Interesting discussion from more than one angle … So regarding the last few posts, here my 2c :

If you can’t trade manually, you most certainly won’t be able to trade automatically. Then indeed you will be bailing out while your algo was made (by you !!) not to do bail out ;-). And yes, this all comes down to your knowledge and vast experience on when to bail out, or 90% of the time : when NOT to bail out.

This is all easier said than done;

A/o I have a PRT-IG account with positions (not Automatic). I never look at it. I did not look at it for so long, that now – after yearssss – I can look at it without interfering with it. I trust it. It ran over Trump – it ran over Corona. It works. Maybe I did not put in the worst stocks and indexes (so all starts with thinking over decently what to have to begin with), so that is a kind of prerequisite. I mean, maybe don’t put in Bevcanna Enterprises Inc in there (which I am looking at in my PRT-IB account and position in it, 17% down yesterday and such).

Then I created myself a “Monkey” account. It should do the same thing, with a pre-selected Future. Well thought-over. I should make a lot of money with that. But never touch it (Monkey) ? … I can’t … It is another PRT-IB account, and the same future I trade x times per day in my main account. How can I leave alone that Monkey account, knowing how much I am losing there, at times.

Still with me ? 😉

And so I reserved a small area on my monitors for that account. The Trade buttons are “On”. Since I run that account, the Future has been risen 10% (this is in just a month only). This is way beyond expectations. But the volatility is high. What’s bad for the monkey, is that while the Future rose 10%, my portfolio in there – only (in the end actively)trading that one future, rose 20%. Mind you, this is “net” after a month, because it has been 40% as well. You win some, you lose some.

But think of it : on a day like yesterday, the lot drops 1.5% without reason, and those with experience will know that “without reason” will come back to you with +1.5%. So there I am … I made profit on the first normal 1% rise. I then made profit on the 1.5% drop. And lastly I made 1.5% on the rise again.

Moral

There is no single way that I can incorporate that in my algos, but that could be me. What it IMO would need is the News, where “no news” means that no drop / rundown is dangerous; I know this by experience (experiencing such happenings a 1000 times).

I would attest that with the instruments and algos you people would apply (of course I can’t know exactly), there is no escape from looking “constantly” and bailing out when you deem it necessary. Thus, my story above is easy to tell, but might Trump have hidden the nuclear Codes there in Palm Beach somewhere, you can think it will be OK at some stage, but prior to that your money has left you. All of it.

I don’t think any algo can run forever without looking at it, unless it is a most technical one. With “technical” I mean that you firstly can see through what the charts are telling you for real, which secondly you are able to code 1 to 1. With that I surely will allow to put that in a monkey account and watch the news for something going wrong on an exchange somewhere. Haha.

I hope this post is not too much of loose sand. But a sub-moral could be that while you get better and better in (manually) trading itself, it becomes more and more of a challenge to let the AutoTrade program make more profit than you would be able to achieve manually.

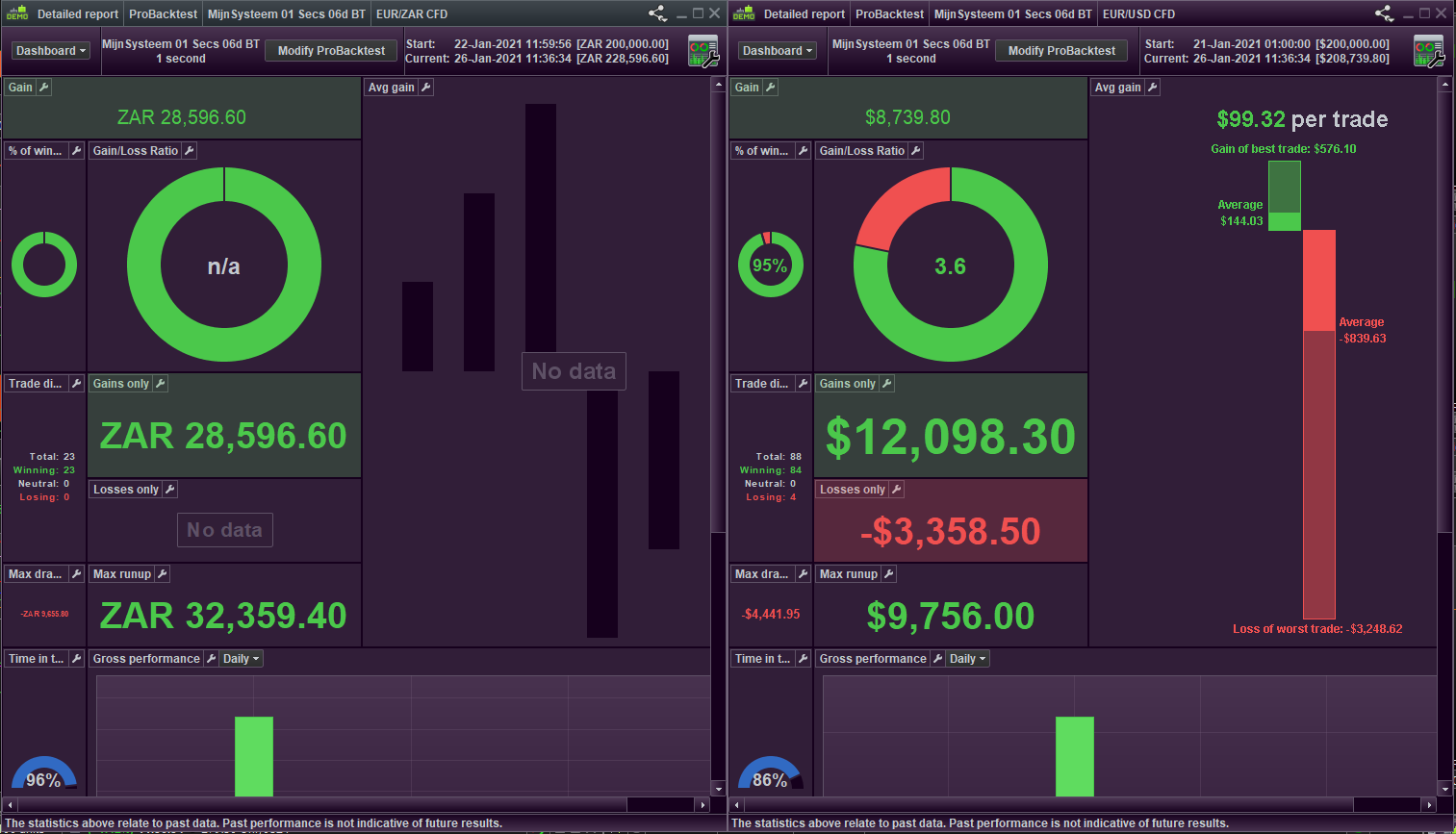

The below could be a teaser, a show-off, or just unimportant, but with that I try to tell you that both don’t say much. I know for myself, that at least the left hand one is sheer coincidental. However, I also know that I could make any instrument work out like this if only one trade with gain has been accomplished. This chance is, say, 95% that this will be so. You can see that somewhat on the right hand one, which, well, shows 95%. To let it work out like that is easy enough : have a Stop 1 mile away and the money to cover for that when it goes wrong. But it is not about that … it is about the absolute money. So look at the left one, EUR/ZAR. The thing behaves well within my set bands which is exactly why there are no losses. But look closer and see that there are 22 trades only over the same period of time as the other one, EUR/USD. This would be the same as setting the Stop that mile away, never reach it and have few trades only.

And so I allow that lower Stop, more losses – and so we can quickly proceed with those 95% of winning trades, bringing in the end more money. Mind you, both have the same Stop distance, but EUR/ZAR is just less volatile. Btw, the ZAR is something like 18.50 against the EUR thus what you see there is EUR 1545, while the EUR/USD (at 1.22) = EUR 6821 – at the moment of this writing with 84 trades, as that one goes on and on and on. Not so with the ZAR, which just entered its 5th trade today because of insufficient sense of direction (haha).

Right. According to GraHal’s “rule”, the currently shown 3.49 x 95 gives 332. Yes, that is more than 100-ish. And I am sure that in a certain (consistent) environment this could consistently be useful as some standard. But I never saw it like that. It is about the $. OK, we all know that, but would 100-ish be OK not to lose and gain a little, 300-ish might imply that bank job you always dreamt of. And just saying : don’t look at that number you see there. It is only that “low” because it is not possible to throw more money at it, at this moment – there’s something wrong with PRT-IB’s leverage for the newly introduced CFDs for Forex (thank you mr Brexit) – combined with the limited portfolio (base) in the Paper environment. Normally that should be multiplied by 10 (I always did that until two weeks ago) which means that it would say 83K. And that in 200K seconds, because that is what it is.

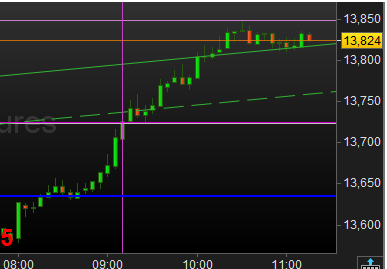

Do I have more to show off ? oh, probably. One example : during this typing I did not notice really that the DAX (Future) rose 2% (from -0.5 to +1.5). See 2nd attachment. Now trust me, … when the same amount of money is thrown at that as the EUR/USD uses there (which is 1M) then that would bring over 20K. Thus, this is 8.5K vs 20K. So what is better ? that AutoTrading stupid show off, or my real trading ? Sadly that is even in 12K seconds instead of 200K. So you see, I must still me lousy on the autotrading.

Last thing : The Gain/Loss ratio doesn’t tell a thing, because it van be coincidental. IOW, would I let run this for a day longer, it may have dropped drastically. The % of winning is quite crucial though, because it determines the robustness of the to be expected Ratio. While this is logical (in my view), it should not be underestimated as a robustness figure in itself. Thus, if it would say 1.01 it will mean that I just may have made one more profit-trade than a loss-trade, but at what profit do we work and more especially, at what losses (Stops !!). Both are as crucial as the profit (say Trailing) dtermines the initial profit, while the distance of the Stop determines the money you allow yourself to lose in a number of expected trades (Ratio !) which meanwhile doesn’t give you profit at all (waiting for the run up again). … In the beginning of this post I tried to talk about all these aspects in different wording. These aspects indeed all weigh in.

I hope this helps someone !

Peter