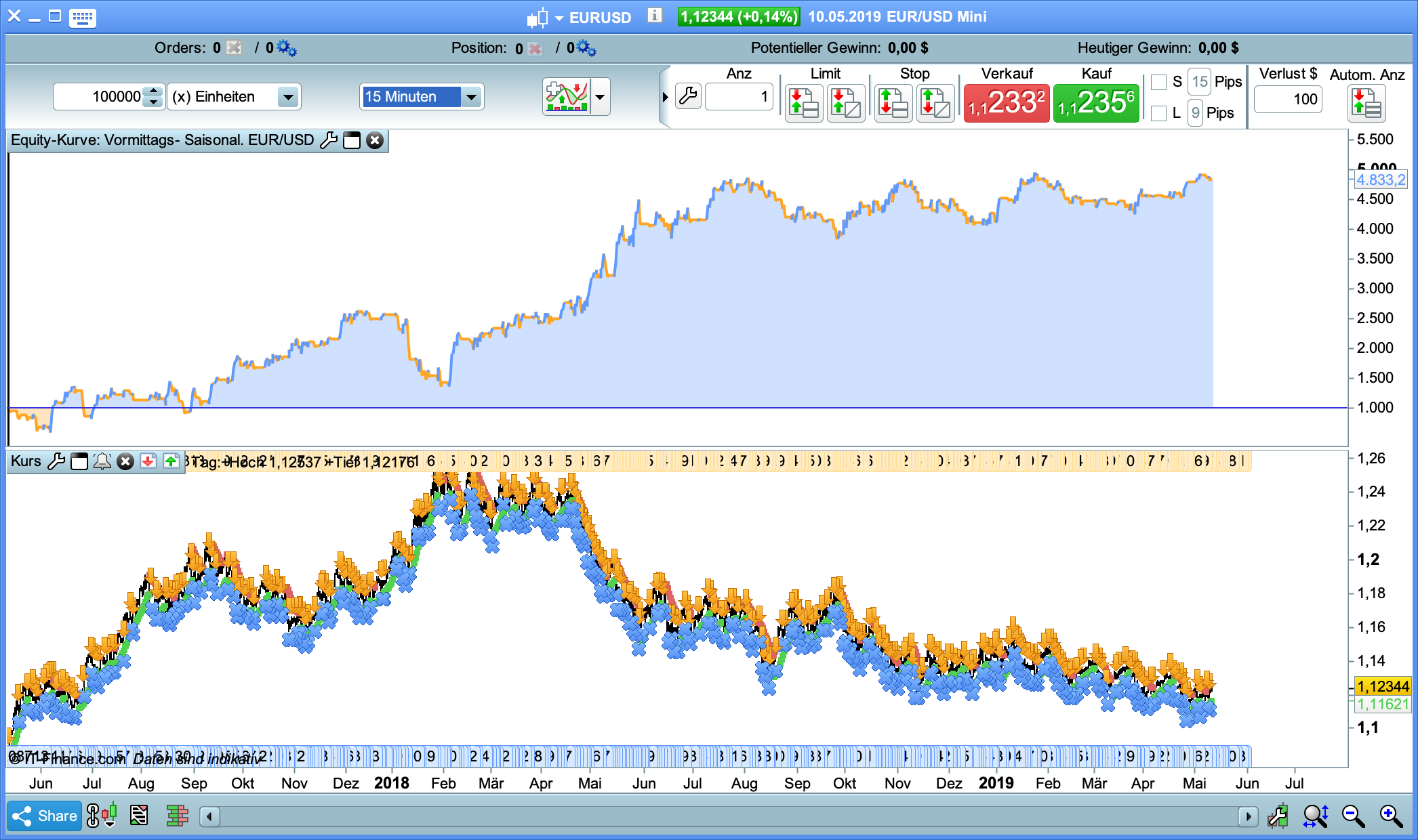

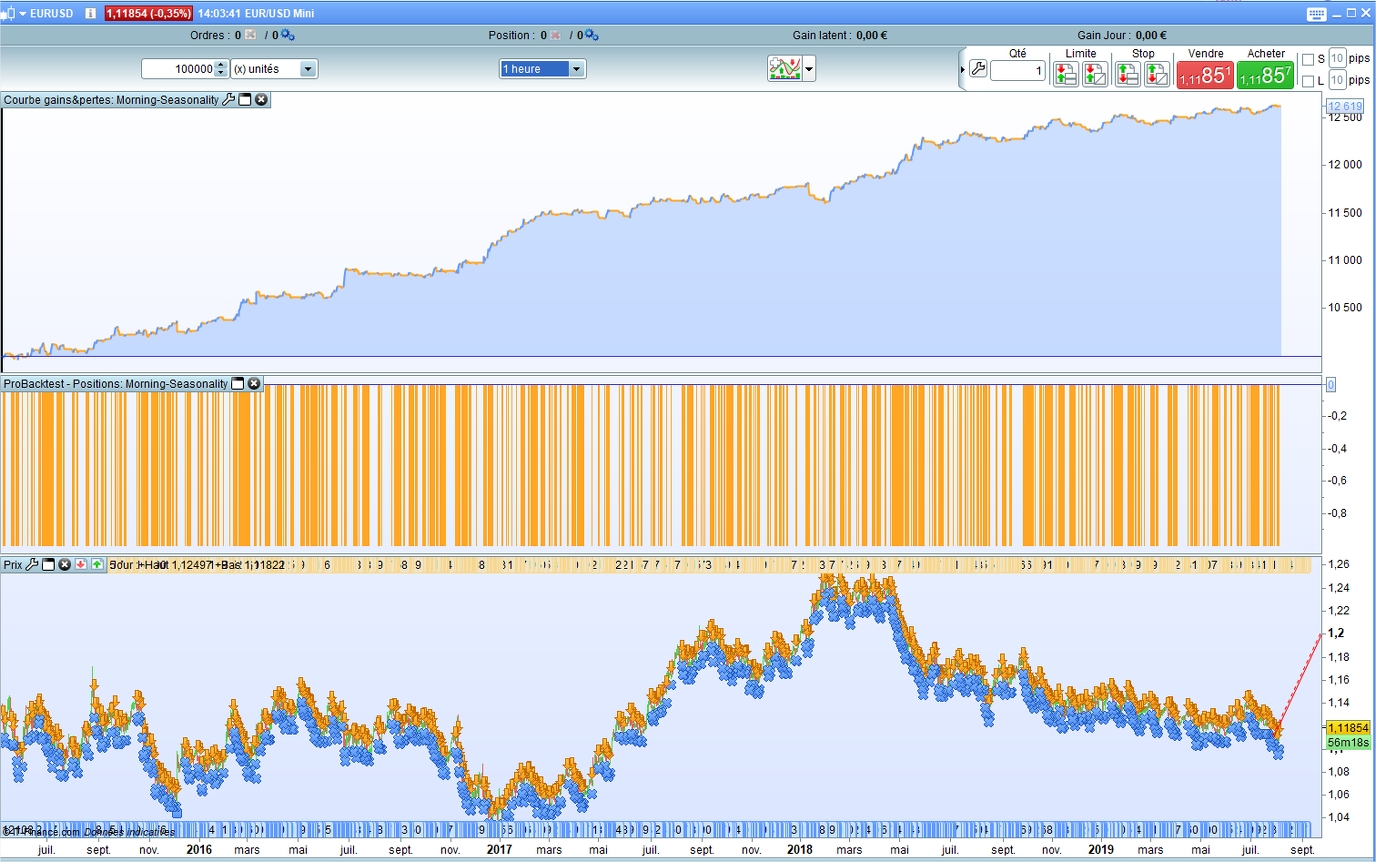

I would like to introduce a very nice and simple strategy. Unfortunately it is not mine. I found it on https://www.trading-treff.de/wissen/handelsstrategie-fuer-daytrader-im-eurusd-backtest-inklusive and rebuilt it once. It just make Short-Trades, because Long-Trades would increase the Equity curve. As you can see, it works quite well (Spread: 1). If someone can test it for a longer period of time, that would be nice. If someone had an idea to minimize the drawdowns a bit, it also would be nice.

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = False // Kumulieren von Positionen deaktiviert

// Das Handelssystem wird um 0:00 Uhr alle pending Orders stornieren und alle Positionen schließen. Es werden vor der "FLATBEFORE"-Zeit keine neuen Orderaufträge zugelassen.

DEFPARAM FLATBEFORE = 100000

// Stornieren aller pending Orders und Schließen aller Positionen zur "FLATAFTER"-Zeit

DEFPARAM FLATAFTER = 140000

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen vor einer bestimmten Uhrzeit

noEntryBeforeTime = 100000

timeEnterBefore = time >= noEntryBeforeTime

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen nach einer bestimmten Uhrzeit

noEntryAfterTime = 140000

timeEnterAfter = time < noEntryAfterTime

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Bedingungen zum Einstieg in Short-Positionen

indicator1 = Average[200](close)

c1 = (close < indicator1)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

SELLSHORT 5 CONTRACT AT MARKET

ENDIF

// Stops und Targets

SET STOP %LOSS 1

Paul

PaulParticipant

Master

Hi imokdesign

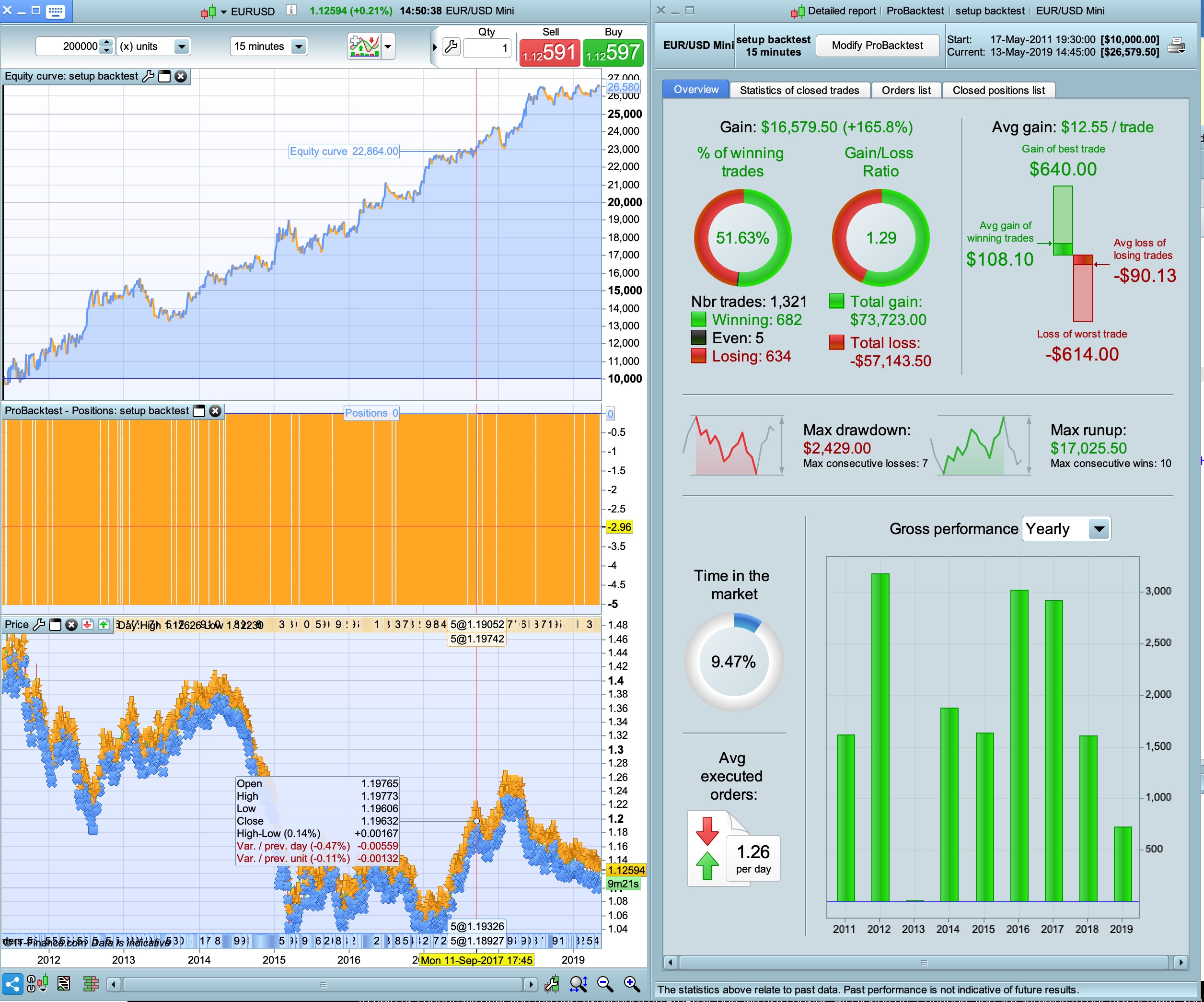

Thanks for sharing! Did give it a spin and I’am surprised about the results!

defparam cumulateorders = false

DEFPARAM FLATBEFORE = 100000

DEFPARAM FLATAFTER = 140000

noEntryBeforeTime = 100000

timeEnterBefore = time >= noEntryBeforeTime

noEntryAfterTime = 140000

timeEnterAfter = time < noEntryAfterTime

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

indicator1 = Average[200](close)

c1 = (close < indicator1)

if c1 and timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

sellshort 5 contract at market

endif

SET STOP %LOSS 1

Paul, i have good result but maybe not enough history. Could you test 200K on UT1 with

indicator1 = Average[50](close)

Maybe interesting with the frequency per day and a higher position size. What are you thinking about it ?

PaulParticipant

Master

it’s not good enough

perhaps I will work on it later

Abz

AbzParticipant

Veteran

hello

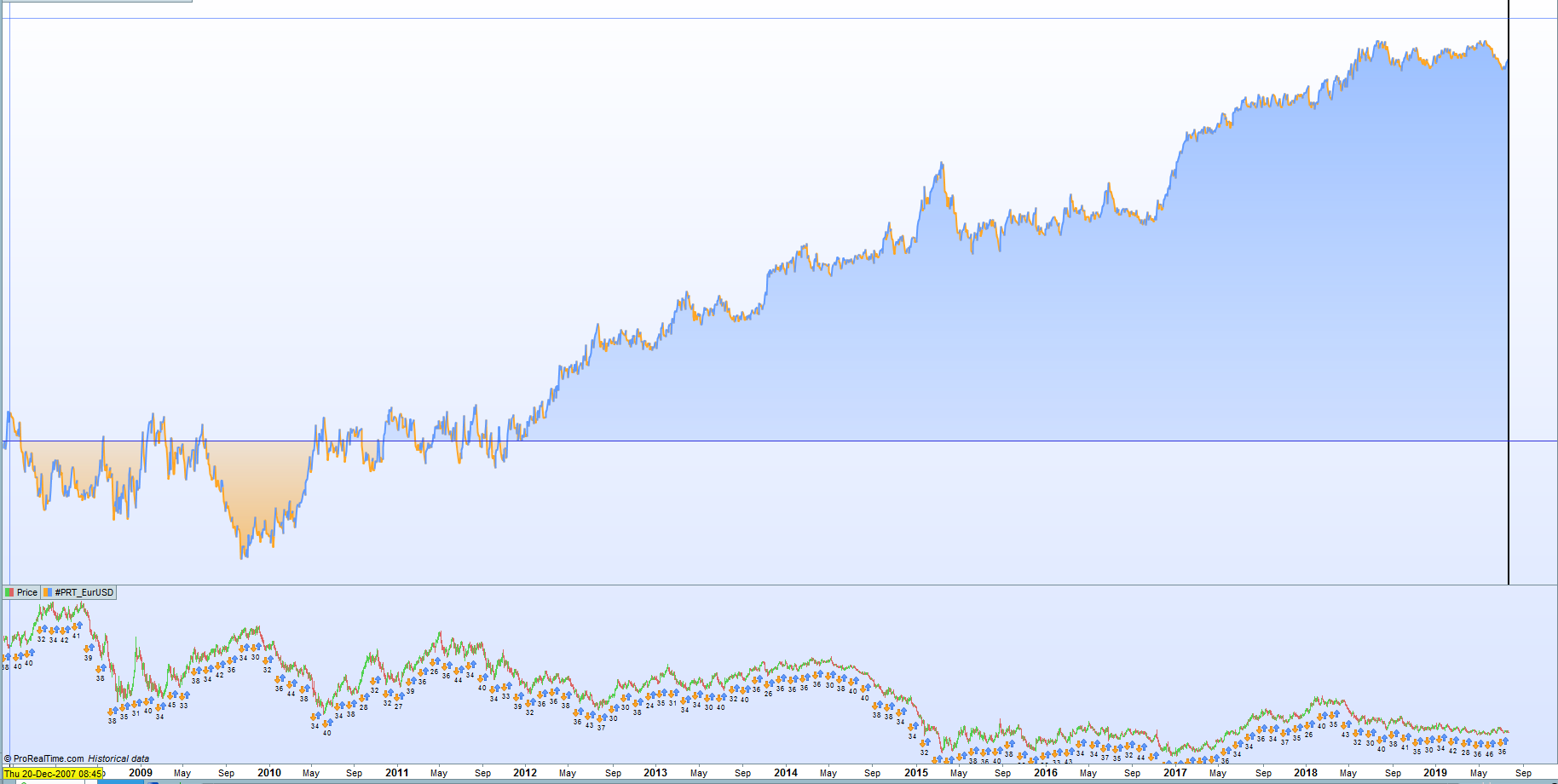

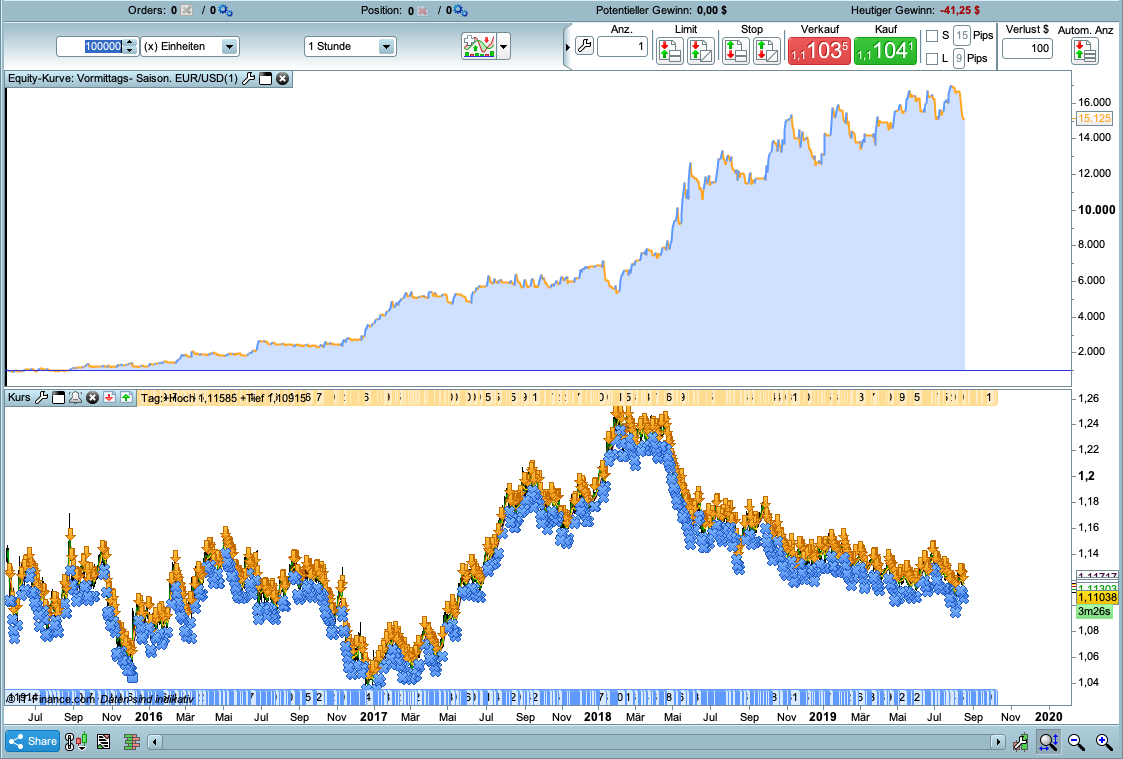

backtest from april 2006 , it performs much better with average 50 rather than 200. Attached result are for average 50

I try this system on ut1, but it’s stop by pro order. That’s often the case with ut1. Someone know why and how to avoid that?

The best results are with the average between 70 and 120

indicator1 = Average[80](close)

Tips: you can backtest this strategy with a 1hour timeframe, it give very similar results and the backtest is much longer.

Also, you can reduce the %LOSS to 0.5-0.75

It does not affect the G/L ratio, but it helps to reduce the max loose for 1 trade.

I join you the report with TF=1hour, spread=0.6, average=80, %LOSS=0.75

What if you still pay attention to the moneymanagement. I like the argument of the compound interest. I inserted it from this link:

https://www.prorealcode.com/blog/learning/money-management-prorealtime-code/

I hope I have inserted this correctly … does not look bad, but I have not tested if that works. (EUR/USD mini)

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = False // Kumulieren von Positionen deaktiviert

// Das Handelssystem wird um 0:00 Uhr alle pending Orders stornieren und alle Positionen schließen. Es werden vor der "FLATBEFORE"-Zeit keine neuen Orderaufträge zugelassen.

DEFPARAM FLATBEFORE = 100000

// Stornieren aller pending Orders und Schließen aller Positionen zur "FLATAFTER"-Zeit

DEFPARAM FLATAFTER = 140000

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen vor einer bestimmten Uhrzeit

noEntryBeforeTime = 100000

timeEnterBefore = time >= noEntryBeforeTime

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen nach einer bestimmten Uhrzeit

noEntryAfterTime = 140000

timeEnterAfter = time < noEntryAfterTime

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Bedingungen zum Einstieg in Short-Positionen

indicator1 = Average[80](close)

c1 = (close < indicator1)

REM Money Management

Capital = 1000

Risk = 10

StopLoss = 0.75 // Could be our variable X

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// SELL order example

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry then

SELLSHORT PositionSize CONTRACTS AT MARKET

ENDIF

// Stops und Targets

SET STOP %LOSS StopLoss

I noticed that the author runs the moving average on a daily basis. that would be multitime. It would also work so far, except that sometimes whole months are not traded.

i think is more or less exactly the same as the other “Short the eur/usd in this time” code which is on this forum? Cant find it right now but its not old either. I do belive the other one looks better than this one. Someone dig it up! 🙂

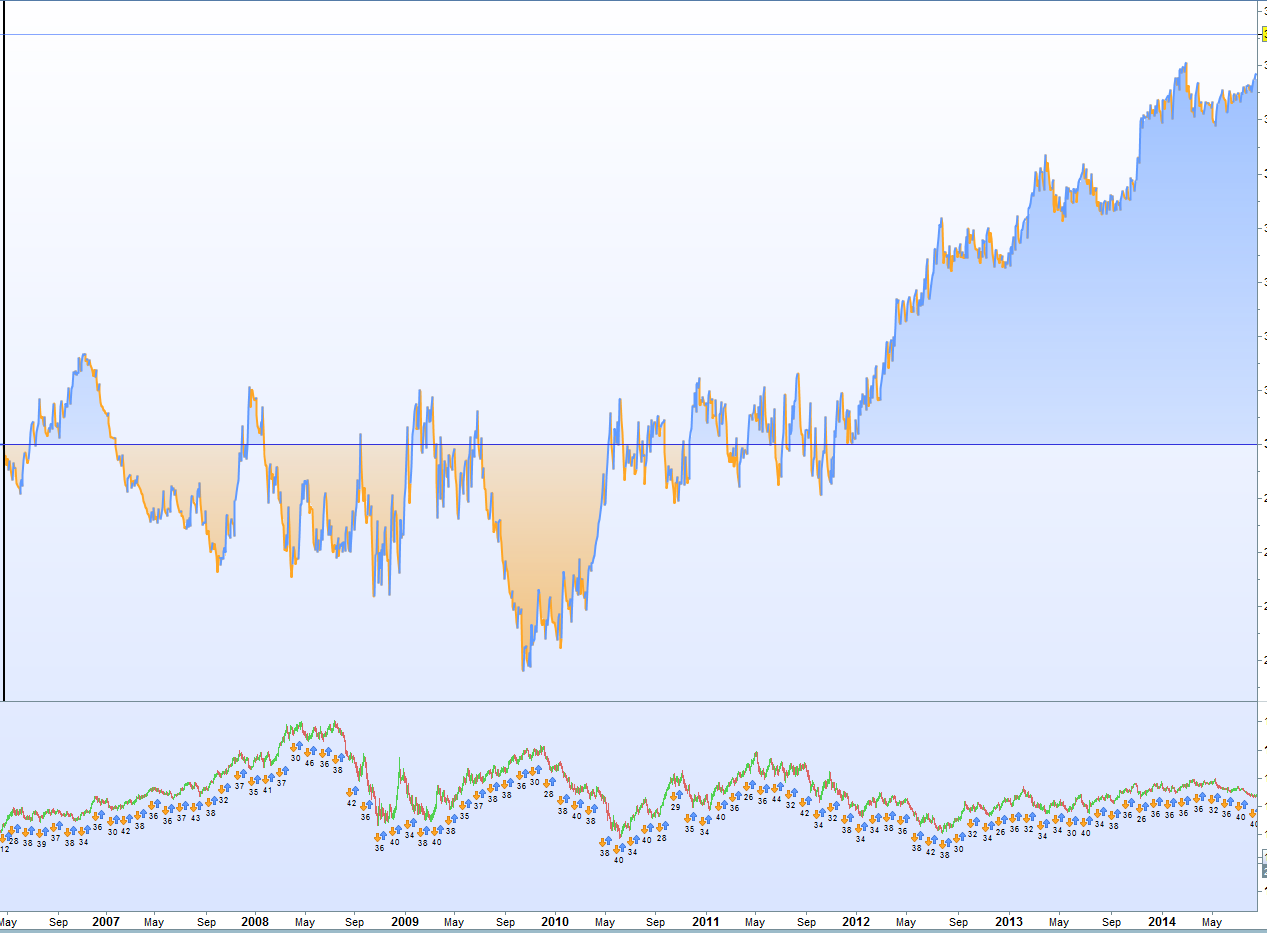

I Just want to update this thread, with very little improvement (more histroy). Its the Resault with the max Profit and not with the min Drawdown. With SMA80 there is a big Drawdown from 2012 -2016. With the SMA 14 its much better but since 2020 a little worse.

indicator1 = Average[14](close)