Hi friends,

I’m working in an automated strategy but I’m having problems with an issue.

I would like to make entries only under a condition. I would like to open shorts when last RSI min. value was between two values, and open longs when last RSI max was between another two values.

I’ve got it defining a N bars number, but I don’t want to use the bars number. I think it may be solved using ONCE or WHILE instructions but I can’t find the way.

My code now is as following:

Open longs:

c7 = ((lowest[20](RSI)) < 20) and ((highest[RSINUMBARS](RSI)) < 80)

Open shorts:

c17 = ((highest[20](RSI)) > 80) and ((lowest[RSINUMBARS](RSI)) > 20)

But I would like to obviate the [20] bars value using something similar to

while ((highest[20](RSI)) > 80) and ((lowest[RSINUMBARS](RSI)) > 20) do ...

I tried wih ONCE too but didn’t work.

Could you guide me to find a solution?

Thanks to all the community.

If you post your full code then I / we could easily run it on our Platforms and it then easier to offer help rather than us having to make above into a working System to check it out.

If you not want to share your full code then I guess some expert coder may spot an anomaly and / or offer suggestions?

I’m not sure I fully understand your problem.

First of all you need to give your RSI’s a period. For example:

RSI[14]

Why not use a simple IF THEN ENDIF?

if ((highest[20](RSI[14])) > 80) and ((lowest[RSINUMBARS](RSI[14])) > 20) then

(whatever you want to do)

endif

The code is read through once at the close of a candle and if your condition of looking back for the lowest RSI and highest RSI over your look back periods is met then whatever you want to do is carried out.

The ONCE instruction means that whatever is written after it is only read at the close of the very first candle and ignored every candle after that.

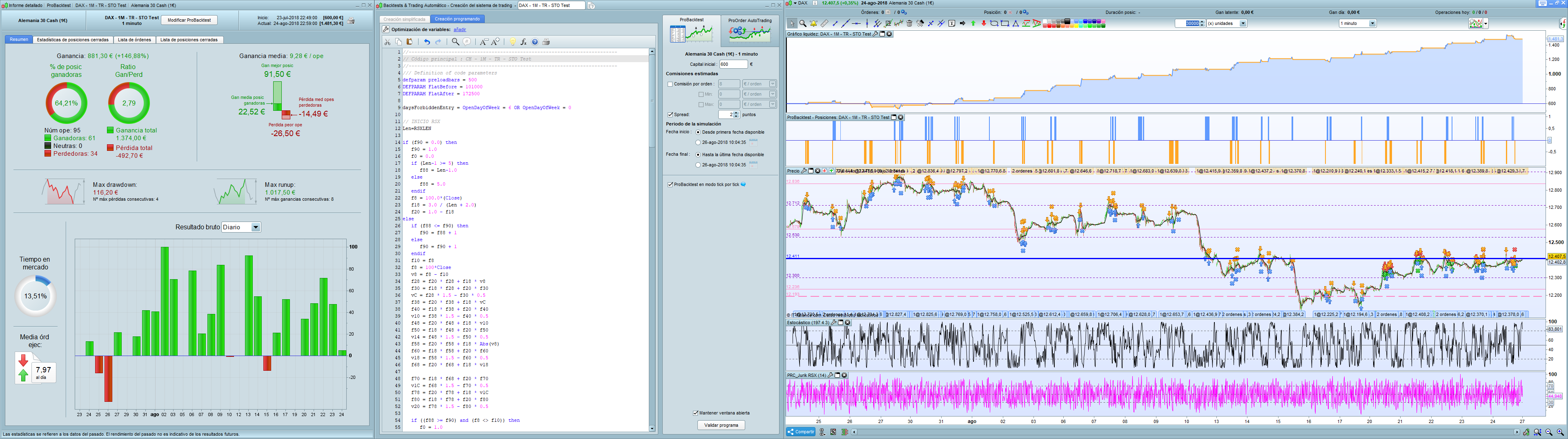

Hi GraHal of course. Also I’ve been all night working on it and I changed a few things to enhance it.

Basically I change RSI by RSX and results are much better now. However code is a bit frankenstein…don’t laugh please 🙂

It’s for DAX M1 and my main question is how to avoid RSXBARS for no limiting trades at that certain vars number. I spent much hours testing with WHILE and ONCE but I can’t solve it.

Also, any other idea to enchance strategy is welcome 🙂

//-------------------------------------------------------------------------

// Código principal : CH - 1M - TR - STO

//-------------------------------------------------------------------------

/// Definition of code parameters

defparam preloadbars = 500

DEFPARAM FlatBefore = 101000

DEFPARAM FlatAfter = 172500

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// INICIO RSX

Len=RSXLEN

if (f90 = 0.0) then

f90 = 1.0

f0 = 0.0

if (Len-1 >= 5) then

f88 = Len-1.0

else

f88 = 5.0

endif

f8 = 100.0*(Close)

f18 = 3.0 / (Len + 2.0)

f20 = 1.0 - f18

else

if (f88 <= f90) then

f90 = f88 + 1

else

f90 = f90 + 1

endif

f10 = f8

f8 = 100*Close

v8 = f8 - f10

f28 = f20 * f28 + f18 * v8

f30 = f18 * f28 + f20 * f30

vC = f28 * 1.5 - f30 * 0.5

f38 = f20 * f38 + f18 * vC

f40 = f18 * f38 + f20 * f40

v10 = f38 * 1.5 - f40 * 0.5

f48 = f20 * f48 + f18 * v10

f50 = f18 * f48 + f20 * f50

v14 = f48 * 1.5 - f50 * 0.5

f58 = f20 * f58 + f18 * Abs(v8)

f60 = f18 * f58 + f20 * f60

v18 = f58 * 1.5 - f60 * 0.5

f68 = f20 * f68 + f18 * v18

f70 = f18 * f68 + f20 * f70

v1C = f68 * 1.5 - f70 * 0.5

f78 = f20 * f78 + f18 * v1C

f80 = f18 * f78 + f20 * f80

v20 = f78 * 1.5 - f80 * 0.5

if ((f88 >= f90) and (f8 <> f10)) then

f0 = 1.0

endif

if ((f88 = f90) and (f0 = 0.0)) then

f90 = 0.0

endif

endif

if ((f88 < f90) and (v20 > 0.0000000001)) then

v4 = (v14 / v20 + 1.0) * 50.0

if (v4 > 100.0) then

v4 = 100.0

endif

if (v4 < 0.0) then

v4 = 0.0

endif

else

v4 = 50.0

endif

// FIN RSX

// General conditions

RSX=v4

RSXLEN = 14 // 34 //12

RSXVARMIN = 28 // 31 //26

RSXVARMAX = 64 //62 //66

RSXBARS = 24 //33 //24

// Conditions long

STOL = Stochastic[204,4]

STOOVERL = 25

STOUNDERL = 60

STOMANTAINL = 89

ATRPROFITL = AverageTrueRange[5] //50 //AverageTrueRange[5]

ATRPROFITMULTL = 5 //1 //4.7

ATRRISKL = AverageTrueRange[10]

ATRRISKMULTL = 3.8 //3.5

MAPROFITAVGL = 14

BBPROFITSTDAVGL = 15

//RSXL = RSX

// Conditions short

STOS = Stochastic[199,2]

STOOVERS = 70

STOUNDERS = 83

STOMANTAINS = 6

ATRPROFITS = AverageTrueRange[10]

ATRPROFITMULTS = 4.6

ATRRISKS = AverageTrueRange[4]

ATRRISKMULTS = 4.4

MAPROFITAVGS = 15

BBPROFITSTDAVGS = 18

//RSXS = RSX

once RRreached = 0

profitpipsl = ATRPROFITL*ATRPROFITMULTL // 0.1 * var:30-60 4.9

riskpipsl = ATRRISKL*ATRRISKMULTL //risk in pips

amountl = 1 //lot amount to open each trade

sdl = 0.17 //standard deviation of MA floating profit - orig: 0.25

profitpipss = ATRPROFITS*ATRPROFITMULTS // 0.1 * var:30-60 4.6

riskpipss = ATRRISKS*ATRRISKMULTS //whole account risk in percent%

amounts = 1 //lot amount to open each trade

sds = 0.17 //standard deviation of MA floating profit - orig: 0.25

// Conditions to enter long positions

c3 = (STOL > STOOVERL) // 20

c4 = (STOL < STOUNDERL) // 40

c5 = (STOL > STOL[1]) // and (STOL[1] < STOL[2])

c6 = (RSX > RSX[1]) and (RSX > RSXVARMIN)

c7 = ((lowest[RSXBARS](RSX)) < RSXVARMIN) and ((highest[RSXBARS](RSX)) < RSXVARMAX)

// Conditions to enter short positions

c13 = (STOS < STOUNDERS) // 80

c14 = (STOS > STOOVERS) // 60

c15 = (STOS < STOS[1])

c16 = (RSX < RSX[1]) and (RSX < RSXVARMAX)

c17 = ((highest[RSXBARS](RSX)) > RSXVARMAX) and ((lowest[RSXBARS](RSX)) > RSXVARMIN)

//first trade whatever condition

if NOT ONMARKET AND c3 and c4 and c5 and c6 and c7 AND NOT daysForbiddenEntry then //close>close[1]

BUY amountl LOT AT MARKET

endif

if NOT ONMARKET AND c13 and c14 and c15 and c16 and c17 AND NOT daysForbiddenEntry then //close<close[1]

SELLSHORT amounts LOT AT MARKET

endif

//money management

//liveaccountbalance = accountbalance+strategyprofit

moneyriskl = riskpipsl

if longonmarket then

onepointvaluebasketl = pointvalue*countofposition

mindistancetoclosel =(moneyriskl/onepointvaluebasketl)*pipsize

endif

moneyrisks = riskpipss

if shortonmarket then

onepointvaluebaskets = pointvalue*countofposition

mindistancetocloses =(moneyrisks/onepointvaluebaskets)*pipsize

endif

//floating profit

floatingprofitl = (((close-positionprice)*pointvalue)*countofposition)/pipsize

floatingprofits = (((close-positionprice)*pointvalue)*countofposition)/pipsize

//actual trade gains

MAfloatingprofitl = average[MAPROFITAVGL](floatingprofitl)

BBfloatingprofitl = MAfloatingprofitl - std[BBPROFITSTDAVGL](MAfloatingprofitl)*sdl

MAfloatingprofits = average[MAPROFITAVGS](floatingprofits)

BBfloatingprofits = MAfloatingprofits - std[BBPROFITSTDAVGS](MAfloatingprofits)*sds

//floating profit risk reward check

if profitpipsl>0 and floatingprofitl>profitpipsl then

RRreached=1

endif

if profitpipss>0 and floatingprofits>profitpipss then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

//if onmarket and RRreached=0 then

//SELL AT positionprice-mindistancetoclose STOP

//EXITSHORT AT positionprice-mindistancetoclose STOP

//endif

if longonmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclosel STOP

//EXITSHORT AT positionprice-mindistancetoclose STOP

endif

if shortonmarket and RRreached=0 then

//SELL AT positionprice-mindistancetoclose STOP

EXITSHORT AT positionprice-mindistancetocloses STOP

endif

//stoploss trigger when risk reward ratio has been reached

//if onmarket and RRreached=1 then

//if floatingprofit crosses under BBfloatingprofit then

//SELL AT MARKET

//EXITSHORT AT MARKET

//endif

//endif

if longonmarket and RRreached=1 and (stol < STOMANTAINL) then

if floatingprofitl crosses under BBfloatingprofitl then

SELL AT MARKET

endif

endif

if shortonmarket and RRreached=1 and (stos > STOMANTAINS) then

if floatingprofits crosses under BBfloatingprofits then

EXITSHORT AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

Thanks a lot!

Hi Vonasi, thanks a lot for your response.

The main problem is defining last condition in a certain number of bars may limit amount of trades done.

What about if RSI or RSX condition is made on last 30 bars and not 14 or 20? I don’t want to lose those trades. So I would like to save in a floating var the last point where that condition were done and open trades in base at that condition.

I’m not sure if I explain it right at all, sorry.

However code is a bit frankenstein…don’t laugh please

I’m not laughing at the code, but I am at the joke! Very good!! I’ll have to remember that one! 🙂

But I have to say I am a bit scared by the monster!

Also you must look and feel like a monster if you have been up all night coding!?

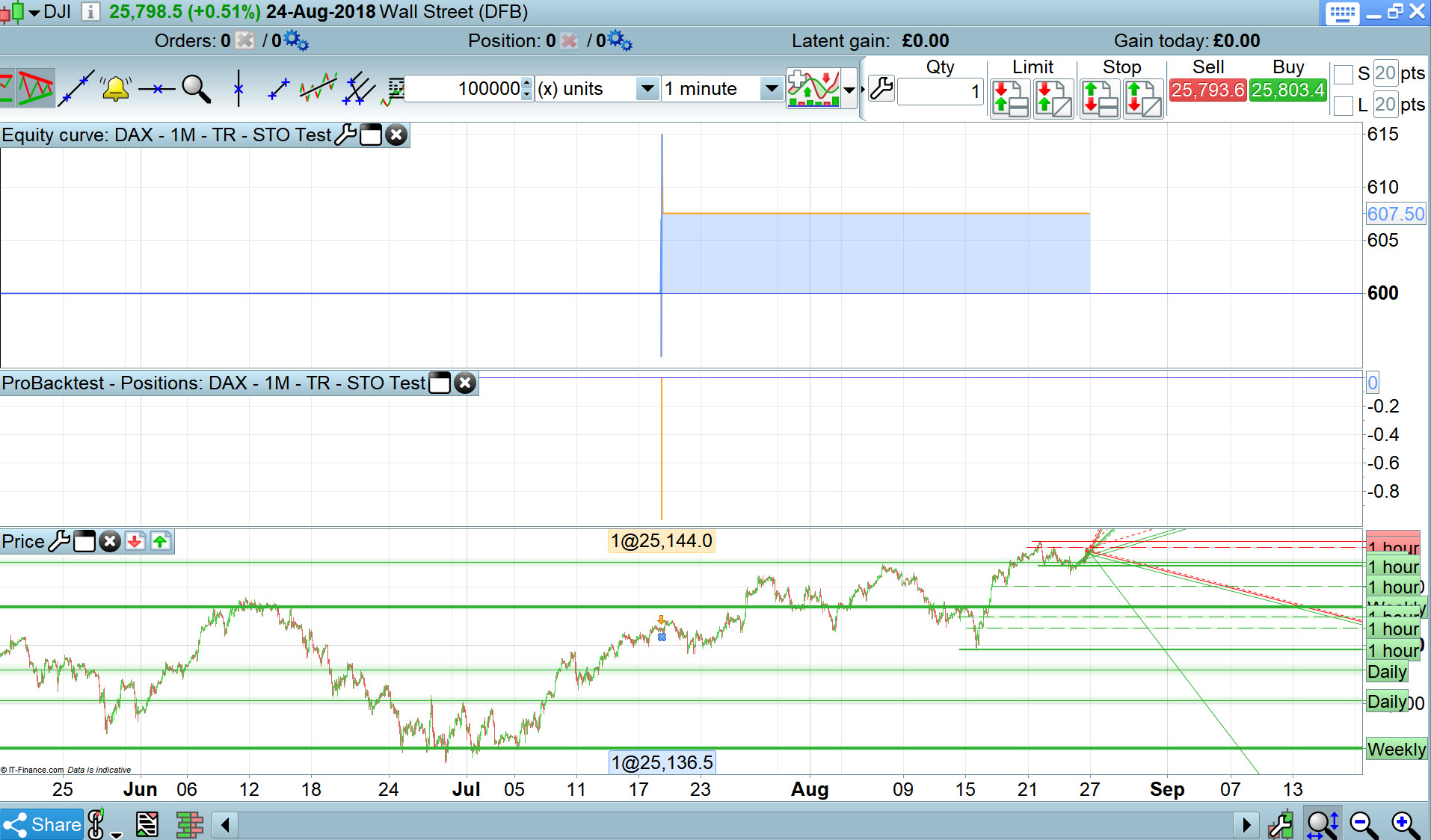

I tried it on my Platform over 100k bars on DAX 1 min and it executes nil / zero trades … so that is the first problem – no trades – Yes??

Hi GraHal,

I don’t feel like Frankie…instead I want more coding…I’m getting addict 😀

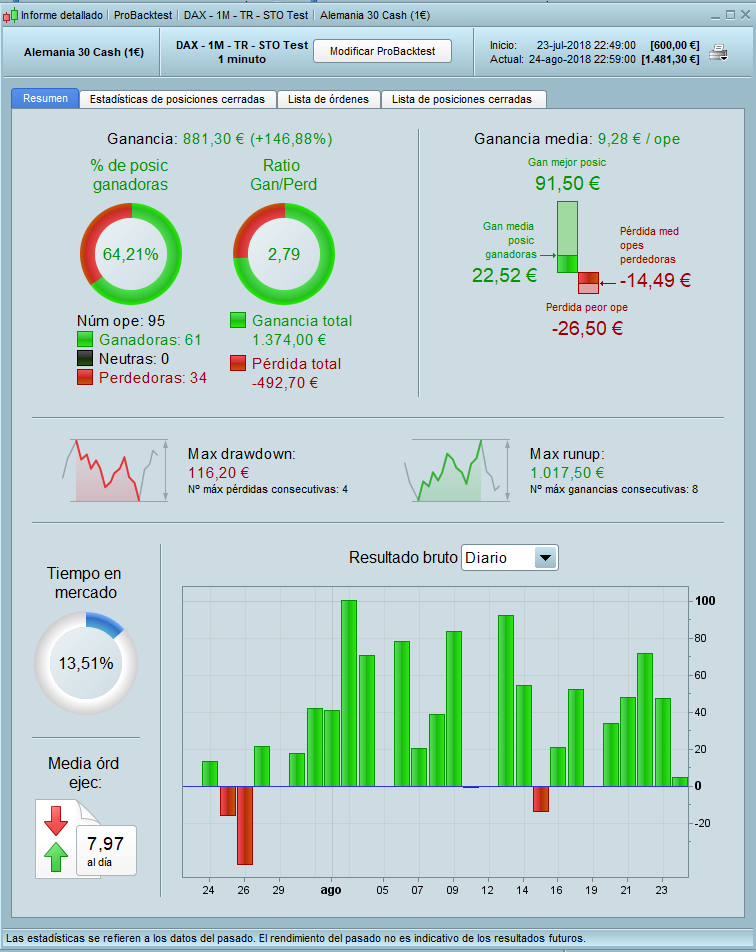

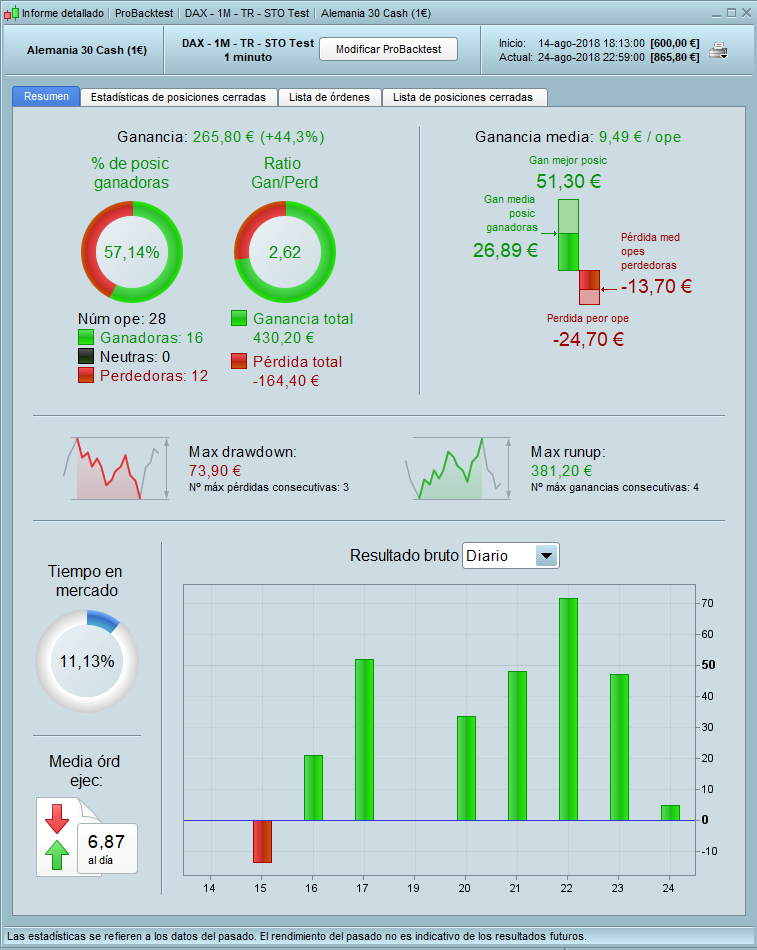

I don’t have problems with code, but I upload it to test it. In 100000 bars doesn’t have great results but yes at 10.000 and 30.000 and my idea is updating vars to adapt it at market conditions.

I attach also some performance results.

Thanks again.

I test it at IG DAX 1€ cash.

I got 1 trade on a 5 min TF over 100k bars on DAX so my conclusions would be that your code has far too many AND conditions and they are not being met all at the same time.

I tried deleting Buy conditions one by one and I got trades (on 1 min TF) but they lost loads and loads of £££s.

I think you need to put chains / ropes on Frankenstein v1.0 and start on Frank v2.0 with far less conditions?? See if you can get signs of life in a finger before putting the whole monster body together?? Sorry couldn’t resist that! 🙂 🙂

On a less jokey note … did you run the System and get trades after adding each condition or did you write lots of conditions and then run the code (apply the lightning bolt to Frank!)??

Edit / PS

I wrote above before I saw your post with results … weird that I get zero trades? I’ll try running again again and report back.

Hi GraHal,

I don’t know which may be the real problem with your tests. I’m testing in € and capital is configured in PRT strategy window.

- Initial capital: 600€

- Spread: 2

Also, my country is Spain…not sure if it may affect to tests and results, because it works from 10:10 to 17:25 to avoid high commissions and market openings.

If you see performance data attached, are very promising. Of course I would like to reduce vars and conditions but I think it works nice for me.

About my doubts, have you got any idea? It’s adding some more code but I don’t fear of it 😀

Thanks again for your comments.

Aha I try it now on my Spread Bet Platform and I get 1 trade on DJI at 1 min TF (still no trades on DAX 1 min on CFD or SB PLatform).

Bit of a mystery, maybe it is the Time settings difference between our Platforms … Ill convert the times and report back.

EDIT / PS

To get same the lightning bolt at same time as Spain, I knocked 1 hour off Flat Before / After and still the same results … no trades on DAX at 1 min. Also I used the .itf file … so I have all Franks body parts in my Test Lab also! 🙂

but yes at 10.000 and 30.000

What do you mean re above?? 10 AM and 3 PM or what?

Sorry… 10000 and 30000 BARS

In Spain we use dots [.] instead commas [,] for thousand separations.

Regards.

@komiya Are you 100% sure that the results you show in post above are results for the code in the .itf file??

I can’t understand how you get trades and I don’t with the same code on same data on same TF etc etc??

Anybody else offer any thoughts on why nil trades for me and 95 trades for komiya??

Hi, I reupload again but it’s working nice for me…

Anybody else may test it and think about my question?

Thanks a lot people!