Cheers @GraHal, Here it is:

// Definition of code parameters

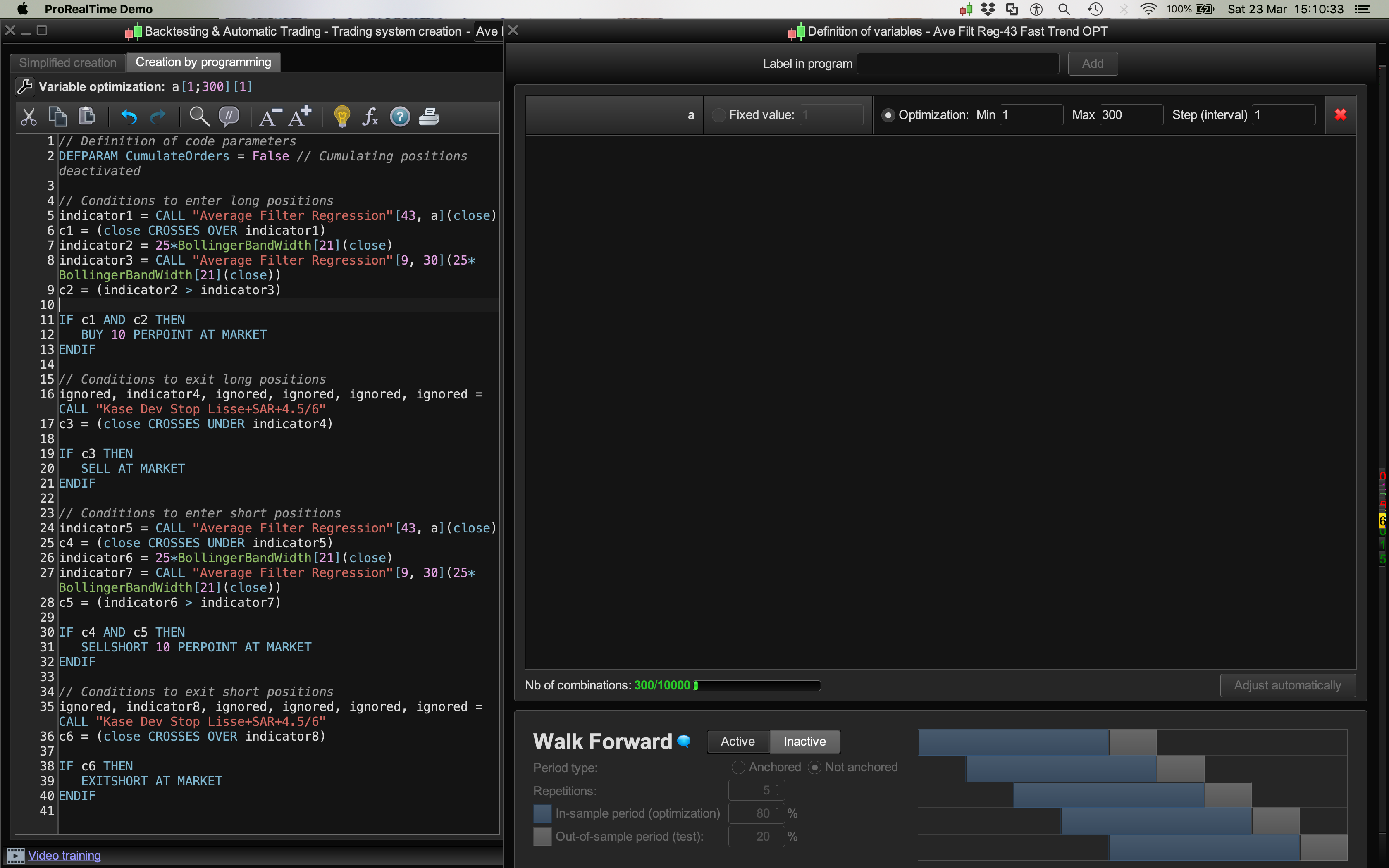

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Conditions to enter long positions

indicator1 = CALL "Average Filter Regression"[43, a](close)

c1 = (close CROSSES OVER indicator1)

indicator2 = 25*BollingerBandWidth[21](close)

indicator3 = CALL "Average Filter Regression"[9, 30](25*BollingerBandWidth[21](close))

c2 = (indicator2 > indicator3)

IF c1 AND c2 THEN

BUY 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

ignored, indicator4, ignored, ignored, ignored, ignored = CALL "Kase Dev Stop Lisse+SAR+4.5/6"

c3 = (close CROSSES UNDER indicator4)

IF c3 THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

indicator5 = CALL "Average Filter Regression"[43, a](close)

c4 = (close CROSSES UNDER indicator5)

indicator6 = 25*BollingerBandWidth[21](close)

indicator7 = CALL "Average Filter Regression"[9, 30](25*BollingerBandWidth[21](close))

c5 = (indicator6 > indicator7)

IF c4 AND c5 THEN

SELLSHORT 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

ignored, indicator8, ignored, ignored, ignored, ignored = CALL "Kase Dev Stop Lisse+SAR+4.5/6"

c6 = (close CROSSES OVER indicator8)

IF c6 THEN

EXITSHORT AT MARKET

ENDIF

//Voici le code en version SAR : plus WITH DEV STOP 4.5 + 6.0

//Settings

n=30

p1=1.0

p2=2.2

p3=3.6

p4=4.5

p5=6.0

difference=0

Hg=highest[2](high)

Lw=lowest[2](low)

DTR=max(max(Hg-Lw,abs(Hg-close[2])),abs(Lw-close[2]))

aDTR=average[n](DTR)

for i=0 to n-1 do

difference=difference+square(DTR[i]-aDTR)

next

difference=difference/n

sdev=sqrt(difference)

dev0=close-aDTR

dev1=close-aDTR-p1*sdev

dev2=close-aDTR-p2*sdev

dev3=close-aDTR-p3*sdev

dev4=close-aDTR-p4*sdev

dev5=close-aDTR-p5*sdev

if dev0<dev0[1] and close>dev5[1] then

dev0=dev0[1]

endif

if dev1<dev1[1] and close>dev5[1] then

dev1=dev1[1]

endif

if dev2<dev2[1] and close>dev5[1] then

dev2=dev2[1]

endif

if dev3<dev3[1] and close>dev5[1] then

dev3=dev3[1]

endif

if dev4<dev4[1] and close>dev5[1] then

dev4=dev4[1]

endif

if dev5<dev5[1] and close>dev5[1] then

dev5=dev5[1]

endif

dev6=close+aDTR

dev7=close+aDTR+p1*sdev

dev8=close+aDTR+p2*sdev

dev9=close+aDTR+p3*sdev

dev10=close+aDTR+p4*sdev

dev11=close+aDTR+p5*sdev

if dev6>dev6[1] and close<dev11[1] then

dev6=dev6[1]

endif

if dev7>dev7[1] and close<dev11[1] then

dev7=dev7[1]

endif

if dev8>dev8[1] and close<dev11[1] then

dev8=dev8[1]

endif

if dev9>dev9[1] and close<dev11[1] then

dev9=dev9[1]

endif

if dev10>dev10[1] and close<dev11[1] then

dev10=dev10[1]

endif

if dev11>dev11[1] and close<dev11[1] then

dev11=dev11[1]

endif

if close>dev11[1] then

flag=-1

else

if close<dev5[1] then

flag=1

endif

endif

if flag=-1 then

ind0=dev0

ind1=dev1

ind2=dev2

ind3=dev3

ind4=dev4

ind5=dev5

//k=1 Blue

r=0

g=191

b=255

else

ind0=dev6

ind1=dev7

ind2=dev8

ind3=dev9

ind4=dev10

ind5=dev11

//k=-1 Orange

r=255

g=128

b=0

endif

//ORIG return ind0 COLOURED BY k,ind1 coloured by k,ind2 coloured by k,ind3 coloured by k//

//ORANGE AND LIGHT BLUE

return ind0 coloured(r,g,b) style(dottedline,2) as "Warning Line", ind1 coloured(r,g,b) style(dottedline,2) as "Dev Stop 1.0", ind2 coloured(r,g,b) style(dottedline,2) as "Dev Stop 2.2", ind3 coloured(r,g,b) style(line,2) as "Dev Stop 3.6", ind4 coloured(r,g,b) style(dottedline,2) as "Dev Stop 4.5", ind5 coloured(r,g,b) style(line,2) as "Dev Stop 6.0"

//NO CHANGE OF COLOUR FOR TREND CHANGE return ind0 coloured(2, 118, 253) style(dottedline,2) as "Warning Line" ,ind1 coloured(2, 118, 253) style(dottedline,2) as "Dev Stop 1.0", ind2 coloured(2, 118, 253) style(dottedline,2) as "Dev Stop 2.2", ind3 coloured(2, 118, 253) style(line,2) as "Dev Stop 3.6", ind4 coloured(2, 118, 253) style(dottedline,2) as "Dev Stop 4.5", ind5 coloured(2, 118, 253) style(line,2) as "Dev Stop 6.0"

I was using filter #43 from here: https://www.prorealcode.com/prorealtime-indicators/average-filter-regression/

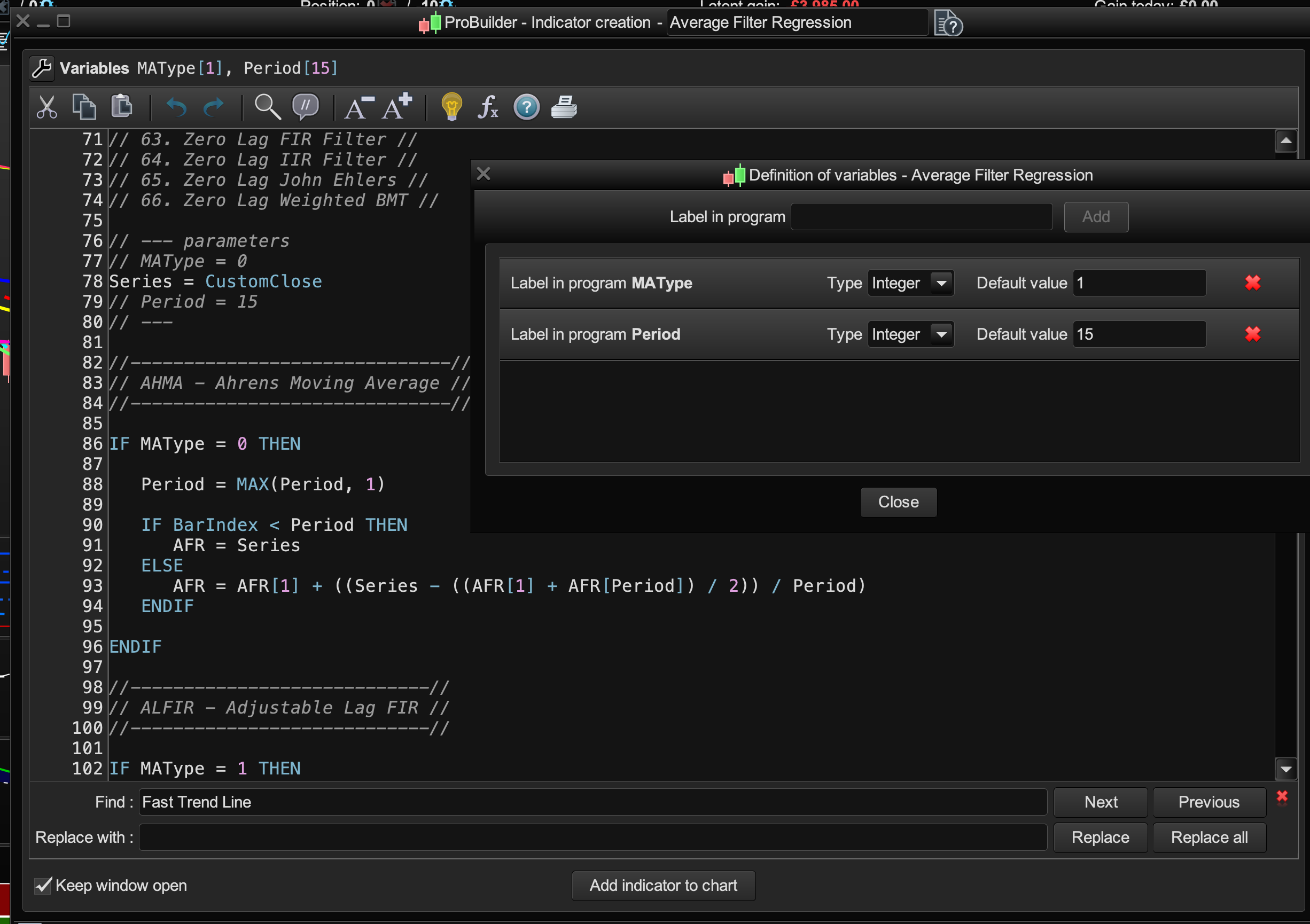

for first part of the Buy signal rules. The other part is the std deviation condition:

Indicator 2 is a 21 period Std Dev indicator. Buy signal if the std dev is > than a 30 period average (#9 from the list of 66 filters) to avoid flat markets.

Ps/ You should check out how the Kase Dev Stop rides some of those trends without stopping you out (regardless of entry type). 👌