Hello,

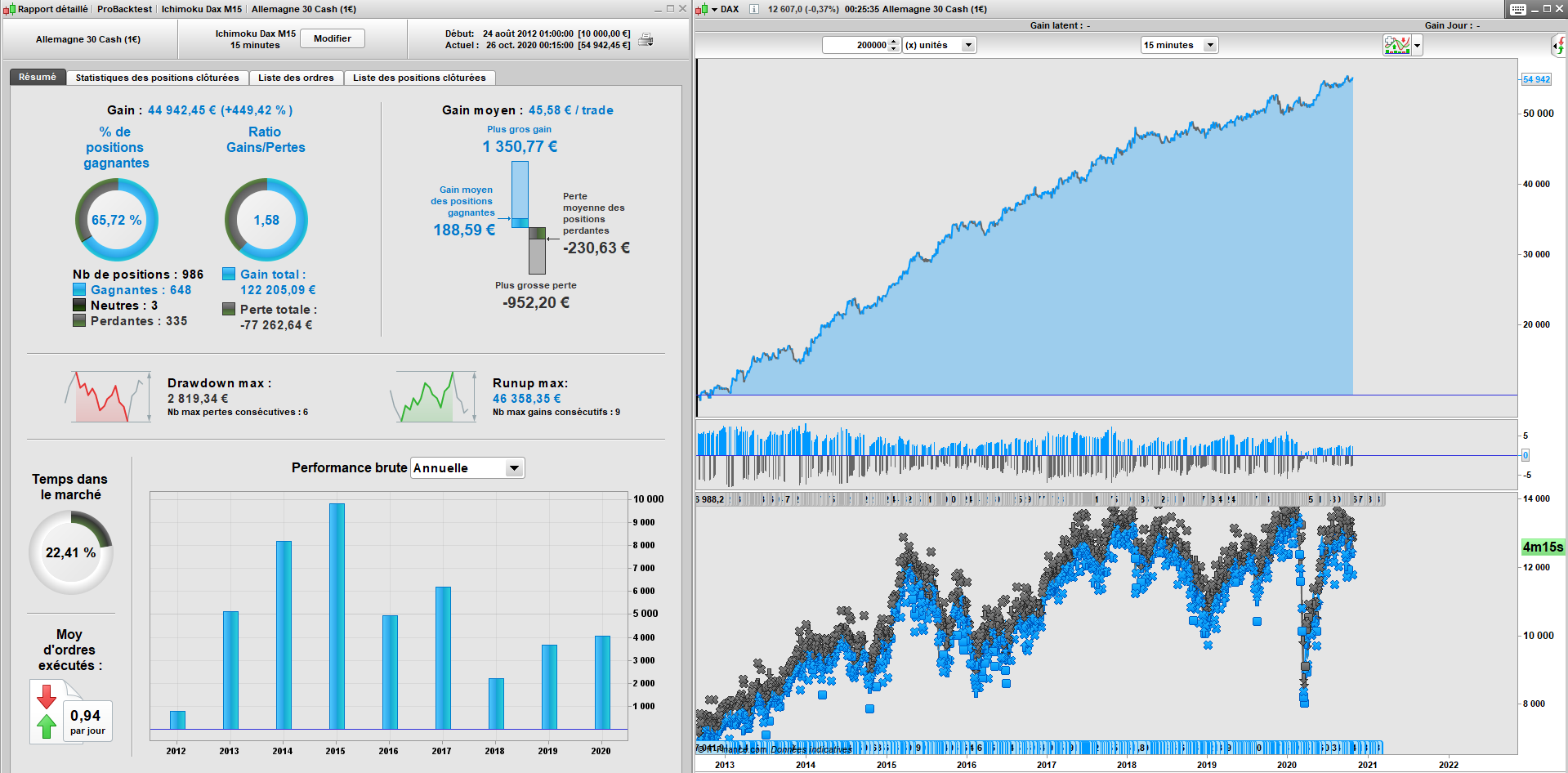

I present you a strategy based on ichimoku and some optimizations.

Ichimoku is optimized to give the best components while keeping the same ratios of difference between the components of the ichimoku.

The values are therefore simply multiplied.

Purchases and sales are processed independently, which makes the backtest more profitable.

Also a currency management system is incorporated into the strategy and can be modified as required.

I wouldn’t have 100% confidence in this strategy given that it has just been developed and we know the effects of optimization.

However, I find it an interesting basis, which could be applied in other markets.

Maybe some ideas could be added to this one to make it more profitable!

Feel free to give your opinions and suggestions.

IV

//

//=/===============/=//=/===============/=//=/ Basic settings

//

//=/ Cumulation of Orders

DefParam CumulateOrders = False

//

//=/===============/=//=/===============/=//=/ Management Settings

//

//=/ Capital

Capital = 10000

//=/ Percentage Risk

Risk = 1

//=/ Reinvestment

Reinvestment = 0

//

//=/===============/=//=/===============/=//=/ Calcul Management Settings

//

//=/ Reinvestment Settings

if Reinvestment = 1 then

Capital = Capital + StrategyProfit

elsif Reinvestment = 0 then

Capital = Capital

endif

//=/ Lotss Settings

Lotss = ((Capital*Risk) /100) /RiskVolatility

if Lotss < 0.5 then

Lotss = 0.5

endif

if Lotss > (0.0015*Capital) then

Lotss = 0.0015*Capital

endif

//=/ Risk by Volatility Settings

VL1 = Average[500,0](TypicalPrice)

VH1 = VL1 + (1*Average[500,1](Range))

VD1 = VL1 - (1*Average[500,1](Range))

VL2 = Average[1000,0](TypicalPrice)

VH2 = VL2 + (1*Average[1000,1](Range))

VD2 = VL2 - (1*Average[1000,1](Range))

VH = (VH1+VH2) /2

VD = (VD1+VD2) /2

RiskVolatility = VH-VD

//

//=/===============/=//=/===============/=//=/ Activation Settings

//

//=/ Buy Activation

BuyActivation = 1

//=/ Sell Activation

SellActivation = 1

//

//=/===============/=//=/===============/=//=/ Time Settings

//

//=/ TimeTable

Before = Time >= 080000

After = Time < 220000

TTime = Before and After

//=/ No Trade

if OpenDayOfWeek = 5 and Time > 200000 then

NoTrade = 1

else

NoTrade = 0

endif

//

//=/===============/=//=/===============/=//=/ Indicator Settings

//

//=/ Ichimoku Buy

ICBuy = 1.13

BSpanA = (BTenkan[26*ICBuy]+BKijun[26*ICBuy])/2

BTenkan = (highest[9*ICBuy](high)+lowest[9*ICBuy](low))/2

BKijun = (highest[26*ICBuy](high)+lowest[26*ICBuy](low))/2

BSpanB = (highest[52*ICBuy](high[26*ICBuy])+lowest[52*ICBuy](low[26*ICBuy]))/2

//=/ Ichimoku Sell

ICSell = 0.86

SSpanA = (STenkan[26*ICSell]+SKijun[26*ICSell])/2

STenkan = (highest[9*ICSell](high)+lowest[9*ICSell](low))/2

SKijun = (highest[26*ICSell](high)+lowest[26*ICSell](low))/2

SSpanB = (highest[52*ICSell](high[26*ICSell])+lowest[52*ICSell](low[26*ICSell]))/2

//

//=/===============/=//=/===============/=//=/ Buy Settings

//

//=/ Conditions Buy

CB1 = momentum[9] > 0

CB2 = momentum[44] > 0

CB3 = momentum[187] > 0

CB4 = close > BSpanA and close > BSpanB

CB5 = BKijun > BSpanA and BKijun > BSpanB

CB6 = close > BTenkan and close > BKijun

CB7 = BTenkan > BSpanA and BTenkan > BSpanB

CB8 = close > BSpanA[26*ICBuy] and close > BSpanB[26*ICBuy]

CB9 = close > BTenkan[26*ICBuy] and close > BKijun[26*ICBuy]

ConditionsBuy = CB1 and CB2 and CB3 and CB4 and CB5 and CB6 and CB7 and CB8 and CB9

//=/ Conditions Sell

CXB1 = close < open

CXB2 = close < BSpanA and close < BSpanB

CXB3 = BKijun < BSpanA and BKijun < BSpanB

CXB4 = close < BTenkan and close < BKijun

CXB5 = BTenkan < BSpanA and BTenkan < BSpanB

CXB6 = close < BSpanA[26*ICBuy] and close < BSpanB[26*ICBuy]

CXB7 = close < BTenkan[26*ICBuy] and close < BKijun[26*ICBuy]

ConditionsSell = CXB1 and CXB2 and CXB3 and CXB4 and CXB5 and CXB6 and CXB7

//=/ Confirmation Time Buy

if ConditionsBuy then

CB = 1

elsif ConditionsSell then

CB = -1

else

CB = 0

endif

CTB1 = CB[1] = 1

CTB2 = CB[2] = 1

CTB3 = CB[3] = 1

CTB4 = CB[4] = 1

CTB5 = CB[5] = 1

CTB6 = CB[6] = 1

CTB7 = (close-open) > (high-close)

CTB = CTB1 and CTB2 and CTB3 and CTB4 and CTB5 and CTB6 and CTB7

if CTB then

ConfirmationTimeBuy = 1

else

ConfirmationTimeBuy = 0

endif

//=/ Buy

if NoTrade = 0 and BuyActivation = 1 and TTime and ConditionsBuy and ConfirmationTimeBuy = 1 then

Buy Lotss Contract at Market

Set Stop %Loss 2.27

endif

//=/ Sell

if NoTrade = 1 or close < BKijun and close > PositionPrice or ConditionsSell then

Sell at Market

endif

//

//=/===============/=//=/===============/=//=/ Sell Settings

//

//=/ Conditions Sell Short

CS1 = close < open

CS2 = momentum[18] < 0

CS3 = momentum[167] < 0

CS4 = momentum[224] < 0

CS5 = close < SSpanA and close < SSpanB

CS6 = SKijun < SSpanA and SKijun < SSpanB

CS7 = close < STenkan and close < SKijun

CS8 = STenkan < SSpanA and STenkan < SSpanB

CS9 = close < SSpanA[26*ICSell] and close < SSpanB[26*ICSell]

CS10 = close < STenkan[26*ICSell] and close < SKijun[26*ICSell]

ConditionsSellShort = CS1 and CS2 and CS3 and CS4 and CS5 and CS6 and CS7 and CS8 and CS9 and CS10

CXS1 = close > open

CXS2 = close > SSpanA and close > SSpanB

CXS3 = SKijun > SSpanA and SKijun > SSpanB

CXS4 = close > STenkan and close > SKijun

CXS5 = STenkan > SSpanA and STenkan > SSpanB

CXS6 = close > SSpanA[26*ICSell] and close > SSpanB[26*ICSell]

CXS7 = close > STenkan[26*ICSell] and close > SKijun[26*ICSell]

ConditionsExitShort = CXS1 and CXS2 and CXS3 and CXS4 and CXS5 and CXS6 and CXS7

//=/ Confirmation Time Sell

if ConditionsSellShort then

CS = 1

elsif ConditionsExitShort then

CS = -1

else

CS = 0

endif

CTS1 = CS[1] = 1

CTS2 = CS[2] = 1

CTS3 = (open-close) > (close-low)

CTS = CTS1 and CTS2 and CTS3

if CTS then

ConfirmationTimeSell = 1

else

ConfirmationTimeSell = 0

endif

//=/ Sell Short

if NoTrade = 0 and SellActivation = 1 and TTime and ConditionsSellShort and ConfirmationTimeSell = 1 then

SellShort Lotss Contract at Market

Set Stop %Loss 1.09

endif

//=/ Exit Short

if NoTrade = 1 or close > SKijun and close < PositionPrice or ConditionsExitShort then

ExitShort at Market

endif

//

//=/===============/=//=/===============/=//=/ End

//

//

//=/===============/=//=/ IV mcm

//

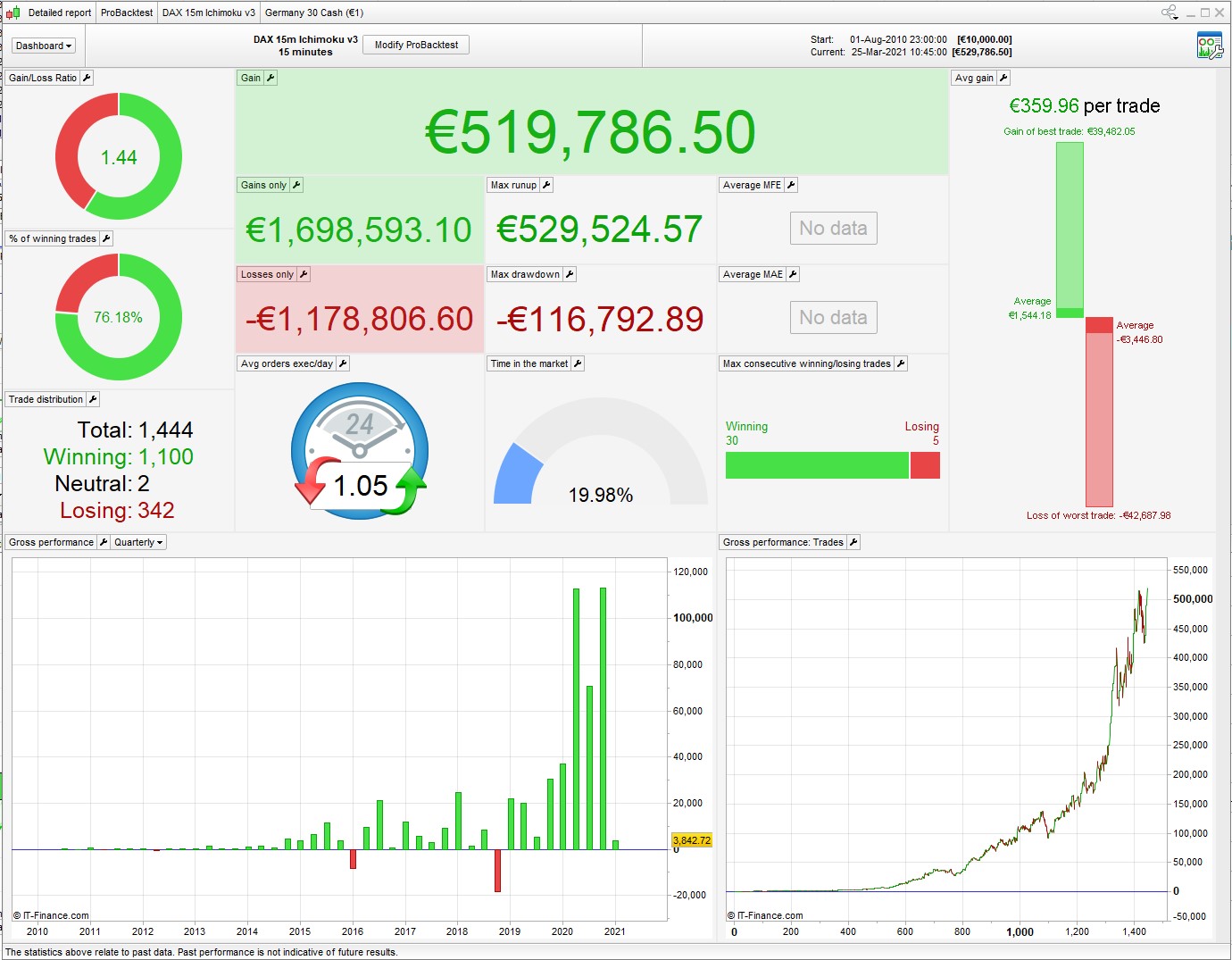

thanks for that, looks interesting – can you post the results with all money management turned off to get a better idea of the level performance?

Thanks a lot for this new idea, I moved your post into the forum to discuss about, because it would attract a lot of questions in the library because of its optimization settings. Did you made some OOS testing?

Hello Nicolas

No indeed, the OOS tests were not performed for the simple reason that I don’t know how to do it, could you tell me how to proceed?

Thank you

Hello nonetheless

The strategy is developed with system management, so for a fixed batch system, you should probably review the parameters to get more conclusive results.

Sincerely yours,

Use the walk forward tool in the platform in order to test your optimization over an out of sample period (OOS period). You should always divide your backtest history when optimizing, into 2 parts, the first one to optimize the value (In-Sample period = IS) and the second one to test those variables values into “real” market conditions, the OOS period. There are so many topics discussing strategy robustness over the forums, you should dig into them 🙂

Hello IV Mcm,

did you test your strategu with Walkforward ?

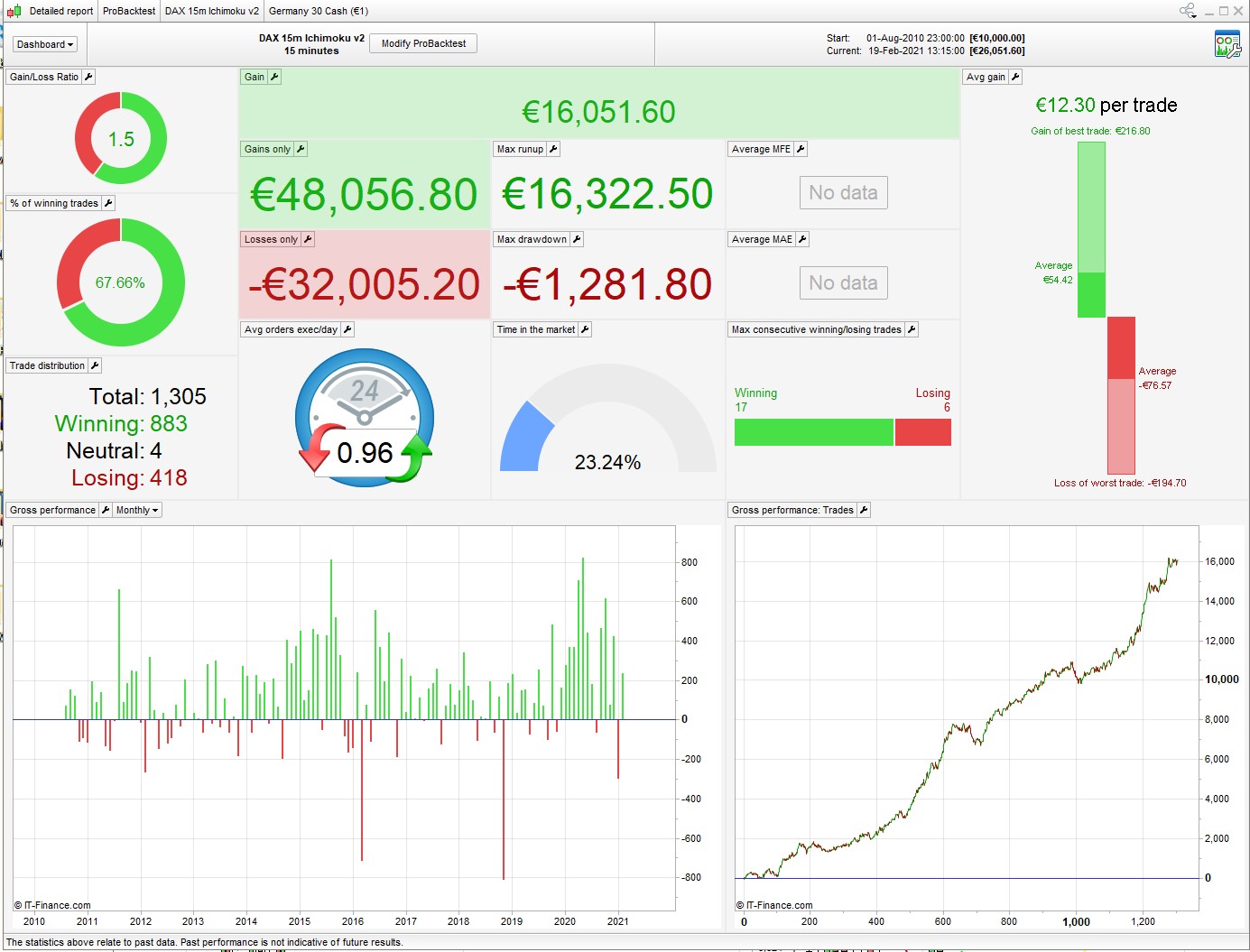

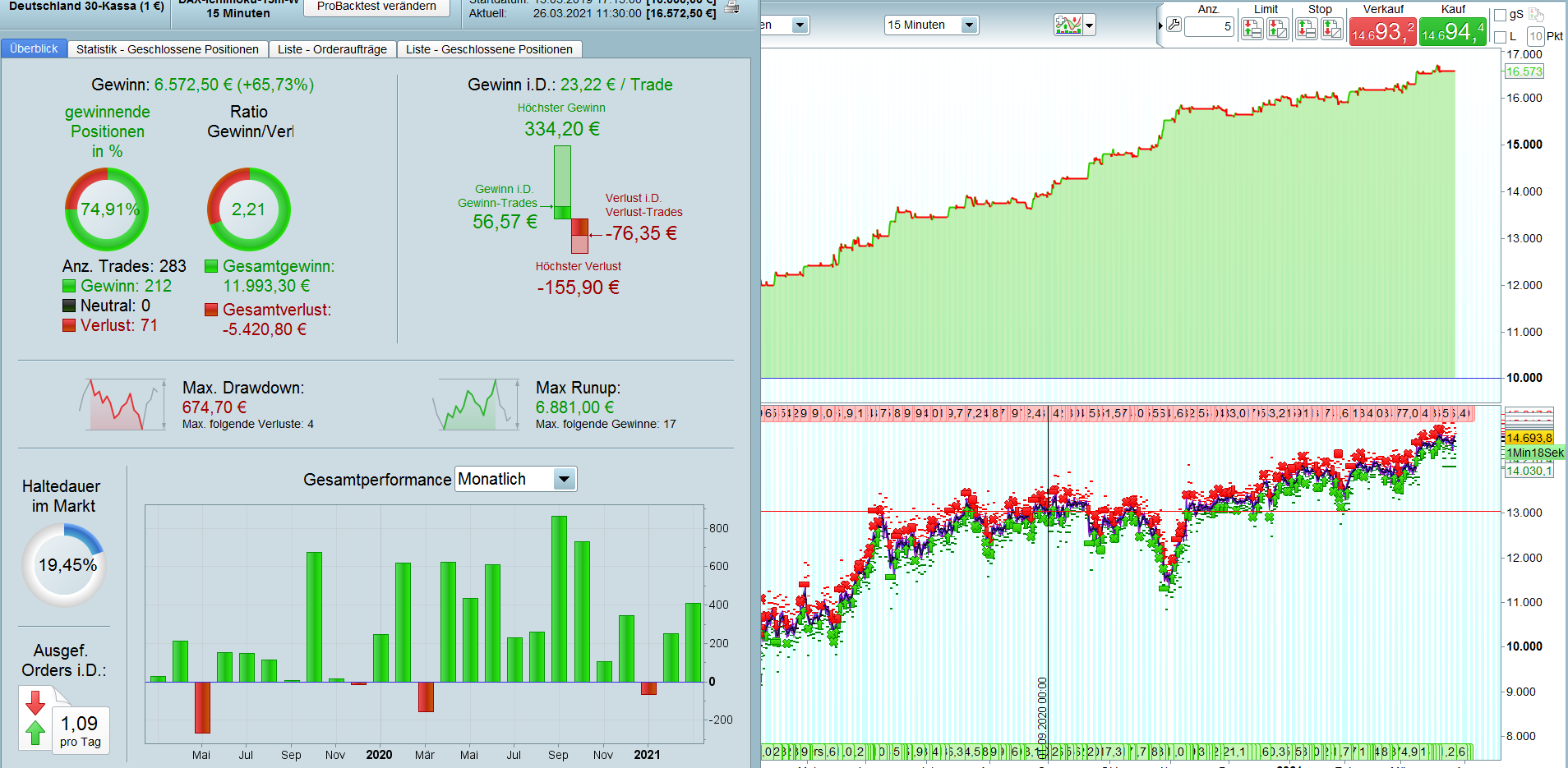

Here’s a version of this with no MM, optimized 70/30

Not too bad (apart from 2 awful months) … but unfortunately I’m getting the dreaded Negative/Zero Parameter error in demo.

Most grateful to anyone with any thoughts on this.

DefParam CumulateOrders = False

//

//=/===============/=//=/===============/=//=/ Activation Settings

//

BuyActivation = 1

SellActivation = 1

//

//=/===============/=//=/===============/=//=/ Time Settings

//

Before = Time >= 080000

After = Time < 213000

TTime = Before and After

//

//=/===============/=//=/===============/=//=/ Indicator Settings

//=/ Ichimoku Buy

ICBuy = 1.15

BSpanA = (BTenkan[26*ICBuy]+BKijun[26*ICBuy])/2

BTenkan = (highest[9*ICBuy](high)+lowest[9*ICBuy](low))/2

BKijun = (highest[26*ICBuy](high)+lowest[26*ICBuy](low))/2

BSpanB = (highest[52*ICBuy](high[26*ICBuy])+lowest[52*ICBuy](low[26*ICBuy]))/2

//=/ Ichimoku Sell

ICSell = 0.9

SSpanA = (STenkan[26*ICSell]+SKijun[26*ICSell])/2

STenkan = (highest[9*ICSell](high)+lowest[9*ICSell](low))/2

SKijun = (highest[26*ICSell](high)+lowest[26*ICSell](low))/2

SSpanB = (highest[52*ICSell](high[26*ICSell])+lowest[52*ICSell](low[26*ICSell]))/2

MA = average[36,5](typicalprice)

MAS = average[53,4](typicalprice)

//=/===============/=//=/===============/=//=/ Buy Settings

//

//=/ Conditions Buy

CB1 = momentum[9] > 0

CB2 = momentum[45] > 0

CB3 = momentum[160] > 0

CB4 = close > BSpanA and close > BSpanB

CB5 = BKijun > BSpanA and BKijun > BSpanB

CB6 = close > BTenkan and close > BKijun

CB7 = BTenkan > BSpanA and BTenkan > BSpanB

CB8 = close > BSpanA[26*ICBuy] and close > BSpanB[26*ICBuy]

CB9 = close > BTenkan[26*ICBuy] and close > BKijun[26*ICBuy]

CB10 = ma > ma[1]

ConditionsBuy = CB1 and CB2 and CB3 and CB4 and CB5 and CB6 and CB7 and CB8 and CB9 and CB10

//=/ Conditions Sell

CXB1 = close < open

CXB2 = close < BSpanA and close < BSpanB

CXB3 = BKijun < BSpanA and BKijun < BSpanB

CXB4 = close < BTenkan and close < BKijun

CXB5 = BTenkan < BSpanA and BTenkan < BSpanB

CXB6 = close < BSpanA[26*ICBuy] and close < BSpanB[26*ICBuy]

CXB7 = close < BTenkan[26*ICBuy] and close < BKijun[26*ICBuy]

ConditionsSell = CXB1 and CXB2 and CXB3 and CXB4 and CXB5 and CXB6 and CXB7

//=/ Confirmation Time Buy

if ConditionsBuy then

CB = 1

elsif ConditionsSell then

CB = -1

else

CB = 0

endif

CTB1 = CB[1] = 1

CTB2 = CB[2] = 1

CTB3 = CB[3] = 1

CTB4 = CB[4] = 1

CTB5 = CB[5] = 1

CTB6 = CB[6] = 1

CTB7 = (close-open) > (high-close)

CTB = CTB1 and CTB2 and CTB3 and CTB4 and CTB5 and CTB6 and CTB7

if CTB then

ConfirmationTimeBuy = 1

else

ConfirmationTimeBuy = 0

endif

//=/ Buy

if BuyActivation = 1 and TTime and ConditionsBuy and ConfirmationTimeBuy = 1 then

Buy 1 Contract at Market

Set Stop %Loss 1.4

SET TARGET %PROFIT 1.5

endif

//=/ Sell

if close < BKijun and close > PositionPrice or ConditionsSell then

Sell at Market

endif

//

//=/===============/=//=/===============/=//=/ Sell Settings

//

//=/ Conditions Sell Short

CS1 = close < open

CS2 = momentum[22] < 0

CS3 = momentum[170] < 0

CS4 = momentum[230] < 0

CS5 = close < SSpanA and close < SSpanB

CS6 = SKijun < SSpanA and SKijun < SSpanB

CS7 = close < STenkan and close < SKijun

CS8 = STenkan < SSpanA and STenkan < SSpanB

CS9 = close < SSpanA[26*ICSell] and close < SSpanB[26*ICSell]

CS10 = close < STenkan[26*ICSell] and close < SKijun[26*ICSell]

CS11 = mas < mas[1]

ConditionsSellShort = CS1 and CS2 and CS3 and CS4 and CS5 and CS6 and CS7 and CS8 and CS9 and CS10 and CS11

CXS1 = close > open

CXS2 = close > SSpanA and close > SSpanB

CXS3 = SKijun > SSpanA and SKijun > SSpanB

CXS4 = close > STenkan and close > SKijun

CXS5 = STenkan > SSpanA and STenkan > SSpanB

CXS6 = close > SSpanA[26*ICSell] and close > SSpanB[26*ICSell]

CXS7 = close > STenkan[26*ICSell] and close > SKijun[26*ICSell]

ConditionsExitShort = CXS1 and CXS2 and CXS3 and CXS4 and CXS5 and CXS6 and CXS7

//=/ Confirmation Time Sell

if ConditionsSellShort then

CS = 1

elsif ConditionsExitShort then

CS = -1

else

CS = 0

endif

CTS1 = CS[1] = 1

CTS2 = CS[2] = 1

CTS3 = (open-close) > (close-low)

CTS = CTS1 and CTS2 and CTS3

if CTS then

ConfirmationTimeSell = 1

else

ConfirmationTimeSell = 0

endif

//=/ Sell Short

if SellActivation = 1 and TTime and ConditionsSellShort and ConfirmationTimeSell = 1 then

SellShort 1 Contract at Market

Set Stop %Loss 1.1

SET TARGET %PROFIT 1.6

endif

//=/ Exit Short

if close > SKijun and close < PositionPrice or ConditionsExitShort then

ExitShort at Market

endif

//MFE exit

ONCE MFEx = 0

if mfex then

MFE = summation[barindex-tradeindex](positionperf > 0)

IF longonmarket and barindex-tradeindex > 9 and (MFE = 0) then

sell at market

endif

endif

Not sure what you mean. The optimization is 70/30, so almost 3 years OOS.

But the Negative/Zero Parameter is the bigger problem as it won’t run as it is.

You will notice that the version without MM loses a lot in gain.

The MM allows you to adapt to the volatility to avoid ruining yourself during a crack or gaining nothing during low volatility.

I am all in favour of MM, but for backtest and optimization it’s better to run with level stakes so you know what you’re dealing with. Also easier to compare performance with other algos. MM is added after.

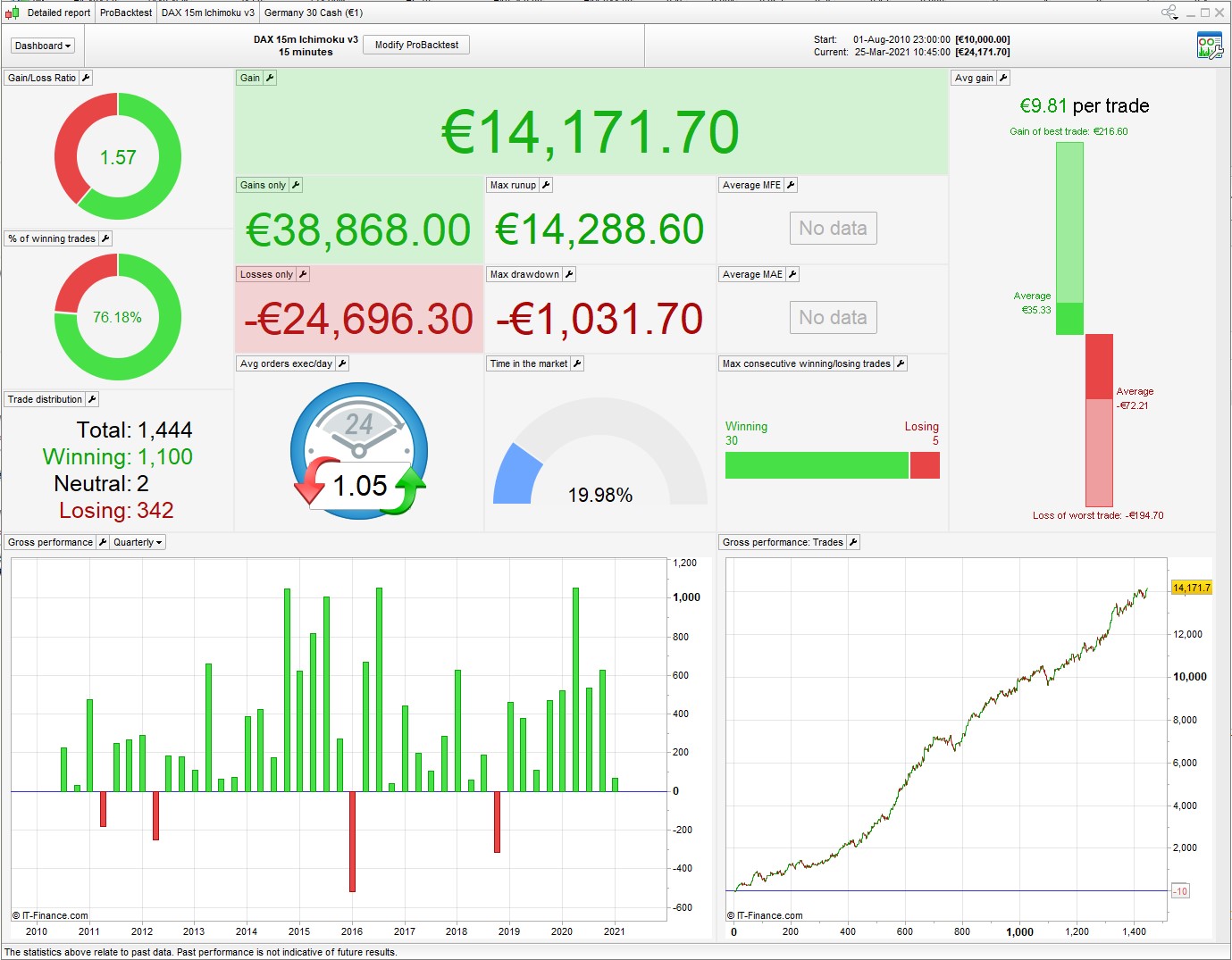

Here’s another version, lower profit but more trades and better %win. Also fixes the zero parameter problem.

2nd image is with my MM code.

Nice algo. I changed some variables. Backtested it since 13.03.2019

Hi, would you like to post your set of variables / algo including it ?

Hi, would you like to post your set of variables / algo including it ?

If yr post was adressed to me, pls find attached the itf file.