Hello,

I have the code below for a H1 EURGBP system that I’m backtesting but as you can see from the code, I only want PRT to trade within certain times. On backtesting the system keeps ignoring these times with multiple trades at 00;00,00 (midnight) which is not what I expect the code to allow. These errant trades seem to be after the system has not traded the day before (such as after the weekend). Could anyone ascertain why it is not abiding by the if time= commands?

defparam cumulateorders=false

// --- settings

balance = 10000 //balance of the strategy when activated the first time

minlot = 1 //minimum lot size for the current instrument (example: 1 for DAX)

riskpercent = 2 //risk percent per trade

activationtime = 080000 //Close time of the candle to activate the strategy

LimitHour = 140000 //Time to close off strategy

//choose days of week to trade

if dayofweek=1 then //Monday

daytrading=1

endif

if dayofweek=2 then // Tuesday

daytrading=1

endif

if dayofweek=3 then // Wednesday

daytrading=1

endif

if dayofweek=4 then //Thursday

daytrading=1

endif

if dayofweek=5 then // Friday

daytrading=1

endif

if dayofweek=6 or dayofweek=7 then //Sat and Sun

daytrading=0

endif

// ---

// --- indicators

ema = exponentialaverage[150](close)

ema2 = exponentialaverage[50](close)

//set trend using highs and lows

Trend1= highest[1](high)

Trend2= highest[20](high)

Trend3 = trend2-trend1

///

Trend4= lowest[1](low)

Trend5= lowest[20](low)

Trend6 = trend4-trend5

///

EMAabove = ema2>ema

EMAbelow = ema2<ema

atr = averagetruerange[24]

hh = highest[12](high)

ll = lowest[12](low)

Long = emaabove and trend3 >0

Short = emabelow and trend6 >-1

// ---

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

if time=activationtime and time<limithour then

// case 1 : If price candle touches MA (even wicks) then look at high or low of signal candle

if trend3<0 or trend6<-1 then

case = 1

levelhi = CALL"#floor and ceil"[high,10.0,1]

levello = CALL"#floor and ceil"[low,10.0,-1]

endif

//case 2 : If price is above the MA then only trade long BUT only above the highest high of the past 24 hrs

if long and case = 0 then

case = 2

levelhi = hh[1]

endif

//case 3 : If price is below the MA then only trade short BUT only below the lowest low of the past 24 hrs

if short and case = 0 then

case = 3

levello = ll[1]

endif

endif

if alreadytraded = 0 then

//money management

if case=1 then

StopLoss = 10

else

StopLoss = 10

endif

Risk = riskpercent/100

//calculate contracts

equity = balance + StrategyProfit

maxrisk = round(equity*Risk)

size = max(minlot,abs(round((maxrisk/StopLoss)/PointValue)*pipsize))

//in all cases put pending orders on market

while case <> 0 and daytrading=1 and time <=LimitHour do

if levelhi>0 then

buy size contract at levelhi stop

endif

if levello>0 then

sellshort size contract at levello stop

endif

wend

endif

//set target and profit

if onmarket then

if case = 1 then

set target profit 1*ATR

set stop ploss StopLoss

endif

if case = 2 or case = 3 then

set target profit 1*ATR

set stop ploss StopLoss

endif

endif

currentprofit = strategyprofit

//debugging

//graph case as "case"

//graph time=activationtime coloured(100,120,133) as "activation time!"

graph time

//graph ema

//graph levelhi coloured(0,200,0) as "level high"

//graph levello coloured(200,0,0) as "level low"

//graph size as "mm"

Hi, had a quick look at this, I don’t think your code is doing what you think it is doing:

if time=activationtime and time<limithour then

This will only perform the tests on the following lines at 080000, I think you meant it to be between the 2 times so time >= activationtime and time<limithour?

while case <> 0 and daytrading=1 and time <=LimitHour do

if levelhi>0 then

buy size contract at levelhi stop

This will execute orders at any time before LimitHour including 000000 if it meets the entry criteria

Thanks autostrategist.

I see what you mean for the first command, so the second element is correct further down under //in all cases put pending orders on market

while case <> 0 and daytrading=1 and time <=LimitHour do

So this part of the code should ensure that trades are not activated beyond/past the limitHour set earlier in code?

Autostrategist

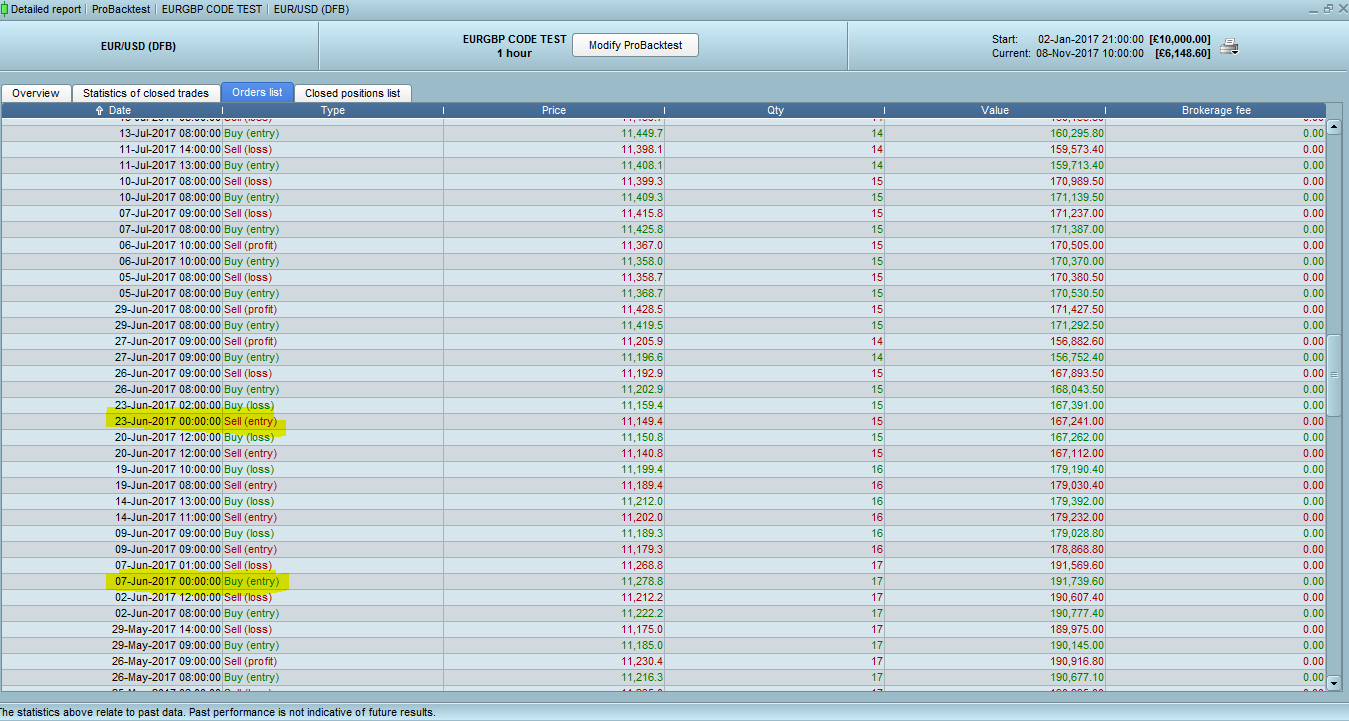

I just tried the above and sadly the system is still taking trades at 00:00.00 (midnight) randomly. Could this be linked to this part of the code?

// ---

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

It seems to take the random midnight trades when the system has not traded the day before? (such as criteria not met, or weekends)?

You need to change this line:

while case <> 0 and daytrading=1 and time <=LimitHour do

to be:

while case <> 0 and daytrading=1 and (time >= activationtime and time <=LimitHour) do

Ahh, brilliant. Thanks AS! That should solve it.

Best wishes