Paul

PaulParticipant

Master

Fantasio2020 whatever number of variables you prefer and works for you.

PaulParticipant

Master

looks like I got the difference between 200k & 50k fixed on the same strategy. If reset is used, the cycle should restart again too.

One part will always be a bit doubtful, if reps 1 (ore more) is used, and in a backtest results is +0.01 and live -0.01 it can have on the impact on the rest of the strategy for value x & y.

That’s why it’s important I guess to have a reset, daily, weekly etc. depending on timeframe.

PaulParticipant

Master

this is the code as I’ve it now.

Also interesting is to optimise the direction 1 to 6. The reset is set to daily here.

once value1a=6 // 6

once value2a=8 // 8

once heuristicsengine=1

// heuristics engine

if heuristicsengine then

StartingValue = 4

increment = 1 //5, 20, 10

maxincrement = 2 //5, 10 limit of no of increments either up or

reps = 1 //1 number of trades to use for analysis //2

minvalue = 1 //5, minimum allowed value

maxvalue = 10 //20, 300, 150 //maximum allowed 12

StartingValue2 = 10

increment2 = 1 //5, 10

maxincrement2 = 2 //1, 30 limit of no of increments either up/down //4

reps2 = 1 //1, 2 nos of trades to use for analysis //3

minvalue2 = 1 //5, minimum allowed value

maxvalue2 = 10 //20, 300, 200 maximum allowed value

reset = 1

weighting = 1

direction=1

if direction=1 then

a1=0

a2=0

a3=0

a4=0

elsif direction=2 then

a1=1

a2=0

a3=1

a4=0

elsif direction=3 then

a1=0

a2=1

a3=0

a4=1

elsif direction=4 then

a1=1

a2=0

a3=0

a4=1

elsif direction=5 then

a1=0

a2=1

a3=1

a4=0

elsif direction=6 then

a1=1

a2=1

a3=1

a4=1

endif

if reset=1 then

if intradaybarindex=0 then

ValueX = StartingValue

Valuey = StartingValue2

WinCountB = 0

WinCountB2 = 0

StratAvgB = 0

StratAvgB2 = 0

BestA = 0

BestA2 = 0

BestB = 0

BestB2 = 0

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

wincounta2 = 0 //initialize current win count

stratavga2 = 0 //initialize current avg strategy profit

endif

else

once ValueX = StartingValue

once Valuey = StartingValue2

once WinCountB = 0

once WinCountB2 = 0

once StratAvgB = 0

once StratAvgB2 = 0

once BestA = 0

once BestA2 = 0

once BestB = 0

once BestB2 = 0

endif

heuristicscyclelimit = 2

if reset=1 then

if intradaybarindex=0 then

heuristicscycle = 0

endif

else

once heuristicscycle = 0

endif

once heuristicsalgo1 = 1

once heuristicsalgo2 = 0

if heuristicscycle >= heuristicscyclelimit then

if heuristicsalgo1 = 1 then

heuristicsalgo2 = 1

heuristicsalgo1 = 0

elsif heuristicsalgo2 = 1 then

heuristicsalgo1 = 1

heuristicsalgo2 = 0

endif

heuristicscycle = 0

else

once valuex = startingvalue

once valuey = startingvalue2

endif

if heuristicsalgo1 = 1 then

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

once valuex = startingvalue

once pincpos = a1 //positive increment position

once nincpos = a2 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 0 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as "wincountb"

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as "stratavgb"

if optimise = reps then

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*-1)*-1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2"

//graph stratavga*-1 as "stratavga"

//once besta = 300

//graph besta coloured (0,0,0) as "besta"

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as "bestb"

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = min((valuex + (increment*pincpos)),maxvalue)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = min((valuex + (increment*pincpos)),maxvalue)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

Else

if weighting=1 then

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX1 = min(round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20),maxvalue) //Lower Reps = Less weight assigned to Win%

valuex=max(minvalue,valuex1)

EndIf

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

elsif heuristicsalgo2 = 1 then

// heuristics algorithm 2 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise2 = optimise2 + 1

endif

once valuey = startingvalue2

once pincpos2 = a3 //positive increment position

once nincpos2 = a4 //negative increment position

once optimise2 = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode2 = 0 //switches between negative and positive increments

//once wincountb2 = 3 //initialize best win count

//graph wincountb2 coloured (0,0,0) as "wincountb2"

//once stratavgb2 = 4353 //initialize best avg strategy profit

//graph stratavgb2 coloured (0,0,0) as "stratavgb2"

if optimise2 = reps2 then

heuristicscycle = heuristicscycle + 1

for i2 = 1 to reps2 do

if positionperf(i2) > 0 then

wincounta2 = wincounta2 + 1 //increment current wincount

endif

stratavga2 = stratavga2 + (((positionperf(i2)*countofposition[i2]*close)*-1)*-1)

next

stratavga2 = stratavga2/reps2 //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1-2"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2-2"

//graph stratavga2*-1 as "stratavga2"

//once besta2 = 300

//graph besta2 coloured (0,0,0) as "besta2"

if stratavga2 >= stratavgb2 then

stratavgb2 = stratavga2 //update best strategy profit

besta2 = valuey

endif

//once bestb2 = 300

//graph bestb2 coloured (0,0,0) as "bestb2"

if wincounta2 >= wincountb2 then

wincountb2 = wincounta2 //update best win count

bestb2 = valuey

endif

if wincounta2 > wincountb2 and stratavga2 > stratavgb2 then

mode2 = 0

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 1 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 1 then

valuey = min((valuey + (increment2*pincpos2)),maxvalue2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 2 then

valuey = min((valuey + (increment2*pincpos2)),maxvalue2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 2 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

endif

if nincpos2 > maxincrement2 or pincpos2 > maxincrement2 then

if besta2 = bestb2 then

valuey = besta2

Else

if weighting=1 then

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY1 = min(round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20),maxvalue2)

valuey=max(minvalue2,valuey1)

//Lower Reps = Less weight assigned to Win%

EndIf

endif

nincpos2 = 1

pincpos2 = 1

elsif valuey > maxvalue2 then

valuey = maxvalue2

elsif valuey < minvalue2 then

valuey = minvalue2

endif

optimise2 = 0

endif

endif

// heuristics algorithm 2 end

value1=valuex

value2=valuey

else

value1=value1a

value2=value2a

endif

get error when using your last code paul

ullle73 what errors?

Paul’s code above is not a complete Algo with Buy and Sell etc.

Hi Juan, Hi All, I’m following your posts and grateful that you share a lot of fancy stuff here. Thanks. I’d like to better understand the operating mode of the so called ML and have a few questions:

1/ where does the programme store the various results learned from the past?

2/ what happen if the Algo is stopped for some reason? Are we starting again from scratch the “learning from the past” process? I noticed that even the Algo performance (calculated by PRT) are reset to zero when the same Algo is stopped and restarted, so I guess there is now way to capitalize on previous learning if the Algo is stopped, is that right? if so, is there a way to overcome this?

3/ have you been running “live” the same programme with and without ML module? Backtest seems to give better results? are you really getting better results in rel trading?

Facinating ML!!!

Thanks

Hi Khaled, I am unfortunately not very active on the forum lately as I am kept just way too busy between PRT development and my other work. But to briefly answer your questions:

1. It is stored locally in the respective variables defined in the code (WinCount, StratAvg, Best, etc.)

2. Yes unfortunately the variables are reset. Although they can be initialized using the commented out once code and using the graph command in backtest to find the latest values.

3. I use this successfully in most of my live strategies but only using a single heuristics set applied to a single variable not multiple ones as in the code above

Hope this helps

Hi Juan, Thank you for taking the time to answer my questions. I see in your ML Code that you don’t have CONDITIONS (IF C1 THEN..) before BUY and SHORTSELL instructions, which is not a problem in itself. However, in my case, the pending orders arenot cancelled automatically at the end of the candle, so I’m carying orders with irrelevant market conditions, which not only prevent other Orders with more “recent” conditions to come in but also sometimes stop the Algo…

Do you have a trick to make the pending orders cancel at the end of each candle?

Thanks

Khaled

defparam cumulateorders = false

defparam preloadbars = 2000

TIMEFRAME (15 minutes)

N = 1 //Number of Contracts

Condition = 1

/////////////////////////////////////////

// CALCULATION OF VALUE X AND VALUE Y //

////////////////////////////////////////

boxsizeL = max ( ValueX , 20)

boxsizeS = max ( ValueY , 10)

renkomaxL = round(close / boxsizeL) * boxsizeL

renkominL = renkomaxL - boxsizeL

renkomaxS = round(close / boxsizeS) * boxsizeS

renkominS = renkomaxS - boxsizeS

if high > renkomaxl + boxsizel then

renkomaxl = renkomaxl + boxsizel

renkominl = renkominl + boxsizel

endif

if low < renkomins - boxsizes then

renkomaxs = renkomaxs - boxsizes

renkomins = renkomins - boxsizes

endif

IF time>=133000 AND time>200000 then

spread = 0.5

ELSIF time>=200000 AND time>220000 then

spread = 2.5

ELSIF time>=220000 AND time>133000 then

spread = 1

ENDIF

IF CONDITION=1 THEN

BUY N CONTRACT at (renkoMaxL + boxSizeL + spread) STOP

SELLSHORT N CONTRACT at (renkoMinS - boxSizeS - spread) STOP

ENDIF

SET STOP pTRAILING 5

SET TARGET pPROFIT 1000

I have a doubt, and I am not joking, nor hesitating.

You are dealing with a very interesting topic, but with so many explanations, so many codes, and so many posts it is impossible for me to know if there is something useful.

I don’t know, it would be interesting for someone to explain in a single post what the code is for and if there is any specific code that is really useful.

I have lost myself.

You should be thankful to those many explanations, codes and posts 🙂

If it’s useful you can only understand by yourself with your own tests on your own strategies.

Fran55

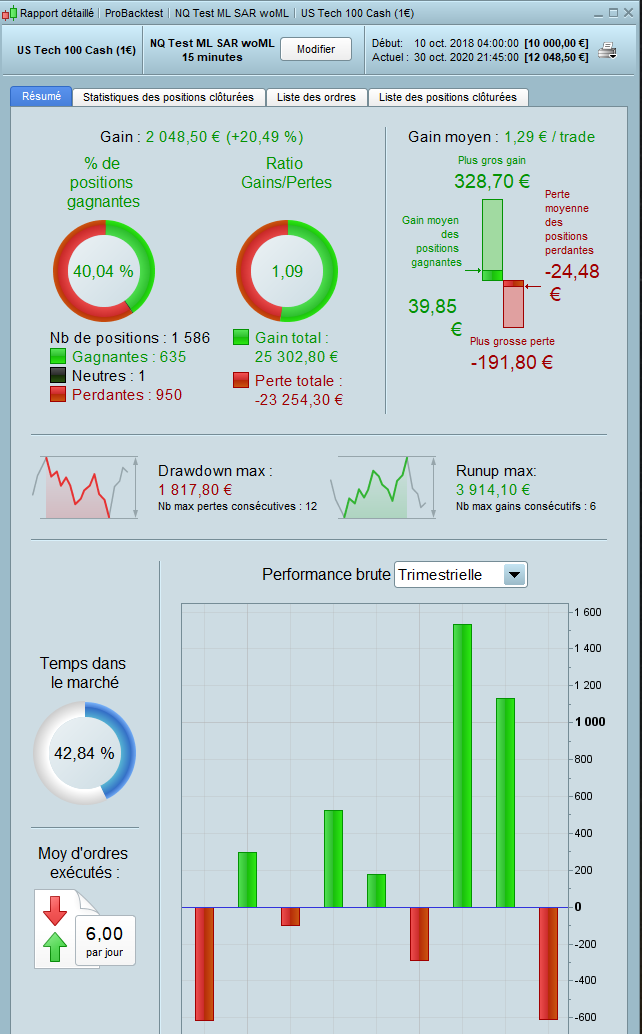

I was skeptical too and I’ve made a quick and dirty test. I’ve put together a simple LONG only code if SAR>Close and EMA21>EMA8 then buy 1 contract (Nasdaq cash 1€, 15 min TF) and exit if SAR<Close and Close<EMA8. This strategy run on a Tick by Tick mode over the period 10 Oct. 2018 to 30 Oct. 2020 (2 years) did generate a Win Rate 40.04%, Profit Ratio 1.09x and Capital gain 2048€ (attached results and ITF file).

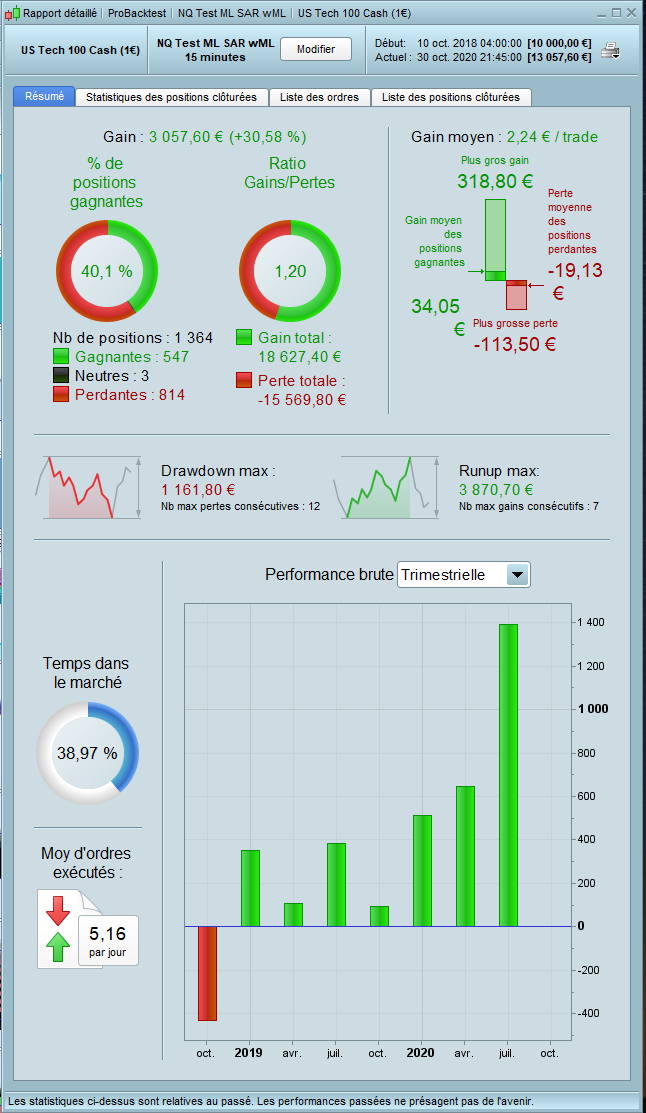

I’ve added a simple ML code on 1 variable (courtesy of juanj) that you can find at (https://www.prorealcode.com/topic/machine-learning-in-proorder/), and the results are better: Win Rate 40.1%, Profit Ratio 1.2x and Capital gain 3057€ (attached results and ITF file). The increment in € absolute gain is +50%!

You can also note that the number of losing positions have been reduced from 950 to 814 and the Drawdown has been reduced from 1817€ to 1161€. The biggest loss went from -191€ to -113€.

So, even though I didn’t write the ML code and have nothing to sell 🙂 it seems like it’s working !

Others have had different experience?

Está bien Khaled, he introducido ese código.

Problems!

Okay Khaled, I entered that code. Problems!

@Fran55

Only post in the language of the forum that you are posting in. For example English only in the English speaking forums and French only in the French speaking forums.

Thank you 🙂