Being always ON MARKET the MM part will never run as it is now, but you can replace IF NOT ON MARKET THEN with:

IF StrategyProfit <> StrategyProfit[1] THEN

because each time a trade is closed (no matter whether a new one is started at the same time), STRATEGYPROFIT is updated, so it will be different than it was the previous candle.

Another solution would be replacing IF NOT ONMARKET THEN with:

IF (LongOnmarket AND ShortOnMarket[1]) OR (LongOnmarket[1] AND ShortOnMarket)

which checks whenever a different positions has been entered (and the previous one closed).

I prefer the first solution.

This way you will be able to execute the MM part to manage the position size.

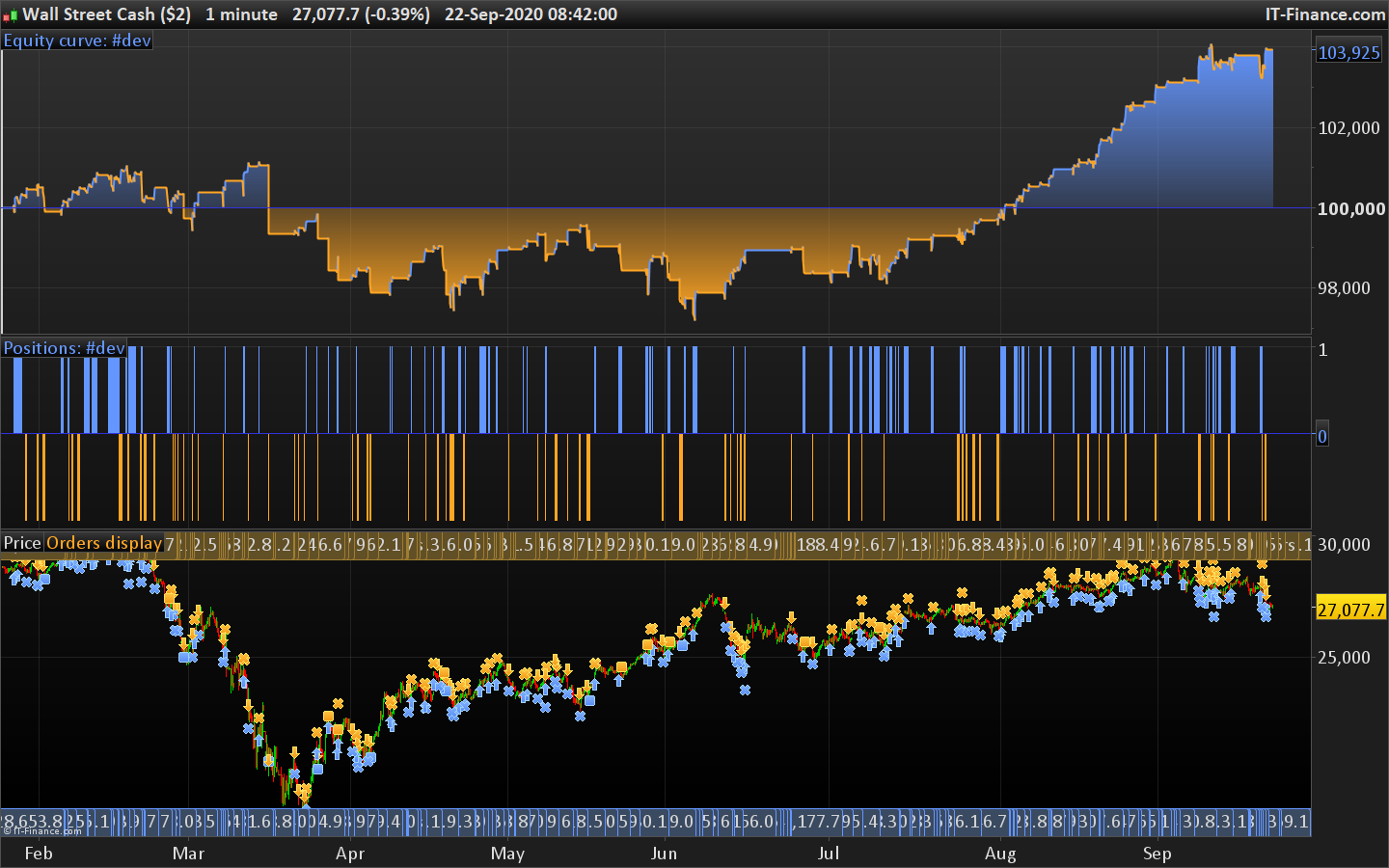

Anyone can run this on 200k?

DJI-1m

Could be too curve fitted, but interesting to see how it goes. Thanks in advance.

Defparam CumulateOrders = false

TIMEFRAME(5 minutes, updateonclose)

mac = MACD[8,6,4]

bull5 = mac > 0

bear5 = mac < 0

TIMEFRAME(2 minutes, updateonclose)

bull2 = Average[5] > Average[13]

bear2 = Average[5] < Average[13]

TIMEFRAME(default)

Period= 7

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

Periodb= 42

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

Periodc= 17

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c1 = HULLb > HULLa

c2 = HULLb < HULLa

c3 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c4 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

c5 = HULLc > HULLc[1]

c6 = HULLc < HULLc[1]

bull = c1 and c3 and c5 and bull5 and bull2

bear = c2 and c4 and c6 and bear5 and bear2

//Timeframe(default)

//Once BB = 20

//Once p = 54

//MaxbbUP = highest[p](BollingerUp[BB](close)) and bull

//MinbbDN = lowest[p](BollingerDown[BB](close)) and bear

//MyAdx = (summation[p](Adx[14] < 25) = p)

//If MyAdx then

//Buy 1 contract at MaxbbUP Stop

//Sellshort 1 contract at MinbbDN Stop

//Endif

//// Conditions to enter long positions

IF NOT LongOnMarket AND bull THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

//

//// Conditions to exit long positions

//If LongOnMarket AND YourConditions THEN

//SELL AT MARKET

//ENDIF

//

//// Conditions to enter short positions

IF NOT ShortOnMarket AND bear THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

//

//// Conditions to exit short positions

//IF ShortOnMarket AND YourConditions THEN

//EXITSHORT AT MARKET

//ENDIF

// Stops and targets : Enter your protection stops and profit targets here

//SET STOP %LOSS 1

SET STOP pLoss 300

//SET TARGET pProfit 100

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = .03//.05 // set to 0 to ignore tsincrements

once tsminatrdist = 1//3

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 2 // ts atr distance

trailingstopshort = 2 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

That’s indeed overfitted over the last 100k bars.

Thanks @Nicolas.

I thought so 🙂

Anyone have any inputs how it can be improved further?

Prolly optimization expert @nonetheless ?