Hi Lombard974

Doesn’t exactly work the way I wanted, it takes one position based on high/low from 15min bar after crossing, on the next bar, with only 1 trade a day between 9.00-9.15

Lines display the high/low from the 15min candle 845-0900. You also see your stoploss and the trailing-stops.

Your second option isn’t implemented and is perhaps not suitable for this code.

The code is a bit long, it the layout I work with. Focus on the main criteria part for adjustment and time settings.

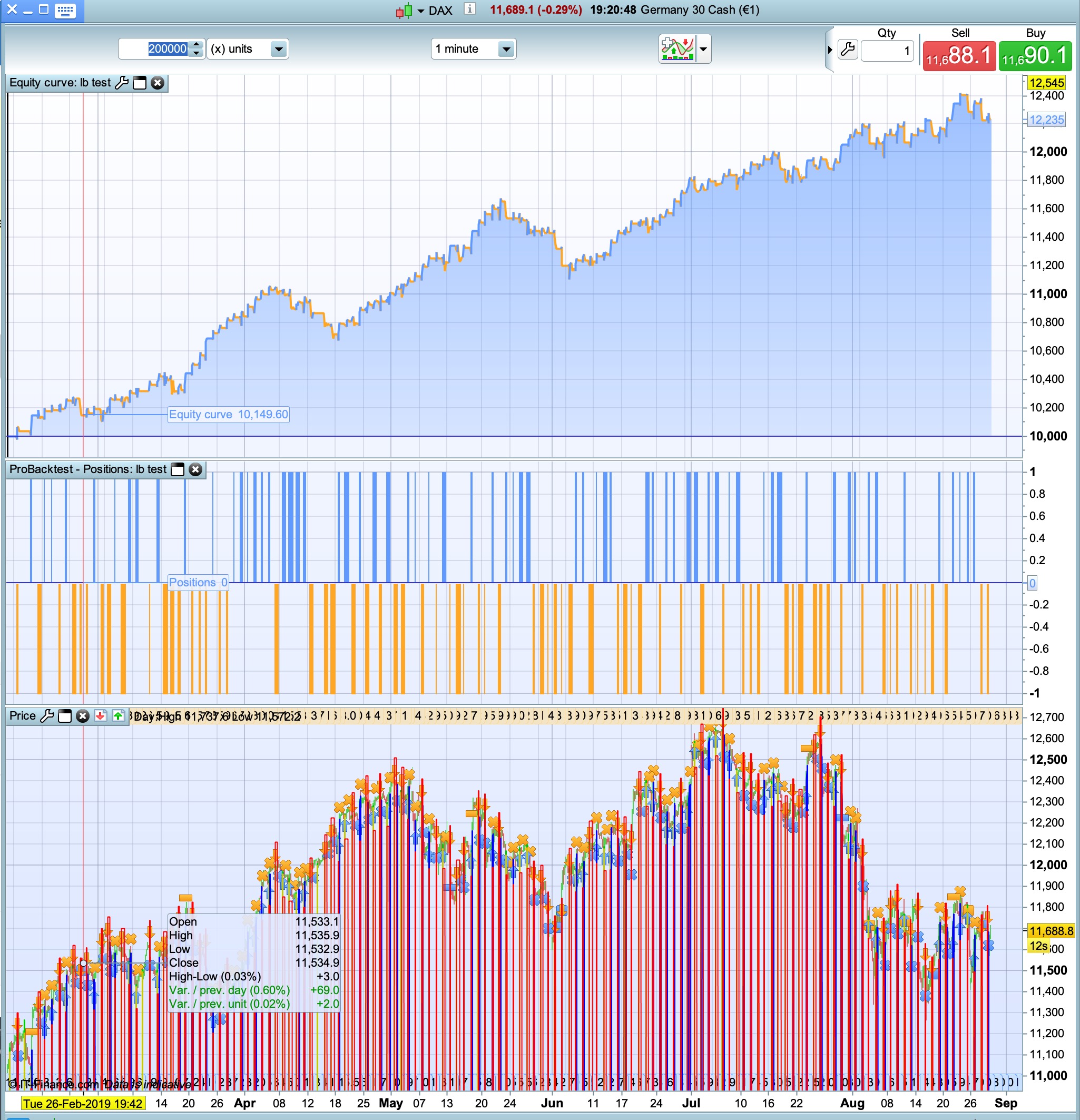

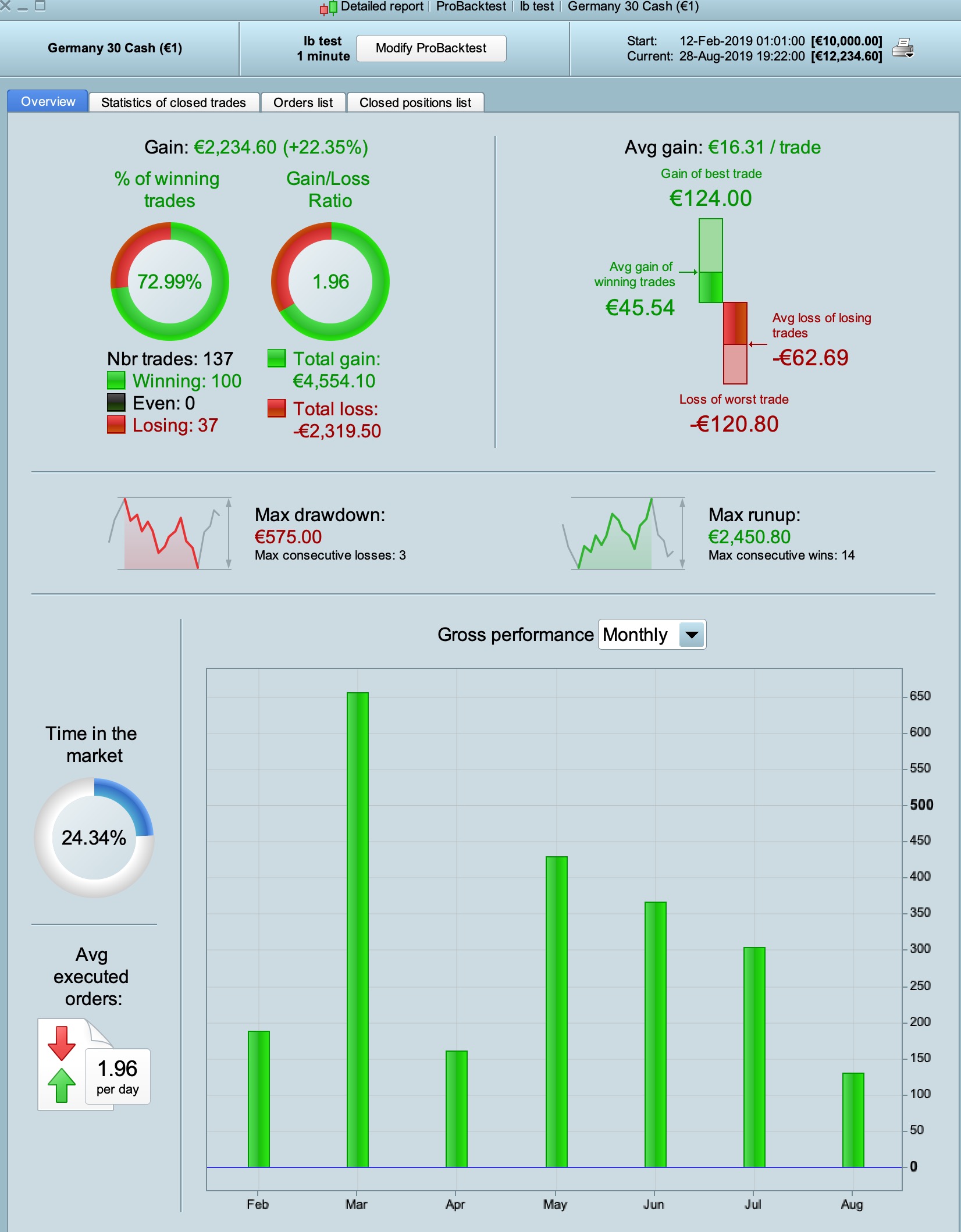

Tested on DAX30 1 minute.

// common rules

defparam cumulateorders = false

defparam preloadbars = 10000

TIMEFRAME (default)

// on/off

once enablesl = 1 // stoploss

once enablept = 1 // profit target

once enablets = 1 // trailing stop

once enablebe = 0 // breakeven stop

//activate graph(onprice); maximum 5 lines active !

once displaysl = 1 // stop loss [1 line]

once displaypt = 0 // profit target [1 line]

once displayts = 1 // trailing stop [3 lines]

once displaybe = 0 // breakeven stop [1 line]

once displaydim = 0 // days in market [1 line]

once displaypp = 0 // position performance [1 line]

positionsize = 1

sl = 1 // % stoploss

pt = 1 // % profit target

// trailingstop exit activates when positionperformance (pp)

ts1=0.35 // is greater then this percentage then use trailingstop ts1

switch=0.45 // is greater then this percentage then use trailingstop ts2

ts2=0.25

switch2=0.60 // is greater then this percentage then use trailingstop ts3

ts3=0.20

// breakeven exit

besg = 0.30 // % break even stop gain

besl = 0.05 // % break even stop level

// used for sl/pt/ (not used for ts); not to be optimized!

// forex use 0.01; securities use 1, index use 100

// profittargets and stoploss have to match the lines with displaysl/tp/ts set to 1

underlaying=100

// day & time

once entertime = 090000

once lasttime = 091500

once closetime = 210000 // greater then 23.59 means it continues position overnight

once closetimefr = 180000

tradetime = (time >= entertime and time < lasttime)

// reset at start

if intradaybarindex=0 then

longtradecounter=0

shorttradecounter=0

tradecounter=0

endif

// [pc] position criteria (also set a limit to the number of trades a day) (or set high for no impact)

pclong = countoflongshares < 1 and longtradecounter < 1 and tradecounter < 1

pcshort = countofshortshares < 1 and shorttradecounter < 1 and tradecounter < 1

//[mc] main criteria

TIMEFRAME (15 minutes, updateonclose)

if intradaybarindex=35 then //0845-0900 on 15 min

MaxPrice = high

MinPrice = low

else

MaxPrice = 0

MinPrice = 0

ENDIF

graphonprice MaxPrice coloured(0,200,0) as "MaxPrice"

graphonprice MinPrice coloured(200,200,0) as "MinPrice"

TIMEFRAME (default)

if intradaybarindex=0 then

mclong=0

mcshort=0

endif

if close crosses over MaxPrice then

mclong=1

endif

if close crosses under MinPrice then

mcshort=1

endif

// long & short entry

if tradetime then

if pclong and mclong then

buy positionsize contract at MaxPrice stop

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

elsif pcshort and mcshort then

sellshort positionsize contract at MinPrice stop

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

endif

endif

//

pp=(positionperf*100)

// trailing stop

if enablets then

trailingstop1 = (tradeprice(1)/100)*ts1

trailingstop2 = (tradeprice(1)/100)*ts2

trailingstop3 = (tradeprice(1)/100)*ts3

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice1=0

minprice1=close

priceexit1=0

maxprice2=0

minprice2=close

priceexit2=0

maxprice3=0

minprice3=close

priceexit3=0

a1=0

a2=0

a3=0

pp=0

endif

if onmarket then

if pp>=ts1 then

a1=1

endif

if pp>=switch then

a2=1

endif

if pp>=switch2 then

a3=1

endif

endif

// setup long

if longonmarket then

maxprice1=max(maxprice1,close)

maxprice2=max(maxprice2,high)

maxprice3=max(maxprice3,high)

if a1 then

if maxprice1-tradeprice(1)>=(trailingstop1)*pointsize then

priceexit1=maxprice1-(trailingstop1/(underlaying/100))*pointsize

endif

endif

if a2 then

if maxprice2-tradeprice(1)>=(trailingstop2)*pointsize then

priceexit2=maxprice2-(trailingstop2/(underlaying/100))*pointsize

endif

endif

if a3 then

if maxprice3-tradeprice(1)>=(trailingstop3)*pointsize then

priceexit3=maxprice3-(trailingstop3/(underlaying/100))*pointsize

endif

endif

endif

// setup short

if shortonmarket then

minprice1=min(minprice1,close)

minprice2=min(minprice2,low)

minprice3=min(minprice3,low)

if a1 then

if tradeprice(1)-minprice1>=(trailingstop1)*pointsize then

priceexit1=minprice1+(trailingstop1/(underlaying/100))*pointsize

endif

endif

if a2 then

if tradeprice(1)-minprice2>=(trailingstop2)*pointsize then

priceexit2=minprice2+(trailingstop2/(underlaying/100))*pointsize

endif

endif

if a3 then

if tradeprice(1)-minprice3>=(trailingstop3)*pointsize then

priceexit3=minprice3+(trailingstop3/(underlaying/100))*pointsize

endif

endif

endif

// exit long

if longonmarket and priceexit1>0 then

sell at priceexit1 stop

endif

if longonmarket and priceexit2>0 then

sell at priceexit2 stop

endif

if longonmarket and priceexit3>0 then

sell at priceexit3 stop

endif

// exit short

if shortonmarket and priceexit1>0 then

exitshort at priceexit1 stop

endif

if shortonmarket and priceexit2>0 then

exitshort at priceexit2 stop

endif

if shortonmarket and priceexit3>0 then

exitshort at priceexit3 stop

endif

if displayts then

graphonprice priceexit1 coloured(0,0,255,255) as "trailingstop1"

graphonprice priceexit2 coloured(0,0,255,255) as "trailingstop2"

graphonprice priceexit3 coloured(0,0,255,255) as "trailingstop3"

endif

endif

// break even stop

if enablebe then

if not onmarket then

newsl=0

endif

if ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl=0

endif

if longonmarket then

if close-tradeprice(1)>=(((tradeprice(1)/100)*besg)/(underlaying/100))*pointsize then

newsl=tradeprice(1)+(((tradeprice(1)/100)*besl)/(underlaying/100))*pointsize

endif

endif

if shortonmarket then

if tradeprice(1)-close>=(((tradeprice(1)/100)*besg)/(underlaying/100))*pointsize then

newsl=tradeprice(1)-(((tradeprice(1)/100)*besl)/(underlaying/100))*pointsize

endif

endif

if longonmarket and newsl>0 then

sell at newsl stop

endif

if shortonmarket and newsl>0 then

exitshort at newsl stop

endif

if displaybe then

//graphonprice newsl coloured(244,102,27,255) as "breakevenstop"

endif

endif

// set stoploss

if enablesl then

if not onmarket then

sloss=0

elsif longonmarket then

sloss=tradeprice(1)-((tradeprice(1)*sl)/underlaying)*pointsize

elsif shortonmarket then

sloss=tradeprice(1)+((tradeprice(1)*sl)/underlaying)*pointsize

endif

set stop %loss sl

if displaysl then

graphonprice sloss coloured(255,0,0,255) as "stoploss"

sloss=sloss

endif

endif

// to display profittarget

if enablept then

if not onmarket then

ptarget=0

elsif longonmarket then

ptarget=tradeprice(1)+((tradeprice(1)*pt)/underlaying)*pointsize

elsif shortonmarket then

ptarget=tradeprice(1)-((tradeprice(1)*pt)/underlaying)*pointsize

endif

set target %profit pt

if displaypt then

//graphonprice ptarget coloured(121,141,35,255) as "profittarget"

ptarget=ptarget

endif

endif

// exit at closetime

if onmarket then

if time >= closetime or (currentdayofweek=5 and time>=closetimefr) then

sell at open stop

exitshort at open stop

endif

endif

// display days in market

if displaydim then

if not onmarket then

dim=0

endif

if (onmarket and not onmarket[1]) or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

dim=1

endif

if not (dayofweek=1 and hour = 1) then

if onmarket then

if openday <> openday[1] then

dim = dim + 1

endif

endif

endif

//graph dim coloured(121,141,35,255) as "days in market"

endif

if displaypp then

//graph pp coloured(0,0,0,255) as "positionperformance"

endif

//for trading all graph & graphonprice have to be comment out

//for backtesting and to have a visual idea of exits or pp

//uncomment and set displaysl and/or displaypt and/or displayts to 1

//maximum of 5 can be used to display lines (graph & graphonprice combined)