Hi,

as we are approaching end of this year I will post some data from my „model account“ (trading DAX only): behind there is a portfolio of 11 algos, 6 long and 5 short, which I run with 10k EUR live on CFDs, almost no changes since more than 2 years on those algos, all earnings when exceeding certain amount above 10k I am withdrawing from this account, so periodically bringing equity down to 10k and keeping position sizes for each algo stable (as % of those 10k). this account is a „model“ in these terms:

- it contains most robust of my systems with kind of optimal position sizing for each of algo as part of the portfolio, resulting in – for me – acceptable portfolio result in terms of risk/reward.

- Since the reference of all results are always those 10k, having almost no changes of systems, also not adding or removing systems, I have comparable numbers month over month, and year over year

- It’s not my main account 😀 since „main“ I am now running on futures, but „main“ contains currently 7 out of 11 algos from the „model“ (the reason I am not running all 11 on futures is because I would not be able currently to run all of them with intended/their unique position sizes within a portfolio)

So, end of month results as % of equity on „model account“:

SEP +3,7% OCT -6,2% NOV +1,2%

So yep, OCT/NOV was not great but in fact nothing extraordinary – even if somewhere end of NOV this account was reaching drawdown of 13,7% of equity. Not funny for sure, yet 13,2% drawdawn it experienced in APR this year as well (when GraHal was opening this discussion), and SEP 2023 it had similar drawdown, too. So all fine – this matches my target: not to have drawdowns exceeding 15% of equity.

What do I learn, from such months… and drawdown periods… they will come again and again! They have to come. And the worst is probably not in the past but in the future. So I have to expect such times – and that means I have to be prepared. And being prepared means first of all – don’t „overtrade“ (means – don’t trade too big positions compared to the equity available). And reduce risk (position size) if drawdowns approach levels which are not „comfortable“ any more for me personally. I was reading that I think some 15 years ago but I will never forget, what Larry Hite was telling in his interview: „Risk is a no-fooling-arround game. It does not allow for mistakes. If you do not manage the risk, eventually they will carry you out“. Furthermore, what I learnt during “bad times” is that there are times where kind of everything goes wrong, longs do not work, shorts fail, diversifications seems not to help, everything “goes to hell”. I think there are probably time periods where biggest market players withdraw from the market, not acting, not taking decisions, waiting, just waiting for some catalysts, and during such times there is quite a mess “everywhere”, in major indices, currencies, commodities… maybe at these times trading single stocks would work, but I don’t know and I don’t care these days. I have to take care I “survive” those messy periods until they are gone. one cannot predict when they will start, nor when they will be gone.

I would never again accept drawdowns bigger than 20% of equity, but as mentioned above, I am targeting (since arround 4 years) to have not more than 15% as max drawdown. And I think if my main account will be growing further I will be probably reducing my expectations down to max 10% drawdown and possibly even further. I kind of do not have „target“ for earnings / no precise max profit expectations, but I definetely have a „target“ for max acceptable losses.

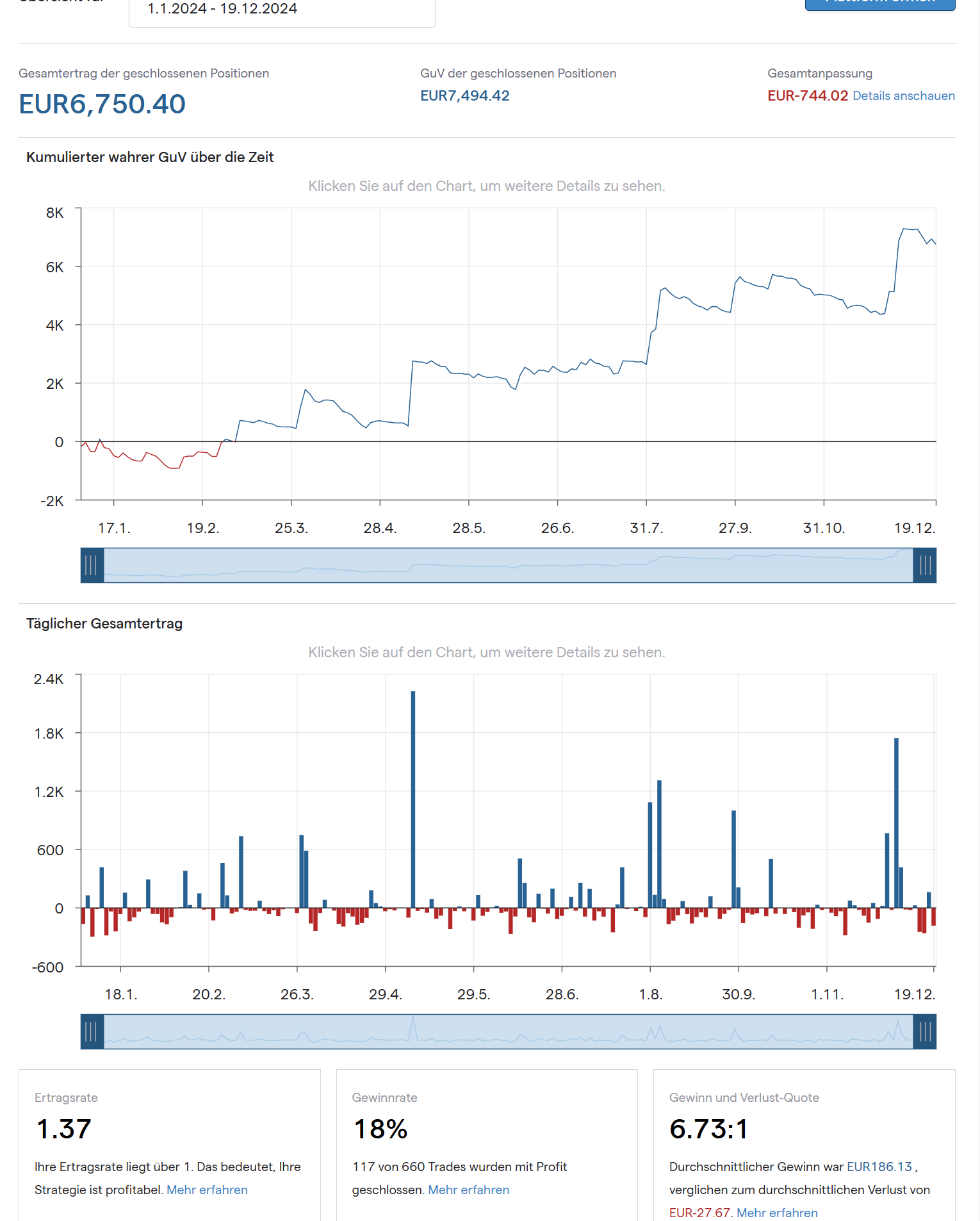

And since SweTrade posted his YTD result and asking others, I am willing to post mine: the „model account“ earned so far 67,5% with above mentioned 13,7% max drawdown. In fact pure trading result was ~75% but lot of if was „eaten“ by overnight financing costs and some smaller part by guaranteed stop fees (using such stops for those few algos which are designed to carry positions over weekends and bank holidays).

Even it’s not a 100% proof, I am attaching as „proof“ the printscreen from IG platform with real results of that „model account“, where you can detect equity curve and some more details as well. Maybe funny one – especially for those chasing win-rates of 70% 80% 90%: my „win-rate“ is only 18%, so only 117 out of total 660 trades this year were closed with profit.

What’s possibly interesting but not showing up in IG’s statistics: until mid of NOV my shorts on DAX – which was making multiple all time highs whole year – all together were earning YTD slightly more than longs all together. Ok, it turned arround very end of NOV – when DAX kicked off that amazing rally, going up with no significant pullback for 7 days in row.

Cheers

justisan