] and CndS and count3=0 then

sellshort positionsize shares AT MARKET

count3=count3+1

endif

else

If time >=192000 and time <210000 then

MAType = 69

MATypeV2 = 7

if wAFR < wAFRv2 and wAFR[1] > wAFRv2[1] and CndS and count4=0 then

sellshort positionsize shares AT MARKET

count4=count4+1

endif

endif

endif

endif

endif

That doesn’t actually help … but probably I’ve made mistakes?

Yes thats it, im going to try to find a solution

Well, I think that the problem is that PRC does not allow to manage each trade independently (partial closure is not allowed)

Yes, I think you’re right. Even if we could get the opening right, the aggregate of positions would all be subject to the same stop loss, which won’t work.

Never mind, they work perfectly well separately. Thanks for your help.

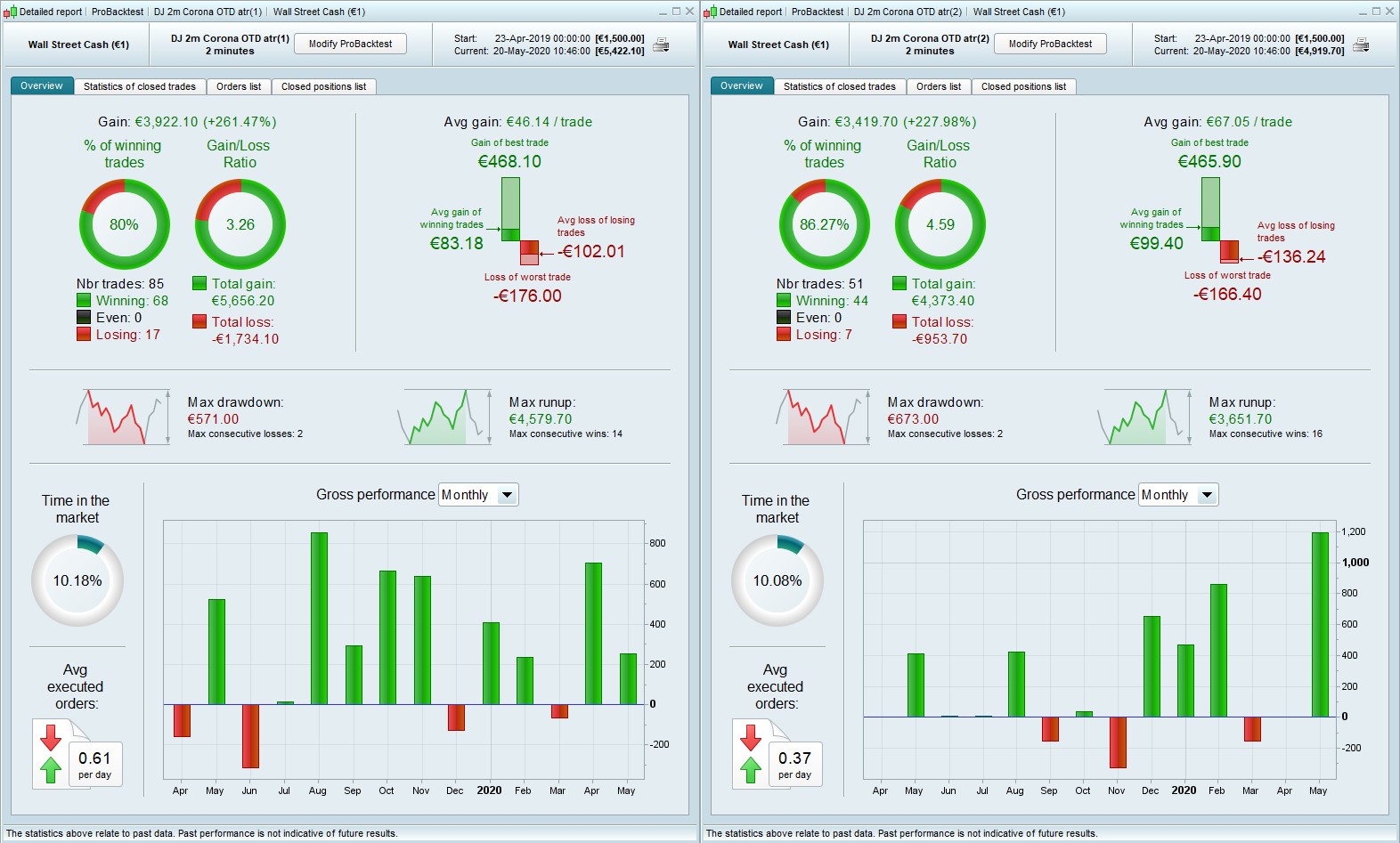

This is the 2m version of my ongoing Corona project. Like the 5m it works as one basic strategy divided into 4 separate time slots. All values are identical except for a different pair of crossing averages as thrown up by @jan’s cross-finding engine. There is no other optimisation. The 4 need to be viewed together as 1 strategy; for example the results for (3) look poor but those months are balanced by stronger performance by 1,2 and 4.

These work with a small SL of just .6% and a healthy risk/reward ratio. Unlike the 5m version, I’ve used @Paul’s ATR trail, but with a conventional break even at .1% This can be switched off, and in some cases that improves profit but with a lower Win%.

Beware that the back test here is only about 13 months. WF results were very good as you’d expect with no optimisation. There is however the possibility of a sort of reverse curve-fit, ie not that the values are adjusted to fit a particular curve but that the cross-finding engine finds a curve to fit the values you give it. No idea whether that’s better or worse ??? but for my money it seems to be worth a punt. A starting position of €.2pp means a max single loss of around €30

This can also be used as a template for other instruments, you just have to re-run the cross-finding engine for MAType

This is the code I added to @jan’s

TIMEFRAME(10 minutes)

Perioda= 20

innera = 2*weightedaverage[round( Perioda/2)](typicalprice)-weightedaverage[Perioda](typicalprice)

HULLa = weightedaverage[round(sqrt(Perioda))](innera)

cnd1 = HULLa > HULLa[1]

cnd2 = HULLa < HULLa[1]

TIMEFRAME(6 minutes)// typically 2x or 3x default TF

ST1 = SuperTrend[3,10]

cnd3 = (close > ST1)

cnd4 = (close < ST1)

Periodb= 20

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

cnd5 = HULLb > HULLb[1]

cnd6 = HULLb < HULLb[1]

TIMEFRAME(default)

ST2 = SuperTrend[3,10]

cnd7 = (close > ST2)

cnd8 = (close < ST2)

//Stochastic RSI | indicator

lengthRSI = 14 //RSI period

lengthStoch = 14 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 3 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K2 = average[smoothK](stochrsi)*100

D2 = average[smoothD](K2)

cnd9 = K2>D2

cnd10 = K2<D2

Periodc= 20

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

cnd11 = HULLc > HULLc[1]

cnd12 = HULLc < HULLc[1]

CndB = cnd1 and cnd3 and cnd5 and cnd7 and cnd9 and cnd11

CndS = cnd2 and cnd4 and cnd6 and cnd8 and cnd10 and cnd12

//Profit and Loss

SL = .6 // % STOP LOSS

TP = 1.6 //% TARGET PROFIT

Hello,

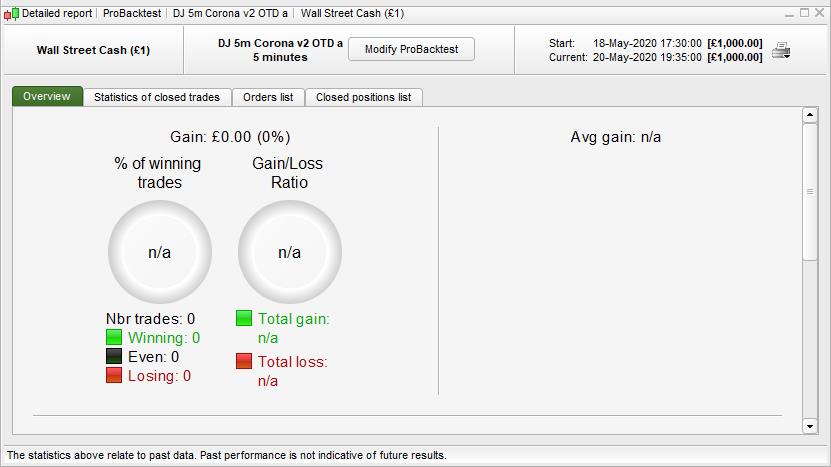

@Nonetheless, I have been trying to setup your 5m-Corona code on the Wall Street Cash (thanks for sharing!) but for some reasons my Probacktest are giving me no value. I think there might be some reasons to that:

- Based in Hong Kong so I changed the time for version “a” to: Ctime = time >=213000 and time <230000

- The minimum order quantity I can set is 0.5, so I changed: ONCE startpositionsize = 0.5, ONCE minpositionsize = 0.5

- I don’t have access to Wall Street Cash €1 but I have either Wall Street Cash £1 or Wall Street Cash $10. Not sure if you have anything in your code that specifies this market.

So I don’t see where the problem might be coming from, and I wouldn’t mind some help 🙂

Thanks

The instrument (Wall St Cash £1 or $10) is not determined in the code, it will run on any chart you launch it from. For me it runs fine with your other settings so not sure where the problem is ???

minimum order quantity I can set is 0.5

Are you sure this is the min position? If I run mine with position size €.1 then I get the same result as you (my minimum is €.2)

Try it with startpositionsize = 1

The instrument (Wall St Cash £1 or $10) is not determined in the code, it will run on any chart you launch it from. For me it runs fine with your other settings so not sure where the problem is ???

Yes that’s what I thought so all good.

minimum order quantity I can set is 0.5

Are you sure this is the min position? If I run mine with position size €.1 then I get the same result as you (my minimum is €.2)

Try it with startpositionsize = 1

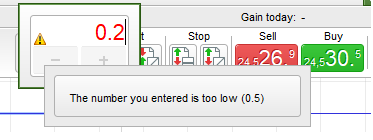

Yes, I am sure about the minimum position, I have attached a screenshot for the sake of being 100% sure.

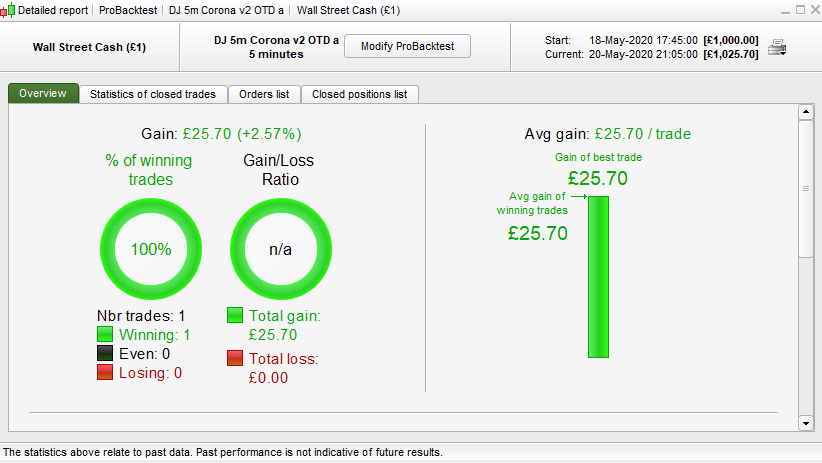

I did some further test and weirdly if I change the time constraint and replace the “AND” by “OR”, I have a result.

Ctime = time >=213000 OR time <230000

But I am concerned that it may affect the results…

I am sure about the minimum position

your screenshot is the PRT chart, but the minimum position will be set by your broker. If you’re with IG, you have to go to their web platform and click on the info button, see attached image.

My first thought about the time was to change AND to OR, but that wouldn’t be right as you’re still in the same day. OR would only be used if it were

Ctime = time >=213000 OR time <010000

ie the second time is less than the first.

Yes, I understand and I assumed the OR would not be the solution.

I am with IG and the minimum position is 0.25 but it does not work with the “OR” if I use anything less than 0.5

May I attach the code “A” in here, maybe I am missing something…thanks for the help here!

DEFPARAM cumulateOrders = False // Cumulating positions deactivate

DEFPARAM preloadbars = 1000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=0.5

ENDIF

if MM = 1 then

ONCE startpositionsize = 0.5

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // IG first tier margin limit

ONCE maxpositionsize = 550 // IG tier 2 margin limit

ONCE minpositionsize = 0.5 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

Ctime = time >=213000 and time <230000

ONCE MAType = 54

ONCE MATypeV2 = 14

once Period = 15 //period1 // // set fixed to limit possible combinations of optimisations

once Period2 = 15 // period2 second set of 69 averages // // set fixed to limit possible combinations of optimisations

Series = (open+high+low+Close)/4 // kind of close of a bar

Seriesv2 = (open+high+low+Close)/4 // kind of close of a bar

OTD = Barindex - TradeIndex(1) > IntradayBarIndex // limits the (opening) trades till 1 per day (OTD One Trade per Day)

TIMEFRAME(15 minutes)

ST1 = SAR[.015,.01,.15]

cnd1 = (close > ST1)

cnd2 = (close < ST1)

mx1 = average[60,3](close)

cnd3 = mx1 > mx1[1]

cnd4 = mx1 < mx1[1]

TIMEFRAME(default)

ST2 = SuperTrend[3,10]

cnd5 = (close > ST2)

cnd6 = (close < ST2)

//Stochastic RSI | indicator

lengthRSI = 14 //RSI period

lengthStoch = 14 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 3 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K2 = average[smoothK](stochrsi)*100

D2 = average[smoothD](K2)

cnd7 = K2>D2

cnd8 = K2<D2

PeriodH2= 22

innerH2 = 2*weightedaverage[round( PeriodH2/2)](typicalprice)-weightedaverage[PeriodH2](typicalprice)

HULLb = weightedaverage[round(sqrt(PeriodH2))](innerH2)

cnd9 = HULLb > HULLb[1]

cnd10 = HULLb < HULLb[1]

CndB = cnd1 and cnd3 and cnd5 and cnd7 and cnd9

CndS = cnd2 and cnd4 and cnd6 and cnd8 and cnd10

//Profit and Loss

SL = 1 // % STOP LOSS

TP = 2 //% TARGET PROFIT

TST = .1//%trailing start

ST = .001 //% trailing step

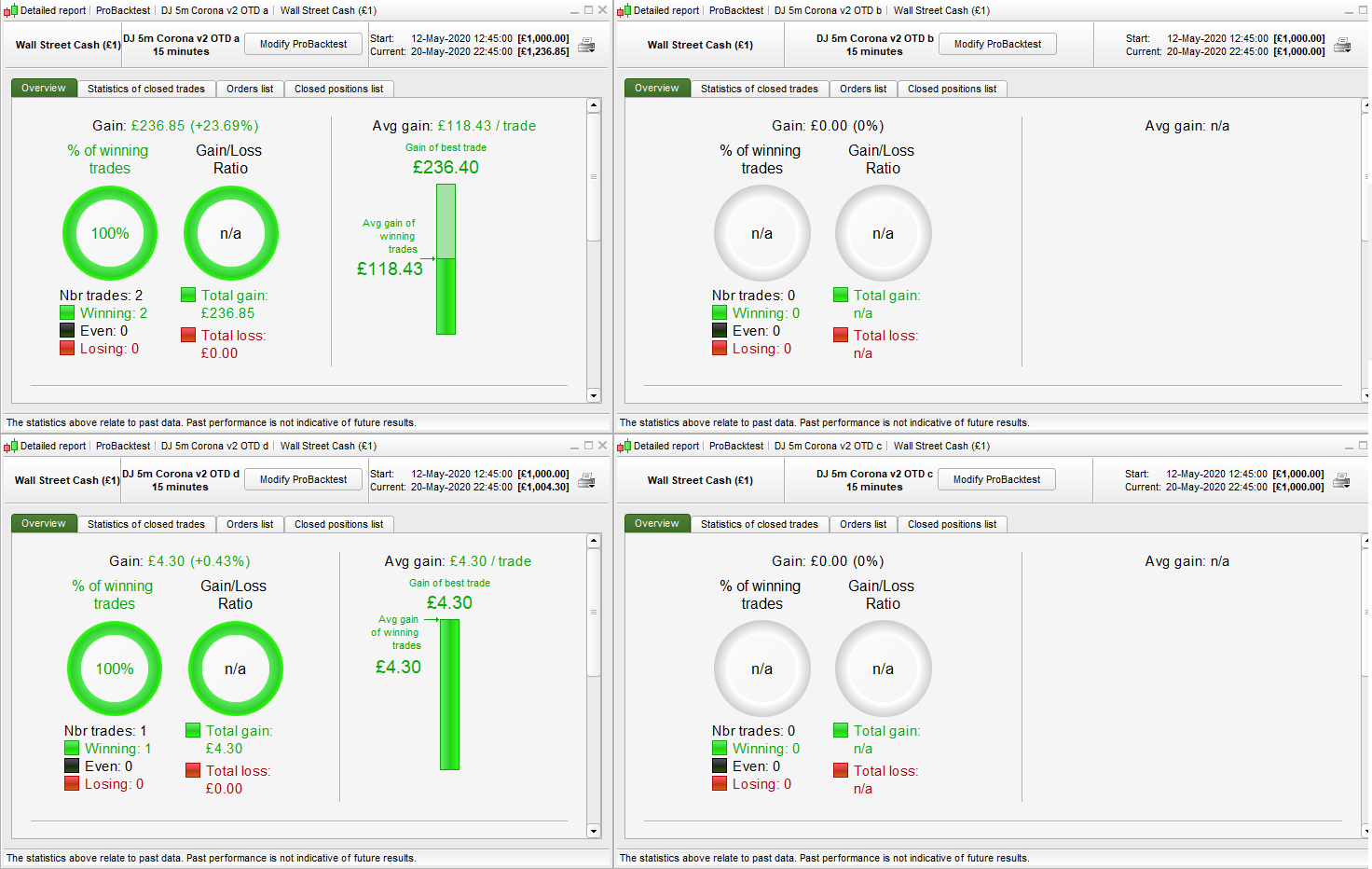

I have tested the exact same in M15 and I get results for A and D, but nothing for B and C. If that ever helps.