jebus89 – thanks for these very interesting insights (very rare in this forum…)!

I don’t think you need any advices since you are doing obviously many things right. but allow me just few inspirations. “risk appetite” is of course everybody’s personal decision, yet I think almost everybody is (massively) overestimating his psychological ability to sustain big and/or long-lasting losses, at least in the beginning. accepting drawdown up to 50% of capital sounds to me like total hardcore, since surviving both financially and psychologically is priority #1, being long-term profitable is “just” #2. try to cut your risk in half – and your psychological comfort will increase 10 times. cut your risk again in half – and your peace of mind will increase 100 times. I know what many would answer to this approach, like “but profits will also go down accordingly!..” yep, they sure will, but see again above priority #1.

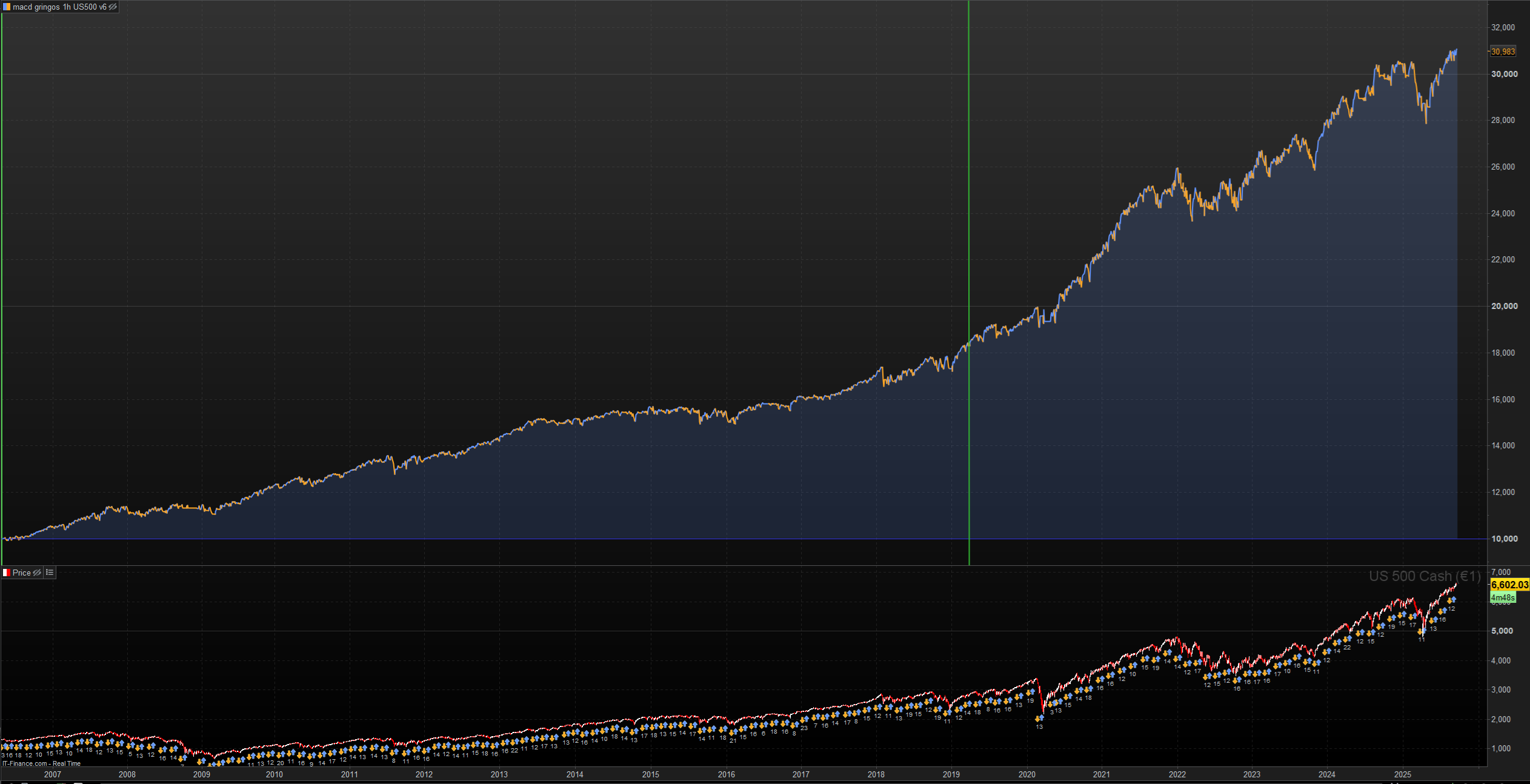

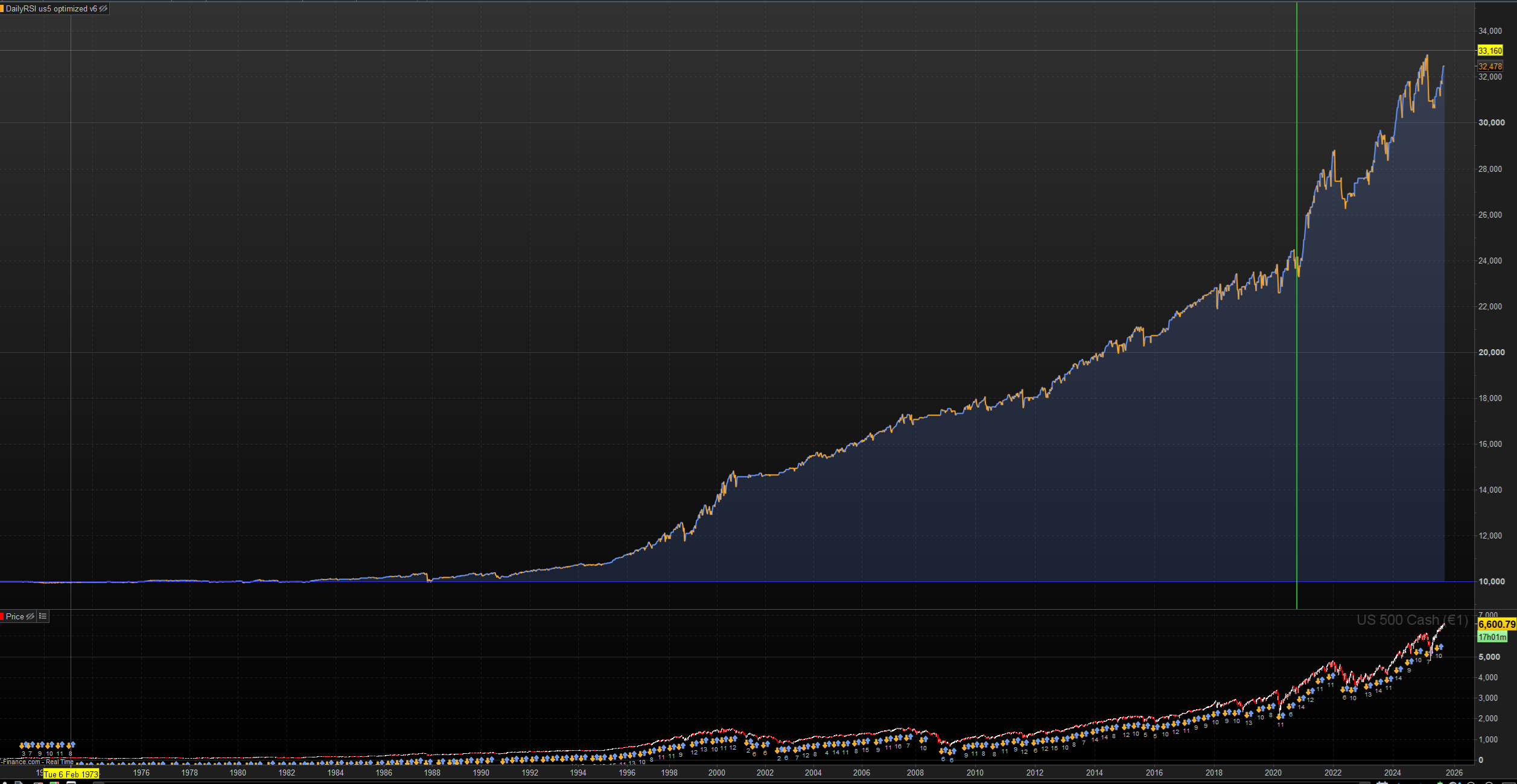

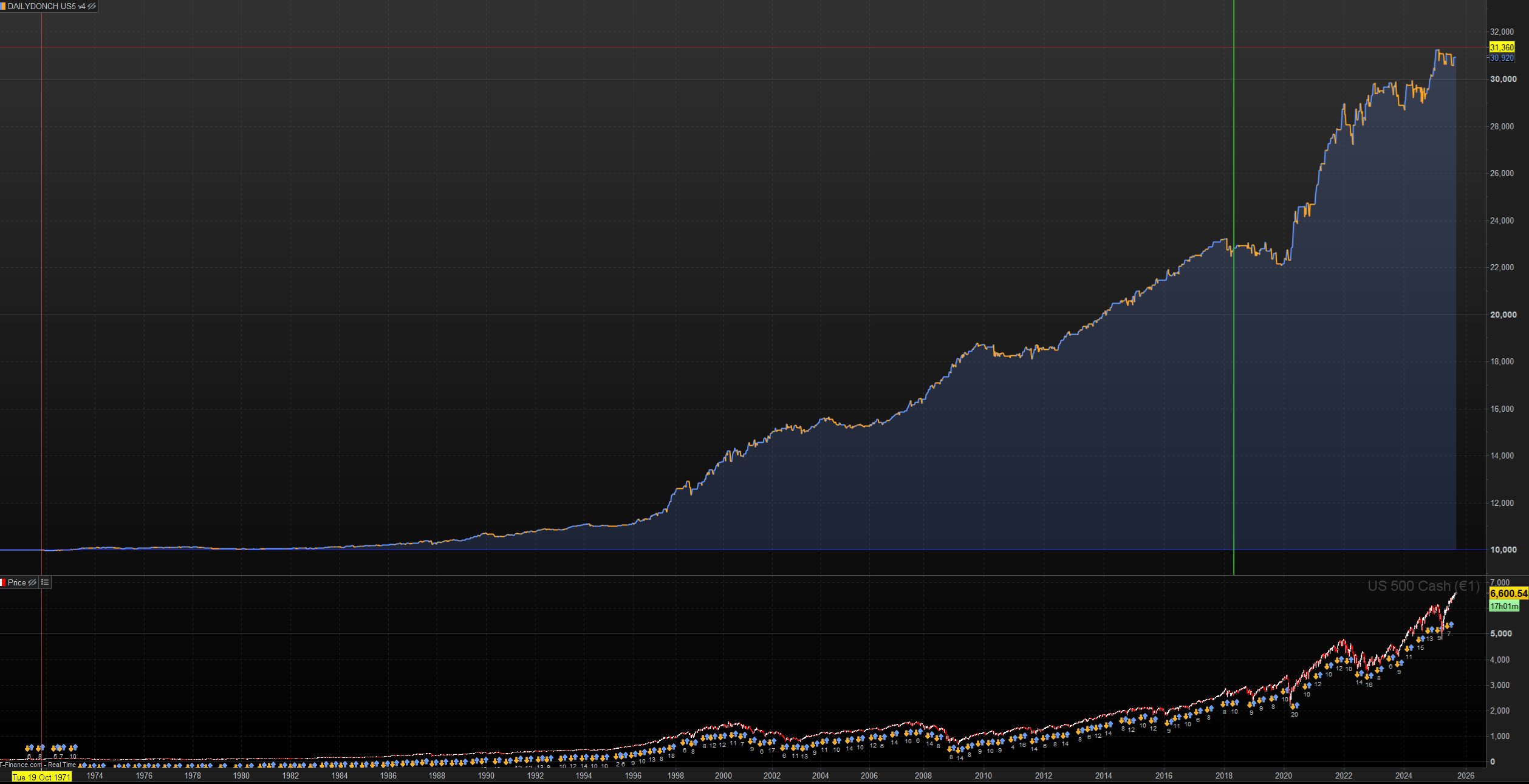

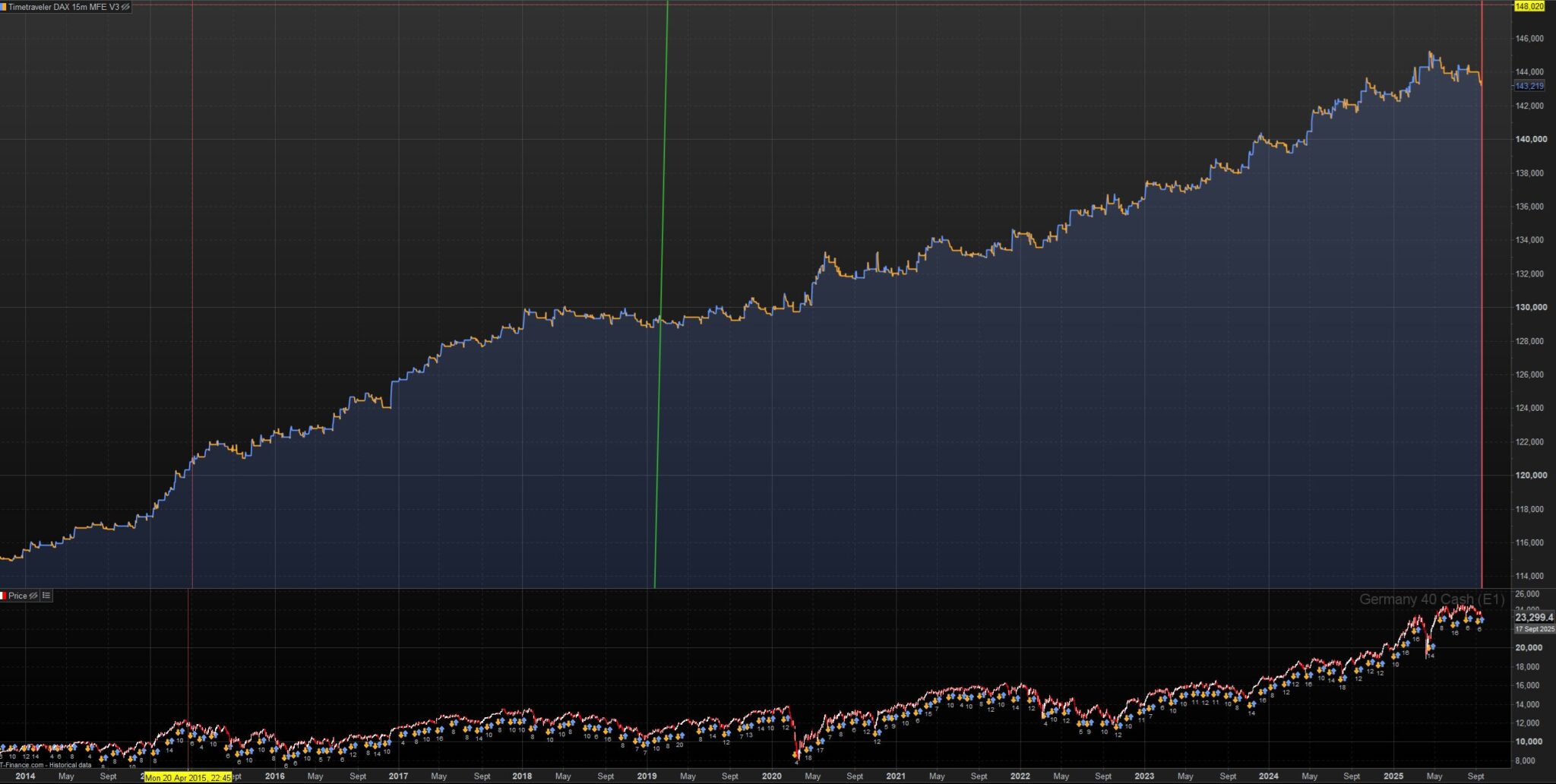

did you think already about moving to futures trading? they have so many very serious advantages vs cfd, among them – no overnight fees. most of my strategies carry positions for several days very frequently, and in rare cases even for up to few weeks. I figured out same/similar like you: those fees cost arround 10% of the performance per year on whole strategy-portfolio. it was definetely not the major reason why I approx 2 years ago started to move stepwise my algos to futures, but one of those few very significant reasons definetely. possibly due to higher margin requirements you will not be able to run all your algos with futures, but still you could select some 2-3 (or at least 1, why not…), most uncorrelated, most robust strategies, and those which catch and ride trends frequently continuing multiple days. and run all others still with cfd. by now only 2% of my capital is with cfd, and I do not regret it for any single day. actually I could close my cfd accounts, but I keep them, run there exactly those algos which I can’t trade / don’t want to trade with futures due to limited capital, running them just for fun, for example in order to see how they perform live vs. backtest (never using walk-forward in the backtest, and never using demo-shmemo account…)

cheers

justisan

Thanks for the reply!

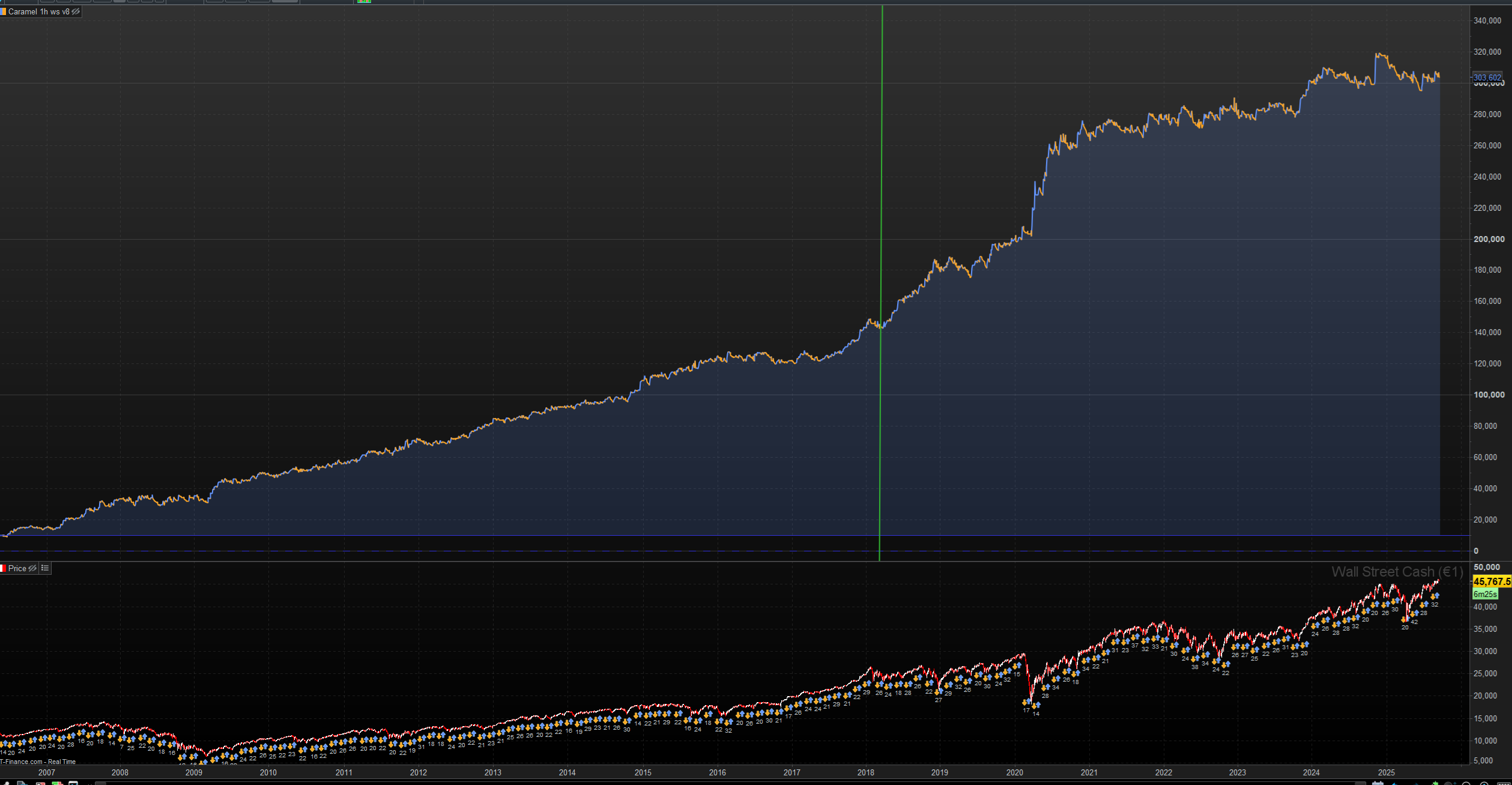

You are SO right about the” -50% is hell on your mental health”. The self doubting, the self loathing, the loss of confidence and the inability to keep working as normal on your algos and trading, when every time you log in, you wonder why even bother.. I think honestly you’re right, and its not for everyone.. However, as for now when my account peaked at 55k (currently at 35k) its not enough money for me to want to tune it down. Im going to ride out the hardships and learn from the immense pain it is to see your account -30% and -40% and even -50%.. WHEN, ;), i reach 100k++ i will for sure tune down my risk appetite.

Is it worth running your account down to -50% for “quicker profits” (and more risky profits..)? Im not 100% sure to be honest.. It really does take a toll on you… I will say that it definitely makes you stronger mentally to go through it, but it also hurts so much that it does hinder my work with algos because you become demotivated.

The first time i saw -50% it felt like it was all over, i could just throw in the towel and give up on my dreams. The second time it happened its not as bad as the first time.. but i would lie if i said that i didnt feel the fear.. the fear of failing, the fear of being proven wrong..

And im not saying $10-50K is insignificant money, but money comes and money goes, it wouldnt ruin my life if i lost 100%. The most painful part is knowing i “did it wrong” and i failed at what im doing… This is my “Passion project”, i still work full time and i dont plan on quitting my day job anytime soon.. So what im saying is that one thing is that the money would be lost, that would suck but wouldnt break me. Being proven wrong and failing is what truly hurts..

I really want to thank you tho, what youre saying comes from a compassionate place within you. Im really glad you chose to write your reply to me!

Regarding the futures, i haven’t really checked it out to be honest. Is it easy to find a broker that allows you to trade algos with real futures? I thought it was restricted to US markets and/or pro’s? Whats the capital needed to hold 1 futures contract on say Dow jones or SP500?