Here is a strategy on the SP500, which in its raw version is already effective long and short. With similar settings the code is also effective on other indexes.

It is a mixture of gap close and mean reversion. We buy intraday below a low from the daily chart. We are selling above a high from the daily chart. The exit is the close of the previous day. So theoretically a gap closure. We exit open positions every evening and are flat overnight. A simple stoploss based on the daily range is also included in the algo. That’s all. Improvements and/or thoughts on this algo are always welcome.

//================================================

//SP500

//Spread 0.5

DEFPARAM CUMULATEORDERS = false

defparam preloadbars = 10000

//Risk Management

PositionSize = 5

//Max-Orders per Day///////////////////////////////////////

once maxOrdersL = 1

once maxOrdersS = 1

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

///////////////////////////////////////

once TimeEx = 1

once TimeEx2 = 1

once Exit = 1

timeframe(1day,updateonclose)

myhigh = high

myclose= close

mylow = low

myopen = open

mylowX = lowest[3](low) //1-20

myhighX = highest[13](high)//1-20

timeframe(default)

area = myhigh-mylow

long = close < mylowX and ordersCountL < maxOrdersL //crosses over

short= close crosses under myhighX and ordersCountS < maxOrdersS

// trading window

ONCE BuyTime = 080000

ONCE SellTime = 210000

// position management

IF Time >= BuyTime AND Time <= SellTime THEN

If long Then

Buy PositionSize CONTRACTS AT market

SET STOP LOSS area*0.4

ENDIF

If short Then

sellshort PositionSize CONTRACTS AT market

SET STOP LOSS area*1

ENDIF

endif

graphOnPrice mylowX coloured("Red")

graphonprice myclose coloured("Black")

graphOnPrice myhighX coloured("green")

if longonmarket and close > myclose and Exit=1 then

sell at market

endif

if shortonmarket and close < myclose and Exit=1 then

exitshort at market

endif

//TimeEx

if (time >= 220000 and TimeEx=1)then

sell at market

exitshort at market

endif

if time >= 220000 and dayofweek=5 and TimeEx2=1 then

sell at market

exitshort at market

endif

Thank you for sharing your code.

What time are overnight fees triggered in Germany? In UK it is for trades open at 22:00.

Your exit times of if time >= 220000 would allow overnight fees to be triggered in UK.

Feel free to make improvements to the code and adjust the time. If you set TimeEx to 0 in line 29, the result changes only minimally. In theory, you even get money if you hold the SP500 overnight. It is a short-term strategy. Little time on market. There are not many positions that are held overnight. I also tried to add another exit with a bigger profit. But this variant works very reliably. And that’s what I wanted. Short time on the market and “reliability”.

Also works great on NASDAQ. I haven’t tried Dow Jones yet.

As a matter of interest then … what time are overnight fees triggered in Germany?

I’m just interrested if it is 22:00 same as UK even though Germany is currently UTC+1 and UK is currently UTC?

I can’t see German IG website to find out, maybe you can?

Whenever I have checked on UK IG re overnight fees it awlays says 22:00 so I guess it is 22:00 all year round regardless of the hour going forward or back (as now).

Maybe UTC+1 countries are the same at 22:00 all year round … anybody can answer?

End of hijacking your thread 🙂

Your strategy shows a good equity curve on DJI 1 Hour timeframe (no changes except minus 1 hour for UK on the UTC +1 times and I use spread = 5 for DJI when backtesting).

As far as I know, overnight fees always apply from 10 p.m. Here in Germany. Can you post a picture of Dow Jones? How big is the drawdown?

good equity curve on DJI 1 Hour timeframe

I forget how I work is not same as most … above is only over 10k bars.

Nearly blows the Account (£100k) at pos size = 1 over 100k bars so no point me posting an equity curve for 10K bars?

Optimize lines 39 and 57 together and lines 40 and 62.

@Admin

@Roberto

Can you test and approve my contribution to the library?

When backtesting u need to allow for varying spreads throughout the day, testing on 0.5 spread when spread can be 2 until US open wont give accurate results.

Can have some drawdown… would need some time to look more closely, but spreads can make a significant difference in strategy success when testing….

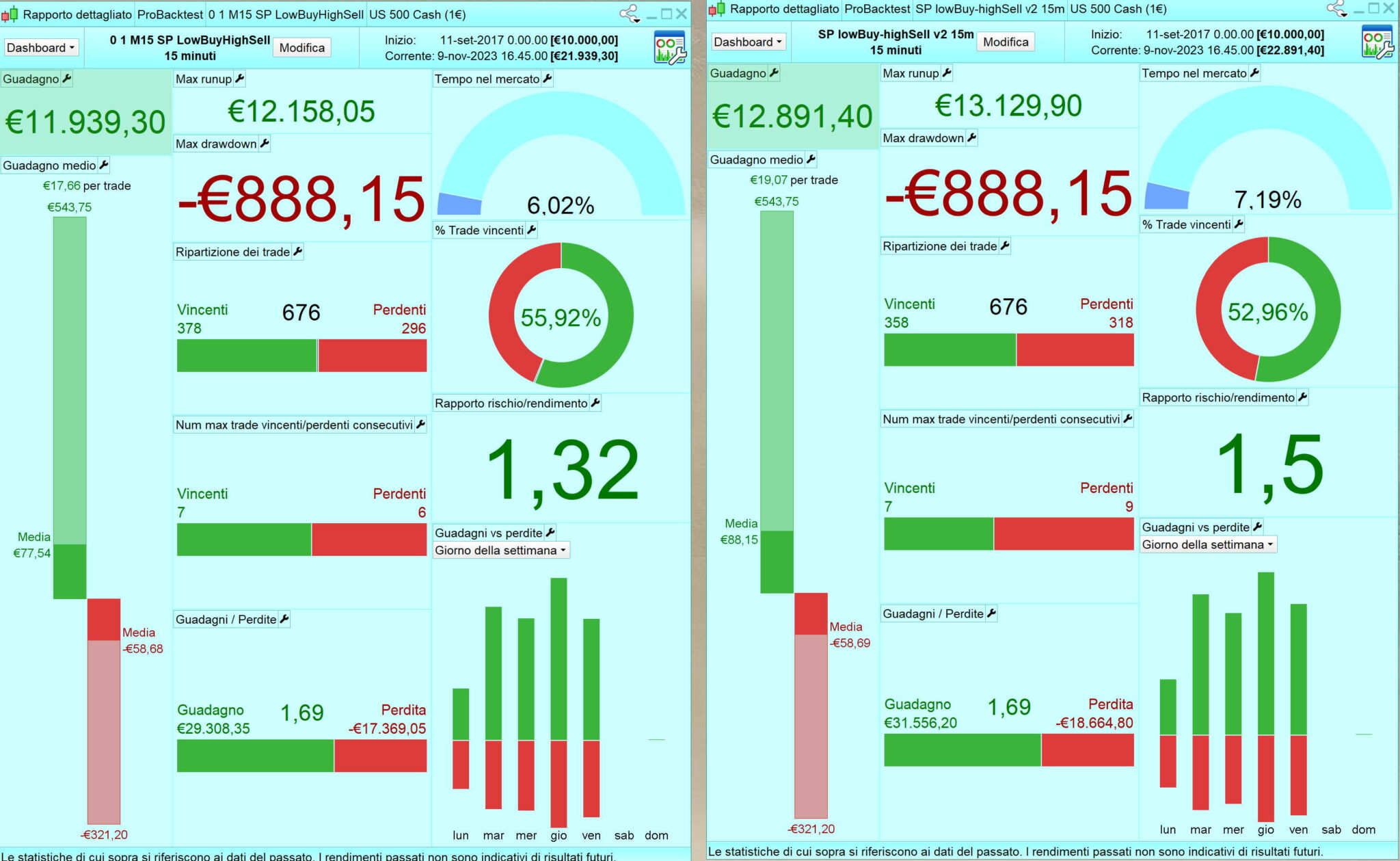

Hi Phoentzs, interesting code. I rewrote the code in the simplest form and added only a certain percentage to the exit. Up to 50k the results are similar, then are better.

//SP "lowBuy-highSell" v2 15m [spread 0.5] //TS by Phoentzs

//https://www.prorealcode.com/topic/m15-sp500-lowbuyhighsell-strategy/

//*********************************************************************************

defParam cumulateOrders = false

defParam preLoadBars = 10000

defParam flatAfter = 220000

cTime = time >= 080000 and time <= 210000

positionSize = 5

//-----------------------------------------------------------------------

once maxOrdersL = 1 //max-Orders per Day

once maxOrdersS = 1

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------

timeframe(1 day, updateOnClose)

//*********************************

periodL = 3

periodS = 13

multiplierL = 0.4

multiplierS = 1

//*********************************

dailyHigh = high

dailyClose = close

dailyLow = low

dailyOpen = open

dailyLowX = lowest[periodL](low)

dailyHighX = highest[periodS](high)

areaDaily = dailyHigh - dailyLow

//--------------------------------------------------------------

timeframe(15 minutes)

cLong = close < dailylowX

cShort = close crosses under dailyHighX

if cTime and cLong and ordersCountL < maxOrdersL then

buy positionSize contracts at market

set stop loss areaDaily * multiplierL

endif

if longOnMarket and close > dailyClose and positionPerf*100 > 0.1 then // exit: gain > 0.1%

sell at market

endif

//----------------------

if cTime and cShort and ordersCountS < maxOrdersS then

sellshort positionSize contracts at market

set stop loss areaDaily * multiplierS

endif

if shortOnMarket and close < dailyClose and positionPerf*100 > 0.3 then // exit: gain > 0.3%

exitShort at market

endif

//---------------------------------------------------------------------------------------

graphOnPrice dailyLowX coloured("red")

graphonprice dailyClose coloured("black")

graphOnPrice dailyHighX coloured("green")

//---------------

once equity = 0

once performanceLastMonth = 0

if month <> month[1] then

performanceLastMonth = strategyProfit - equity

equity = strategyProfit

endif

graph performanceLastMonth

Thanks @Mauropro, great work with you as always.

I initially used “set target Price myclose”. But the exit brings a little more power. This system in combination with a breakout system should be enough for a portfolio.

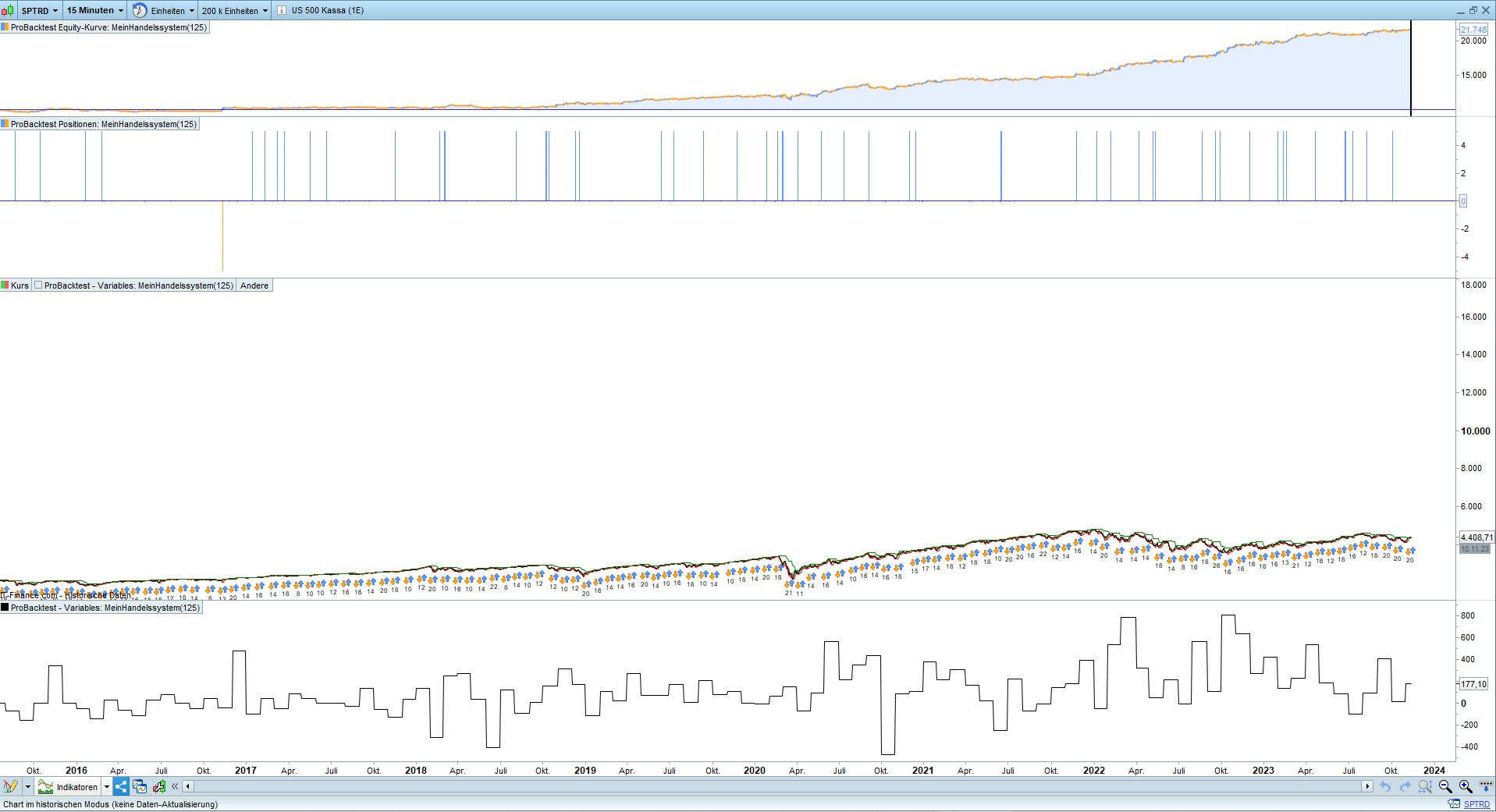

Here is the 200k backtest. The post-corona-volatility seems to be doing the system a lot of good.

Thanks for sharing.

Es ist wichtig, sich daran zu erinnern, dass wir hier über das SP500 sprechen. Vor fünf Jahren lag diese noch bei rund 2000 Punkten, die Volatilität war also sicherlich deutlich geringer. Wir arbeiten auf einen Lückenschluss hin, der auch heute noch manchmal nur wenige Punkte umfasst. Aber es scheint sicher, dass die Bewegung sehr oft auftreten wird, und wir können uns dieses Prinzip zunutze machen. Selbst wenn wir “highest and lowest” im Code auf “1” setzen, funktioniert das System trotzdem. Lediglich der Drawdown nimmt leicht zu und die Kurve ist etwas zackig. Probieren Sie das System an der Nasdaq aus… 😉

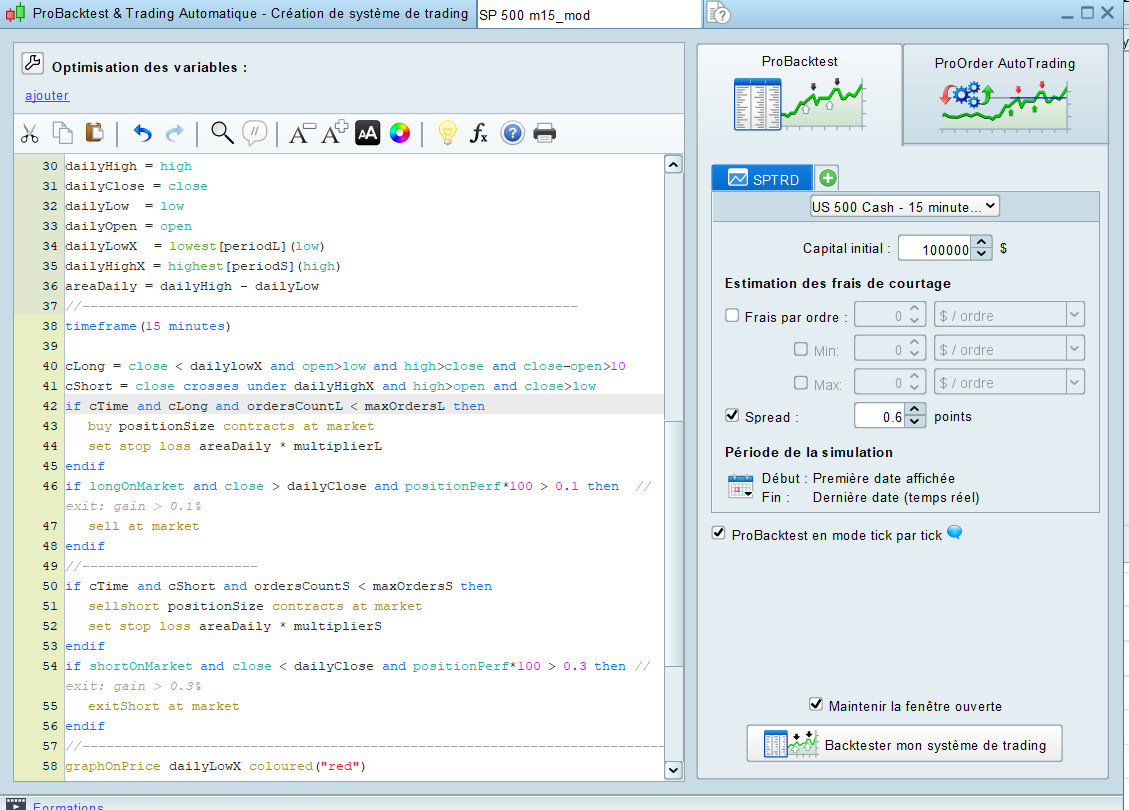

Test with a spread of 0.6 as this is the minimum at IG and the maximum is 1.4

Added buy and sell conditions

//SP "lowBuy-highSell" v2 15m [spread 0.5] //TS by Phoentzs

//https://www.prorealcode.com/topic/m15-sp500-lowbuyhighsell-strategy/

//*********************************************************************************

defParam cumulateOrders = false

defParam preLoadBars = 10000

defParam flatAfter = 220000

cTime = time >= 080000 and time <= 210000

positionSize = 1

//-----------------------------------------------------------------------

once maxOrdersL = 1 //max-Orders per Day

once maxOrdersS = 1

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------

timeframe(1 day, updateOnClose)

//*********************************

periodL = 3

periodS = 13

multiplierL = 0.4

multiplierS = 1

//*********************************

dailyHigh = high

dailyClose = close

dailyLow = low

dailyOpen = open

dailyLowX = lowest[periodL](low)

dailyHighX = highest[periodS](high)

areaDaily = dailyHigh - dailyLow

//--------------------------------------------------------------

timeframe(15 minutes)

cLong = close < dailylowX and open>low and high>close and close-open>10

cShort = close crosses under dailyHighX and high>open and close>low

if cTime and cLong and ordersCountL < maxOrdersL then

buy positionSize contracts at market

set stop loss areaDaily * multiplierL

endif

if longOnMarket and close > dailyClose and positionPerf*100 > 0.1 then // exit: gain > 0.1%

sell at market

endif

//----------------------

if cTime and cShort and ordersCountS < maxOrdersS then

sellshort positionSize contracts at market

set stop loss areaDaily * multiplierS

endif

if shortOnMarket and close < dailyClose and positionPerf*100 > 0.3 then // exit: gain > 0.3%

exitShort at market

endif

//---------------------------------------------------------------------------------------

graphOnPrice dailyLowX coloured("red")

graphonprice dailyClose coloured("black")

graphOnPrice dailyHighX coloured("green")

//---------------

once equity = 0

once performanceLastMonth = 0

if month <> month[1] then

performanceLastMonth = strategyProfit - equity

equity = strategyProfit

endif

graph performanceLastMonth