This code calculates both DrawDown and RunUp and their ratio, butyou have to add it to one of your strategies, not indicators:

// DrawDown & RunUp (abridged)

//

ONCE Capital = 10000

ONCE MinPoint = Capital

ONCE MaxPoint = 0

ONCE MaxRU = 0

ONCE MaxDD = 0

//------------------------------------------

// EQUITY

Equity = Capital + StrategyProfit

TempProfit = PositionPerf * PositionPrice / PipSize * PipValue // / abs(CountOfPosition)

TempEquity = Equity + TempProfit

//------------------------------------------

// DrawDown

MaxPoint = max(MaxPoint,TempEquity)

DD = MaxPoint - TempEquity

MaxDD = max(MaxDD,DD)

DDperc = MaxDD * 100 / Capital

//

//------------------------------------------

// RunUp

MinPoint = min(MinPoint,TempEquity)

RU = TempEquity - MinPoint

MaxRU = max(MaxRU,RU)

RUperc = MaxRU * 100 / Capital

//------------------------------------------

// DD/RU ratio

DDRUratio = (MaxDD / MaxRU) * 100

//------------------------------------------

You only have to set your Capital, in place of 10000.

@robertogozzi Isn’t there a mistake on line 24?

MaxRU = min(MaxRU,RU)

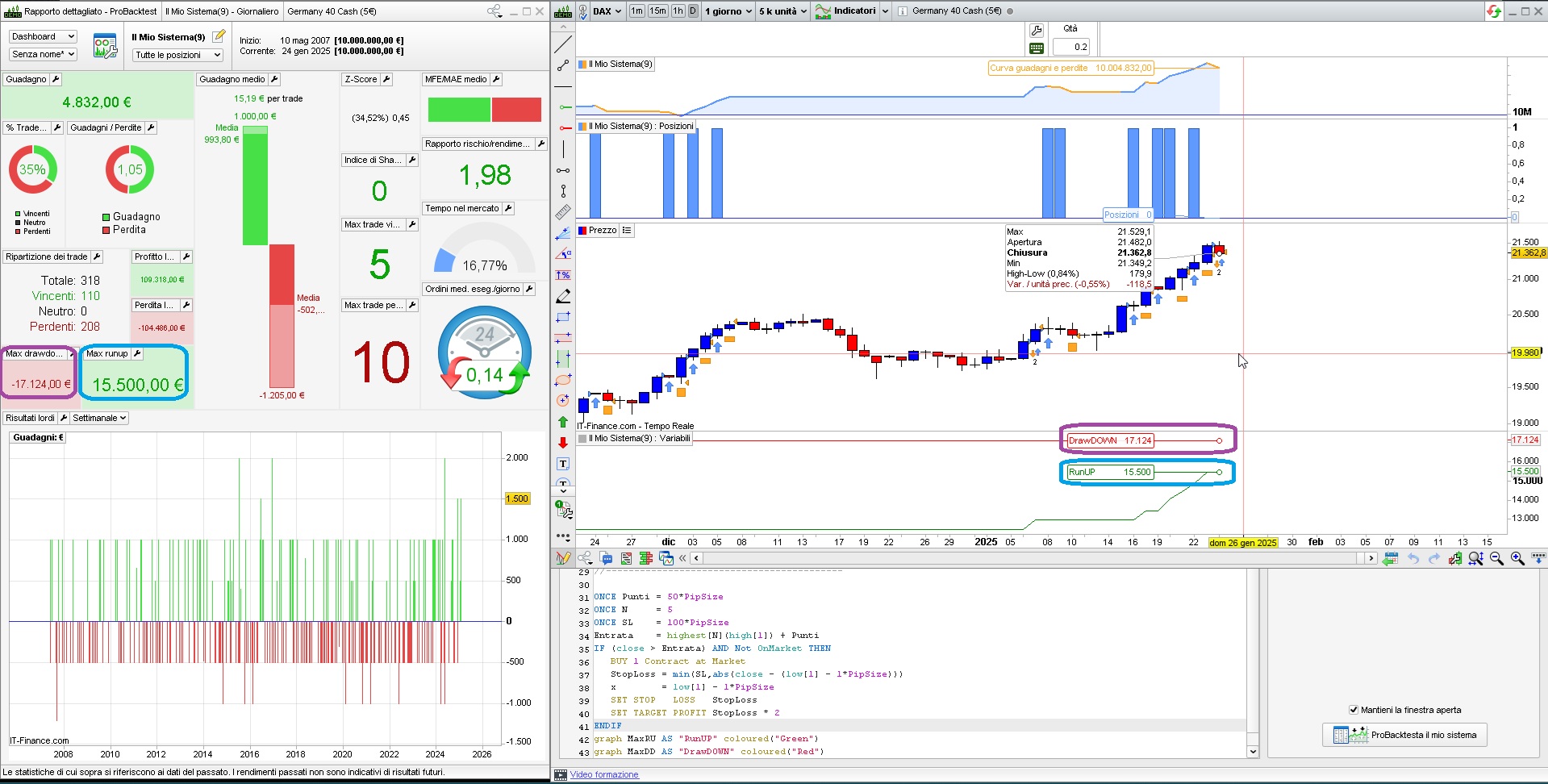

No, as we always have to store the highest value, both for RunUP and DrawDOW, this code matches ProRealTime calculations (on Dax, DailyTF) as shown in the attached pic:

// DrawDown & RunUp

//

ONCE Capital = 100000

ONCE MinPoint = Capital

ONCE MaxPoint = 0

ONCE MaxRU = 0

ONCE MaxDD = 0

//------------------------------------------

// EQUITY

Equity = Capital + StrategyProfit

TempProfit = PositionPerf * PositionPrice / PipSize * PipValue // / abs(CountOfPosition)

TempEquity = Equity + TempProfit

//------------------------------------------

// DrawDown

MaxPoint = max(MaxPoint,TempEquity)

DD = MaxPoint - TempEquity

MaxDD = max(MaxDD,DD)

DDperc = MaxDD * 100 / Capital

//

//------------------------------------------

// RunUp

MinPoint = min(MinPoint,TempEquity)

RU = TempEquity - MinPoint

MaxRU = max(MaxRU,RU)

RUperc = MaxRU * 100 / Capital

//------------------------------------------

// DD/RU ratio

DDRUratio = (MaxDD / MaxRU) * 100

//------------------------------------------

ONCE Punti = 50*PipSize

ONCE N = 5

ONCE SL = 100*PipSize

Entrata = highest[N](high[1]) + Punti

IF (close > Entrata) AND Not OnMarket THEN

BUY 1 Contract at Market

StopLoss = min(SL,abs(close - (low[1] - 1*PipSize)))

x = low[1] - 1*PipSize

SET STOP LOSS StopLoss

SET TARGET PROFIT StopLoss * 2

ENDIF

graph MaxRU AS "RunUP" coloured("Green")

graph MaxDD AS "DrawDOWN" coloured("Red")

Same ast the code above, the do match!

Same ast the code above, the do match!

How do I get time-series Drawdown into a ProRealTime CSV export?

I’ve added your code to my strategy and it displays correctly on the chart in ProRealTime—great!

But I can’t figure out how to include Drawdown in my CSV export.

What I’m doing now

What I actually need

Ideal CSV columns (any equivalent works):

-

Date/Time, Equity (or Balance/NetLiquidation), Running Peak, Drawdown (amount), Drawdown (%).

With those I can filter any interval and calculate max DD for that window.

Question

If PRT can’t export DD directly

Current path used: Detailed report → Closed positions list (CSV).

Looking for the precise click path (and settings) to get a time-series drawdown out. Thanks!

You may get some data from the backtest:

- entry price

- exit price

- outcome

- type of trade (long or short)

then you have to get the OHLC data from the chart (you can find posts on how to get it, which is not as straightforward, though, at

https://www.prorealcode.com/topic/exporter-les-donnees-historiques-ohlc/#post-250046).

Once you have that data I think a spreadsheet app, such as eXcel, might be able to recalculate the drawdown, maybe with the help of Visual Basic for Applications (VBA).