I was building a simple multi timeframe strategy based on the Absolute Strength indicator:

Absolute Strength

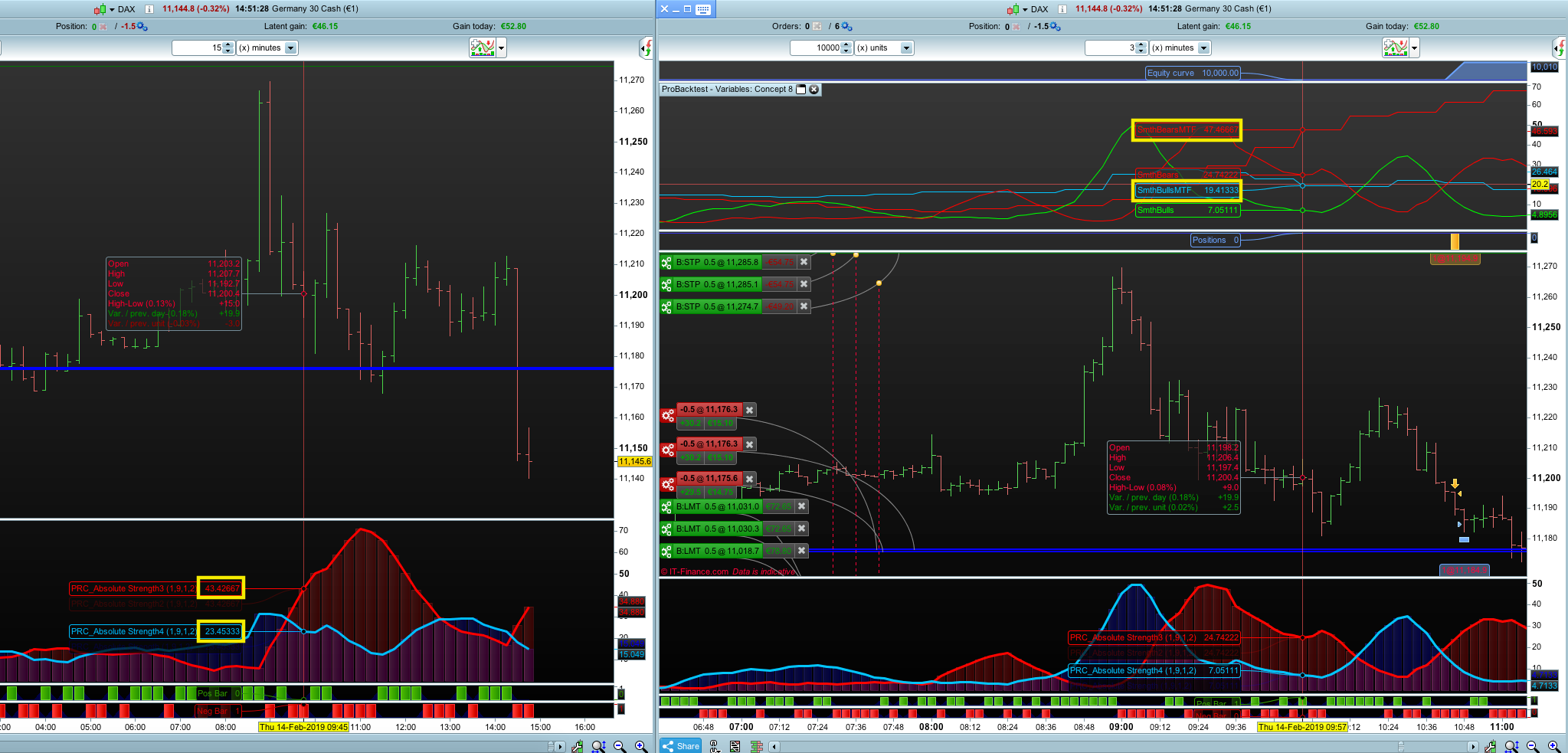

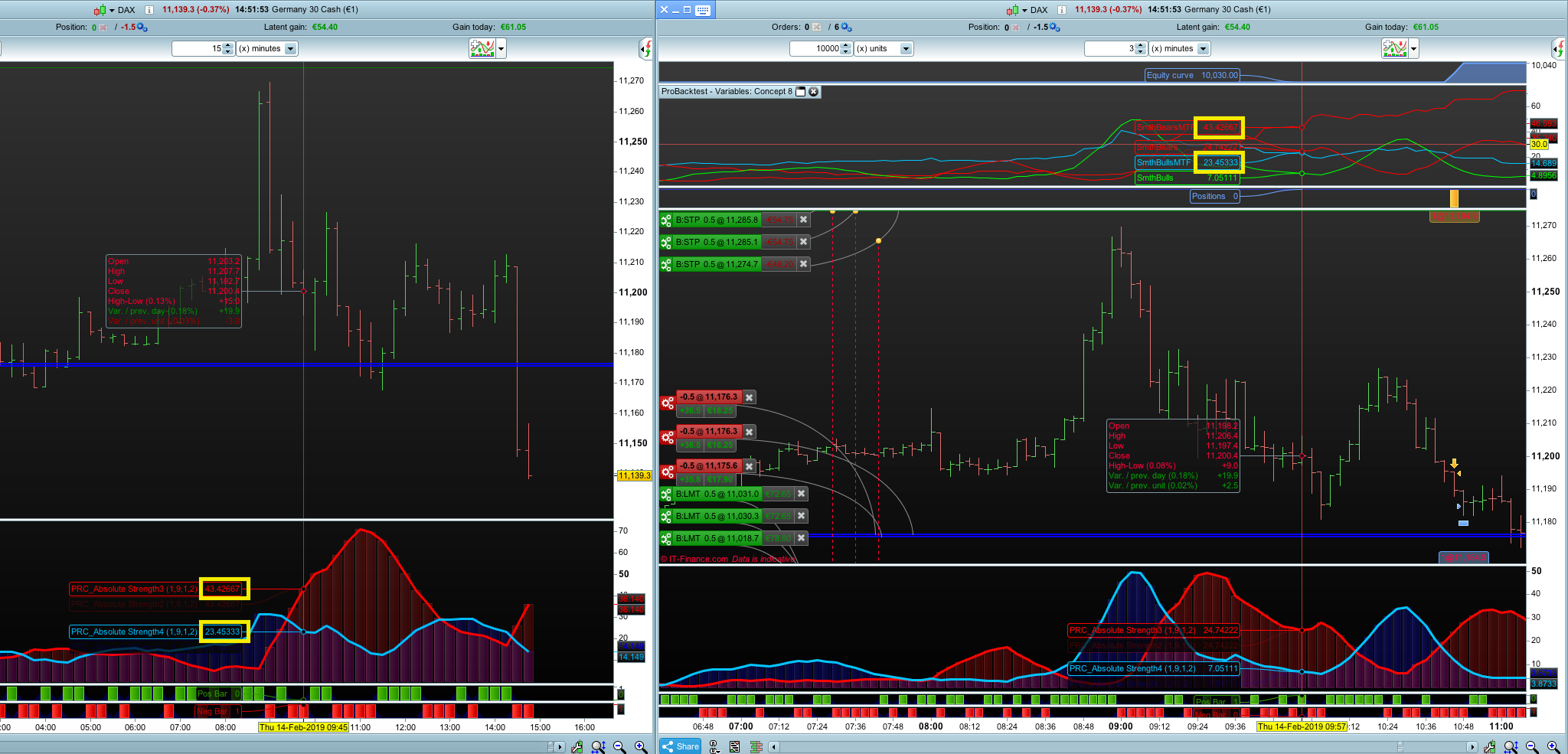

I am using the 3 Min chart of the Germany 30 Cash index as my current timeframe and the 15 Min chart for my higher timeframe.

I am also using the Graph function to make sure I get the correct values for the Absolute Strenght lines.

When looking at the Graph output, I noticed that when I use the condition “Timeframe(15 minutes,updateonclose)”, the Absolute Strength lines of the 15 Min timeframe slightly differ from the “true” values on the 15 Min chart.

However, when I use the condition “Timeframe(15 minutes)” [without, updateonclose], the Absolute Strenght lines are correct.

I would rather like to use the updateonclose condition for my strategy, so I would like to find out why this difference exist and if it can be fixed?

Below you can find my code and some screenshots to further illustrate my problem (I realise it probably isn’t the best looking code, especially the way I handled the MTF bit, but thats due to my lack in coding experience – mayby that’s why I have this problem in the first place)

//-------------------------------------------------------------------------

// Main code : AbsStrength (3M) - Concept 8

//-------------------------------------------------------------------------

Defparam Cumulateorders = False

//15 minute timeframe conditions

Timeframe(15 minutes,updateonclose)

//Absolute Strength Indicator START

// --- settings

ModeMTF = 1 // 0-RSI method 1-Stoch method

LengthMTF = 9 // Period

SmoothMTF = 1 // Period of smoothing

ModeMAMTF = 2 // Mode of Moving Average

// --- end of settings

if barindex>max(LengthMTF,SmoothMTF) then

Price1MTF=customclose

Price2MTF=customclose[1]

if ModeMTF=0 then

BullsMTF=0.5*(Abs(Price1MTF-Price2MTF)+(Price1MTF-Price2MTF))

BearsMTF=0.5*(Abs(Price1MTF-Price2MTF)-(Price1MTF-Price2MTF))

endif

if ModeMTF=1 then

smaxMTF=Highest[LengthMTF](high)

sminMTF=Lowest[LengthMTF](low)

BullsMTF=Price1MTF - sminMTF

BearsMTF=smaxMTF - Price1MTF

endif

AvgBullsMTF=average[LengthMTF,ModeMAMTF](BullsMTF)

AvgBearsMTF=average[LengthMTF,ModeMAMTF](BearsMTF)

SmthBullsMTF=average[SmoothMTF,ModeMAMTF](AvgBullsMTF)

SmthBearsMTF=average[SmoothMTF,ModeMAMTF](AvgBearsMTF)

endif

//Absolute Strength Indicator END

//"default" timeframe conditions

Timeframe(default)

//Size & Targets

Positionsize = 1

PTL = 10

SLL = 10

PTS = 10

SLS = 10

// Day & Time

Once Entertime = 090000

Once Lasttime = 173000

Tt1 = Time >= Entertime

Tt2 = Time <= Lasttime

Tradetime = Tt1 And Tt2

//Absolute Strength Indicator START

// --- settings

Mode = 1 // 0-RSI method 1-Stoch method

Length = 9 // Period

Smooth = 1 // Period of smoothing

ModeMA = 2 // Mode of Moving Average

// --- end of settings

if barindex>max(Length,Smooth) then

Price1=customclose

Price2=customclose[1]

if Mode=0 then

Bulls=0.5*(Abs(Price1-Price2)+(Price1-Price2))

Bears=0.5*(Abs(Price1-Price2)-(Price1-Price2))

endif

if Mode=1 then

smax=Highest[Length](high)

smin=Lowest[Length](low)

Bulls=Price1 - smin

Bears=smax - Price1

endif

AvgBulls=average[Length,ModeMA](Bulls)

AvgBears=average[Length,ModeMA](Bears)

SmthBulls=average[Smooth,ModeMA](AvgBulls)

SmthBears=average[Smooth,ModeMA](AvgBears)

endif

//Absolute Strength Indicator END

//"default" timeframe

Timeframe(default)

//Entry & Exit Conditions

If Tradetime Then

If SmthBulls>SmthBears and SmthBulls[1]<SmthBears[1] and SmthBullsMTF>SmthBearsMTF and SmthBullsMTF>SmthBullsMTF[1] and SmthBearsMTF<SmthBearsMTF[1] Then

Buy Positionsize Contract At Market

SET TARGET PROFIT PTL

Set Stop loss SLL

Endif

Endif

If Tradetime Then

If SmthBulls<SmthBears and SmthBulls[1]>SmthBears[1] and SmthBullsMTF<SmthBearsMTF and SmthBullsMTF<SmthBullsMTF[1] and SmthBearsMTF>SmthBearsMTF[1] Then

Sellshort Positionsize Contract At Market

SET TARGET PROFIT PTS

Set Stop loss SLS

Endif

Endif

graph SmthBullsMTF coloured(0,191,255)

graph SmthBearsMTF coloured(255,0,0)

graph SmthBulls coloured (0,300,0)

graph SmthBears coloured (300,0,0)