Hello, please can someone help I’m about to go live full time with my first automated trading system but have the following questions?

1)When backtesting do we receive different results if carried out over the weekend? The gain on my 1 minute dji strategy when backtested over 100,000 units has dropped by aprrox £1400 since yesterday which isn’t a result of Friday losses or me altering the base code?

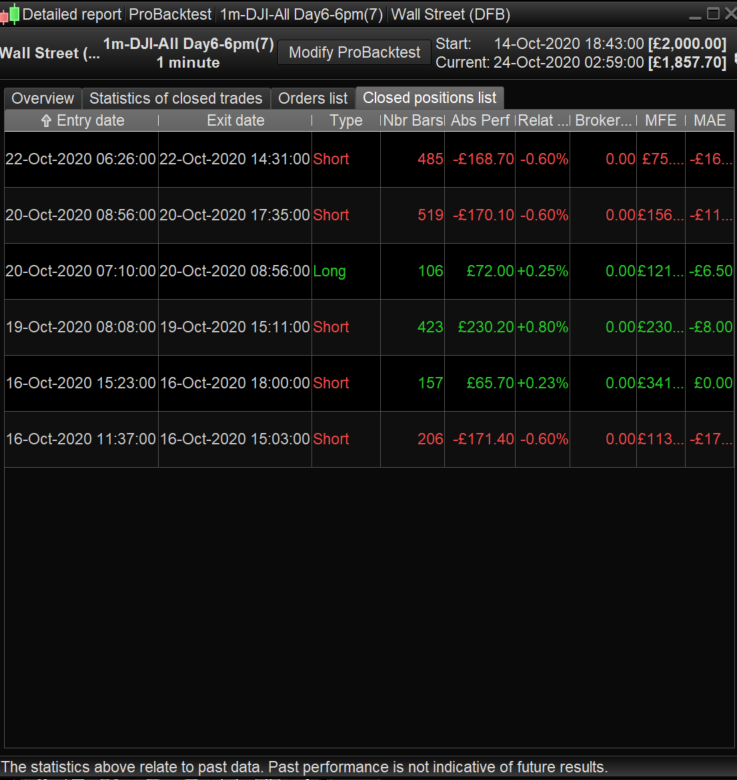

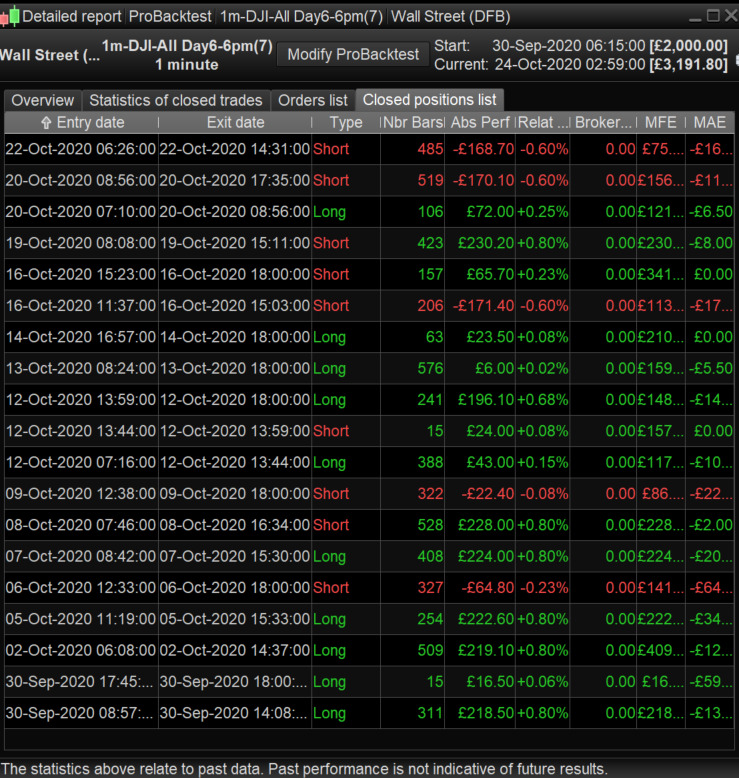

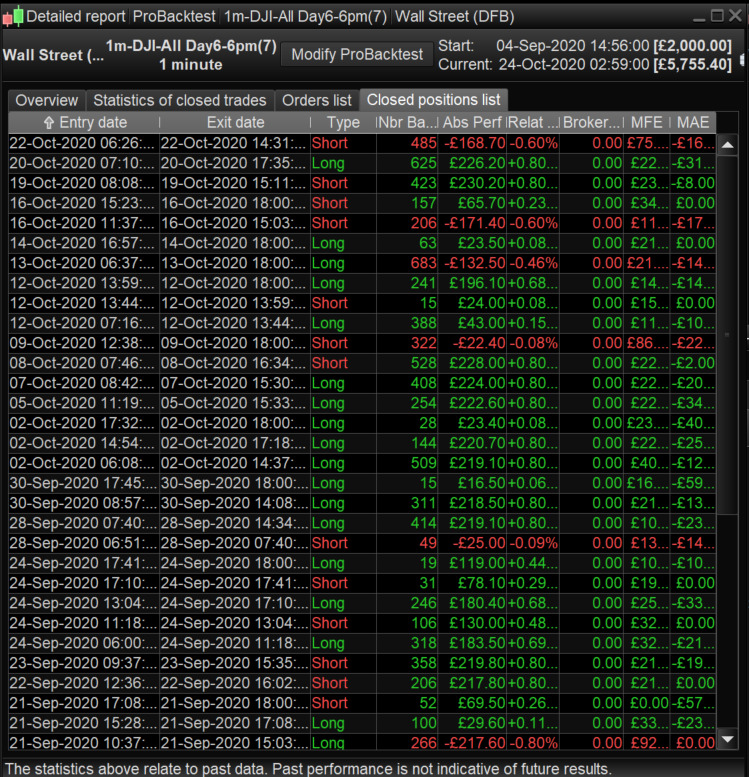

2)I’m getting different win/losses when backtesting the different quantities of units 50,000, 25,000 and 10,000. In the attached screenshots the

20th October turns from a single win on 50,000 units to a loss and a win on 25,000 and 10,000

2nd October on 50,000 units 3 wins turns into a single win on a 25,000 unit backtest?

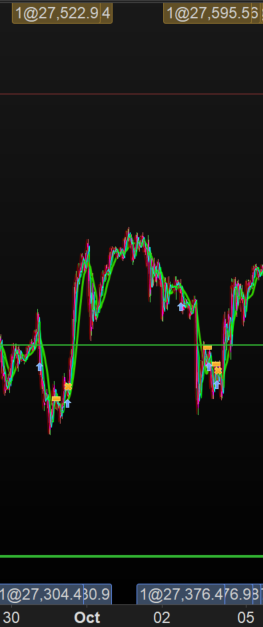

3)In the graph screenshot I have two backtest trades showing long wins on graph but clearly showing as exiting below their entrance ?

Would it be possible for one of the live automated traders to give a rough estimate of what to expect for probacktest/proorder peculiarities together with the expected slippage based on their own experiences so I can factor it in to my expectations? For example shave 20% of any backtest gain figures, would get you in the ball park for a live trading figure.

Apologies for the longwinded post and thanks in advance for any help and advice.

This happened to me too. Had the same code the backtest results suddenly changed yesterday. Checked today its back to normal. Maybe a software update error?

I have suspected it happening in the past, but I put it down to my imagination as I never had the weekday results and the weekend results to compare one with the other.

Is it possible that as the start date changed (weekend is a few days later than a day in the week) that a profitable trade is missed off the weekend results?

about to go live full time

We need to test any Algo in Demo Live (first) until we get a minimum of 50 to 100 trades and then we can judge if we can live with drawdown values / stress etc.

Hi Monochrome and GraHal thanks for getting back to me.

It doesn’t seem to have been missed off the current weekend although the strategy is a 6am to 6pm one with no weekend trading but I suppose there is a chance that winning trades may have been dropped off at the beginning of the unit period calculation although with my tp and sl set I can’t see how it could drop £1400 in a single day.

Racking my brains about the different results with different units backtesting the only thing I could think of is maybe with 10,000 units as some of my indicators reference [14] days and 10000 units is under 14 days it’s maybe giving different results but I can’t hazard a guess as why that might be reporting difference results for older backtest trades captured within the 50,000 units and 25,000 units.

Do we know anything about how the backtest chart pricing is updated is it a database of fixed figures with only the current live weeks figures updating as I would have thought the only variable should be live prices ?

maybe giving different results

10,000 bars dos not always cover the same period even 10 minutes later!

- Select 10000 bars of 5 min TF and note down the start date and time.

2. Then select 10000 bars of 1 hour TF.

3. Then – without closing the Chart – select 10000 bars of 5 mins TF and note down the start date and time.

4. Compare 1. with 3. … are they the same start date and time?

5. Let us know the findings?

Hi GraHal,

I’m not sure what that will achieve, my strategy is optimised for a 1 minute time frame, am I right in understanding that 10,000 units would be 10,000 1 minute candles and this is an ever evolving figure as time unfortunately is forever moving forward?

10,000 5 minute or 10,000 1hr candles would understandably reach back further ?

I’m not sure what that will achieve

I just did my experiment and the difference is not as marked (a few hours only) as I have noted previously.

If / when I note wide difference (as I have noted previously) I will post on here.

Thanks Grahal,

My greatest concern is how backtest trades can give two different resulting wins or losses on the same day depending on the quantity of units selected for back test as shown in the backtest screenshots?

May just be the case that it’s time to throw some money at it and see what happens in Demo Live. I’ll drop the positionsize right down and see how it does thanks again.

@Kovit

1)When backtesting do we receive different results if carried out over the weekend?

with 100K bars you always change the starting and ending time and bars, since every new bar may open new trades and you will lose any trade opened in the 100Kth bar. Backtest will be different the smaller the TF and the more trades are opened and whether you close them on Friday night or let them run over the weekend thus affected by gaps at the beginning of any new week.

2)I’m getting different win/losses when backtesting the different quantities of units 50,000, 25,000 and 10,000. In the attached screenshots the

20th October turns from a single win on 50,000 units to a loss and a win on 25,000 and 10,000

2nd October on 50,000 units 3 wins turns into a single win on a 25,000 unit backtest?

That happens often, a shorter range may help you select a good period, while a greater range implies operating in both good and bad periods.

3)In the graph screenshot I have two backtest trades showing long wins on graph but clearly showing as exiting below their entrance ?

I’ll need to check on my PC, with dates and times.

Slippage cannot be known, as well as any prediction. Every day and every bar is different from the past ones.

Looks like Frankyboy is having the problem I highlighted above.

Maybe the same root cause is responsible for your Issue?

my data for backtest is capped, why?

see what happens in Demo Live

I get fed up messing about with the same Algo after a while and I do above … suck it and see ... costs nothing to try on Demo and may even work better than backtest! 🙂

Thanks Roberto and Grahal for your replies and feedback. For some reason I had it in my head that I couldn’t run prorealtime autotrading on a demo live account with IG but will look into it now as that would be the perfect intermediate step if possible.

Yep live demo account up and running now, so will get my stuff loaded up on there, will definitely save me some stress before going live live. 🙂