Sorry to be posting this here but cannot access the community forum.

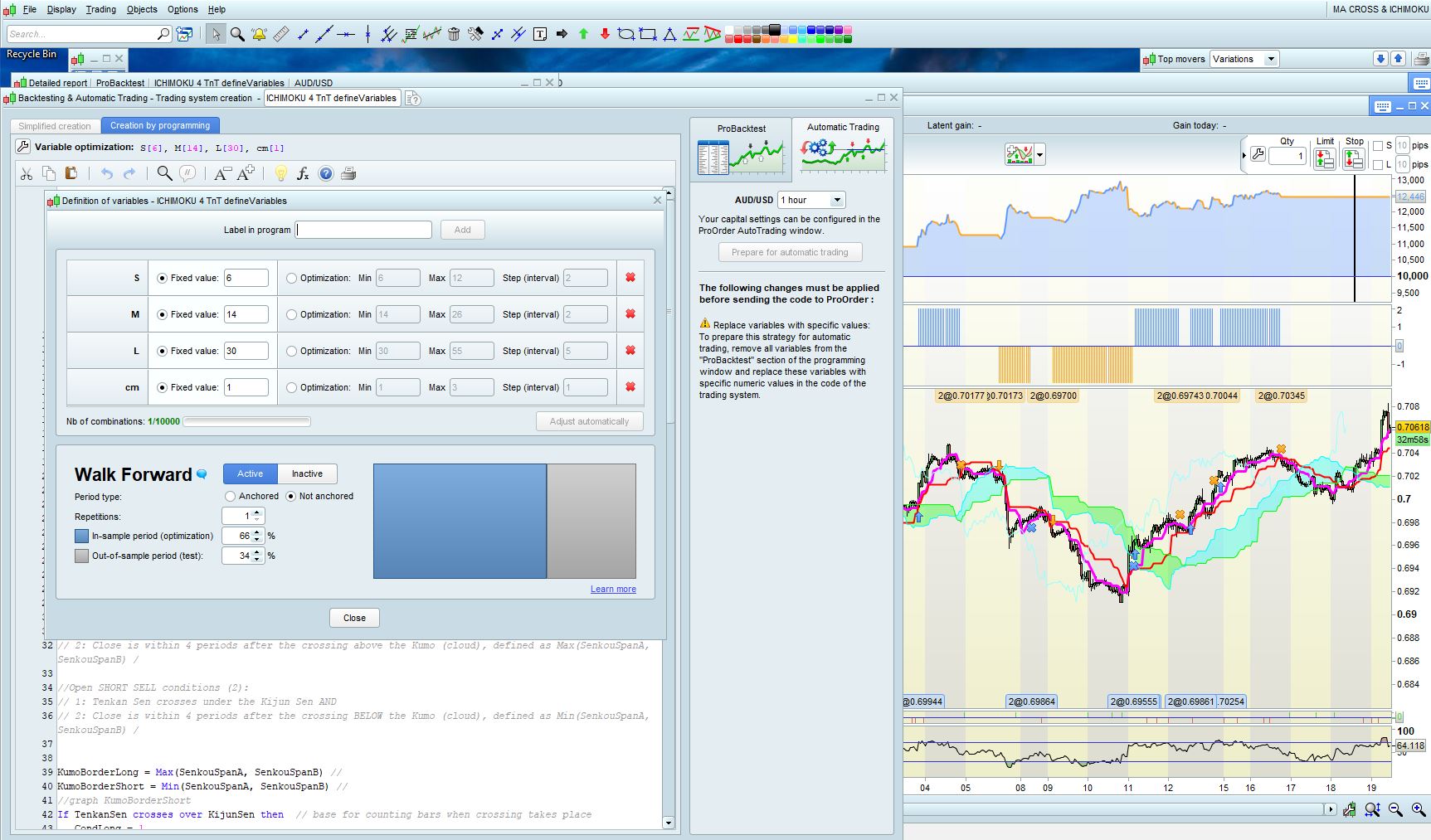

When preparing for trading the issue with defined variables stops me from trading. The variables are defined as you can see from the attachment.

The following, is the code I want to use. Could someone please help me to sort out the undefined variable conflict? It would help if proRealTime highlighted the error in the code. I have defined all the variables within any [ ] brackets.

/LINK https://www.prorealcode.com/prorealtime-trading-strategies/ichimoku-exits-cloud/

//Source idea: https://www.whselfinvest.nl/nl-nl/trading-platform/gratis-trading-strategie/tradingsysteem/17-ichimoku-tkc

Defparam CumulateOrders = false // Cumulating positions deactivated

//Defparam flatafter = 164500

//once StartE = 080000 //start time for opening positions

//once StartL = 160000 //ending time for opening positions (only trading in the morning)

once N = 2 // intitial number of contracts

OTD = Barindex - TradeIndex(5) > IntradayBarIndex // limits the (opening) trades till 1 per day

once Spread = 6 //total spread buy and sell, the actual price is always in between !

once SL = round(close * 100/10000) //Setting Stop loss //Dynamic for indices

// Ichimoku settings

TenkanSen = (highest[S](high)+lowest[S](low))/2 // default setting S = 9

KijunSen = (highest[M](high)+lowest[M](low))/2 // default setting M = 26

SenkouSpanA = (Tenkansen[M]+Kijunsen[M])/2 // default setting M = 26

SenkouSpanB = (highest[L](High[M])+lowest[L](Low[M]))/2 //default setting L = 52

// Closing methodes (described for long positions, for short positions exactly the opposite

//Method 1 if TenkanSen crosses under the Kijunsen

//Method 2 if close closes under the upper side of the Kumo / Cloud, based upon the SenkouSpanA

//Method 3 if close closes under the lower side of the Kumo / Cloud, based upon the SenkouSpanB

ClosingMethod = cm //default is cm = 1

//Open LONG BUY conditions (2):

// 1: Tenkan Sen crosses over the Kijun Sen AND

// 2: Close is within 4 periods after the crossing above the Kumo (cloud), defined as Max(SenkouSpanA, SenkouSpanB) /

//Open SHORT SELL conditions (2):

// 1: Tenkan Sen crosses under the Kijun Sen AND

// 2: Close is within 4 periods after the crossing BELOW the Kumo (cloud), defined as Min(SenkouSpanA, SenkouSpanB) /

KumoBorderLong = Max(SenkouSpanA, SenkouSpanB) //

KumoBorderShort = Min(SenkouSpanA, SenkouSpanB) //

//graph KumoBorderShort

If TenkanSen crosses over KijunSen then // base for counting bars when crossing takes place

CondLong = 1

else

CondLong = 0

endif

If TenkanSen crosses under KijunSen then

CondShort = 1

else

CondShort = 0

endif

//graph cond1L

if OTD and not onmarket then

IF summation[4](CondLong) = 1 and summation[4](CondShort) = 0 and Close > KumoBorderLong then //

BUY N shares AT MARKET

SET STOP ploss SL

endif

IF summation[4](CondLong) = 0 and summation[4](CondShort) = 1 and Close < KumoBorderShort THEN //

SELLSHORT N shares AT MARKET //short sell conditie

SET STOP pLOSS SL

endif

endif // end purchase conditions

if not onmarket then

PriceExit = 0

endif

if longonmarket then // 3 Exit strategies

if ClosingMethod = 1 then

If TenkanSen crosses under KijunSen then

sell at market

endif

endif

if ClosingMethod = 2 then

if close - Spread * 0.5 < KumoBorderShort then //to secure a possible stop for Sell at market

PriceExit = close - Spread * 0.5

else

PriceExit = KumoBorderShort // regular STOP for sell at market, set for each trading bar

endif

endif

if ClosingMethod = 3 then

if close - Spread * 0.5 < KumoBorderLong then //to secure a possible stop for Sell at market

PriceExit = close - Spread * 0.5

else

PriceExit = KumoBorderShort // regular STOP for sell at market, set for each trading bar

endif

endif

endif

if shortonmarket then //// 3 Exit strategies

if ClosingMethod = 1 then

If TenkanSen crosses over KijunSen then

exitshort at market

endif

endif

if ClosingMethod = 2 then

if close + Spread * 0.5 > KumoBorderLong then //to secure a possible stop for Sell at market

PriceExit = close + Spread * 0.5

else

PriceExit = KumoBorderLong // regular STOP for EXIT SHORT at market, set for each trading bar

endif

endif

if ClosingMethod = 3 then

if close + Spread * 0.5 > KumoBorderShort then //to secure a possible stop for Sell at market

PriceExit = close + Spread * 0.5

else

PriceExit = KumoBorderShort // regular STOP for EXIT SHORT at market, set for each trading bar

endif

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then //price exit set for each trading bar

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//graph priceexit

Undefined variables means that they are not present in the code (or commented with either a double slash // or with REM instruction). So remove the double slash and REM from the code in order to get the variables to be defined.

Another way is to download the file in the library and import it into the platform instead of copy/pasting it.