JS

JSParticipant

Veteran

If you want to use different time frames, you have to put that above your code:

TimeFrame(5 minutes)

// Conditions to enter long positions

indicator1 = ExponentialAverage[8](close)

indicator2 = (High[1] + Low[1] + Close[1])/3

c1 = (indicator1[1] < indicator2[1])

indicator3 = ExponentialAverage[8](close)

indicator4 = (High[1] + Low[1] + Close[1])/3

c2 = (indicator3 > indicator4)

TimeFrame(15 minutes)

indicator5 = Close[1] + (High[1]-Low[1]) * (1.1 / 4)

c3 = (close > indicator5)

indicator6 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c4 = (low[1] < indicator6[1])

indicator7 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c5 = (close > indicator7)

Thanks JS,

I haven’t made myself clear.

The code is all based on the 1m chart . So visually, I have two sets of camarilla indicators on my chart (5m & 15m). On this 1m chart I have a set of criteria I want to meet based on 5m cam levels & another set of conditions to meet based on the 15m cam levels.

// Conditions to enter long positions

//Set of criteria to meet on the 5m cam

indicator1 = ExponentialAverage[8](close)

indicator2 = (High[1] + Low[1] + Close[1])/3

c1 = (indicator1[1] < indicator2[1])

indicator3 = ExponentialAverage[8](close)

indicator4 = (High[1] + Low[1] + Close[1])/3

c2 = (indicator3 > indicator4)

//Set of criteria to meet on the 15m cam

indicator5 = Close[1] + (High[1]-Low[1]) * (1.1 / 4)

c3 = (close > indicator5)

indicator6 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c4 = (low[1] < indicator6[1])

indicator7 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c5 = (close > indicator7)

Thanks for your patience.

JSParticipant

Veteran

Put your indicators under the correct time frame and put your conditions under time frame “default” (1 minute)

TimeFrame(15 minutes)

indicator5 = Close[1] + (High[1]-Low[1]) * (1.1 / 4)

indicator6 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

indicator7 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

TimeFrame(5 minutes)

indicator1 = ExponentialAverage[8](close)

indicator2 = (High[1] + Low[1] + Close[1])/3

indicator3 = ExponentialAverage[8](close)

indicator4 = (High[1] + Low[1] + Close[1])/3

TimeFrame(Default)

c1 = (indicator1[1] < indicator2[1])

c2 = (indicator3 > indicator4)

c3 = (close > indicator5)

c4 = (low[1] < indicator6[1])

c5 = (close > indicator7)

Ill have to take a look at this tomorrow.

Can you just confirm if they need to appear in the code in the order you have written them?

Thanks.

P

JSParticipant

Veteran

Hi Paulg999

This must indeed be the order..

Good luck and we’ll probably talk to each other again… 😉

Hi JS,

I got a chance to re-enter my code in the right order & re-run it but something is still drastically wrong (with my interpretation no doubt).

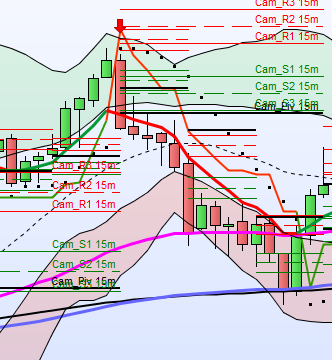

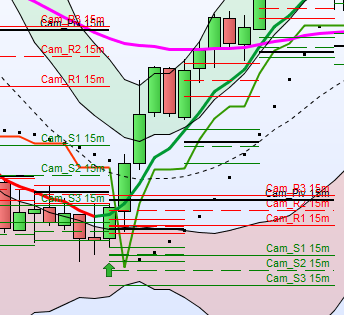

I have attached the itf file along with a summary of the strategy & the code written. Underneath the summary, I have given an example trigger of both short & long along with a PNG file showing each example

CP = Current Period / PP = Previous Period.

| Long |

Short |

|

|

| Using 15m [Camarilla Levels] |

Using 15m [Camarilla Levels] |

| Low < S2 (PP) |

High > R2 (PP) |

| Close > R2 (CP) |

Close < S2 (CP) |

|

|

| Using 5m [Camarilla Levels] |

Using 5m [Camarilla Levels] |

| 8ema < [Pivot Point] (PP) |

8ema > [Pivot Point] (PP) |

| 8ema > [Pivot Point] (CP) |

8ema < [Pivot Point] (CP) |

| Close > [R3] (CP) |

Close < [S3] (CP) |

|

|

|

|

| (Default) |

(Default) |

| Close < BB20-2.3 Upper (Boll2) (CP) |

Close < BB20-2.3 Lower (Boll2) (CP) |

| 55ema < 144ema (CP) |

55ema > 144ema (CP) |

| 8ema < 21sma (CP) |

8ema > 21sma (CP) |

| 8ema < 55ema (CP) |

8ema > 55ema (CP) |

| Close < 55ema (CP) |

Close > 55ema (CP) |

| Close < 21sma (CP) |

Close > 21sma (CP) |

|

|

| Exit = Close (CP) < Low (PP) |

Exit= Close (CP) > High (PP) |

|

|

|

|

| US30 26-09-22 1m @ 17:45 |

US30 22-09-22 1m @ 20:15 |

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Conditions to enter long positions

TimeFrame(15 minutes)

indicator1 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c1 = (low[1] < indicator1[1])

indicator2 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c2 = (close > indicator2)

TimeFrame(5 minutes)

indicator3 = ExponentialAverage[8](close)

indicator4 = (High[1] + Low[1] + Close[1])/3

c3 = (indicator3[1] < indicator4[1])

indicator5 = ExponentialAverage[8](close)

indicator6 = (High[1] + Low[1] + Close[1])/3

c4 = (indicator5 > indicator6)

indicator7 = Close[1] + (High[1]-Low[1]) * (1.1 / 4)

c5 = (close > indicator7)

TimeFrame(Default)

indicator8 = Average[20](close)+2.3*std[20](close)

c6 = (close < indicator8)

indicator9 = ExponentialAverage[55](close)

indicator10 = ExponentialAverage[144](close)

c7 = (indicator9 < indicator10)

indicator11 = ExponentialAverage[8](close)

indicator12 = Average[21](close)

c8 = (indicator11 < indicator12)

indicator13 = ExponentialAverage[8](close)

indicator14 = ExponentialAverage[55](close)

c9 = (indicator13 < indicator14)

indicator15 = ExponentialAverage[55](close)

c10 = (close < indicator15)

indicator16 = Average[21](close)

c11 = (close < indicator16)

IF c1 AND c2 AND c3 AND c4 AND c5 AND c6 AND c7 AND c8 AND c9 AND c10 AND c11 THEN

BUY 1 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

c12 = (close < low[1])

IF c12 THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

TimeFrame(15 minutes)

indicator17 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c13 = (high[1] > indicator17[1])

indicator18 = Close[1] + (High[1]-Low[1]) * (1.1 / 6)

c14 = (close < indicator18)

TimeFrame(5 minutes)

indicator19 = ExponentialAverage[8](close)

indicator20 = (High[1] + Low[1] + Close[1])/3

c15 = (indicator19[1] > indicator20[1])

indicator21 = ExponentialAverage[8](close)

indicator22 = (High[1] + Low[1] + Close[1])/3

c16 = (indicator21 < indicator22)

indicator23 = Close[1] + (High[1]-Low[1]) * (1.1 / 4)

c17 = (close < indicator23)

TimeFrame(Default)

indicator24 = Average[20](close)-2.3*std[20](close)

c18 = (close > indicator24)

indicator25 = ExponentialAverage[55](close)

indicator26 = ExponentialAverage[144](close)

c19 = (indicator25 > indicator26)

indicator27 = ExponentialAverage[8](close)

indicator28 = Average[21](close)

c20 = (indicator27 > indicator28)

indicator29 = ExponentialAverage[8](close)

indicator30 = ExponentialAverage[55](close)

c21 = (indicator29 > indicator30)

indicator31 = ExponentialAverage[55](close)

c22 = (close > indicator31)

indicator32 = Average[21](close)

c23 = (close > indicator32)

IF c13 AND c14 AND c15 AND c16 AND c17 AND c18 AND c19 AND c20 AND c21 AND c22 AND c23 THEN

SELLSHORT 1 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

c24 = (close > high[1])

IF c24 THEN

EXITSHORT AT MARKET

ENDIF

Lets see what this uncovers……..

JSParticipant

Veteran

Hi Paulg999

I have time to look at your code again over the weekend…

JSParticipant

Veteran

Hi Paulg999

I see several double indicators (ind1 = ind2, ind3 = ind5, ind4 = ind6, etc.)

It’s not wrong but not necessary and somewhat confusing.

Furthermore, I don’t see any errors in your code…

What goes “dramatically wrong”?

Hi JS,

Apologies for the late reply. I am currently in the middle of a house sale which is proving to be very time consuming. I will get back to you in a few weeks when things have calmed down.