This strategy is designed to take advantage of new highs and new lows compared to the previous trading day.

Previous trading day on Monday is Friday and the code filters out any weekend data should it be present.

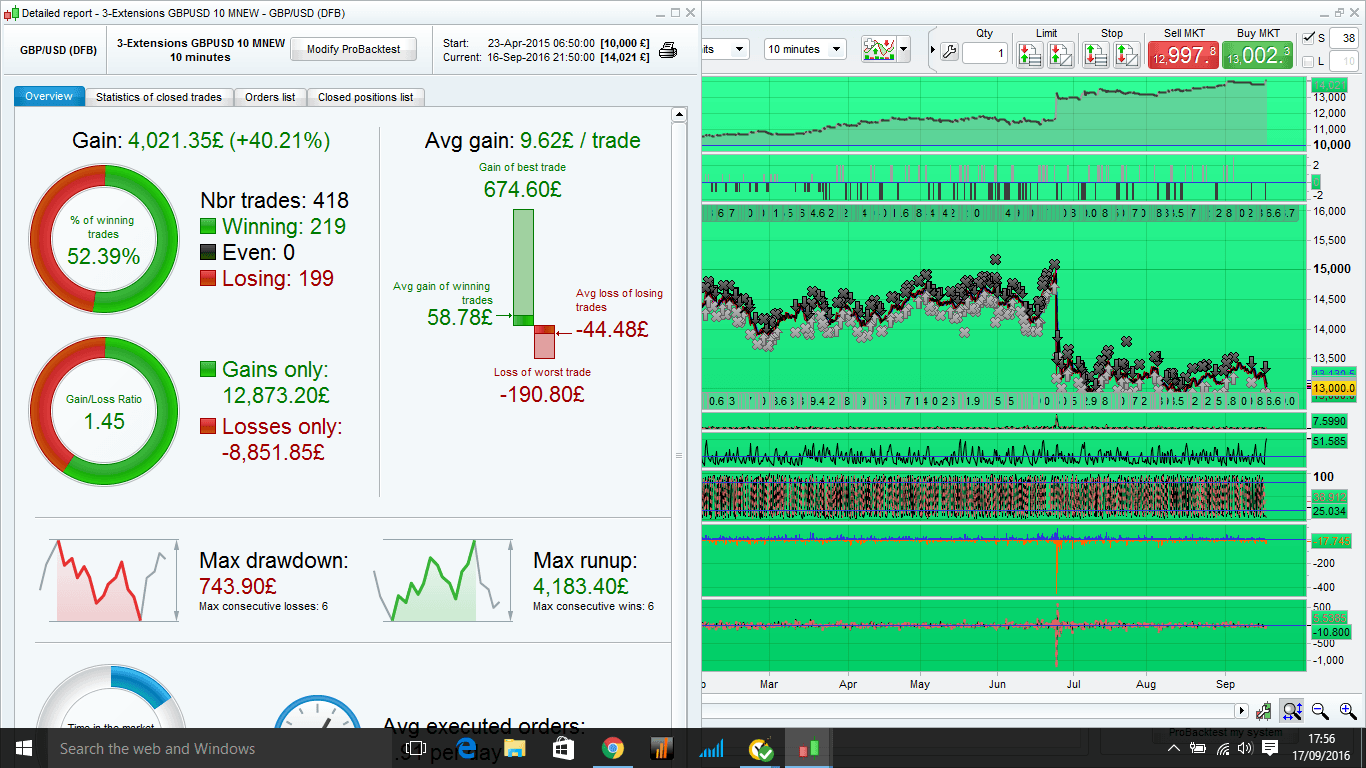

The stops are optimized for GBPUSD in the timeframe tested which was 100000 units between 23rd April and 16th September 2016.

In theory you should be able to adapt to other pairs, or anything, but works best where there is a trend or imbalance between currencies.

Currently the strategy is set up to trade from 001000. Note that I have proved that using 000000 will result in the code picking up the day before yesterday setting to 10 minutes past midnight (uk time) makes the code work as intended but will still be profitable if you use midnight.

The test used a spread of 1.5 points.

Hope this is of some use

// extension JAP change buy price on Mondays for Friday High/Low

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

DEFPARAM FLATBEFORE = 001000

DEFPARAM FLATAFTER = 160000

DEFPARAM PRELOADBARS = 2000

LastEntryTime = 130000

//ignore saturday and Sunday trading TD=Trading Day

if DayOfWeek = 6 OR DayOfWeek = 7 THEN

TD = 0

else

TD = 1

endif

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

// Money Management

Capital = 3530

Risk = 0.01

StopLoss = 30 // VARY TO DETERMINE RISK

//Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

if PositionSize >= 5 Then

PositionSize = 5

endif

//prices to enter trades

if DayOfWeek = 1 Then

BuyPrice = (DHigh(2)+3*PointSize)

SellPrice = (DLow(2)-3*PointSize)

else

BuyPrice = (DHigh(1)+3*PointSize)

SellPrice = (DLow(1)-3*PointSize)

endif

// Conditions to enter long positions

indicator2 = MACD[8,25,3](close)

c2 = (indicator2 > 0)

indicator1 = TD

c1 = (indicator1=1)

IF TIME < LastEntryTime and c1 and c2 THEN

BUY PositionSize CONTRACTS AT BuyPrice STOP

ENDIF

// Conditions to enter short positions

indicator3 = MACD[8,25,3](close)

c3 = (indicator3 < 0)

IF TIME < LastEntryTime and c1 and c3 THEN

SELLSHORT PositionSize CONTRACTS AT SellPrice STOP

ENDIF

//trailing stop

trailingstop = 25

//case SHORT order

trailshort = 40

if shortonmarket then

MINPRICE = MIN(MINPRICE,Low) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailshort*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailshort*pointsize //set the exit price at the MFE + trailing stop price level

endif

if tradeprice(1)-MINPRICE<=trailshort*pointsize then

priceexit = tradeprice+trailshort*pointsize

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,High) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

if MAXPRICE-tradeprice(1)<=trailingstop*pointsize then

priceexit = tradeprice-trailingstop*pointsize// ensures trailing stop is in place mJAP improvement

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif