Hi guys!

This code looks really interesting and I’m following your work and progress since I think proper money management is a key to profitable trading.

Just a thought on the 1% stoploss. As it is coded now newSL = positionprice – (positionprice*0.99) doesn’t it just calculate the difference between the positionprice and the new sl? Shouldn’t it just be newSL = positionprice*0.99?

This code states:

make the New Stop Loss = POSITIONPRICE (being the average of the Positions Price(s) – 1% of the Average Position Price(s))

Lets say the Position Prices are:

95 + 100 +105 = 300

300/3 = 100

newSL = 100 – (100*0.99)

newSL = 100 – 99

newSL = 1 (which is 1% of 100)

If understand it correctly.

@Brage @dwgfx

Thanks for your help.

Yes It were that I thought at the first glance, but since we want to exit at 1% loss of the account balance, it’s not it 🙂

So now tests are good, I coded the sell side version and made a small fixed for forex pairs. Here is the full code (also attached in itf file to this post):

defparam preloadbars = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

gridstep = 20 //grid step in point

amount = 1 //lot amount to open each trade

//first trade whatever condition

if NOT ONMARKET AND close>close[1] AND STRATEGYPROFIT=0 then

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND close<close[1] AND STRATEGYPROFIT=0 then

SELLSHORT amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep*pipsize then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

//GRAPH mindistancetoclose as "d"

//stoploss trigger

if onmarket then

SELL AT positionprice-mindistancetoclose STOP

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

Please don’t leech it only. Instead, please add comments or any ideas that would improve a strategy or create a new one with this code. There are many brainful traders here and i’m pretty sure that we can make something cool all together with this nice money management idea 🙂

cfta

cftaParticipant

Senior

Amazing Nicolas and thanks a lot! I will start testing it tonight and I’ll come back with an update tomorrow night…

cftaParticipant

Senior

I’m afraid I have already come across some trouble, when I try to run the code in real time market I get this error message and the system is stopped;

“This trading system was stopped due to a division by zero during the evaluation of the last candlestick. Please add protections to your code to prevent divisions by zero.”

This is the code I was using, tried both long and short and with or without the graph line;

//-------------------------------------------------------------------------

// Main code : Grid Short Nicolas

//-------------------------------------------------------------------------

defparam preloadbars = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

gridstep = 20 //grid step in point

amount = 1 //lot amount to open each trade

//first trade whatever condition

if NOT ONMARKET AND close<close[1] AND STRATEGYPROFIT=0 then

SELLSHORT amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep*pipsize then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

//stoploss trigger

if onmarket then

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

Any idea what might be the problem?

Ahahah

“division by zero” is something that ProBacktest don’t know apparently 🙂

Well, if you have set correctly the line 7 to 10 (no zero values), the problem is in line 26 (this is the only code line with a division).

A quick fix would be, move the line 26 into the “//stoploss trigger” function, like this:

//stoploss trigger

if onmarket then

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

That would make the trick.

Great work! This is fun! 🙂

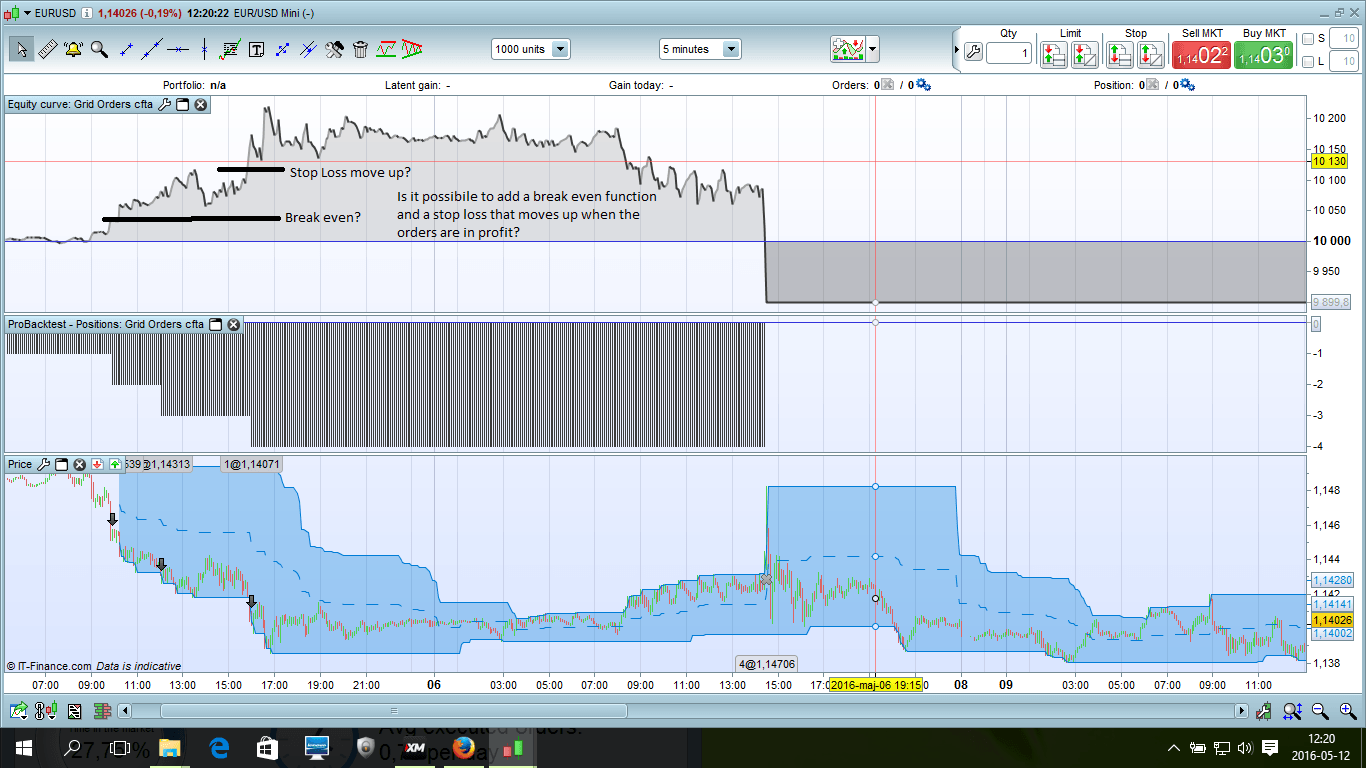

Question: Is it possibile to add a breakeven function, and a stop loss that moves up when the orders are in profit?

I thought the code:

liveaccountbalance = accountbalance+strategyprofit

would do that, but it seems like the stop loss don’t take the profit (from the orders) into calculation? But only start account balace?

So maybe a breakeven function, and a stop loss that moves up when the orders are in profit based on equity curve?

I have tried this but can’t make it right.

Or will this behave differently in real market?

All the best!

Yes, everything’s possible.

Actually, the code don’t calculate the floating profit. The code do actually exactly what cfta wanted and there’s no any ‘takeprofit’ system in it. I already have some ideas for that based on the live equity curve as you mentioned it.

Firstly I would like to find a mechanical way to enter the market for this system, that would be fun 🙂 Any idea?

Nice Nicolas!

Yes, I have thought and tried a few things 🙂

My conclustion was that maybe it isn’t nessesarily because of the 1% account stop loss.

Otherwise my best suggestions is:

a) Entry based on pricemove:

// Conditions to enter long and short positions

gridstep1=x

//first trade whatever condition

if NOT ONMARKET AND close-tradeprice(1)>=gridstep1*pipsize then

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND tradeprice(1)-close>=gridstep1*pipsize then

SELLSHORT amount LOT AT MARKET

endif

b) “Good old turtle fashion” (on 5min TF):

// Conditions to enter long positions

c1 = (close=Highest[600](close))

// Conditions to enter short positions

c2 = (close=Lowest[600](close))

//first trade whatever condition

if NOT ONMARKET AND c1 then

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND c2 then

SELLSHORT amount LOT AT MARKET

endif

c) I have also tried MA, but don’t like it:

// Conditions to enter long positions

indicator1 = WilderAverage[40](close)

indicator2 = WilderAverage[40](close)

c1 = (indicator1 > indicator2[1])

// Conditions to enter shortpositions

c2 = (indicator1 < indicator2[1])

//first trade whatever condition

if NOT ONMARKET AND c1 then

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND c2 then

SELLSHORT amount LOT AT MARKET

endif

But as said, maybe this is not nessisarily, or maybe a “mini-turtle” is enough :

c1 = (close=Highest[200](close))

I also think its important that I don’t “cut” this thread from cfta, since he started it 🙂

You are right. I’ll code floating profit of the whole orders basket and then we’ll can move stoploss accordingly to x% profit.

About entries, breakout of recent highs or lows is clever. However, I think that we should introduce another trigger like recent volatility.

Hi Nicolas and cfta!

Nice work so far. Really interesting.

Can this grid order code be combined with any of the 15-min Breakout-systems in the library for a daytrading system? With gridsteps and riskpercent adjusted to the market traded? And perhaps flat after market close?

Yes of course. It only needs some copy/paste experience 🙂

I need to finish some other things right now, maybe someone can have a look in the mean time.

cftaParticipant

Senior

Good morning fellows,

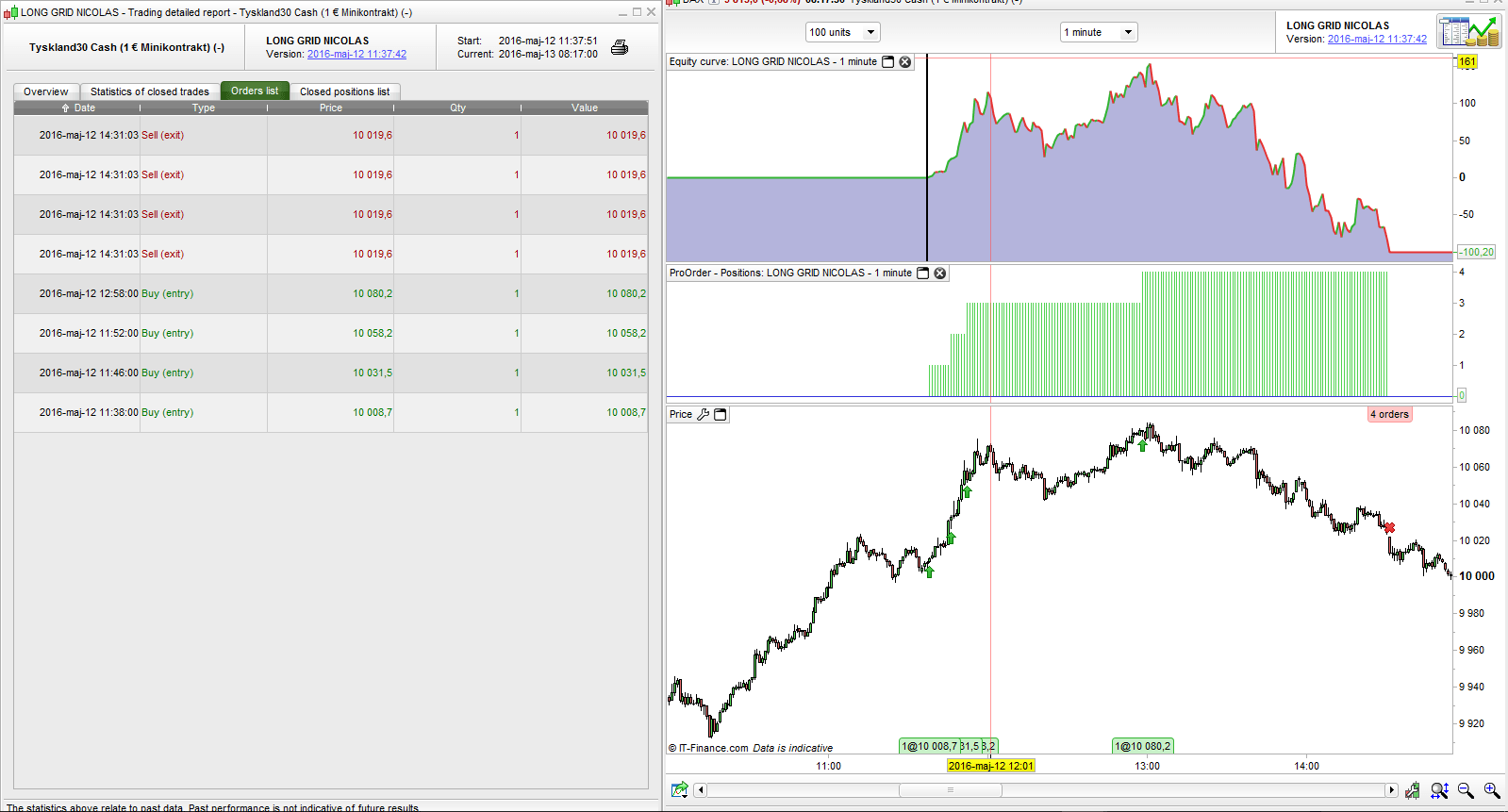

I had a very long day at my regular old school job yesterday so I didn’t have time for posting but I did some testing remotely. I’m thrilled to see all the suggestions for further developement, a stop loss triggered by trend change, by MA cross, stochastics, ADX or whatever is the most effective is of course a great way to maximize profits.

For the real market testing everything looks well, entries where taken as intended and the SL worked perfectly. Great job Nicolas!

I’ll stay in the mix for discussing further improvements…