I’m setting up a simple trading system and need a way to trigger a one-time entry (either long or short) at the start if there’s no existing position. This is particularly important after rolling contracts and restarting the system, so it can re-enter immediately if required. I’ve tried using ONCE and various flags, but the system keeps triggering unintended signals. Looking for a simple, reliable code solution to execute an entry just once at the start without affecting ongoing trade signals. Any suggestions?

// Set code parameters

DEFPARAM CumulateOrders = False // Cumulating positions disabled

ONCE checkLongPosition = NOT LONGONMARKET

// Buy only once on system start

IF checkLongPosition THEN

BUY 1 SHARE AT MARKET

ENDIF

superTrendValue = SuperTrend[5.4,36]

// Conditions for entering long positions

c1 = (close CROSSES OVER superTrendValue)

IF NOT LONGONMARKET AND c1 THEN

BUY 1 SHARES AT MARKET

ENDIF

// Conditions for exiting long positions

c2 = (close CROSSES UNDER superTrendValue)

IF LONGONMARKET AND c2 THEN

SELL AT MARKET

ENDIF

// Conditions for entering short positions

c3 = (close CROSSES UNDER superTrendValue)

IF NOT SHORTONMARKET AND c3 THEN

SELLSHORT 1 SHARES AT MARKET

ENDIF

// Conditions for exiting short positions

c4 = (close CROSSES OVER superTrendValue)

IF SHORTONMARKET AND c4 THEN

EXITSHORT AT MARKET

ENDIF

JS

JSParticipant

Senior

Not a bad idea from ChatGPT… 🙂

DEFPARAM CumulateOrders = False // Prevents multiple entries

ONCE EntryFlag = 0 // Initialization for one-time entry

// Check if there is no position at the start and EntryFlag is 0

IF NOT OnMarket AND EntryFlag = 0 THEN

// Define your entry condition here

IF /* Your Entry Condition */ THEN

BUY 1 CONTRACT AT MARKET // Long Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSEIF /* Alternative Short Condition */ THEN

SELLSHORT 1 CONTRACT AT MARKET // Short Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ENDIF

ENDIF

Thank you! ChatGPT couldn’t solve this, that’s why I am here haha

Unfortunately I’m not getting any entries with this code. I’ve tried it both nested and un-nested, as well as with and without additional conditions, but nothing seems to happen:

// Set code parameters

DEFPARAM CumulateOrders = False // Prevents multiple entries

// Initialize flag for one-time entry

ONCE EntryFlag = 0

// Check for initial entry at the start if there's no position and EntryFlag is 0

IF NOT ONMARKET AND EntryFlag = 0 THEN

BUY 1 SHARES AT MARKET // Long entry

EntryFlag = 1 // Set the flag to prevent re-triggering the initial entry

ENDIF

Sorry… newby here 😅

This was another try, with the full code, but nothing happens:

// Set code parameters

DEFPARAM CumulateOrders = False // Prevents multiple entries

ONCE EntryFlag = 0 // Initialization for one-time entry

superTrendValue = SuperTrend[5.4,36]

// Check if there is no LONG position at the start and EntryFlag is 0

IF NOT LONGONMARKET AND EntryFlag = 0 THEN

BUY 1 CONTRACT AT MARKET

IF NOT LONGONMARKET AND close CROSSES OVER superTrendValue THEN

BUY 1 CONTRACT AT MARKET // Long Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSIF NOT SHORTONMARKET AND close CROSSES UNDER superTrendValue THEN

SELLSHORT 1 CONTRACT AT MARKET // Short Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ENDIF

ENDIF

Add this line at the very beginning:

DEFPARAM PreLoadBars = 0

it will open only ONE trade and will never close, as there is no indication when it must be exited.

Thanks, the one-time entry works now! 🙏🏼

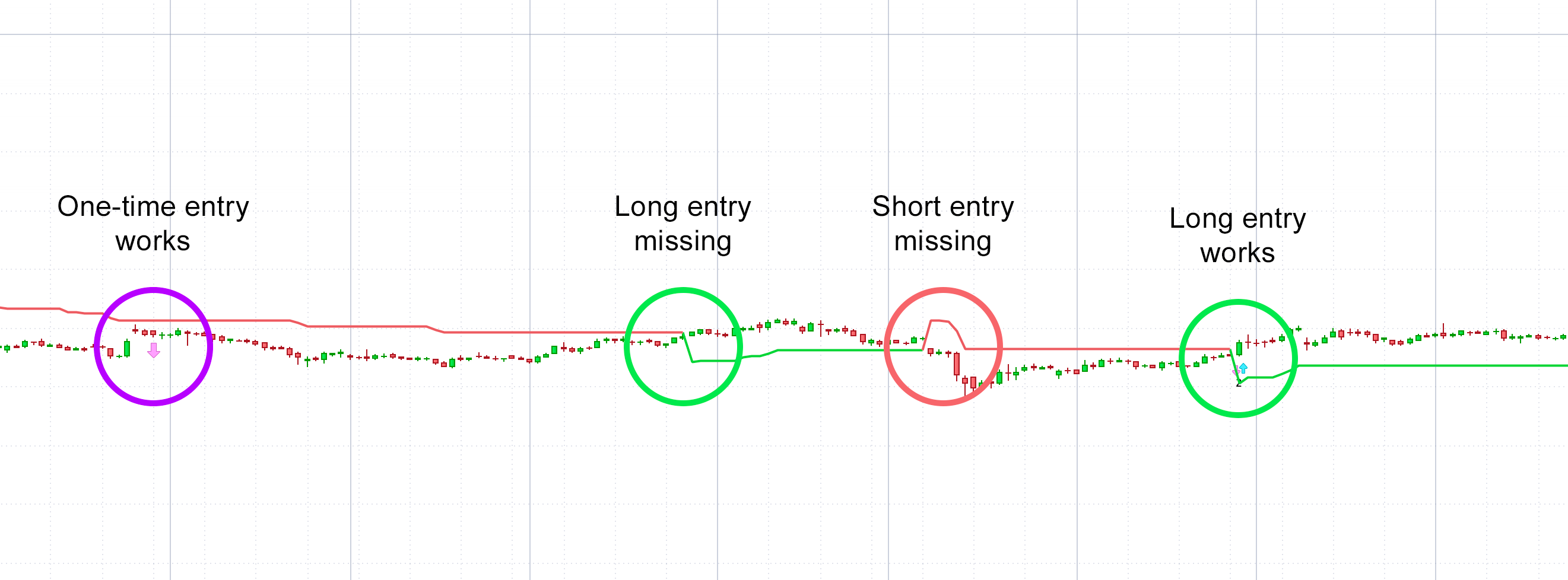

With the following code, the other conditions also seem to work, except the first 2 Supertrend crossings directly after the one-time entry are missing (see attachment) – any idea why? The rest of the signals work fine!

// Set code parameters

DEFPARAM PreLoadBars = 0

DEFPARAM CumulateOrders = False // Prevents multiple entries

ONCE EntryFlag = 0 // Initialization for one-time entry

superTrendValue = SuperTrend[5.4,36]

// Check if there is no position at the start and EntryFlag is 0

IF NOT ONMARKET AND EntryFlag = 0 THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Long Conditions

IF NOT LONGONMARKET AND close CROSSES OVER superTrendValue THEN

BUY 1 CONTRACT AT MARKET // Long Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSIF LONGONMARKET AND close CROSSES UNDER superTrendValue THEN

SELL 1 CONTRACT AT MARKET // Long Exit

ENDIF

// Short Conditions

IF NOT SHORTONMARKET AND close CROSSES UNDER superTrendValue THEN

SELLSHORT 1 CONTRACT AT MARKET // Short Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSIF SHORTONMARKET AND close CROSSES OVER superTrendValue THEN

EXITSHORT 1 CONTRACT AT MARKET // Short Exit

ENDIF

Seems like the first signal is beeing ignored in any case:

JSParticipant

Senior

Hi,

Try this one:

// Set code parameters

DEFPARAM PreLoadBars = 0

DEFPARAM CumulateOrders = False // Prevents multiple entries

ONCE EntryFlag = 0 // Initialization for one-time entry

superTrendValue = SuperTrend[5.4,36]

// Check if there is no position at the start and EntryFlag is 0

IF NOT ONMARKET AND EntryFlag = 0 THEN

SELLSHORT 1 CONTRACT AT MARKET

EntryFlag=1

ENDIF

// Long Conditions

IF NOT LONGONMARKET AND EntryFlag=1 and close CROSSES OVER superTrendValue THEN

BUY 1 CONTRACT AT MARKET // Long Entry

ELSIF LONGONMARKET AND EntryFlag=1 and close CROSSES UNDER superTrendValue THEN

SELL 1 CONTRACT AT MARKET // Long Exit

ENDIF

// Short Conditions

IF NOT SHORTONMARKET AND EntryFlag=1 and close CROSSES UNDER superTrendValue THEN

SELLSHORT 1 CONTRACT AT MARKET // Short Entry

ELSIF SHORTONMARKET AND EntryFlag=1 and close CROSSES OVER superTrendValue THEN

EXITSHORT 1 CONTRACT AT MARKET // Short Exit

ENDIF

When i use your code 1:1 the entry on the backtest starting date is missing – it enters a short position on the next Supertrend short signal (Screenshot attached) – the problem is that I want to do auto trading with Futures, and when I have an open position and need to roll over to a new contract, I have to close that position but might want to continue with the position / auto trading within the new contract (as the trend is still ongoing), and don’t want to wait until the next signal.

Also, opening a position manually won’t work with auto trading systems:

PRT Conditions of execution of automatic trading systems

“When you begin an automatic trading system, any pre-existing positions placed manually are closed first and any pre-existing orders placed manually are canceled. The first position of the system may be opened at the earliest at the open of the next bar after the system is started.”

How do you handle this, as this is sub-optimal for Futures auto trading? It’s kinda frustrating 🥲

JSParticipant

Senior

With short position on start/backtest date:

// Set code parameters

DEFPARAM PreLoadBars = 0

DEFPARAM CumulateOrders = False // Prevents multiple entries

ONCE EntryFlag = 0 // Initialization for one-time entry

superTrendValue = SuperTrend[5.4,36]

// Check if there is no position at the start and EntryFlag is 0

IF NOT ONMARKET AND EntryFlag = 0 THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Long Conditions

IF NOT LONGONMARKET and close CROSSES OVER superTrendValue THEN

BUY 1 CONTRACT AT MARKET // Long Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSIF LONGONMARKET and close CROSSES UNDER superTrendValue THEN

SELL AT MARKET // Long Exit

EntryFlag = 1

ENDIF

// Short Conditions

IF NOT SHORTONMARKET AND close CROSSES UNDER superTrendValue THEN

SELLSHORT 1 CONTRACT AT MARKET // Short Entry

EntryFlag = 1 // Set the flag to avoid re-triggering

ELSIF SHORTONMARKET and close CROSSES OVER superTrendValue THEN

EXITSHORT AT MARKET // Short Exit

EntryFlag = 1

ENDIF

Yes we had that code before, but then upcoming signals are being ignored:

JSParticipant

Senior

Strange, in my graph the first signal is executed…

Can you maybe try it with MBTCUSD and 1 day timeframe?

JSParticipant

Senior

On MBTCUSD TimeFrame 1 day…

It depends on the selected units, when i do a backtest (e.g. 3 or 5 years), 1day timeframe, 10k units there is an inconsistency within the entries. With 100 units (as in your test) it seems to work.