@Makside, could you upload your .itf that I have a look at what’s different and what could be improved in this strategy? 🙂

yes if you want, it’s a poc..

Thanks @Makside!

On the long run (1M candles) it does not looks very linear curve, I’ll have a look is something is interesting in your code 😉

I’m afraid, it looks like overoptimized with 1M historical bar…

yes, it’s just a test… it’s up to everyone to do what they want with this code, it’s not turnkey..

Paul

PaulParticipant

Master

Hi Tanou, the idea I had use market direction before opening reduces the trades too much.

The buy/sellshort stop order does work, for i.e. on 1 minute but it could mean a delayed entry compared to 10s because of Heikin-Ashi. In the past I worked on OpenStraddle DAX v6p, a bit similar.

Hey Paul, I just went to your strat and indeed it looks quite similar in some points. So what do you think of this one? 😉

PaulParticipant

Master

maybe, what I programmed back then failed. You could implemented yours into barhunter and find/optimise the right bar=time where it has the most chance perhaps. long time ago I’ve looked at that setup.

PaulParticipant

Master

forget about barhunter

It happens in your strategy you use time and opentime together. Not saying it’s wrong here, but it’s tricky!

Another way to use a reset is with intradaybarindex=0. It has influence on results though.

You used Heikin-Ashi in the trailingstop, which for me complicates things. Not so easy to improve on this strategy.

Yes, I agree… I’ll keep having an eye in it to see if some changes can be done.

What do you mean by barhunter ?

PaulParticipant

Master

That’s the downside not posting it in the library 🙂 Spent a lot of time on thisone.

Barhunter was a strategy that searches for a bar where it would setup a breakpoint (straddle sortoff) for long & short with stop order for entry. So it uses 1hour timeframe to do the backtest, and after finding it, you switch mode and use 1 minute timeframe to create the same results you had in the backtest of 1 hour. Pretty good implantation of the trailing stop too.

So 1h is easy, you optimise 24 bars and it found that hour 3/4 is the best hour. That in combination with trend detection system & breakpointpercentage .

here’s the link

https://www.prorealcode.com/topic/strategy-barhunter-dax-v1p/

Will post a few charts there.

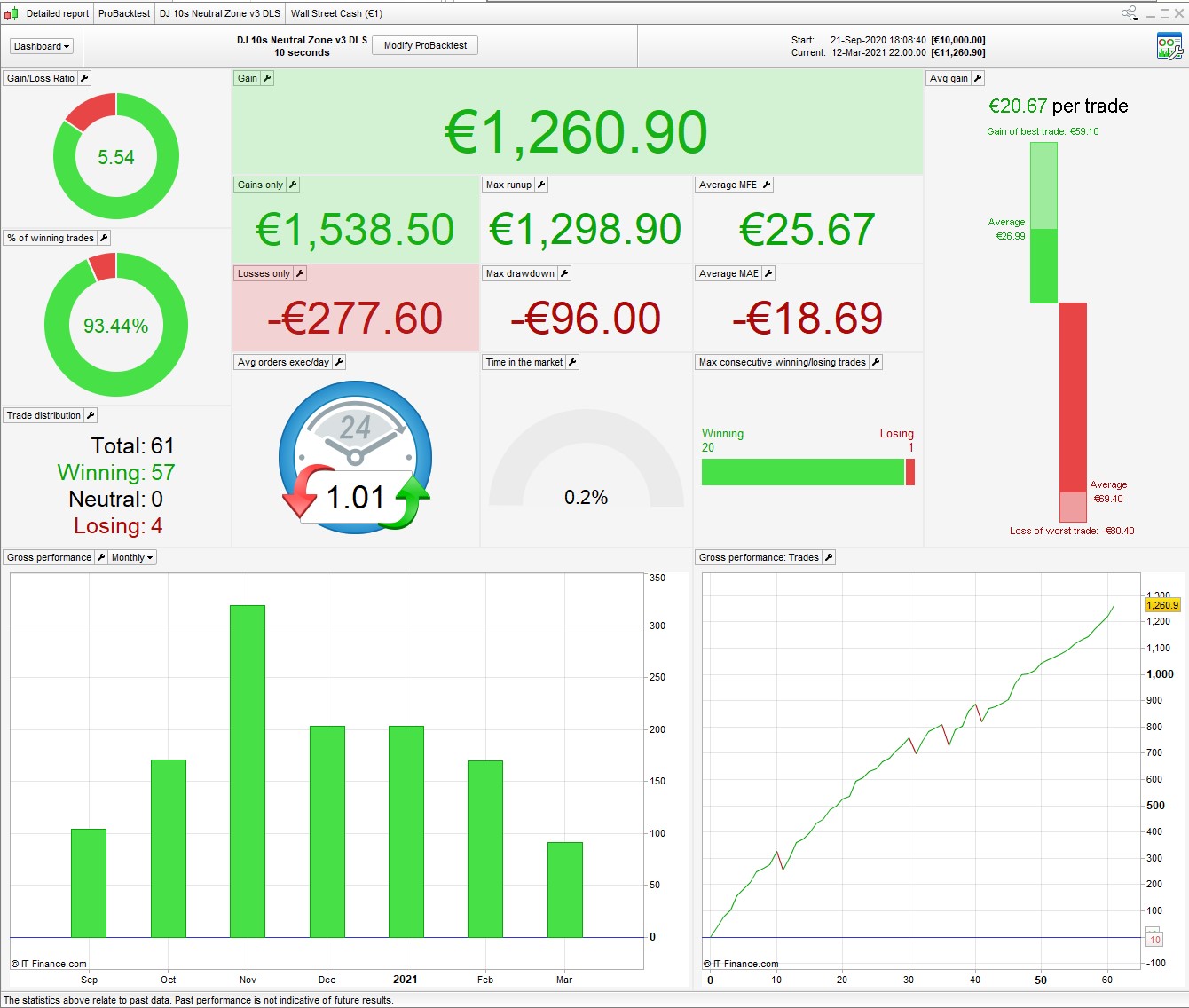

Here’s a version of this with a few tweaks – added MM, TP and allowance for American DLS which makes a big difference. Works quite well for a very short backtest, but I don’t understand why it takes 10x more short trades than long? Should be room for improvement there.

Hello @Nonetheless !

It is because it is th short version 😀

Here is the long one 😉 (I can’t make it linear, if you have ideas!)

//-------------------------------------------------------------------------

// Code principal : Neutral Zone Long.

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Code principal : Neutral Zone Long

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Code principal : Neutral Zone Long

//-------------------------------------------------------------------------

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

// Annule tous les ordres en attente et ferme toutes les positions à 0:00, puis empêche toute création d'ordre avant l'heure "FLATBEFORE".

DEFPARAM FLATBEFORE = 152900

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 220000

// Variables / Réglages :

TimeOpen = 153000

TimeClose = 220000

x=21 //Taille de la zone autour de l'ouverture pour activation/Désactivation

//-----------------------------------------------------------------------------------------------------------------------------------------------------

//HORAIRES DE TRADING

Ctime = time >= TimeOpen and time < TimeClose

//--------------------------------------

//Nouveau OpenPrice et OpenDay a 15:30

IF OPENTIME = (TimeOpen) then

OpenPrice = Open

OpenD = OpenDay

strategyprofitpoint=0

l = 0

s = 0

count = 0

debutopen = barindex

ENDIF

if(strategyprofit<>strategyprofit[1]) then

strategyprofitpoint = (strategyprofit-strategyprofit[1])/pointvalue

endif

//------------------------------------

//Représentation graphique Heikin-Ashi

once xOpen = open

Price = (open + close + low + high)/4

if barindex > 0 then

xOpen = (xOpen + Price[1]) / 2

endif

xLow = min(low,min(Price,xOpen))

xHigh = max(high,max(Price,xOpen))

GreenHA = Price > xOpen

RedHA = Price < xOpen

//------------------------------------

// STRATEGIE ---------------------------------------------------------------------------------

// Conditions Short

If s=0 then

If xHigh=xOpen and xHigh<(OpenPrice-x) then

s1 = 1

Else

s1 = 0

Endif

Endif

//Conditions Long

If l=0 then

If xLow=xOpen and xLow>(OpenPrice+x) then

l1 = 1

Else

l1=0

Endif

Endif

//-------------------------------------------------------------------------------------------

//POSITION LONGUE

IF l1 and strategyprofitpoint<=0 and count<2 and ctime THEN

Buy 1 contract at market

l1 = 0

l = 1

count = count + 1

ENDIF

//POSITION COURTE

IF s1 and not onmarket and strategyprofitpoint<=0 and count<2 and ctime THEN

s1 = 0

count = count + 1

ENDIF

//POSITION COURTE

IF s1 and strategyprofitpoint<=0 and count>=1 and count<2 and ctime THEN

Sellshort 1 contract at market

s1 = 0

s = 1

count = count + 1

ENDIF

//TP et SL ---------------------------------------------------------------------------------

//Variables

NATR = 14 //ATR Period

SATR = 20 // ATR Multiplier for Stop

PATR = 1// ATR Multiplier for Profit

//Stop and Target

SET STOP LOSS SATR*AverageTrueRange[NATR](close)

SET TARGET PROFIT PATR*AverageTrueRange[NATR](close)

It is because it is th short version

Salut Tanou – yes, I did see that you had posted long and short versions, what I meant is that it seemed odd that they weren’t completely exclusive – the short version still takes some long trades and vice versa.

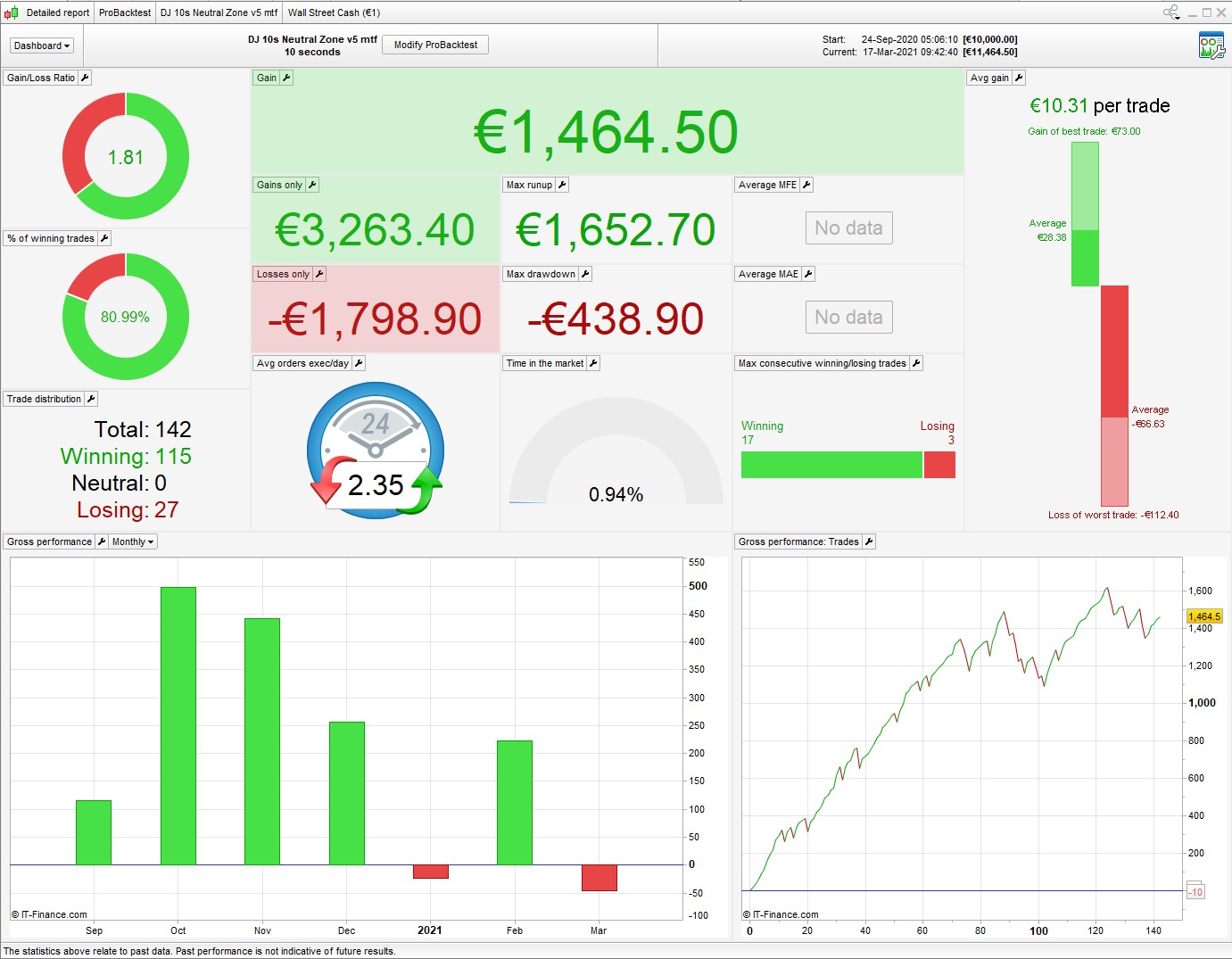

This is the best I could do for a fully ambidextrous version, lots more trades, more or less equal long and short … but only slightly more profitable and less stable. Hard to say if it’s worth it with a short backtest ???

I added an MA on the 2m TF, but this is the main change:

//POSITION LONGUE

IF l1 and strategyprofitpoint<=0 and count<2 and ctime and cb1 THEN

Buy PositionSize contract at market

l1 = 0

l = 1

count = count + 1

SET TARGET %PROFIT tp

ENDIF

//POSITION COURTE

IF s1 and strategyprofitpoint<=0 and count<2 and ctime and cs1 THEN

Sellshort PositionSize contract at market

s1 = 0

s = 1

count = count + 1

SET TARGET %PROFIT tps

ENDIF