Here’s a new algo I’ve had on forward testing for a while (US Tech 100), so far consistent with the BT results. It’s all on moving averages and more or less approximates what I do in manual trading, except where I normally work on a 1min chart, this drops down to 30sec to make up for the 1 candle delay at the entry.

FOR:

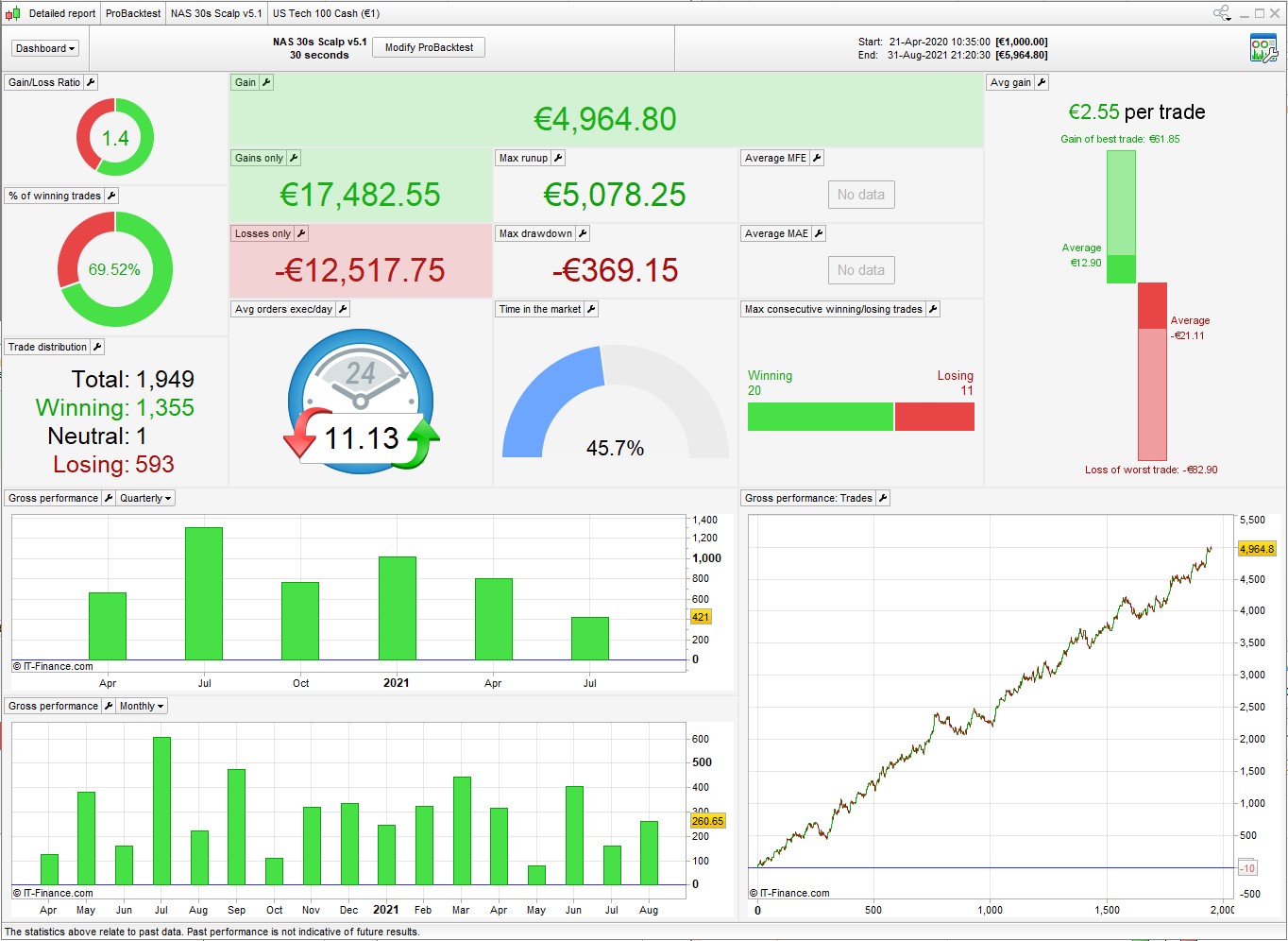

Very nice histogram, as good as it gets.

High number of trades in the BT (4 0r 5 per day)

Low drawdown

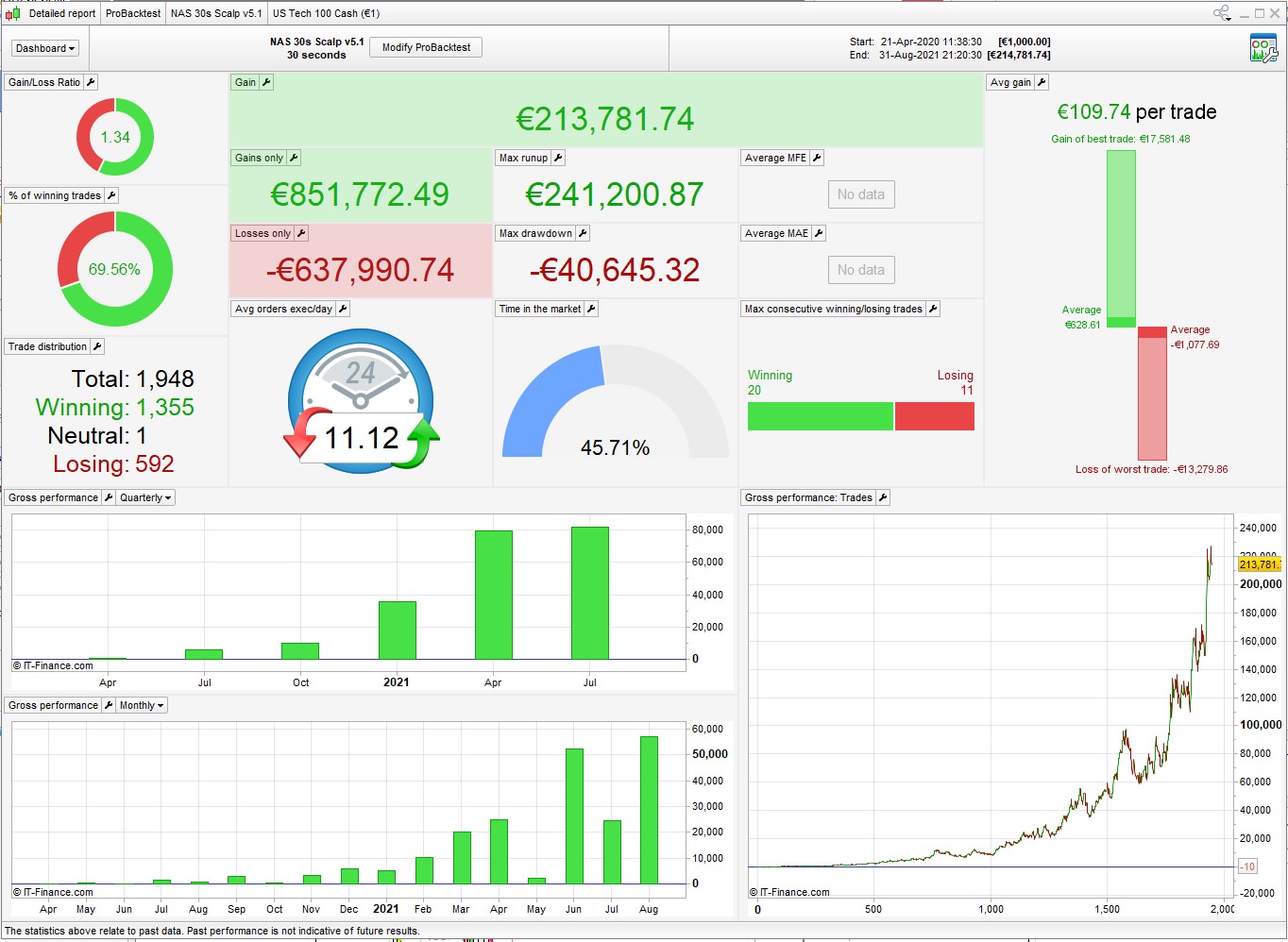

Spectacular ‘potential returns’ when MM is active (2nd pic – haha, dream on…🤣)

Against:

Very short BT, 17 months – assume it’s curve-fit to that period and would need regular reworking

Possibly over-optimized (???)

Stoploss is > Target profit, meaning that loss of worst trade is also > Gain of best trade – not good but unavoidable.

Very low gain per trade, easily eroded with slippage or at times of higher spread.

No WF, as I prefer to do out-of-sample testing in demo (closer to real trading conditions)

***Requires lengthy forward testing before going live***

As with most things in life – could be a winner, could crash and burn … who knows? Be sure to adjust the Tradetime for your time zone.

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 10000

//MONEY MANAGEMENT II

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 0.5

ENDIF

if MM then

MinSize = 0.5 // IG minimum position size allowed

MaxSize = 2000 // IG tier 2 margin limit

ProfitAccrued = 0 // when restarting strategy, enter profit or loss to date in instrument currency

DD = 370 //MinSize drawdown in instrument currency

Multiplier = 3 //drawdown multiplier

if ProfitAccrued + StrategyProfit >= DD*2 then

Multiplier = 2

endif

Capital = DD * Multiplier

Equity = Capital + ProfitAccrued + StrategyProfit

PositionSize = Max(MinSize, Equity * (MinSize/Capital))

if positionsize > MaxSize then

positionsize = MaxSize

endif

PositionSize = Round(PositionSize*100)

PositionSize = PositionSize/100

ENDIF

once tradetype = 1 // [1] long/short [2]long [3]short

once closeonreversal = 0

DLS =(Date >= 20100314 and date <=20100328) or (Date >= 20101031 and date <=20101107) or (Date >= 20110313 and date <=20110327) or (Date >= 20111030 and date <=20111106) or (Date >= 20120311 and date <=20120325) or (Date >= 20121028 and date <=20121104) or (Date >= 20130310 and date <=20130331) or (Date >= 20131027 and date <=20131103) or (Date >= 20140309 and date <=20140330) or (Date >= 20141026 and date <=20141102) or (Date >= 20150308 and date <=20150329) or (Date >= 20151025 and date <=20151101) or (Date >= 20160313 and date <=20160327) or (Date >= 20161030 and date <=20161106) or (Date >= 20170312 and date <=20170326) or (Date >= 20171030 and date <=20171105) or (Date >= 20180311 and date <=20180325) or (Date >= 20181028 and date <=20181104) or (Date >= 20190310 and date <=20190331) or (Date >= 20191027 and date <=20191103) or (Date >= 20200308 and date <=20200329) or (Date >= 20201025 and date <=20201101) or (Date >= 20210314 and date <=20210328) or (Date >= 20211031 and date <=20211107) or (Date >= 20220313 and date <=20220327) or (Date >= 20221030 and date <=20221106) or (Date >= 20230312 and date <=20230326) or (Date >= 20231029 and date <=20231105) or (Date >= 20240310 and date <=20240331) or (Date >= 20241027 and date <=20241103)

If DLS then

Tradetime = time >=133000 and time <200000//UK time

elsif not DLS then

Tradetime = time >=143000 and time <210000//UK time

endif

TIMEFRAME(15 minutes)

ma = average[a,t](typicalprice)

cb1 = ma > ma[1]

mb = average[p2,t2](typicalprice)

cs1 = mb < mb[1]

TIMEFRAME(5 minutes)

mc = average[a3,t3](typicalprice)

cb2 = (mc > ma)

cb3 = mc > mc[1]

md = average[a4,t4](typicalprice)

cs2 = (md < mb)

cs3 = md < md[1]

TIMEFRAME(default)

me = average[a5,t5](typicalprice)

cb4 = me > me[1] and me[1] < me[2]

mf = average[a6,t6](typicalprice)

cs4 = mf < mf[1] and mf[1] > mf[2]

CB = Tradetime and (cb1 or cb2) and cb3 and cb4

CS = Tradetime and (cs1 or cs2) and cs3 and cs4

// Conditions to enter long positions

if tradetype=1 or tradetype=2 then

IF not longonmarket and CB THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

ENDIF

ENDIF

if tradetype=2 and longonmarket and closeonreversal and CS then

sell at market

endif

// Conditions to enter short positions

if tradetype=1 or tradetype=3 then

IF not shortonmarket and CS THEN

sellshort positionsize CONTRACT AT MARKET

SET STOP %LOSS sls

SET TARGET %PROFIT tps

ENDIF

ENDIF

if tradetype=3 and shortonmarket and closeonreversal and CB then

exitshort at market

endif

//% Break even (high/low)

once breakeven =1

if breakeven then

breakevenPC = be // long

breakevenPCS = bes // short

PointsToKeep = pk

startBreakeven = tradeprice(1)*(breakevenPC/100)

startBreakevenS = tradeprice(1)*(breakevenPCS/100)

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND high-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-low>=startBreakevenS*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

endif

// trailing atr stop

once trailingstopATR = 1

if trailingstopATR then

//====================

once tsincrements = tsi // set to 0 to ignore tsincrements

once tsminatrdist = tsm

once tsatrperiod = tsa // ts atr parameter

once tsminstop = 4 // ts minimum stop distance

tssensitivity = 2 // 1 = close 2 = High/Low 3 = Low/High 4 = typicalprice (not use once)

//====================

if barindex=tradeindex then

trailingstoplong = tsl // ts atr distance

trailingstopshort = tss // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10))/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

mypositionpriceatr = 0

endif

positioncountatr = abs(countofposition)

if tsnewsl > 0 then

if positioncountatr > positioncountatr[1] then

if longonmarket then

tsnewsl = max(tsnewsl,positionprice * tsnewsl / mypositionpriceatr)

else

tsnewsl = min(tsnewsl,positionprice * tsnewsl / mypositionpriceatr)

endif

endif

endif

if tssensitivity=1 then

tssensitivitylong=close

tssensitivityshort=close

elsif tssensitivity=2 then

tssensitivitylong=high

tssensitivityshort=low

elsif tssensitivity=3 then

tssensitivitylong=low

tssensitivityshort=high

elsif tssensitivity=4 then

tssensitivitylong=typicalprice

tssensitivityshort=typicalprice

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-positionprice>=tgl then

if tsmaxprice-positionprice>=tsminstop then

tsnewsl=tsmaxprice-tgl

else

tsnewsl=tsmaxprice-tsminstop

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if positionprice-tsminprice>=tgs then

if positionprice-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs

else

tsnewsl=tsminprice+tsminstop

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

mypositionpriceatr = positionprice

endif

//===================================

RSIexit = 1 // in profit

if RSIexit then

myrsi=rsi[r](close)

if myrsi<rl and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsi>rs and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

endif