I guess position sizing is due to money management, but OTT and not conducive to stress free trading.

contract size is 1 too, for the none MM vision, even the MM vision the Position size and the contract size are always 1:1

So do profits on your System cover margin requirements?

Let’s put figures into the MM pos size on NASDAQ.

Assume you are Retail Trader @ 5% Margin?

So pos size 3000 x 20000 (nasdaq) x 5% = 3,000,000 Margin.

This new coffee must be watered down, above can’t be right surely? But if it is then that is why I couldnt sleep … even if funded by profits?? 😀

hi, thanks for the comment, i am not sure i get what you mean.

take a look the attached, it is the same code with MM but lower the auto add % when lose (1/3 of the original), you can see the way it grow is the same but less as the system reinvest less., it can make the % in any less, all depends on the feeling of comfortable, 0-12, the none MM vision is 0, this one attached is 4, so it work any % in between 0-12, in fact it would even 13,14,15, but i drop that as it started to much as my aim is to keep the system can run on itself without any worrying.

ps. this system do not just statically keep adding more position/contract, it only add at each lose.

I am not sure if this answer your question, as i mention in the post that figured out the best balance is £10k capital(cash) start with 1 position/contract, this balance would with either with MM or not, example, it is high chance will be fail if £2k and start with 1 position/contract, as it can easily get to a point there is not enough fun to buy and the system just stop. in the case (2k) it is very play with luck which hope earning would happen first before the lose, which is not the ideal.

Are you trading your System on Demo Account or on a Real Live Account with Real money?

i have both running real money and demo. they both cam out the same, only occasionally 1 or 2 trad not the same.

i am not sure i get what you mean.

So if you are trading on Real Account with Real money you would have to cover 3,000,000 Margin with a position size of 3,000 on NASDAQ (@5% Margin).

What is your current piosition size on Real Account with Real money?

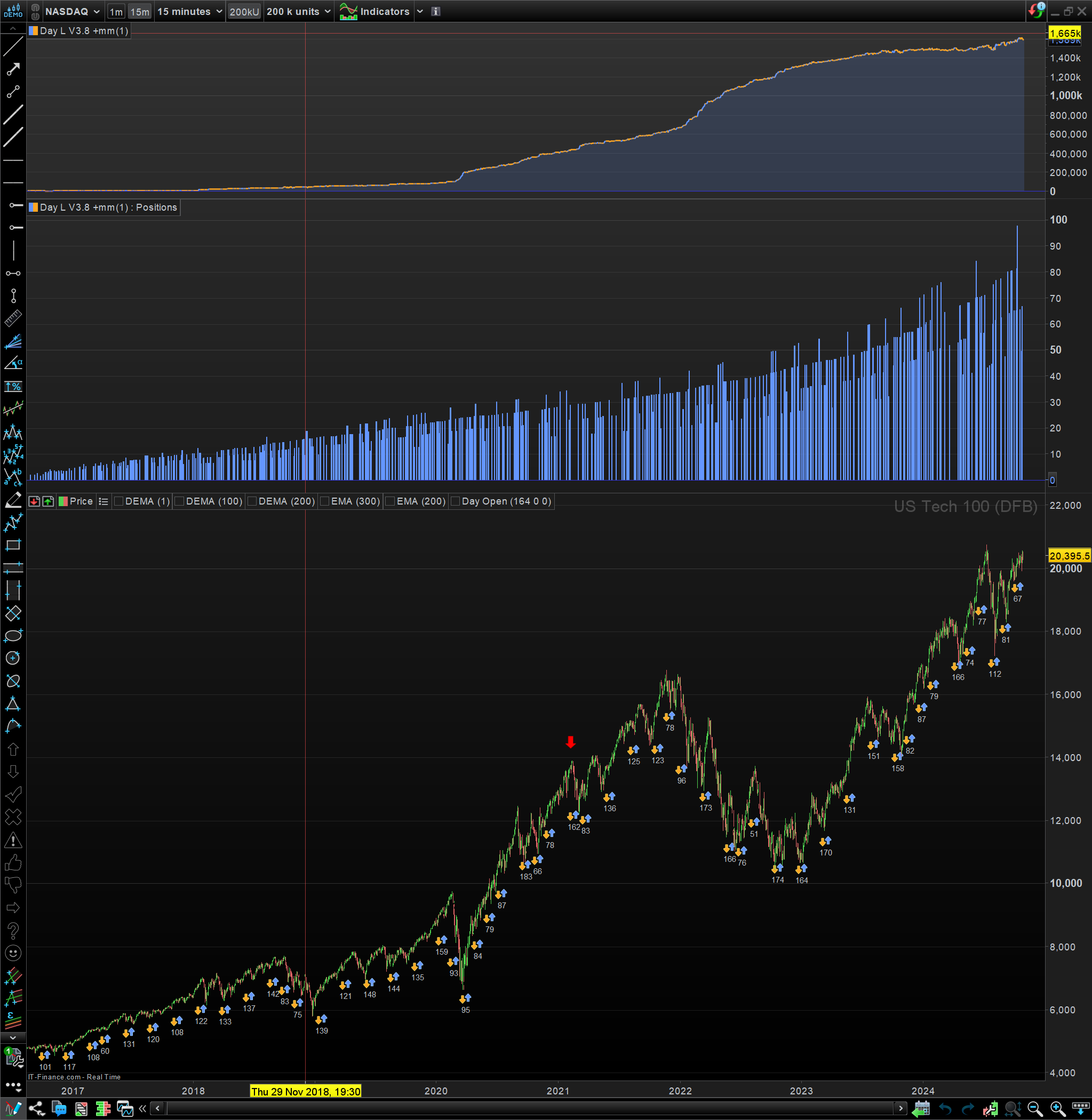

the real account started with position/contract 1 and now it grow to 3.5, this one with capital 10k, since April 2024, it has the same result as the demo, or backtest.

basic on yours

3,000,000 Margin with a position size of 3,000 , therefore position size of 1 is 1000 Margin

in my one I mention position size of 1 should have 10,000 Margin to be safe.

please correct me if i am wrong

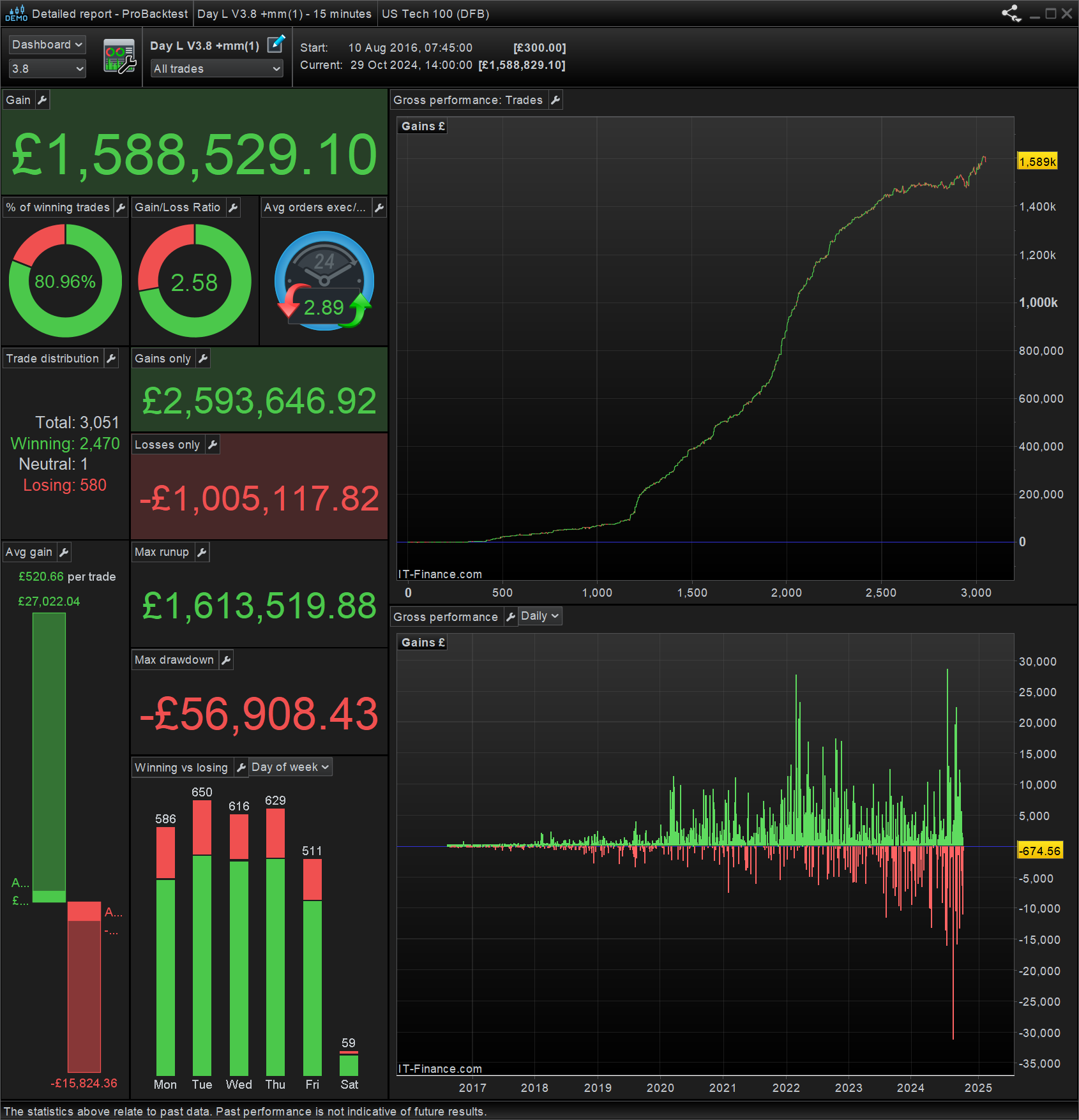

example, like this one from 08-10-2016 to 27-12-2022 (the bottom at time), see attached, the position/contract grow to 279.76 and it has 7,850,645 at that point,

so let call it 280*20000*5%= 280,000, at this point is far more than it requite.

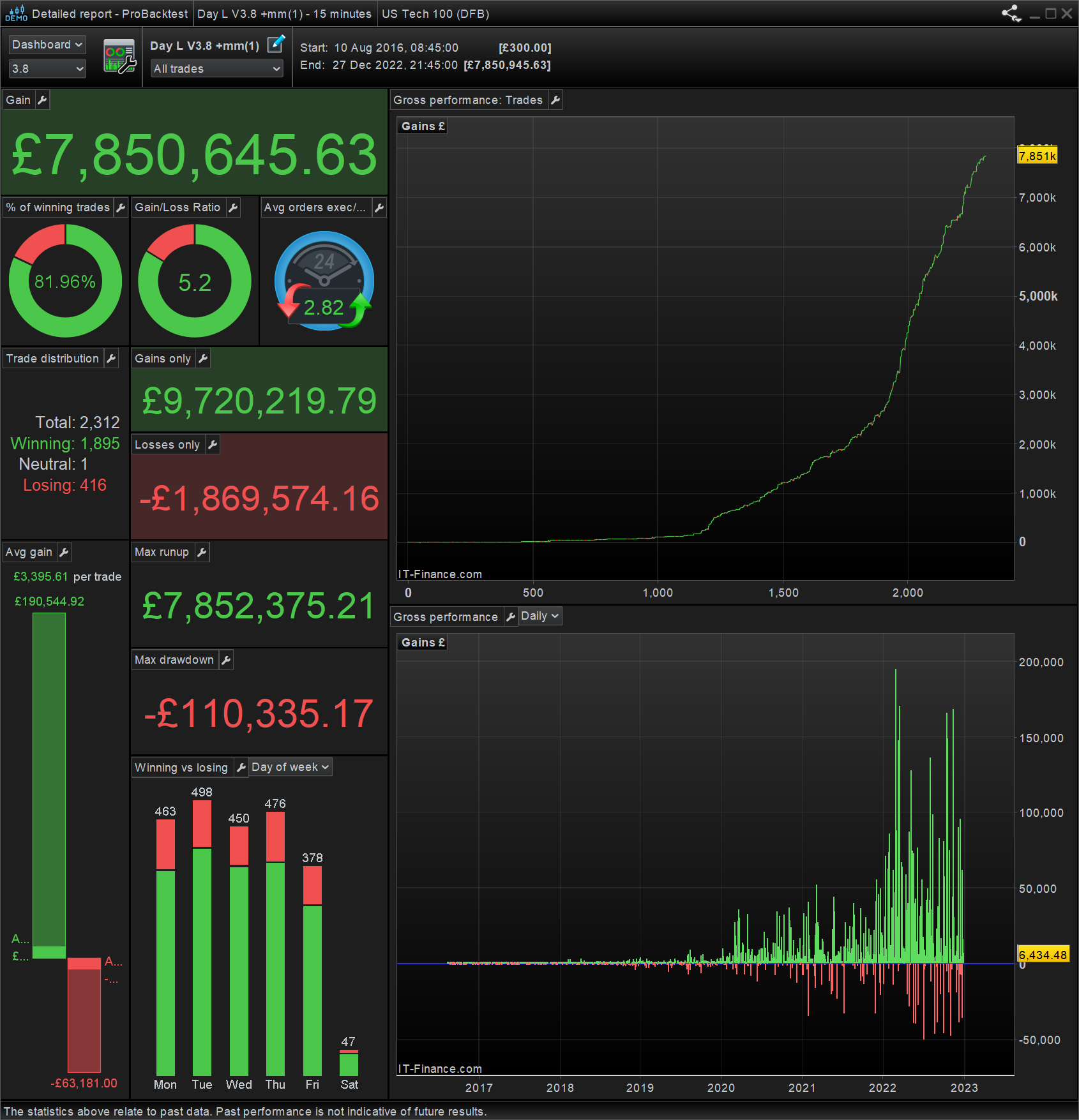

another example: 08-10-2016 to to 20-03-2020 (the bottom at time when covid ended), the position/contract grow to 45.64 and it has 427,685 at that point

so let call it 46*20000*5%= 46,000, at this point is far more than it requite.

but i calculated in safer way that each 1 position/contract should have 10k margin

just for anyone who interest for the time when covid (20-02-2020 to to 20-03-2020), see attached

JS

JSParticipant

Senior

Hi,

If I interpret it correctly, it is possible a kind of Martingale system where you increase your position after a loss?

Furthermore, you close your positions every day at 21:45:00, to start again the next day. Is this closing of your positions related to risk, or does it have to do with the overnight costs of IG?

If I interpret it correctly, it is possible a kind of Martingale system where you increase your position after a loss?

Yes, WingYip can hopefully confirm that he buys extra after a loss – I read that too but it could be a typo.

Btw, this is not necessarily Martingale as I just typed a post for this thread (not posted) where I kind of see and show the similarities with what I do myself, and this includes increasing after a loss – and NOT after a win. And this is not a Martingale system at all.

So WingYip – curious ! 🙂

Not sure if any misunderstanding. In IG 1size(prosition /contract) will cost correct rate, let say now is at 20000, the cost of each size is 20000/20( leverage) = 1000, my system is suggested each 1 size should have 10k for it to buy as well as for it to loss, such as 10k to start with, each size will cost 1000 and it leave 9000 to loss, let say the day loss 1000 than it will end up the end trading day is 9000 as the fund to buy return at the end of the day as tge trade close each day, I am not trying to tell you guys about it as we all know, I just try to explain what I understand.

Regard the end each day, it has many reason, small reason such as overnight fee, expecially the weekend overnight fee, also it is (I belive) when I do any backtest has the mix data to use, as each day become different data, otherwise when a trade on the market for longer the data become less to calculate, in this case it need to use OOS, and I feel even use OSS is not enough to make me feel comfortable it will work for a long time system. As we all know we could test a system in a short time with a choose timefarm, and even use OSS, it sounds great but them it doesn’t really work at other time frame such as in real time, also end each day (to me) the system become simply, clear and easy for myself to understand how it work and the development become manageable as the aim is to look for the most balance setting for all different days data in 8 year, and that’s the reason I use 15 min, although it could be 10min, but I want as much data as I can use for the development, and I always use the mix of the unit 200k, hope it make sense to you guys, thanks