Backtest with Ichimoku, Maximum 36 periods, ADX, MACD and stop with Ichimoku, MACD and %Williams

DEFPARAM CumulateOrders=False

DEFPARAM NOCASHUPDATE = False

REM Comprar/Comprare/Acheter/Buy

myKijun, myTenkan, myChikou, mySpanA, mySpanB = CALL "Ign Ichimoku 1"[0](close)

c1 = (Close > myTenkan)

c2 = (Close > myKijun)

c3 = (Close > mySpanA)

c4 = (Close > mySpanB)

c5 = (Close > Close[26])

c6 = (MACDline[12,26,9](close) > 0)

c61 = (MACDline[12,26,9](close) > MACDSignal[12,26,9](close))

c7 = (Close = highest[n] (close))

c8 = (ADX[14] > ADX[14][1])

c9 = (ADX[14] > DIminus[14](close))

c10 = (DIplus[14](close) > DIminus[14](close))

IF c1 and c2 and c3 and c4 and c5 and c6 and c61 and c7 and c8 and c9 and c10 THEN

BUY 1000 cash AT MARKET

ENDIF

coste = tradeprice

REM Vender/Vendere/Vendre/Sell

if (coste > myKijun) then

myStop = myTenkan

elsif (coste < myKijun) and (coste > mySpanB) then

myStop = myKijun

elsif (coste < mySpanB) then

myStop = mySpanB

endif

IF close < myStop or Williams[14](close) < -80 or MACDline[12,26,9](close) < 0 THEN

sell at market

//SELL AT myStop STOP

ENDIF

Hi! Thanks for sharing your trading strategy idea. Would you mind to tell us more about it please? What is the timeframe to be used? And for what instrument? It seems to work well on major trend, by looking at the picture you provide! 🙂

Line 13 is incorrect, MACDSignal is not a PRT recognised Indicator (it should be … it would make our lives easier!?)

Surely it can only work if coded as …

c61 = (MACDline[12,26,9](close)) > ExponentialAverage[9](MACDline[12,26,9](close))

MACDSIGNAL is now an instruction in PRTv11.

MACDsignal

I think we might be reaching the time where it would be useful if people mentioned the version number if they coded it on v11.

Dear Nicolas,

Only for Weekly, confirmed with monthly.

I send you a indicator than can help you for decissions.

I work only with sotcks and I select only the best stocks for financials, growth and moat.

If you need something else write me.

I apologize for my bad english. I’m spanish 😉

I backtested more and I changed a few things.

Now the code is enhanced.

I work on weekly, but I compare each signal with monthly for confirmation.

Anybody else tried this on v10.3?

Trying with the latest codes above, I get the attached errors. (The original code on the original post had similar errors also).

Even if I include below then more errors messages show … e.g. cc is not used.

If MyChikou or my0 OR Mybs or mybi or mycoste Then

Endif

@inavsan does the above code work perfectly fine on your Platform??

Update:

I’ve got it working now after making a few changes here and there.

I will post the amended code shortly … results looks good!!

Zigo

ZigoParticipant

Master

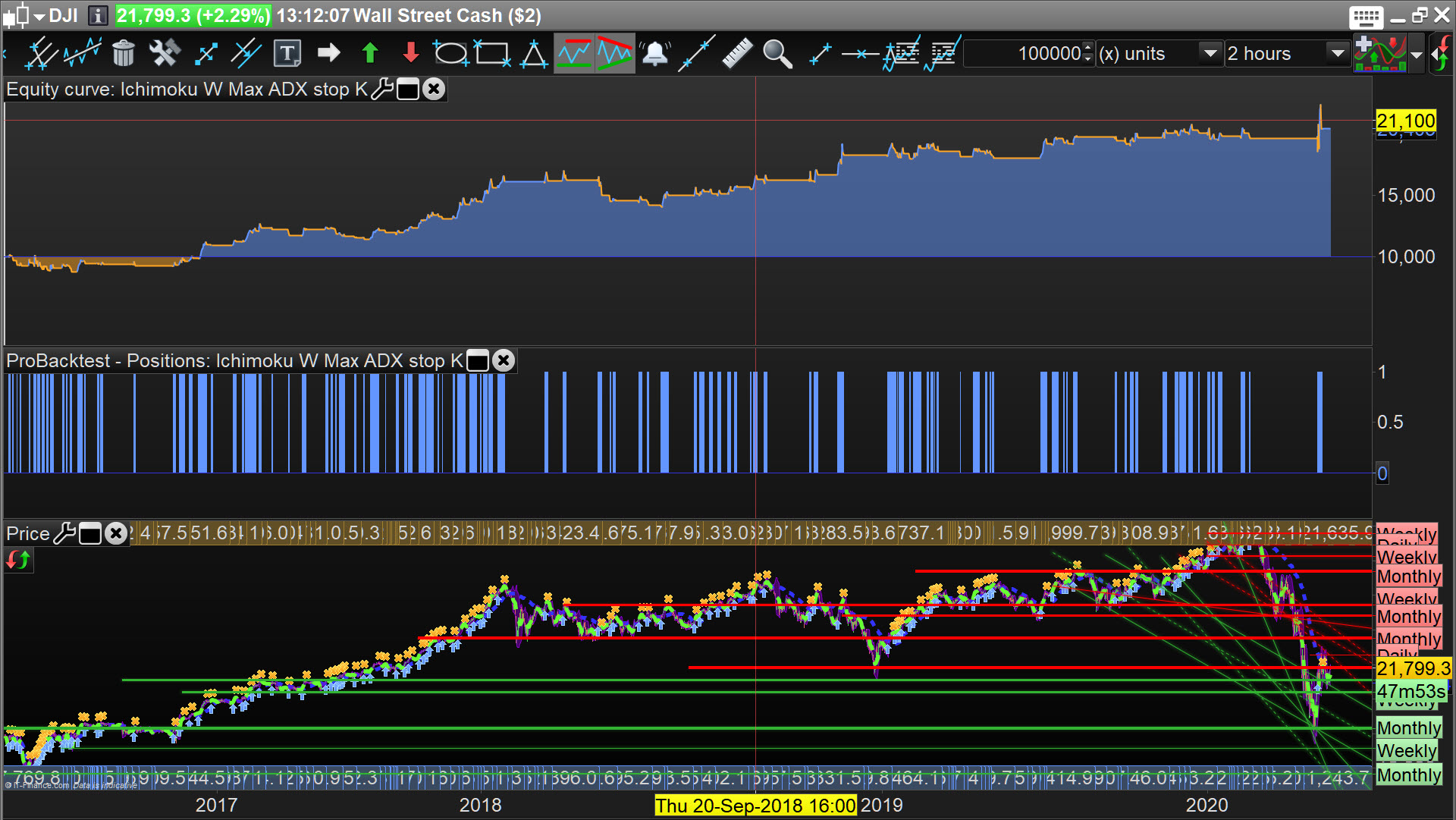

Ichimoku is a very good indicator on its own. I think it doesn’t need any other indicator.

Therfore I have tested it without Macd and ADX (green) (c1, c2, c3, c4 and c5)

and also with Macd and ADX (bleu) (c1, c2, c3, c4, c5, c6, c61, c7, c8, c9 and c10)

DEFPARAM CumulateOrders=False

DEFPARAM NOCASHUPDATE = False

once n= 9

once m= 3*n-1

REM Comprar/Comprare/Acheter/Buy

myTenkan=(highest[n](high)+lowest[n](low))/2

myKijun=(highest[m](high)+lowest[m](low))/2

myspanA=(myTenkan+myKijun)/2

mySpanB=(highest[2*m](high)+lowest[2*m](low))/2

c1 = (Close > myTenkan)

c2 = (Close > myKijun)

c3 = (Close > mySpanA)

c4 = (Close > mySpanB)

c5 = (Close > Close[26])

IF c1 and c2 and c3 and c4 and c5 THEN

BUY 1 contract AT MARKET

ENDIF

coste = tradeprice

REM Vender/Vendere/Vendre/Sell

if (coste > myKijun) then

myStop = myTenkan

elsif (coste < myKijun) and (coste > mySpanB) then

myStop = myKijun

elsif (coste < mySpanB) then

myStop = mySpanB

endif

IF close < myStop or Williams[14](close) < -80 or MACDline[12,26,9](close) < 0 THEN

sell at market

//SELL AT myStop STOP

ENDIF

Thank You inavsan for sharing your code with us all … jolly decent of you! 🙂

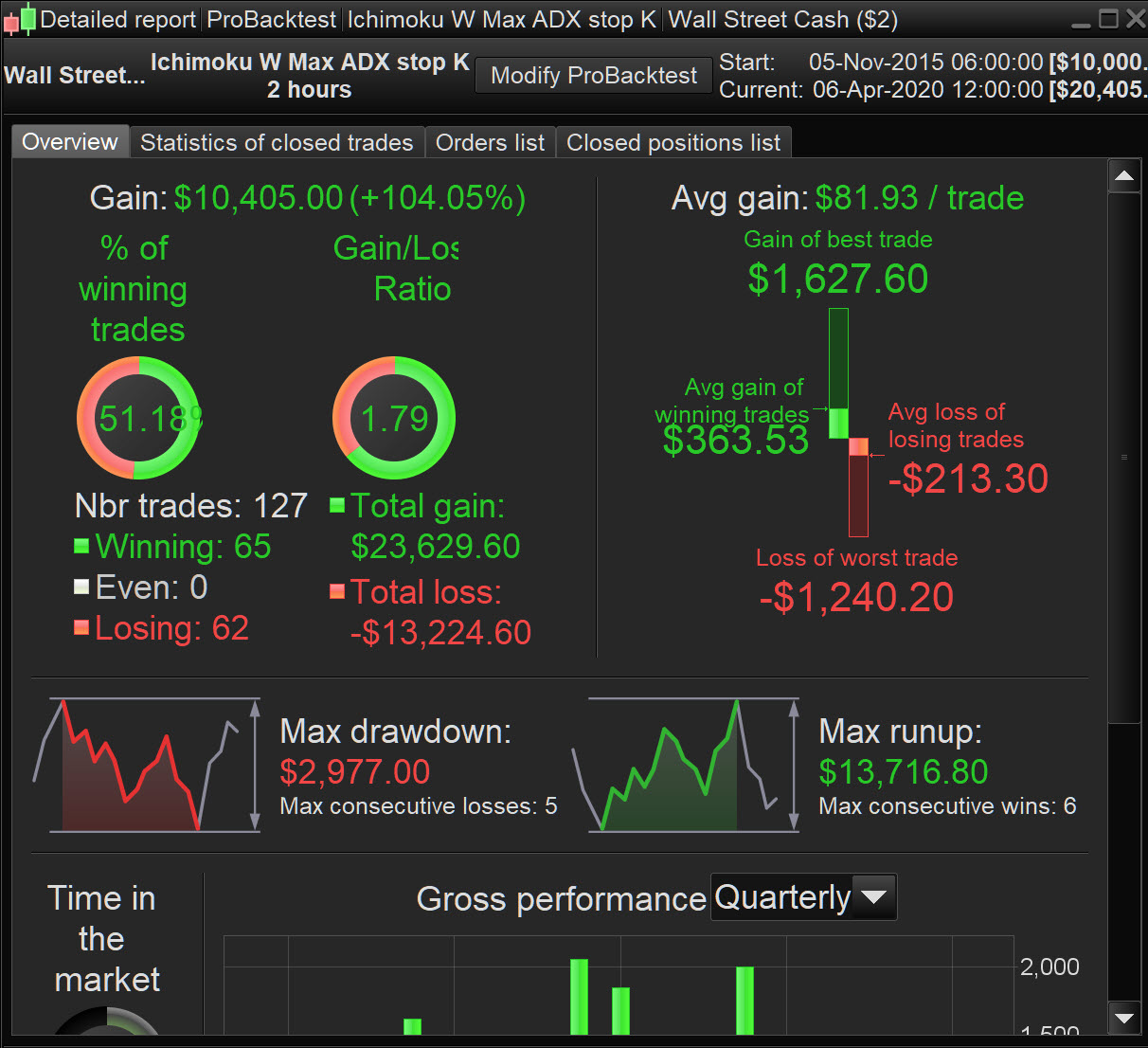

Results attached with spread = 7.

If you make improvements, please post here.

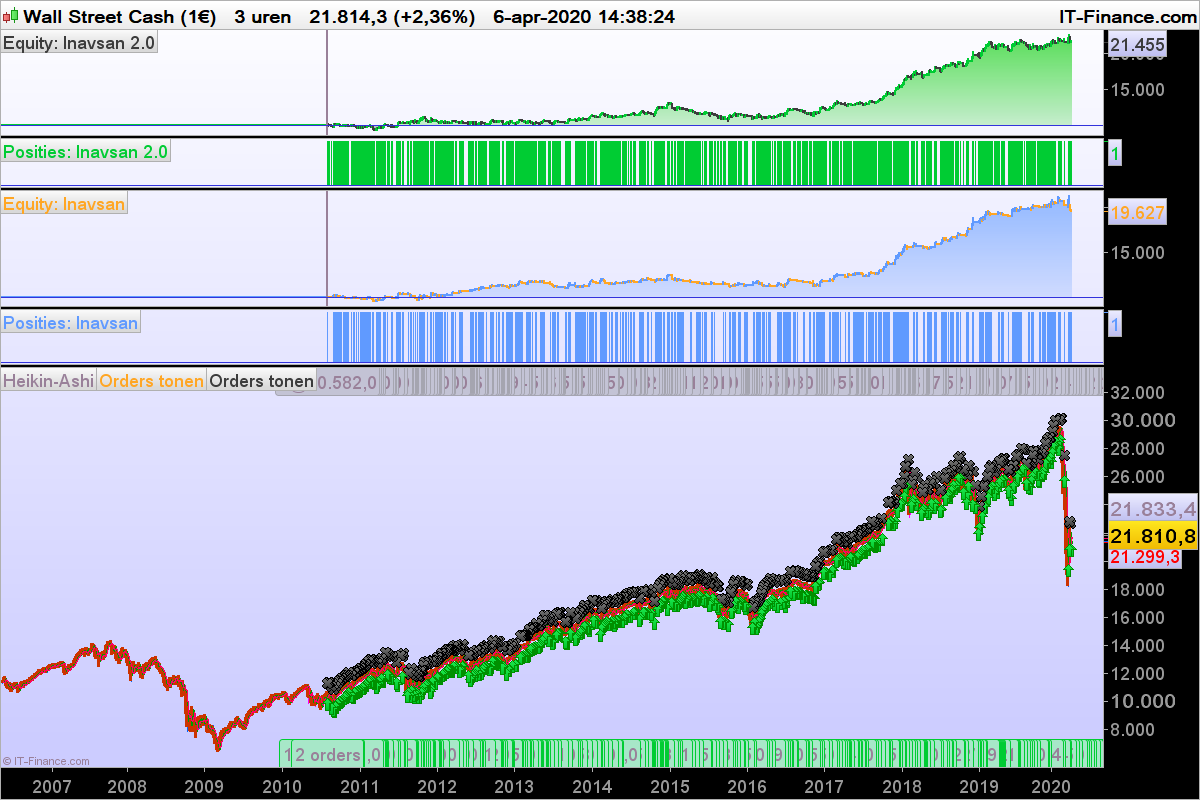

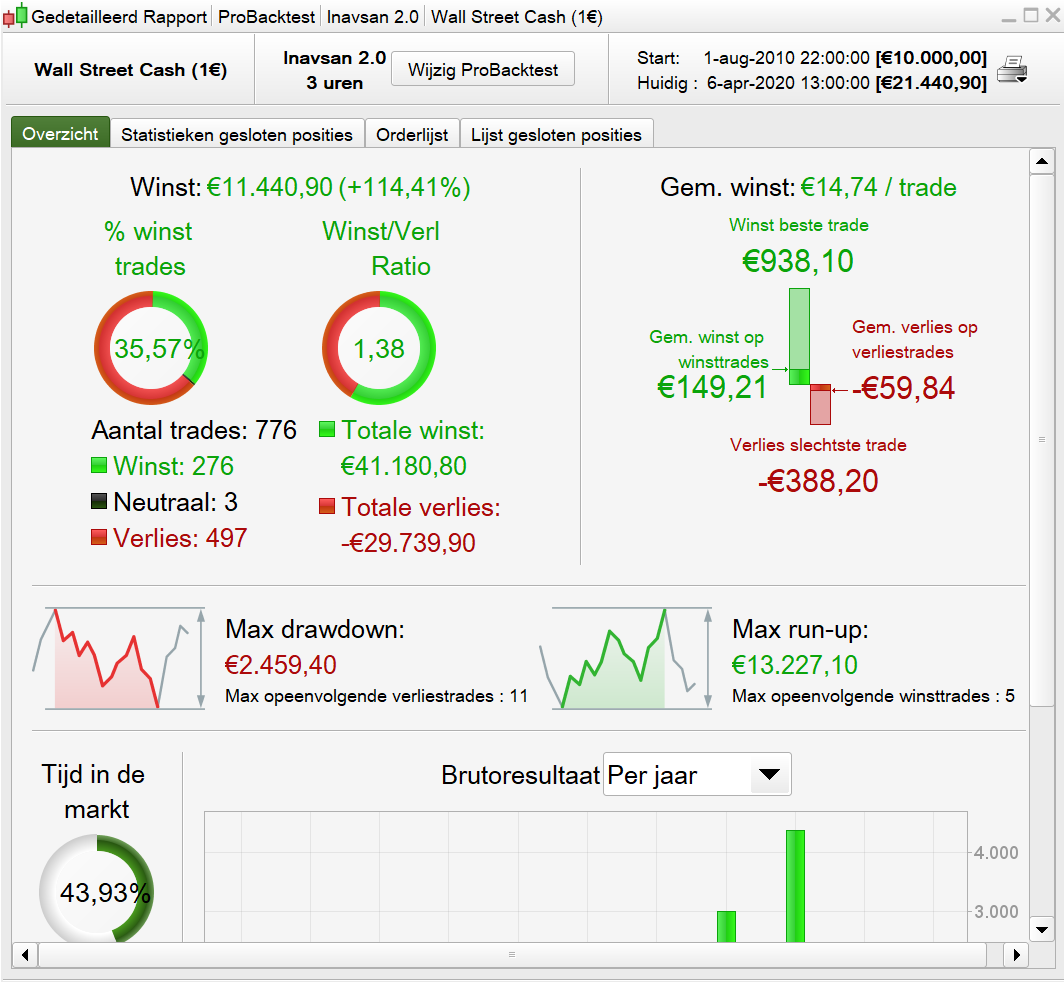

How long term … you don’t show bottom line so we cant see how many years? 🙂

Do you mean 200k bars and what is the TF – 3 uren … is that 3 hours?

ZigoParticipant

Master

DEFPARAM CumulateOrders=False

DEFPARAM NOCASHUPDATE = False

once n= 9

once m= 3*n-1

REM Comprar/Comprare/Acheter/Buy

myTenkan=(highest[n](high)+lowest[n](low))/2

myKijun=(highest[m](high)+lowest[m](low))/2

myspanA=(myTenkan+myKijun)/2

mySpanB=(highest[2*m](high)+lowest[2*m](low))/2

c1 = (Close > myTenkan)

c2 = (Close > myKijun)

c3 = (Close > mySpanA)

c4 = (Close > mySpanB)

c5 = (Close > Close[26])

c6 = Close < mytenkan

c7 = close < myKijun

c8 = close < mySpanA

c9 = close < mySpanB

c10= close < close[26]

IF c1 and c2 and c3 and c4 and c5 THEN

BUY 1 contract AT MARKET

ENDIF

coste = tradeprice

REM Vender/Vendere/Vendre/Sell

if (coste > myKijun) then

myStop = myTenkan

elsif (coste < myKijun) and (coste > mySpanB) then

myStop = myKijun

elsif (coste < mySpanB) then

myStop = mySpanB

endif

IF close < myStop or Williams[14](close) < -80 or MACDline[12,26,9](close) < 0 THEN

sell at market

//SELL AT myStop STOP

ENDIF

If c6 and c7 and c8 and c9 and c10 then

sellshort 1 contract at market

endif

//Kost Verkoop is KV

KV = Tradeprice

if (KV < myKijun) then

myStop = myTenkan

elsif (KV > myKijun) and (KV < mySpanB) then

myStop = myKijun

elsif (KV > mySpanB) then

myStop = mySpanB

endif

IF close < myStop or Williams[14](close) < -80 or MACDline[12,26,9](close) < 0 THEN

sell at market

//SELL AT myStop STOP

ENDIF

Dear Grahal,

I only work weekly.

My backtests are made from the begin of data (about 1995) from the last dat available.

I only work with V11.