Let me unsolicitedly add :

When the technical issue would be out of the way, I think it still can not work, but not sure. You started out in this topic with questions about the adding of parameters. I think that would be a necessity in your situation, so that idea seemed good. Thus, the parameters from the backtesting can be passed on to the Indicator code. I think as how you have it currently, they live on their own (with the same name).

But the technical issue must be solved first. And as said, possibly by following some (more special ?) guidelines.

What you want to do is perfectly normal for Backtesting and Live. But in the MarketPlace situation all is a bit different in PRT (so that would be their issue, not Nicolas).

For @Nicolas : I now recall the similar situation. This was from [now anonymous] who always provided a 100% profitable trades. But all what happened was that his StopLoss parameter was set to the same too high number and could not be influenced by BackTesting. The rest of his parameters were just in-code, so backtesting with *those* seemed to work nicely. But without active StopLoss all looks nice, until you see what causes it.

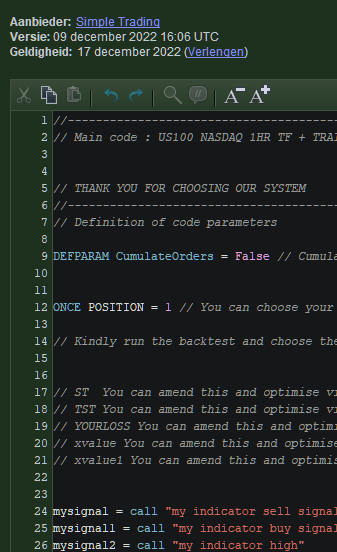

Dizi, I now see that I can also show the time of the version.

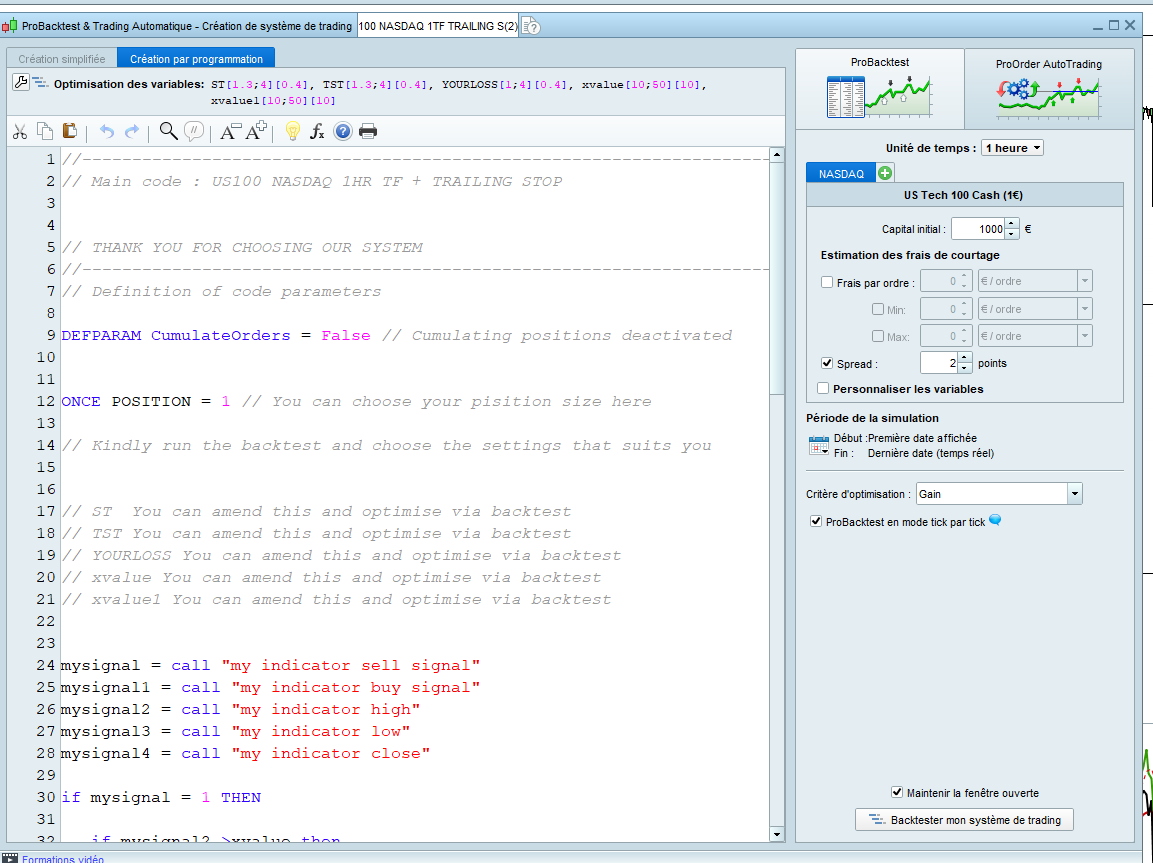

you have to duplicate the version to modify the variables

… which is obviously what I did … (see screenshot a few posts back)

PeterST,

I am uncertain why it does not work at your end. Please find the attached backtest thru prt via my broker, thru prt direct.

The script has been running smoothly since July, also attached.

Hi Dizi,

Buy your own trial, and try to run the backtest from there. Did you do that ? Can you even do that ? (I just don’t know)

To be sure : my broker is IG and it is through PRT-Sponsored (so I have an account with PRT-IB (which would be PRT-Direct) but can obviously only use IG for broker because IB can’t do Autotrading (yet). Notice that I could do backtesting with IB, though.

Does this make a difference somewhere ?

That it can run well in Live is totally expected.

PeterST,

I think I know what the issue is.

I have recorded this issue and solution. Please check this

Very good find !

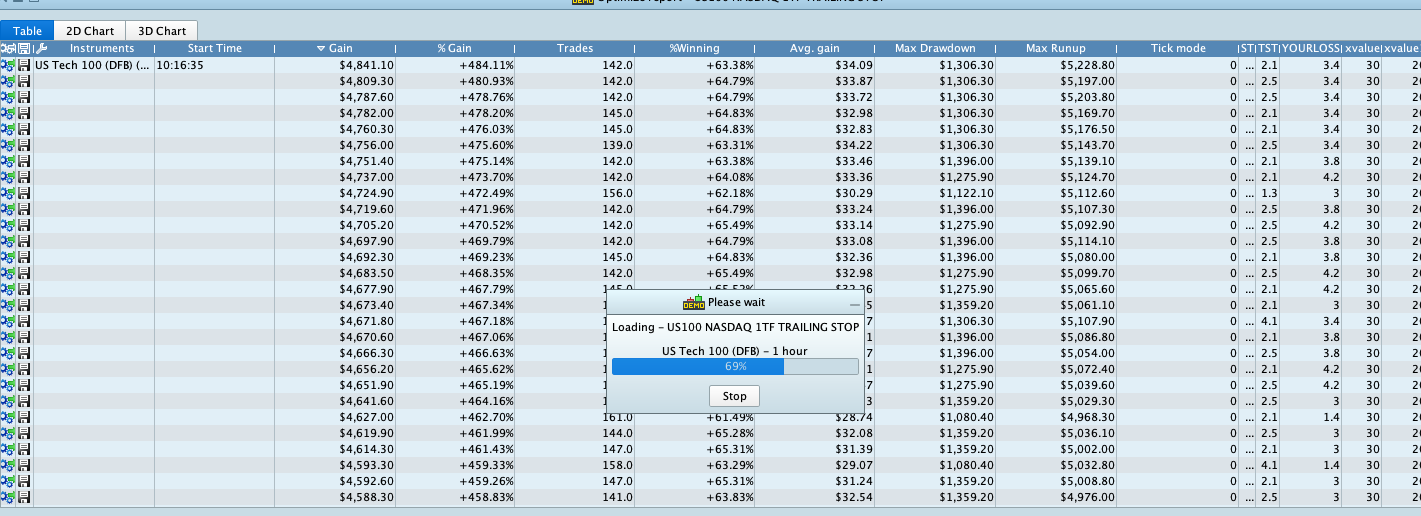

But it is still different. You show the execution of the Backtest of your original (the one which can not be adjusted). That indeed works.

But a copy like one of those in that tree (you have the copies too), still does not work. I suppose this is workable now, but we can’t adjust the parameters (current enumerating by 9800 iterations) and we also can’t adjust the code itself (because that requires a copy).

Unless I see it all wrongly …

Hi PeterST,

Please check the movie update below

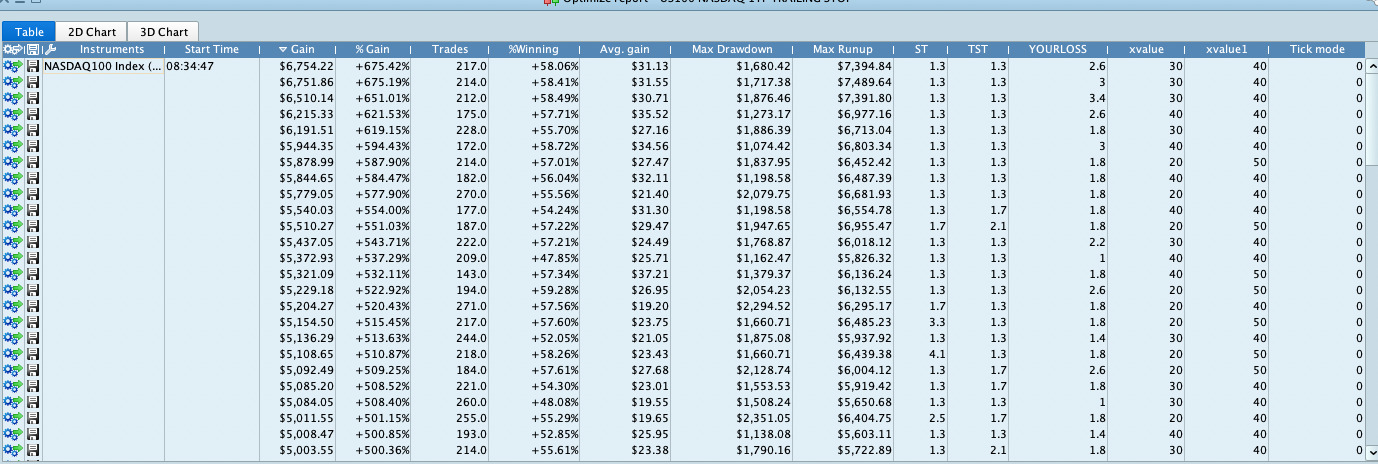

The backtest is running and optimising the strategy based on predefined range of values. This range of values cannot be modified. The code itself also cannot be modified.

Hope it helps.

Haha, it is hard for me to tell / follow what you want to show with that video.

The code itself also cannot be modified.

Not from the Indicators. But from the main strategy, sure it can. E.g. change %LOSS to $LOSS. Everything.

Of course you need to do that in the copy you made (from the top of my head S1 or S2 on your screen).

But influencing the Backtest variables … no. So all we got is the iteration of all the combinations which *you* implied, working. Limit the range here and there so no 9800 iterations come from it, and it could be doable. But not really (not for me) because all what would come from it is an over-optimised strategy. Right ?

Been using this for a last few days in different tf and so far is pretty good