Hi All,

I was wondering if it is possible to replicate an indicator from TradingView.

It is called Nadaraya-Watson: Rational Quadratic Kernel (Non-Repainting). On the charts, it kind of looks like a regular Moving Average. But you can set the lines based on another timefrime

You can find more info and the code on TV

Thank you

Hi,

thanks. but that looks like the Envelope and not the Rational Quadratic Kernel (Non-Repainting), no?

Sorry, I recognised the name and gave the forum link assuming you were after the mid-line (the y2 variable of the return line), if what you’re after is not the same as this y2 then I don’t remember other Nadaraya-Watson code already made in the forum, Nicolas will assess whether it can be converted (and if yes will add it to the conversions list).

It is the same as the y2 line from the above code, apart that in that version the line takes color following another 2 period lag line crossing.

Added to the conversion list in order to get the same as this one.

Ok, so it is not possible to create the same indicator as I posted initially?

Yes it is possible, please be patient 😉

Done!

// © jdehorty

// @version=5

// A non-repainting implementation of Nadaraya-Watson Regression using a Rational Quadratic Kernel.

// Settings

once bullishR = 0

once bullishG = 250

once bullishB = 154

once bearishR = 255

once bearishG = 69

once bearishB = 0

src = customclose

// hh = Lookback Window, minval=3.0, tooltip='The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars. Recommended range: 3-50

r = rr*0.25

//rr = Relative Weighting, step=0.25, Relative weighting of time frames. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel. Recommended range: 0.25-25 => RR from 1 to 100

//xx = 25, Start Regression at Bar, Bar index on which to start regression. The first bars of a chart are often highly volatile, and omission of these initial bars often leads to a better overall fit. Recommended range: 5-25

//smoothColors = false, Smooth Colors, tooltip=Uses a crossover based mechanism to determine colors. This often results in less color transitions overall

//lag = 2, Lag for crossover detection. Lower values result in earlier crossovers. Recommended range: 1-2

//size = array.size(array.from(src)) // size of the data series

size = Min(Barindex,Maxlength)

// Further Reading:

// The Kernel Cookbook: Advice on Covariance functions. David Duvenaud. Published June 2014.

// Estimation of the bandwidth parameter in Nadaraya-Watson kernel non-parametric regression based on universal threshold level. Ali T, Heyam Abd Al-Majeed Hayawi, Botani I. Published February 26, 2021.

// Estimations

currentWeight = 0

cumulativeWeight = 0

for i = 0 to Size-xx-1 do

y = src[i]

w = POW(1+(POW(i,2)/(POW(hh,2)*2*r)),-r)

currentWeight = currentWeight + y*w

cumulativeWeight = cumulativeWeight + w

Next

yhat1 = currentWeight / cumulativeWeight

currentWeight = 0

cumulativeWeight = 0

for i = 0 to Size-xx-1 do

y = src[i]

w = POW(1+(POW(i,2)/(POW(hh-lag,2)*2*r)),-r)

currentWeight = currentWeight + y*w

cumulativeWeight = cumulativeWeight + w

Next

yhat2 = currentWeight / cumulativeWeight

// Rates of Change

wasBearish = yhat1[2] > yhat1[1]

wasBullish = yhat1[2] < yhat1[1]

isBearish = yhat1[1] > yhat1

isBullish = yhat1[1] < yhat1

isBearishChange = isBearish and wasBullish

isBullishChange = isBullish and wasBearish

// Crossovers

isBullishCross = yhat2 crosses over yhat1

isBearishCross = yhat2 crosses under yhat1

isBullishSmooth = yhat2 > yhat1

isBearishSmooth = yhat2 < yhat1

// Colors

If isBullishSmooth then

colorByCrossR = bullishR

colorByCrossG = bullishG

colorByCrossB = bullishB

Else

colorByCrossR = bearishR

colorByCrossG = bearishG

colorByCrossB = bearishB

Endif

If isBullish then

colorByRateR = bullishR

colorByRateG = bullishG

colorByRateB = bullishB

Else

colorByRateR = bearishR

colorByRateG = bearishG

colorByRateB = bearishB

Endif

If smoothColors then

R = colorByCrossR

G = colorByCrossG

B = colorByCrossB

Else

R = colorByRateR

G = colorByRateG

B = colorByRateB

Endif

// Alert Variables

If smoothColors then

alertBullish = isBearishCross

Else

alertBullish = isBearishChange

Endif

If smoothColors then

alertBearish = isBullishCross

Else

alertBearish = isBullishChange

Endif

// Alerts for Color Changes

//alertcondition(condition=alertBullish, title='Bearish Color Change', message='Nadaraya-Watson: {{ticker}} ({{interval}}) turned Bearish ▼')

//alertcondition(condition=alertBearish, title='Bullish Color Change', message='Nadaraya-Watson: {{ticker}} ({{interval}}) turned Bullish ▲')

// Non-Displayed Plot Outputs (i.e., for use in other indicators)

//plot(alertBearish ? -1 : alertBullish ? 1 : 0, "Alert Stream", display=display.none)

Return yhat1 as "Rational Quadratic Kernel Estimate" style(line,4) coloured(R,G,B,255)

Haha ok will do. Thank you!

Oh wow, many thanks. Will try it over the weekend.

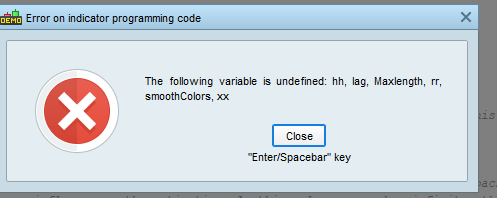

I get this error message. On which rows am I suppose to add values?

sorry, really new to coding

thank you

JS

JSParticipant

Veteran

Hi @Harem

Download the itf -file and import the itf-file under indicators…

Now you have the complete code including the parameters…

(So, don’t copy the code from the forum but download the itf-file)

much appreciated. Thank you

Hi,

sorry, one more question. Do I have to have the maxlength parameter? or is there a default nr for that?

I added Maxlength because otherwise the indicator is very slow.

I just translate the original code (without improving it to be faster, which is possible) and it seems it uses all barindex for calculation (which is not relevant too because it does not change the result after 200 or 300 bars).

That is why i added Maxlength (too lazzy for improving the code)

But you can change 400 to 2000 or more if you want, you will notice no change in the result exept more time of calculation

ps : Lamaille is me