Hi:

I have a problem in which the back-test takes multiple orders in one bar. Mt system is a pyramiding strategy that takes additional positions every time price goes up by 2ATR however, it seems to take on multiple orders on the same bar every time there is a large candle and/or ATR goes up significantly. From the code, it should be taking one position per candle only.

Can anyone tell me what’s wrong? Thank you.

Ruben

Because all the conditions for a new order to open are exactly the same: Close>open+ATR (same Open, same Close and same ATR).

Not quite because there is no problem on the previous 3 transactions (in the attachment). It happens on other instruments as well, the code works well unless there is a large candle, it is only on the large candles that it does this, it executes multiple orders at exactly the same price. However, from the code, it should be recording the close of the candle as a reference for the next transaction. It should also be processing every candle only once.

Even if all conditions were the same you would see trades on every candle, not multiple transactions on the same candle at the same price. The IF/ENDIF conditions should prevent that shouldn’t it?

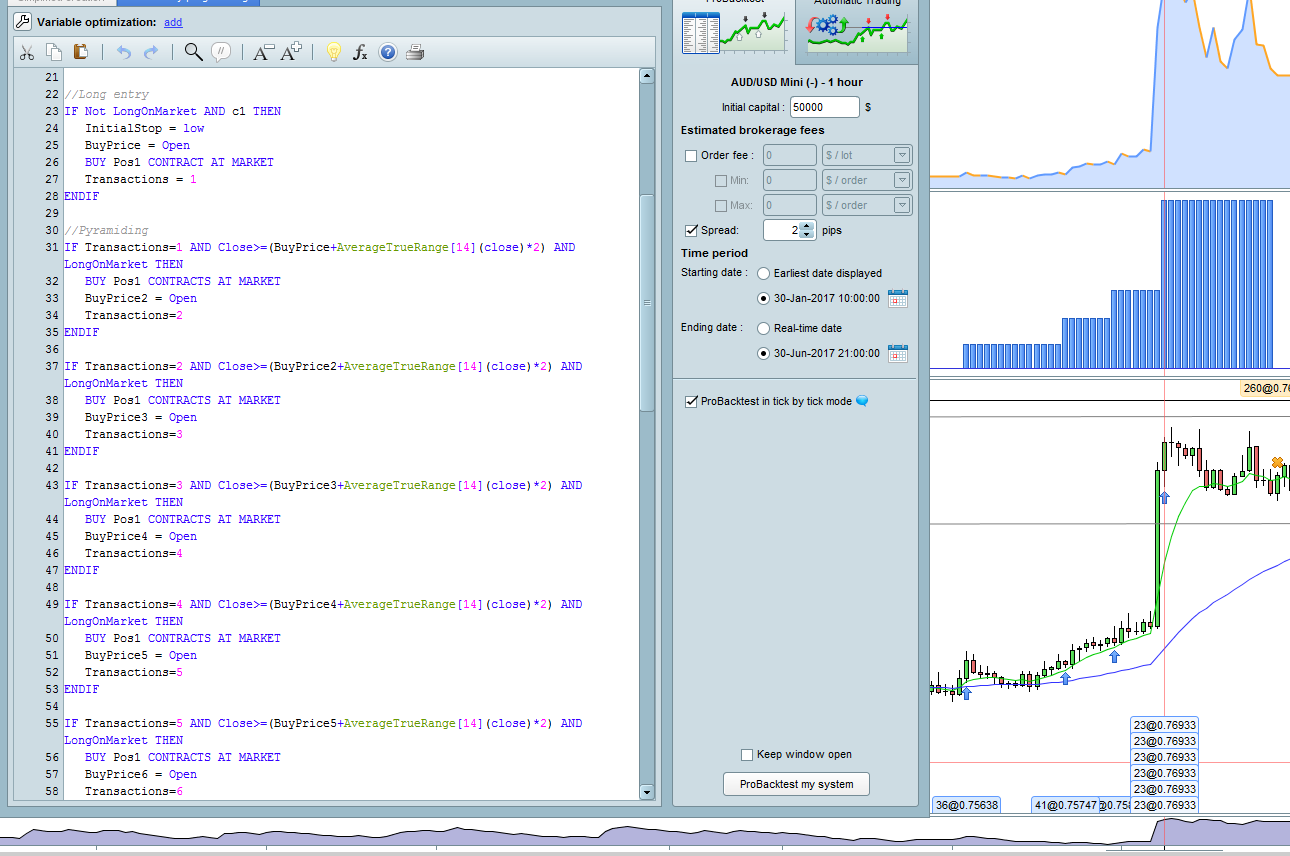

Here’s the code.

Has anyone seen this before? Thanks in advance

// Definition of code parameters

DEFPARAM CumulateOrders = True // Cumulating positions activated

DEFPARAM NoCashUpdate = False //For backtest only - pg 22

// Conditions to enter long positions

indicator1 = ExponentialAverage[8](close)

indicator2 = ExponentialAverage[50](close)

c1 = (indicator1 CROSSES OVER indicator2)

Equity = 50000

Risk = Equity*0.01

FXinAUD=1.50 //Exchange rate for quote currency in to AUD (1 equals = ??AUD)

FXrate = 1/FXinAUD //Add line ABOVE for non-AUD contracts with the FX rate of quote currency in AUD

ContractSize = 10000

ATRdistance = AverageTrueRange[14](close)*2

Risk1 = ATRdistance*ContractSize //Risk per contract in quote currency

ContractRisk = Risk1*Fxrate

Pos1 = Risk/ContractRisk

IF Not OnMarket THEN

Transactions = 0

ENDIF

//Long entry

IF Not LongOnMarket AND c1 THEN

InitialStop = low

BuyPrice = Open

BUY Pos1 CONTRACT AT MARKET

Transactions = Transactions + 1

ENDIF

//Pyramiding

IF Transactions=1 AND Close>=(BuyPrice+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice2 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=2 AND Close>=(BuyPrice2+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice3 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=3 AND Close>=(BuyPrice3+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice4 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=4 AND Close>=(BuyPrice4+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice5 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=5 AND Close>=(BuyPrice5+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice6 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=6 AND Close>=(BuyPrice6+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice7 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=7 AND Close>=(BuyPrice7+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice8 = Open

Transactions = Transactions + 1

ENDIF

IF Transactions=8 AND Close>=(BuyPrice8+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice9 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=9 AND Close>=(BuyPrice9+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice10 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=10 AND Close>=(BuyPrice10+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice11 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=11 AND Close>=(BuyPrice11+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice12 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=12 AND Close>=(BuyPrice12+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice13 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=13 AND Close>=(BuyPrice13+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice14 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=14 AND Close>=(BuyPrice14+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

BuyPrice15 = Close

Transactions = Transactions + 1

ENDIF

IF Transactions=15 AND Close>=(BuyPrice15+AverageTrueRange[14](close)*2) AND LongOnMarket THEN

BUY Pos1 CONTRACTS AT MARKET

ENDIF

// Conditions to exit long positions

ATRx = AverageTrueRange[14](close)*2

StopLoss = CALL "2ATR trailing stop"

IF LongOnMarket AND close <= Buyprice + ATRx AND InitialStop>StopLoss THEN

SELL AT InitialStop STOP

ELSE

SELL AT StopLoss STOP

ENDIF

Yes , it appears on large candle, when the Close is superior to previous “BuyPrice” with 2 ATR, so it never happens on small candle (because ATR is small).

The problem is that each time you open an order you increase the “transactions” variable and this is the only variable tested to open a new order (because your Close>Buyprice+ATR*2 condition is always the same) and since the code is read from to to bottom, you add continuously new order (from line 32 to 119).

Hi Nicholas:

The “BuyPrice” is also supposed to change after every pyramid trade: Buyprice2…Buyprice3… is this variable being ignored?

BTW, thanks for your reply. Is there a way to make it execute each pyramid only once? (I tried “ONCE” in combination with IF but it doesn’t work)

Nicholas:

Don’t worry, I solved it.

Cheers.

No, the BuyPrice don’t change because you are constantly storing the same value on the same candle. You can use TRADEPRICE instead, which refer to the real open price of the last N order.