@Stefanb, yes that´s strange, 1.5 instead of fib in “set target pprofit box*1.5″ and 0,9 in spread, that´s about it.

yes that is how I am running it. my entries are on the 2nd 5min close outside the range. Manually it works for for me, but then again manually you can react to price action on the fly

Thanks Despair.

That is the problem I am having. If you manually draw the range with fib extensions, you will see how often those targets are hit, but when we try code it, the results are not what I am seeing. For example the dow and S&P hit the 261.8 targets 4 times last week.

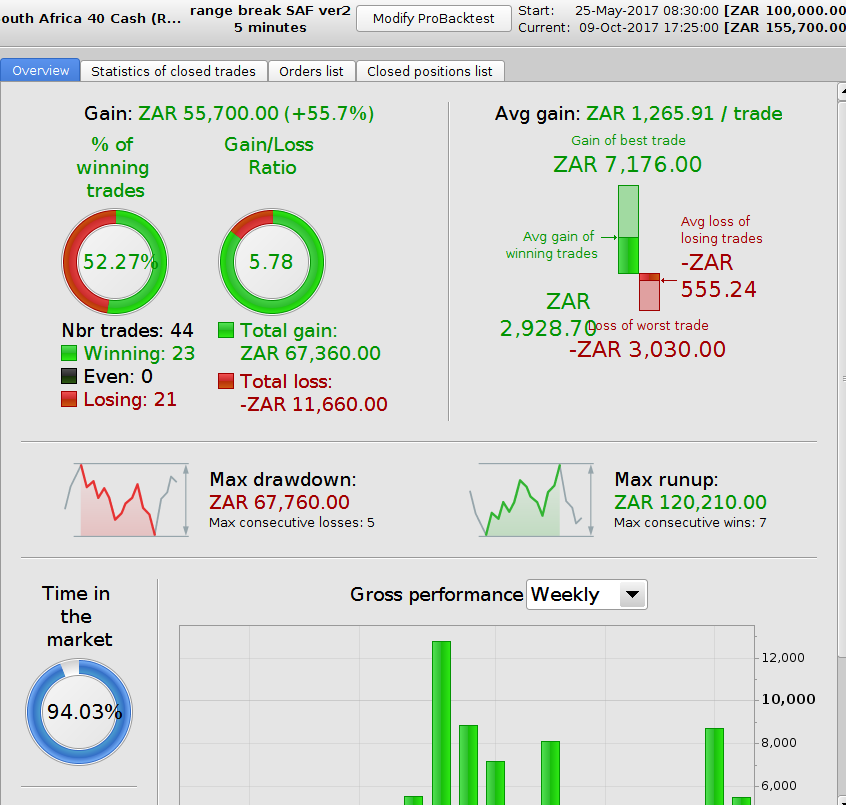

I have made a few changes, still not the results I expect. On SAF 40 it is looking better, but no trades happening in september

defparam cumulateorders=false

tradingtime=dayofweek>=1 and dayofweek<=5 and time>=90000 and time <173000

MAL=ExponentialAverage[5](close) > RangeTop

MAS=ExponentialAverage[5](close) < RangeBottom

once tc=0

if time=90000 then

RangeTop=highest[11](high[1])

RangeBottom=lowest[11](low[1])

endif

if intradaybarindex=0 then

tc=0

endif

CL=close>RangeTop

CS=close<RangeBottom

box=RangeTop-RangeBottom

if not onmarket and not tc and tradingtime then

if CL and MAl then

buy 1 contract at market

tc=1

elsif CS and MAS then

sellshort 1 contract at market

tc=1

endif

set target pprofit box

endif

if longonmarket then

sell at (RangeBottom*.6) stop

elsif shortonmarket then

exitshort at (RangeTop*.6) stop

endif

I notice that the short targets will not work as we are targeting the top of range, I am trying to add criteria that defines a 161.8 expansion but I get errors. Am I coding this correct?

if longonmarket set target pprofit box*1.61

elsif shortonmarket set target pprofit box*0.61

endif

endif

You should make an indicator of the box and its target/stop and applied it on price, better to get a real idea of what happened or not and what to expect from any possible scenario, just my 2 cents 🙂 Great job everyone!

good idea Nicolas! Notice that the dax has broken its open range and on its way to the -61.8 Fibonacci extension. It has already hit the height of the range target

year is the ORB indicator code. Is there a way to only show the lines on the current day during trading hours?

if time =090000 then

RangeTop=highest[6](high[1])

RangeBottom=lowest[6](low[1])

therange= rangetop-rangebottom

tenentrylong=((therange*.3820)+rangetop)

tenentryshort=(rangebottom-(therange*.3820))

takeprofitlong=((therange*1.618)+rangetop)

takeprofitshort=(rangebottom-(therange*1.618))

endif

return rangetop as "top of range", rangebottom as "bottom of range", tenentrylong as "anti fake out long",tenentryshort as "anti fake out short", takeprofitlong as"Long Profit Target", takeprofitshort as"Short Profit Target"

Like this?

if dayofweek=currentdayofweek and time =090000 then

RangeTop=highest[6](high[1])

RangeBottom=lowest[6](low[1])

therange= rangetop-rangebottom

tenentrylong=((therange*.3820)+rangetop)

tenentryshort=(rangebottom-(therange*.3820))

takeprofitlong=((therange*1.618)+rangetop)

takeprofitshort=(rangebottom-(therange*1.618))

endif

return rangetop as "top of range", rangebottom as "bottom of range", tenentrylong as "anti fake out long",tenentryshort as "anti fake out short", takeprofitlong as"Long Profit Target", takeprofitshort as"Short Profit Target"

S&P and Dow both hit their 61.8 open range targets

I played around last night, with some interesting results, running it in demo now

defparam cumulateorders=false

tradingtime=dayofweek>=1 and dayofweek<=5 and time>=090500 and time <170000

MAL=ExponentialAverage[5](close) > close[1]

MAS=ExponentialAverage[5](close) < close[1]

//once tc=0

if time=090500 then

RangeTop=highest[6](high[1])

RangeBottom=lowest[6](low[1])

endif

//if intradaybarindex=0 then

//tc=0

//endif

//CL=close>RangeTop

//CS=close<RangeBottom

box=RangeTop-RangeBottom

entryl=close>=(rangetop+(box*.15))

entrys=close<=(rangebottom-(box*.15))

//trendlong=rangetop<ExponentialAverage[5](close)

//trendshort=rangebottom>entrys

if not onmarket and tradingtime then

if entryl and mal then

buy 2 contract at market

//tc=1

elsif entrys and mas then

sellshort 2 contract at market

//tc=1

endif

set target pprofit box*2.5

endif

if longonmarket then

sell at ExponentialAverage[5](close)> ExponentialAverage[15](close)stop

elsif shortonmarket then

exitshort at ExponentialAverage[5](close)<ExponentialAverage[15](close) stop

//elsif

//endif

endif

//set stop loss 100

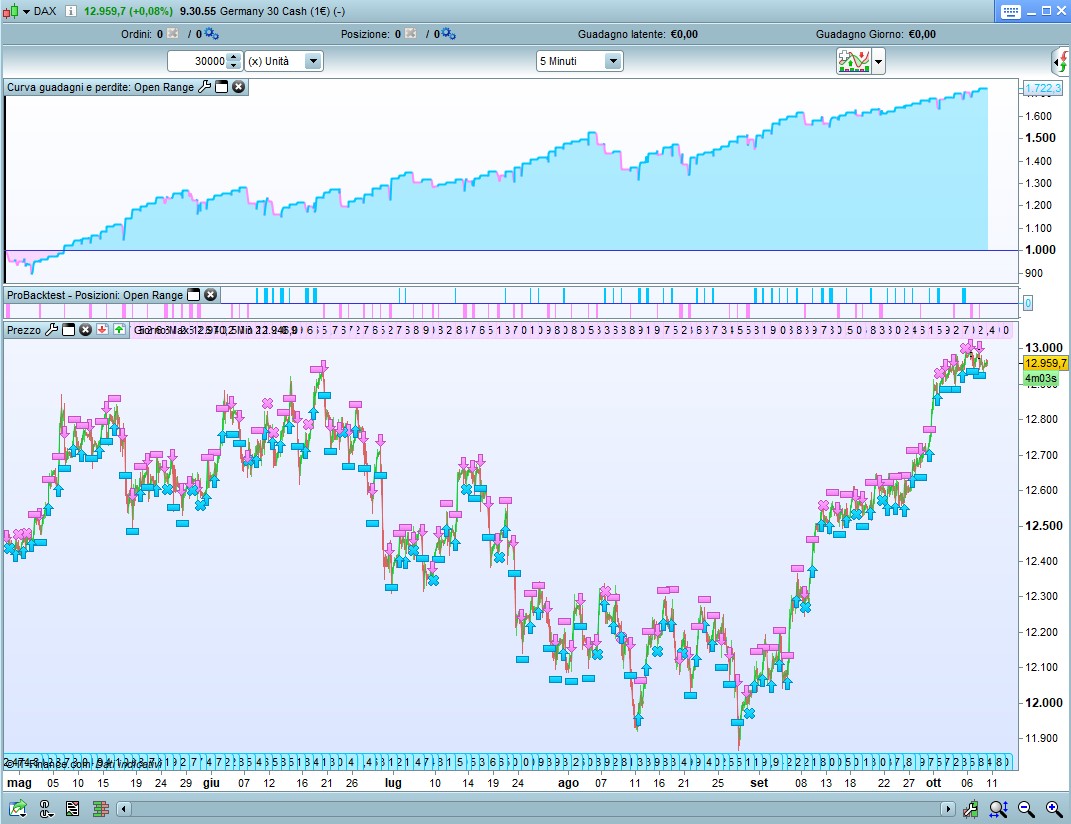

This is the best I could get on Dax. The backtest on the last 30000 candles looks good.

defparam cumulateorders=false

defparam flatafter=173000

tradingtime=dayofweek>=1 and dayofweek<=5 and time>=90000

MA=ExponentialAverage[10](close) //15

once tc=0

if time=90000 then

RangeTop=highest[11](high[1])

RangeBottom=lowest[11](low[1])

Box=RangeTop-RangeBottom

endif

if intradaybarindex=0 then

tc=0

endif

CL=close>RangeTop and close[1]>RangeTop

CS=close<RangeBottom and close[1]<RangeBottom

box=RangeTop-RangeBottom

if not onmarket and not tc and tradingtime then

if CL and close>MA then

buy 1 contract at market

tc=1

elsif CS and close<MA then

sellshort 1 contract at market

tc=1

endif

set target pprofit box*0.618

endif

// Stop Loss

if longonmarket then

sell at RangeBottom-box*1.618 stop

elsif shortonmarket then

exitshort at RangeTop+box*1.618 stop

endif

@dillongr

There is something wrong with your exit conditions (pending orders) at lines 37 and 39. You are trying to put a stop order at 1 or 0 since you are using boolean conditions (is my first value is superior to my second one? TRUE=1 FALSE=0).