Hello,

This strategy will look for a new highs (or lows for shorts) over the last N candles and, in conjunction with 2 x entry filters will take a position. I also added the volatility filter provided by JS in a recent post – thank you, this helped improve overall performance.

Filter for too high volatility

I had originally developed this strategy to run on a daily time frame, but have found that it runs just as well on lower time frames. 5 minutes is the lowest setting I would consider.

Risk Mgt – For initial Profit Target and Stop Loss it uses a simple ATR methodology, with a hard $ value as a backstop to the downside. The trailing stop is taken from another great strategy posted on this great site.

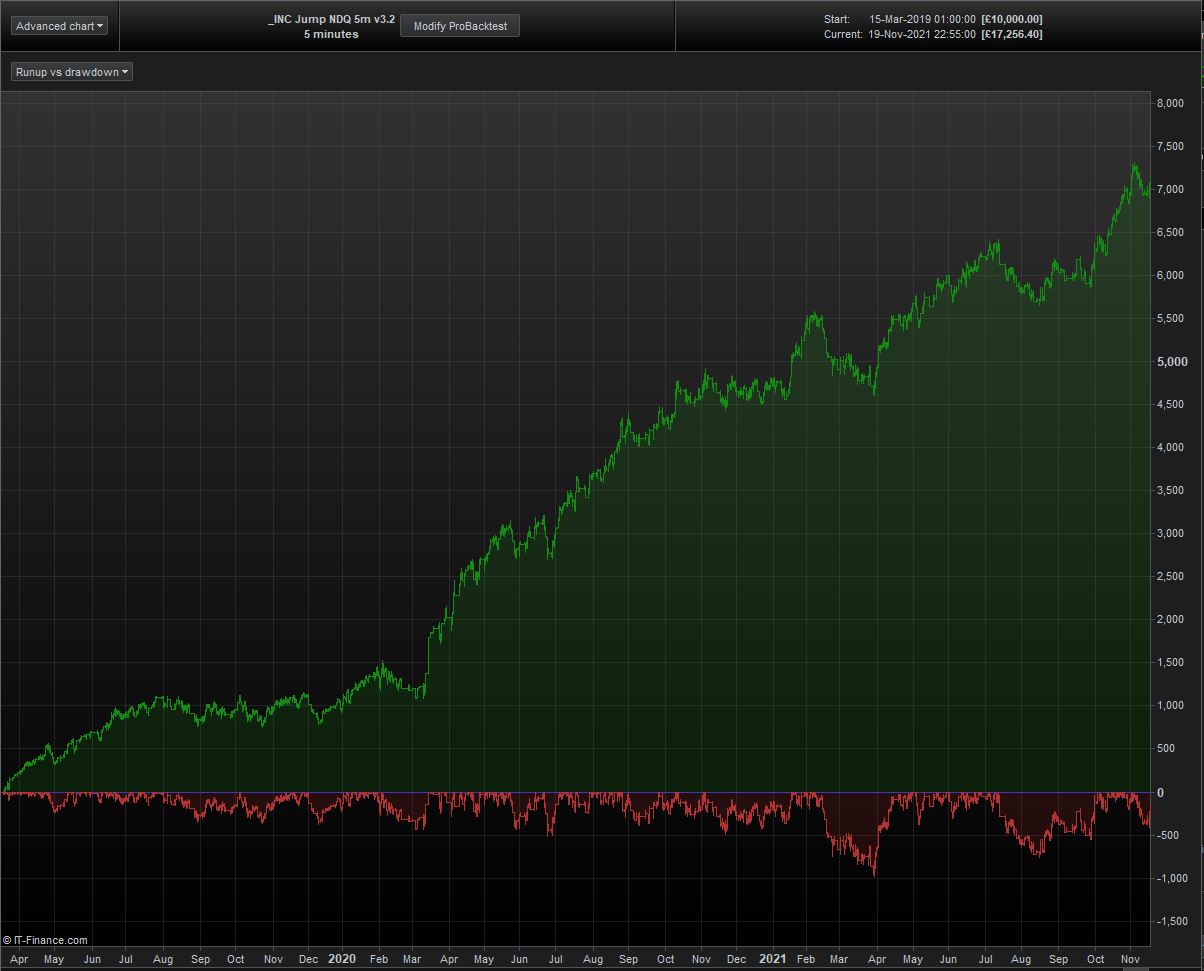

For the walk forward results in the screenshots provided the settings were as follows, running on an EU timezone;

Capital 10k

Position size 1

Spread 2.6

NASDAQ

5 min

Further testing:

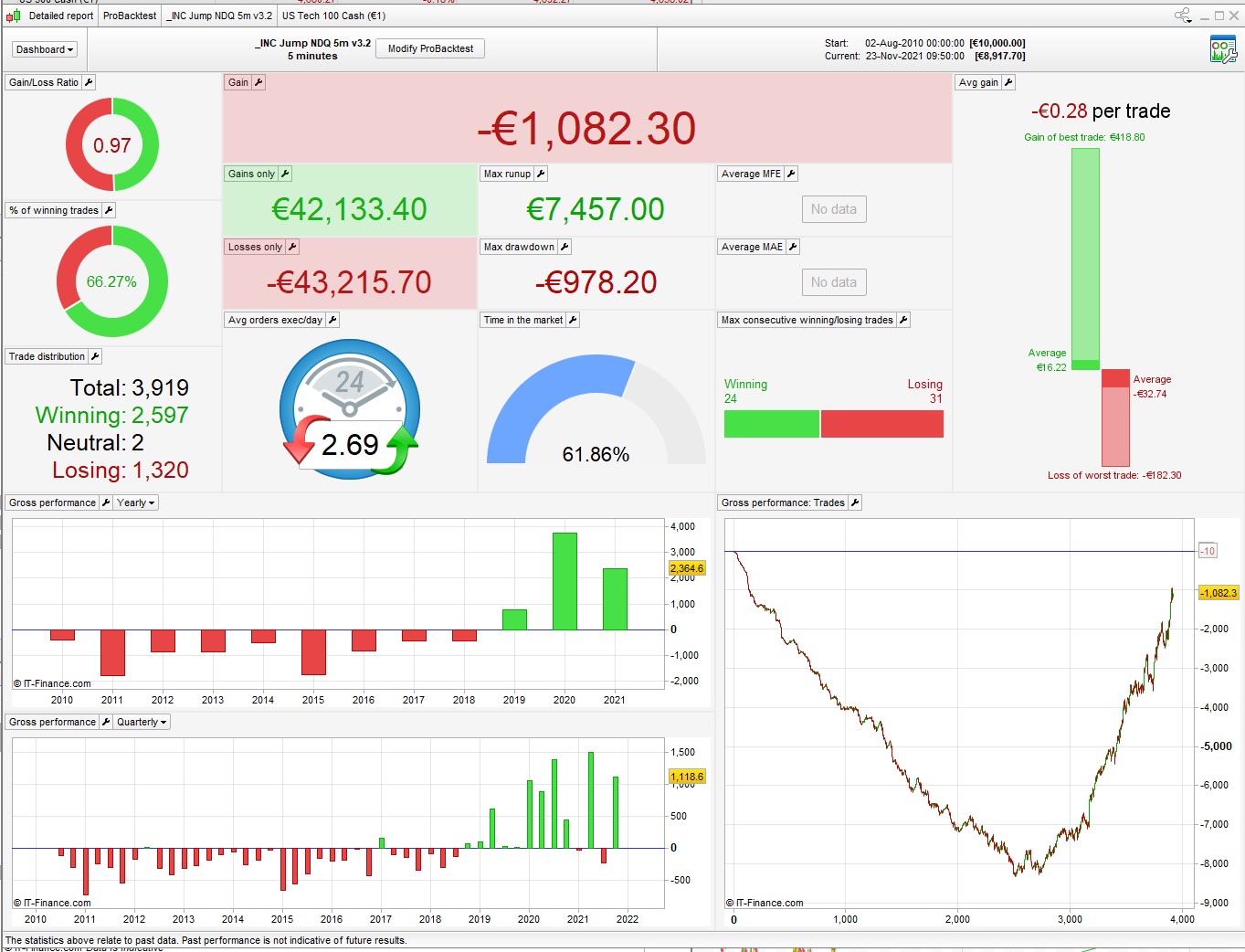

1 – Need to optimise the short side as it doesn’t perform as well as the longs do. Will test different look back periods to try and improve this.

2 – Try to reduce how much the strategy gives back overall looking at the Losses Only metric and reflected in the Gain/Loss Ratio, without curve fitting.

All observations, feedback and questions are always welcome.

Thank you

//==========================================================================================================

// Code: INCUBATOR Jump

// Source: General research

// Version 3

// Index: NASDAQ

// TF: 5 min (adapted from Daily)

// TZ: EU

// Spread: 2.6

// Notes: v1.1 Core strategy, Long only

// v2.1 Added Short entry

// v3.1 Applied Entry Filter on 60 and 30 minute timeframe

// v3.2 19/11/21 Optimised Trailing Stop for 5 minute timeframe (Entry Filter and Criteria remain the same)

// Added Volatility filter to avoid enter trades during choppy marekt conditions

// Author: JS

// https://www.prorealcode.com/topic/filter-for-too-high-volatility/#post-180817

//==========================================================================================================

DEFPARAM CUMULATEORDERS = false

//Risk Management

PositionSize=1

sl = PositionSize *110 //1100

entry3pbase = (HIGHEST[16](High)+LOWEST[16](Low)) / 2

off = 2 * AverageTrueRange[15](Close)

//Filter Filter

Timeframe(60 MINUTES)

indicator1 = average[300] //175

CB1 = close > indicator1

CS1 = close < indicator1

Timeframe(30 MINUTES)

indicator2 = ADX[14] //14

CB2 = (indicator2 >= 20)

CS2 = (indicator2 <= 20)

//Volatility Filter: Avoid entry during choppy markets

xPVolatility = (Std[3](Close) / Close) * 100

F1 = xPVolatility < 0.29

//GRAPH xPVolatility

//Entry Criteria

IF NOT LongOnMarket AND Close>Close[24] AND CB1 AND CB2 and opendayofweek <>5 THEN

BUY PositionSize CONTRACTS AT entry3pbase + off STOP

ENDIF

IF NOT ShortOnMarket AND Close<Close[24] AND CS1 AND CS2 and opendayofweek <>2 AND F1 THEN

SELLSHORT PositionSize CONTRACTS AT entry3pbase - off STOP

ENDIF

//Break even

breakevenPercent = 0.2

PointsToKeep = 15

startBreakeven = tradeprice(1)*(breakevenpercent/100)

once breakeven = 1//1 on - 0 off

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

//--------------------------------------------------------------------------------------------------------------------------------------------------

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = .1 //05 // set to 0 to ignore tsincrements

once tsminatrdist = 5

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 3 // ts atr distance

trailingstopshort = 3 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10))/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

if onmarket then

if dayofweek=0 and (hour=0 and minute>=57) and abs(dopen(0)-dclose(1))>50 and positionperf(0)>0 then

if shortonmarket and close>dopen(0) then

exitshort at market

endif

if longonmarket and close<dopen(0) then

sell at market

endif

endif

endif

//==== ATR Profit Target & Stop Loss ====

atrperiod = 20

atr = AverageTrueRange[atrperiod]

p = 7 //6

l = 8 //7 optimised to 4

set target profit p*atr

set stop ploss l*atr

SET STOP $LOSS sl

Hi. Great coding. I will try the Volatility filter

How does the daily TF-code look like?

Would u like to explain this 🙂

if onmarket then

if dayofweek=0 and (hour=0 and minute>=57) and abs(dopen(0)-dclose(1))>50 and positionperf(0)>0 then

if shortonmarket and close>dopen(0) then

exitshort at market

endif

if longonmarket and close<dopen(0) then

sell at market

endif

endif

endif

if you want to run this on a 5min TF, surely you need to add Timeframe(default) somewhere? like just above the volatility?

also, might be improved to keep the entry within the NDQ open hours

Tradetime = time >=143000 and time <210000//UK

in the ATR trail you want:

once tsminstop = 4

as that’s a given by IG

this is what I get on 1m bar BT

Is this the backtest with ur adjustments, nonetheless?

no, that’s the original. i haven’t done any other tests, just my first thoughts.

Hi

My apologies, I see I posted the wrong code for the strategy you see in the screenshots. Will rectify when I get back.

Working this on to a 15 min time frame. The 1M back test shows the downside testing lower time frame strategies on the standard 200k bars, and you don’t get to see how it performs through periods of real market stress.

There is something there. I might try having a go at creating a 15 min version myself. Higher time frames are definitely the way forward.