cfta

cftaParticipant

Senior

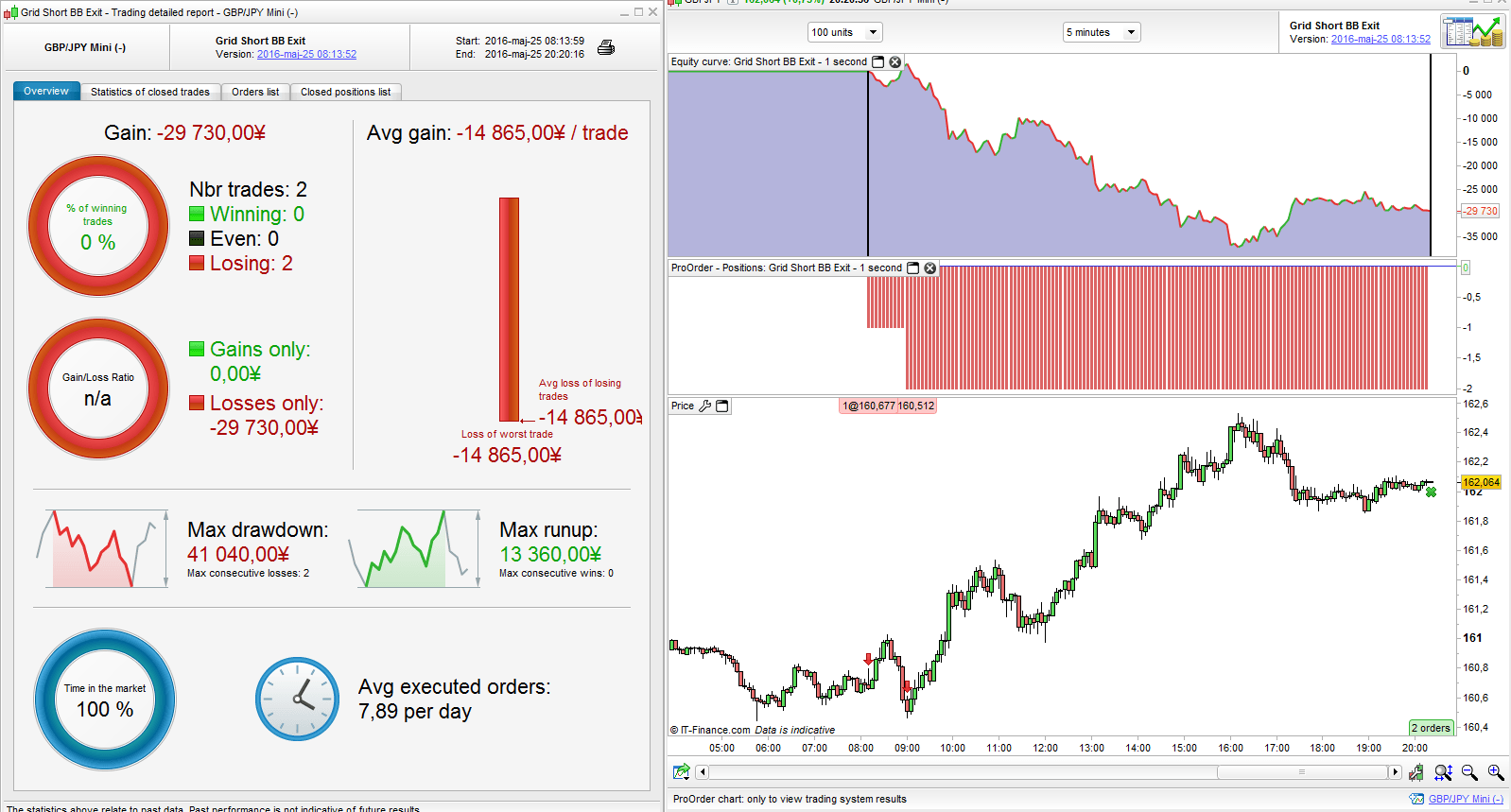

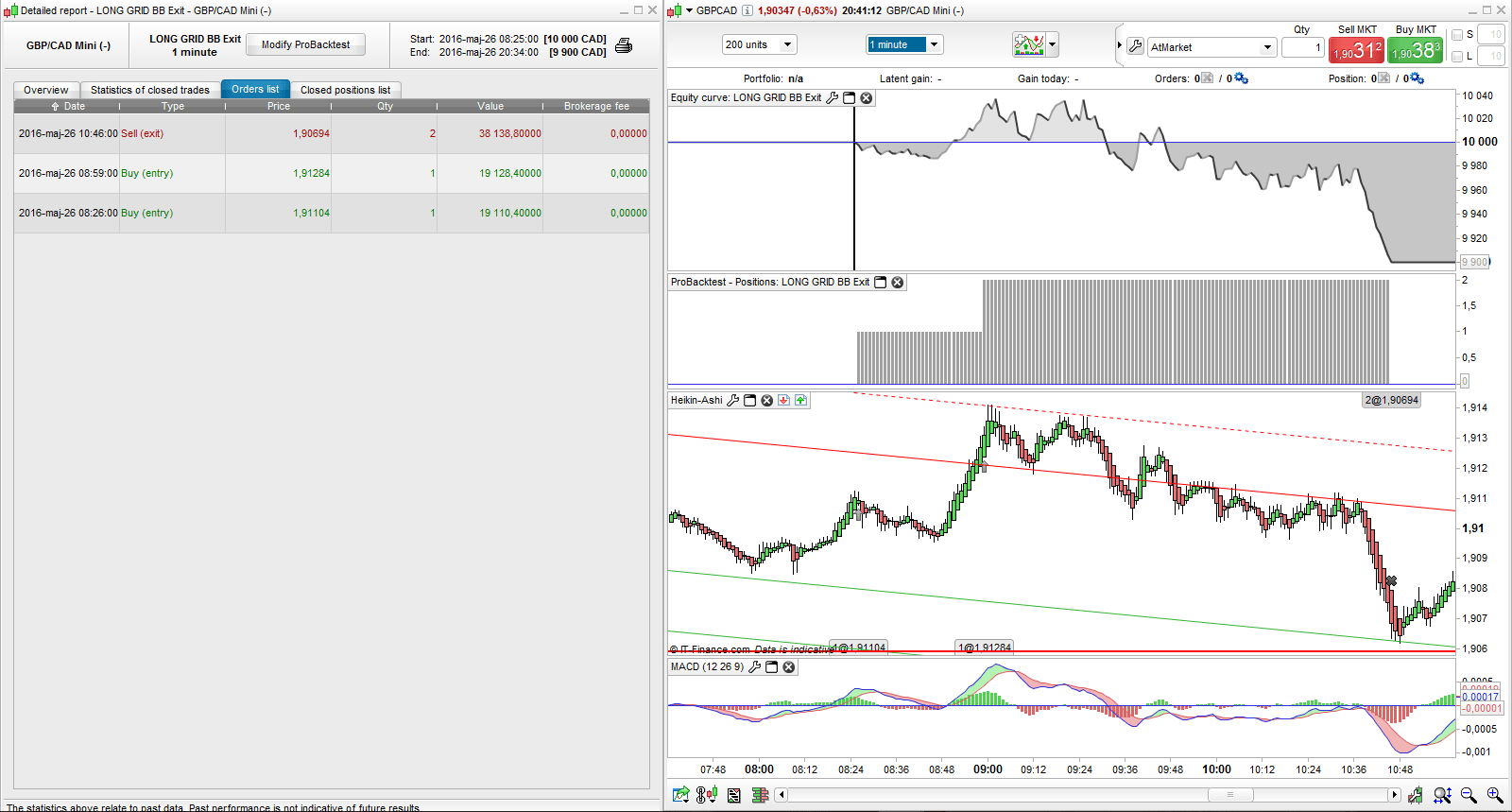

So another day of real time testing, as I mentioned in my post yeterday the BB exit is working great so far but the regular SL at 1 % does not seem to be working. The Nikkei trade I opened on Monday and wrote about was not closed at -2% neitherr was a GBPJPY trade which i took today setting the SL at -1 %, the floating loss reached about -2.3 % before I stopped the system manually. Please have a look guys to see what might be the problem…

@Brage & Simon, sure thing guys there is so much code around it is starting to get tricky to keep track of all of them. These are the ones I have been testing live this week note that I change the parameters depending on which system I run it on;

Long;

//-------------------------------------------------------------------------

// Main code : LONG GRID BB Exit

//-------------------------------------------------------------------------

defparam preloadbars = 100

once RRreached = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 2 //whole account risk in percent%

gridstep = 10 //grid step in point

amount = 1 //lot amount to open each trade

rr = 2 //risk reward ratio (set to 0 disable this function)

//first trade whatever condition

if NOT ONMARKET AND close>close[1] AND STRATEGYPROFIT=0 then

BUY amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = ((close-positionprice)*pointvalue)*countofposition

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*2

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

Short;

//-------------------------------------------------------------------------

// Main code : Grid Short BB Exit

//-------------------------------------------------------------------------

defparam preloadbars = 100

once RRreached = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 2 //whole account risk in percent%

gridstep = 10 //grid step in point

amount = 1 //lot amount to open each trade

rr = 2 //risk reward ratio (set to 0 disable this function)

//first trade whatever condition

if NOT ONMARKET AND close<close[1] AND STRATEGYPROFIT=0 then

SELLSHORT amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep*pipsize then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = ((close-positionprice)*pointvalue)*countofposition

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*2

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risj reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

EXITSHORT AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

Because you didn’t change the line 32 to:

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize //actual trade gains

That’s the reason why your loss is not well calculated.

@cfta and Nicolas – quick question pls. When I run the code as is it only produces one trade, but when i remove STRATEGYPROFIT=0 from the first trade condition it works? Thanks

cftaParticipant

Senior

@davidp13

Does it only take one set of trades or only one single order? It’s only supposed to run one cycle after being started and not take any new trades until started manually again, in addition keep in mind to run it on low timeframes otherwise it will for conditions to be met and for the candle to close.

@davidp13

Yes if you remove this STRATEGYPROFIT=0 condition, it will start over again after each cycle.

Hi,

I am following your work as it progresses and it is positively AWESOME! But I have to agree with Davidp13: if you run the code like this, it only produces 1 (one) trade, not one cycle.

Therefore, if your remove the expression STRATEGYPROFIT=0, it keeps going on. However, as ctfa has pointed out, the idea is that this code finishes a whole cycle of trades, not just one trade. After the cycle, it has to be started manually again. If you remove the STRATEGYPROFIT=0 expression, it keeps going on and that is not the idea either. So, I respectfully conclude that something isn’t perfect with the AND STRATEGYPROFIT=0 condition.

I hope this helps somewhat.

Kind regards

cftaParticipant

Senior

Good morning traders, I still have issues with JPY pairs in real time testing since the SL kick in way too early, do anyone have an idea what might be the issue?

//-------------------------------------------------------------------------

// Main code : LONG GRID BB Exit

//-------------------------------------------------------------------------

defparam preloadbars = 100

once RRreached = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

gridstep = 15 //grid step in point

amount = 1 //lot amount to open each trade

rr = 3 //risk reward ratio (set to 0 disable this function)

//first trade whatever condition

if NOT ONMARKET AND close>close[1] AND STRATEGYPROFIT=0 then

BUY amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize //actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*2

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

Hi guys please read all the topic and not only last page. We have explained why it takes only one sets of entry the code posted by nicolas!

I have shared a version that doesn’t stop working after the first entry.

That’s a very long topic now, maybe if someone plan to make a fork with this code with other concept and strategy, he’s welcome to open a new topic. This forum belong to the community. Me and other coders here can help everyone to make things better, but since I have only one brain 🙂 , please make things happen by yourself, I’ll be not too far.

@cfta

Because the floating profit is calculated in Yen… And it’s the case in any other forex pairs (pipvalue = 1$, 1CHF, 1PLN), pip value is returned in the current currency of the pair and since Japanese pairs have only 3 digits, the pipvalue = 100 Yen.. So all money management has to be reviewed for this case.. I just came across the same error elsewhere.. Need to think for the better way to fix this issue, sorry for that.

cftaParticipant

Senior

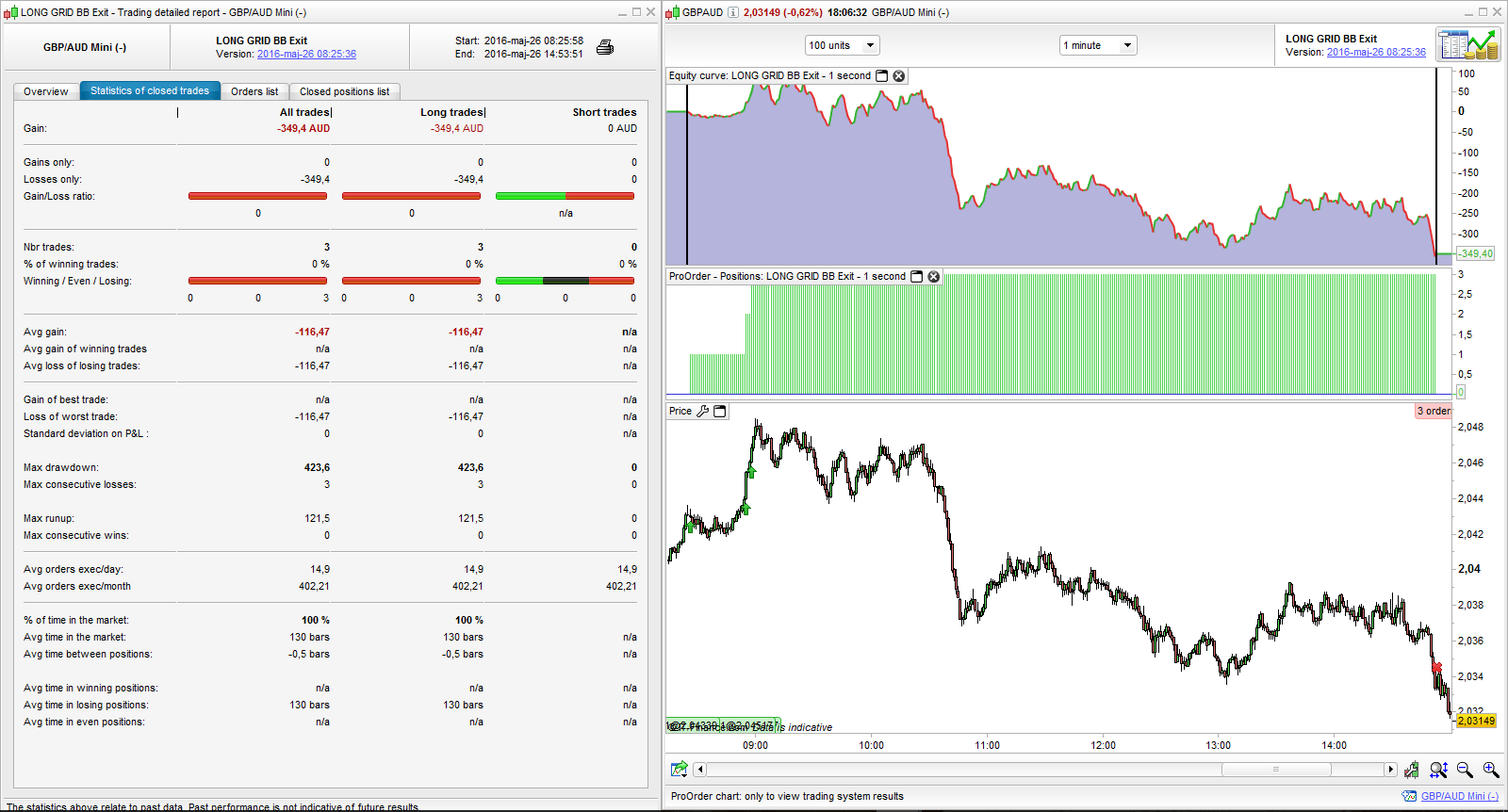

@Nicolas

I updated the code yesterday as you adviced but I still have problems to make the SL work, today I tried it on GBPAUD set to kick in at -1 % but it didn’t trigger. I have been paying attention to update the corrections and changes of the code, I may have missed something but I can’t figure out what. This is the section that I changed;

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize //actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*2

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

Regarding the floating profit issue calculation with the Yen I would not mind having several sets of systems adapted for different assets if it is easier to fix than one system which works for all, such as one for indices, another for FX pairs with one digit and five decimals, a third one for Yen pairs and other crosses with more than one digit and so on.

Is anyone else testing in real market conditions and having the same problem?

Today I will start testing david-1984’s code too 🙂

Did the profit reached the risk reward ratio?

cftaParticipant

Senior

No the profit did not reach the risk reward ratio, whenever it has reached the ratio the BB exit seem to work perfectly, it is when one or a few entry orders are triggered and price then turns around going the wrong way.

The first type of SL fixed at X % worked great for the first code you wrote with 1 % SL of account balance before we implemented the BB exit, could it be possible to integrate parts of that code into the current BB exit code?

I understand, but did some tests again today and everything’s fine in Probacktest so far… Does the same problem occurs in Probacktest on your side please?

cftaParticipant

Senior

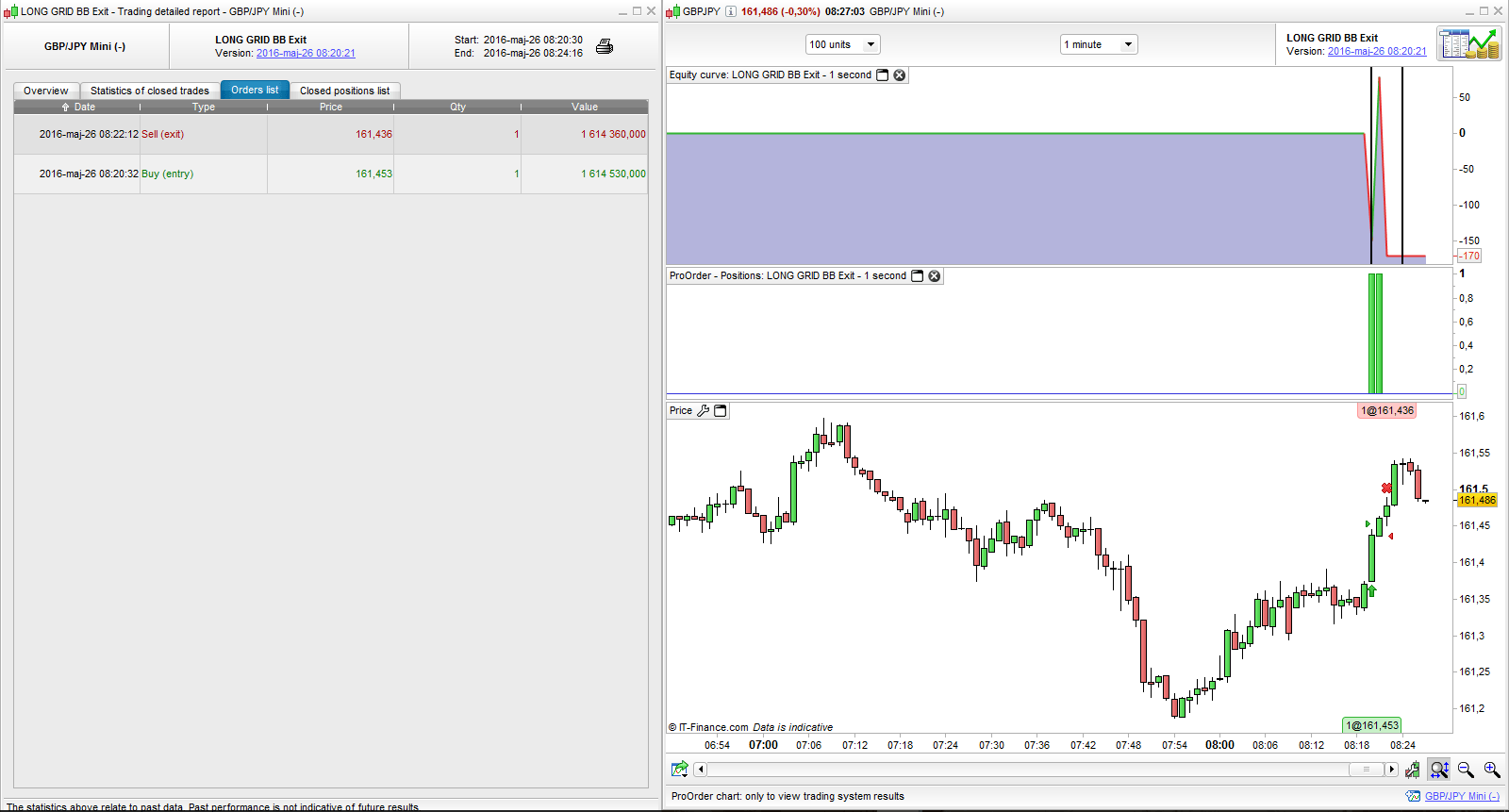

I just checked and entered the same time and parameters as the GBPAUD trades from earlier today but in Probacktest the SL worked perfectly. I ran it on both 1 minute and 1 second, only differnce was that one more trade was entered on 1 seconed and the SL kicked in accordingly at about 33 pips below the average price of the three positions.

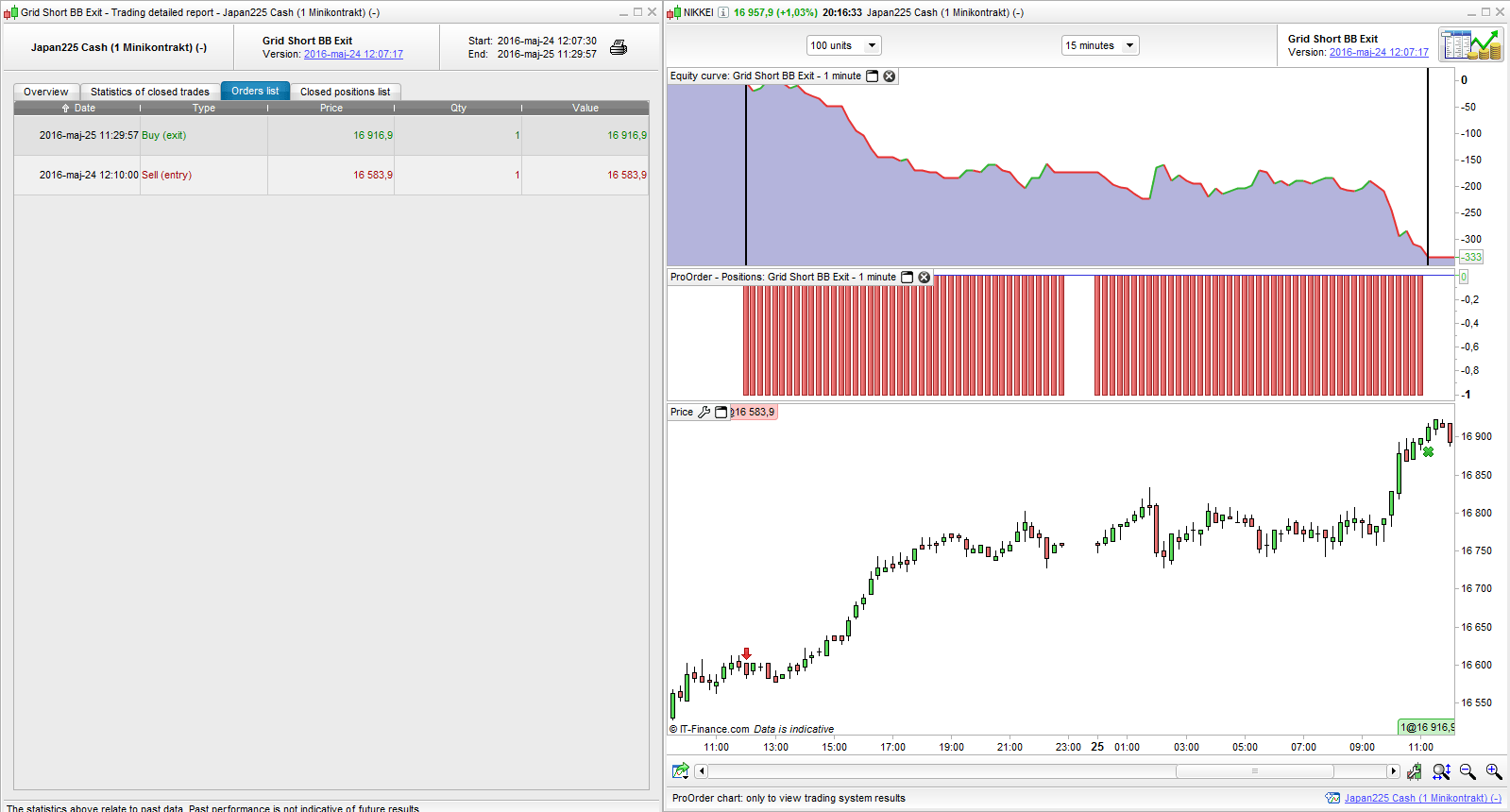

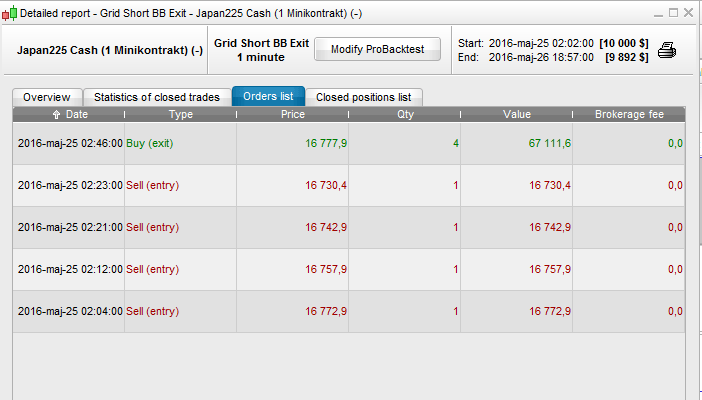

My Nikkei trade from Tuesday which did not stop out yesterday in real time worked fine in test now.