(apologies for the typo in the title of the topic)

Hi Kumo,

Maybe there is a misunderstanding, or possibly is the instrument I used there misleading;

First off, I can’t translate your USD 3000 of required margin into an amount to invest, but if I had to guess it would be 33 x 3000 = EUR 100K (margin 3%). If that is correct, then that would imply Commission on EUR/USD of USD 8 In + Out (thus total 8). I now used the commission for someone not very regularly trading (hence no discount).

This is not what my situation showed. That showed Spot Silver, which bears a relatively (very) high commission for IB. Still it can be scalped nicely – also see below for today’s further progress.

The picture below nicely bridges to your second subject : No SL ?

This system uses a SL all right, though technically it is not visible. If that is what you referred to, then indeed; It creates an Exit when the direction remains against it for too long. Hut maybe you referred merely to this :

What coincicentally happened to this for me new System, is that it almost immediately started out with a loss. And believe it or not, but such a loss is calculated-in; It has been backtested without optimisation, unless it would be about the balance between the number of losses over the backtested period and the gains to counteract those. Of course this all includes the not being afraid of a Loss falling right at the start of the System, which you see applied here for real. And obviously don’t attempt this with a 3% margin and 3000 portfolio with 100K investment. Then you’re Out (in this case the 3000 would really have gone, looking at the 3200 loss I showed in the first post. –maybe you referred to something quite different, then just skip–

To summarise the above : you should of course never allow trades which will not allow the strategy with deep SL to survive (read : your portfolio should survive).

Eureka ?

Maybe not;

One could attest that no SL at all (also not hidden) would always survive best because you will never lose a trade. But this would be very bad for revenue because all the time in DD will not bring new trades and thus also no money. This in itself first requires that your strategy does better than Buy & Hold, hence that it is able to extra-gain on the way back (this one is Long + Short so this part of the story is a bit mute for this instrument but with the notice that Long + Short is only more difficult when using deep SL’s (because you don’t expect a direction in advance)). Otoh, Long + Short already takes advantage inherently from “a way back”, so that part should be more easy (if you get your Entries right).

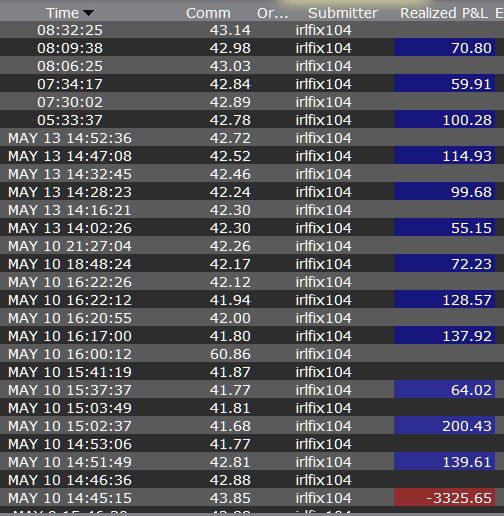

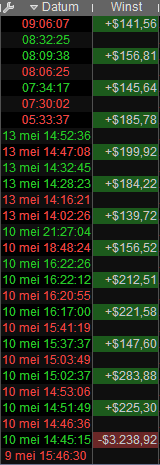

To visualise the “not being unable to trade for too long”, look below where I also showed the duration of that loser, which has been 23 hours.

All ‘n all it is one large forcefield of reasoning and how a strategy will be fine with a deeper SL, if only the profit is more than sufficient to overcome it when needed.

The fun could be that what we saw earlier today and what looked like a failed strategy (at least for these couple of days it is running), now suddenly looks like a winner. Why ? it was given the time (the air) to survive; it obviously was given the portfolio money to survive. Thus I don’t mean “sufficient investment” but just the headroom in the portfolio to allow for this. And this also with the knowledge in that other topic (GraHal’s vanished (demo) portfolio in the first 3 weeks of April), where ALL the instruments/strategies could work out similarly : in DD. And deep.

The beauty of what you see below is that this one loss has already almost been covered for, and it happened today (but not really, see at the PS for explanation). Yes, right; one day. This can only happen because of the deeper DD but unconditionally with the knowledge in advance that the strategy will be a net winning one. Of course that is the hard part, but one has to work for his/her money, right ?

Don’t look at the figures which here coincidentally show; don’t be depressed when you recognize that you can’t make these trades with a portfolio means of 3000. Just divide all by 10, have that same 3000 in the portfolio and thus risk 300 only. Lose a first trade – no harm done. In one day you won’t earn (back) $2731 like you see here, but 273,30. That won’t be bad at all IMO. Notice, however, that my backtesting of this system, with the investment 10 times lower, shows a gain of 1200 per month. So of course it won’t gain 273,30 per day – it is only 1200 / 20 = 60. It may lose 320 once in a while, but that is included.

PS: On-Topic : We did not forget that this 2731 now shown is without deducted commission, right ? haha. So nothing was earned back in almost one day. It takes another day (or more); on estimate it is now at ~ break even. PRT’s glass is half full – always good to be positive ? No I think not. That is dangerous.