Well,

Little update after 2 weeks (The purpose is now to now when we should do another backtest = Update the parameters

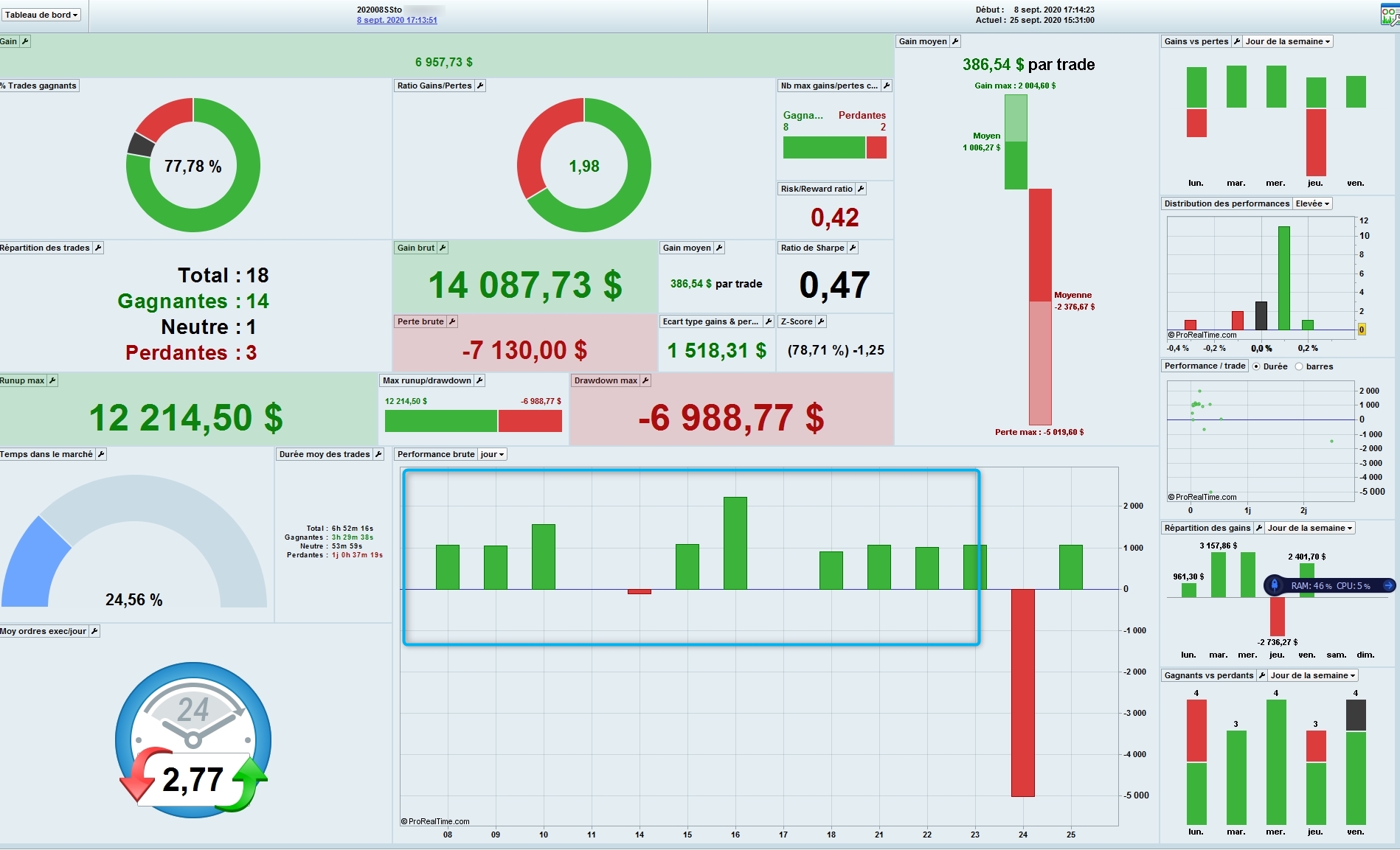

Donkey Sto after 12 days = 12 * 1440= 17 280 = 17 280/100 000 = 17 % of the first backtest = 1/6 of the period

Donkey SAR continue to perform = + 176 % after 16 days. Not bad at all, I’m very surprising …

So let’s continue with this algo and we will see what will happen

Great results! I’m really interesting in your strategy: I understand if you don’t share the code…but if you explain indicators, timeframes, and concept it will really appreciated.

thank you very much.

Hi @danistuta I think it’s on the file, but indicator is SAR of course, timeframe 1 mn on EUR/USD and as always One signal (SAR)+Analyze of the market structure (You can use what you want to determine range/trend)+Money Mangement( Stoploss/Trailing/Target). Nothing complex, always Keep It Simple

Bye

Great, and if it’s possible to know…which condition do you use for entering with SAR?

Thank you very much.

À very simple crossing between SAR and price

Thé purpose was to show/confirm that Strategy doesn’t matter

Byr

Thé purpose was to show/confirm that Strategy doesn’t matter

By strategy I assume you mean ‘entry conditions’? If so then why not just run a strategy that simply opens a trade at the same time every day and remove the entry conditions altogether? You could run 19 of these all opening at different times alongside your SAR test strategy and the results would show whether the entry conditions are important or not by direct comparison.

You can use what you want to determine range/trend

This along with your SAR entry conditions now means that we have three criteria for entry which makes the entry conditions quite an important part of the strategy – which means that it is difficult to determine whether it is the money management, stoploss, trailing, target or entry conditions that are the important part of the strategy.

Hi @vonasi

By strategy I mean mostly “entry conditions”. It means that I think that we can have many good algos with many many “dumb”/donkey indicators. But it doesn’t mean it could work with all indicators and all entries conditions (It will be marvelous). For me entries conditions is probably the least important thing in a strategy. As you see we can have pretty good results with CCI, Repulse, SAR and so on…

But you’re right some strategy exists with no indicators (buy at open …), I could try

For the second part, I change generally only the entries conditions not the money management neither the analyze of the structure that’s why I think entries conditions are the least important things in an algo

Have a nice week-end

And as I said and read (These august holidays and last weeks I think I read more than 15 books on Algos … very very interesting ) the more complex algo and the more parameters give the better IS backtest, with the better curve fitting ,but the worst OOS results too

That’s why I say “keep it simple”

Bye

sure, keep it simple…. but to say the entry is not important and seeing your backtest results with almost no DD, how can you then say that the entry is not importat?

do as Vonasi then, why even invole indicators? show us that it is possible with pure random entries and get the same results

And as I said and read (These august holidays and last weeks I think I read more than 15 books on Algos … very very interesting ) the more complex algo and the more parameters give the better IS backtest, with the better curve fitting ,but the worst OOS results too

Got some to recommend ? What’s your best one ?

@snucke

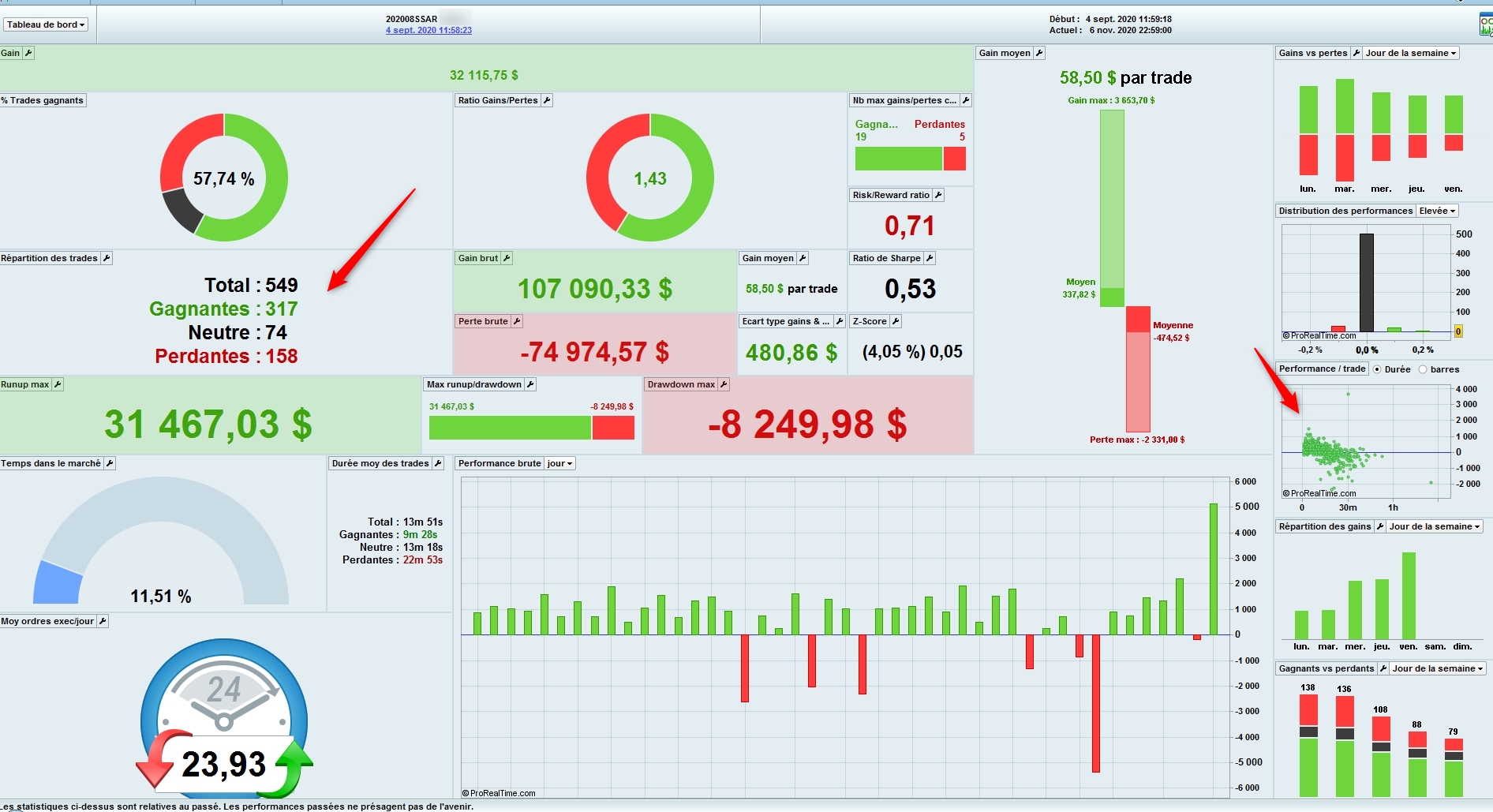

Of course there is a max drawndown (See on the picture). There is always a max drawndown. If not, this is a scam 😉

As I said, saying that entries/signal is the least important thing doesn’t mean we can entry randomly, because it would mean that it’s unuseful

@April O’Neil

There is so many, but I think than books of Chan is a basic to understand the triade Entry/Market structure/Money management

Most of these books say the same things, and of some things we can’t do like Monte Carlo …

https://www.quantstart.com/articles/Top-5-Essential-Beginner-Books-for-Algorithmic-Trading

Bye

As I said, saying that entries/signal is the least important thing doesn’t mean we can entry randomly

An indicator can be curve fitted so eliminate the indicator and you remove the curve fit – unless that is you have proof that an indicator gives an actual benefit. At any moment in time a market can only do two things in the future – go up or go down. It might go up and down a lot or up and down a little – but up or down is what it will do. So we place a bet that it is going to go one way or the other – then we have to decide how much we are willing to guess it will go up or down – that is our target and stop loss. If we are right or wrong we then have to try to use money management to control the amount of our losses or to maximise the amount of our wins. We have to be careful with this because the market does not know or care whether our last guess was right or wrong. Our indicator (or indicators) will be sometimes right and sometimes wrong as much as our guess is going to be right or wrong due to them being based purely on past data which has no idea what tomorrow brings. This means that we should only use an indicator if we have quantified that it actually can help us be right more often than we are wrong. Then once we have proven this we have to prove that its benefits can give our strategy enough of a boost that will overcome spread and slippage.

Hi Guys,

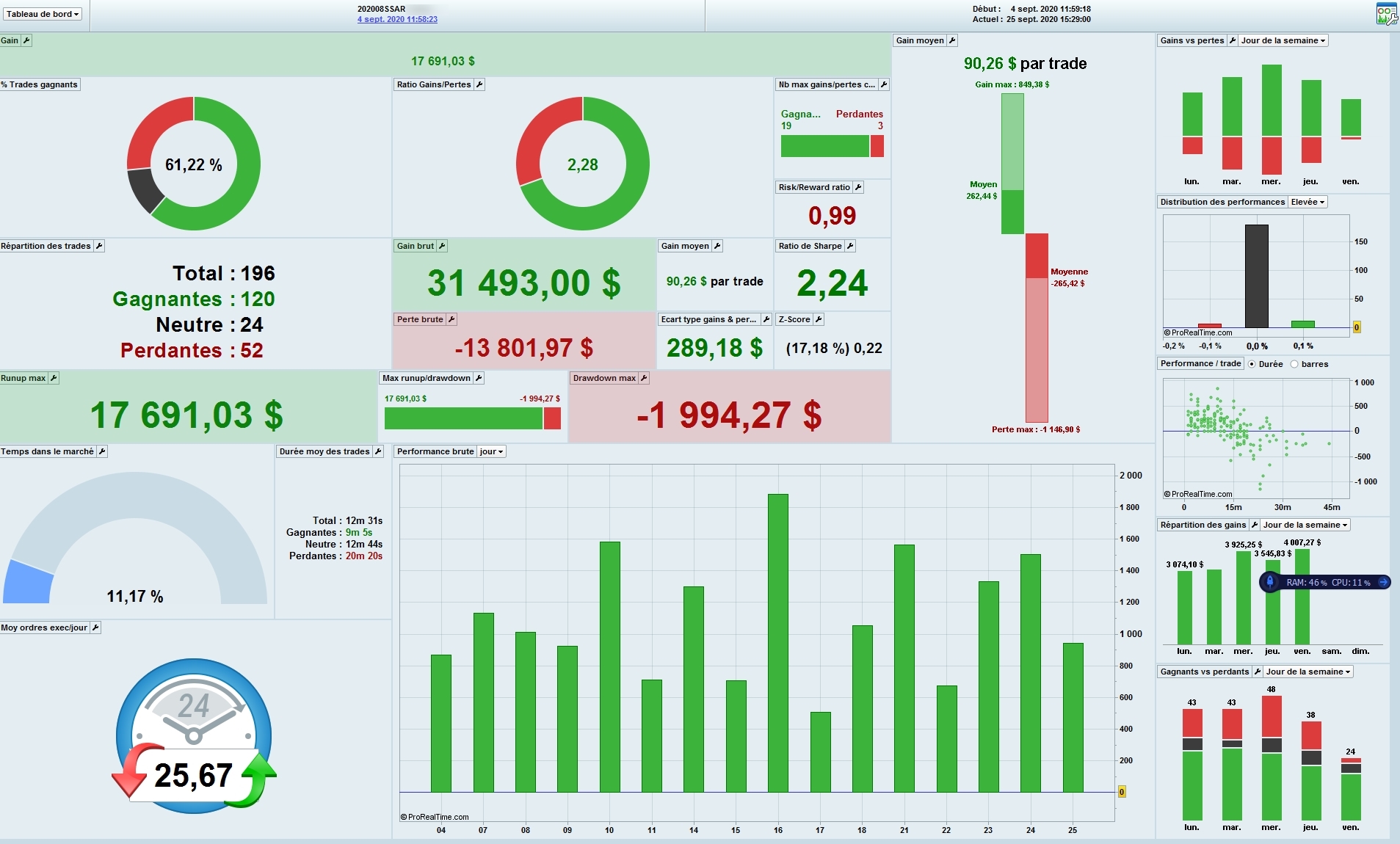

A little update on OOS with this “Donkey” Algo based on SAR after 2 months

As you can see it continues to work well even with 549 trades now. Max drawdown is quite low after 2 months and as you see the majority of tades are closed in the first 30 mn. 11.51 % in time market is quite well

Sharpe ratio is not very good

I changed nothing since 4 september

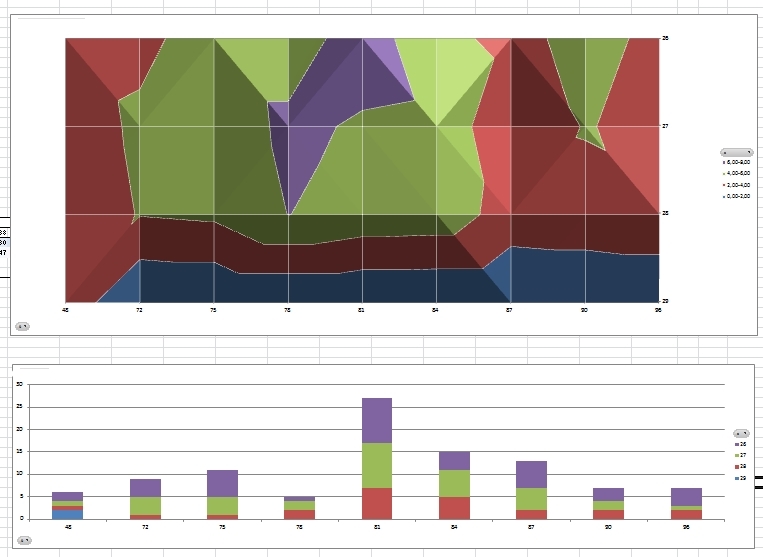

Sorry not a lot of time actually because of a lot of work (I now try to find another way to replace 2D/3D on PRT (Because of lot of problems, failures, erratics results) and better “optimize” (not overfit = I respect all rules I say on previous posts) the correlation on IS/OOS as you can see on last picture)

Have a nice sunday

thanked this post