Hi everyone, I hope you are well,

Here is as promised a version 21, it is not exceptional and you will see that on my code there is a lot of redundancy I know it is not the top but for me it suits me for the moment and it allows me not to make mistakes, we will see later to improve the code

I would like to thank all the people who responded and helped me directly or indirectly (@phoentzs , @GraHal , @Nicolas , @PeterSt , @robertogozzi , …. 😊)

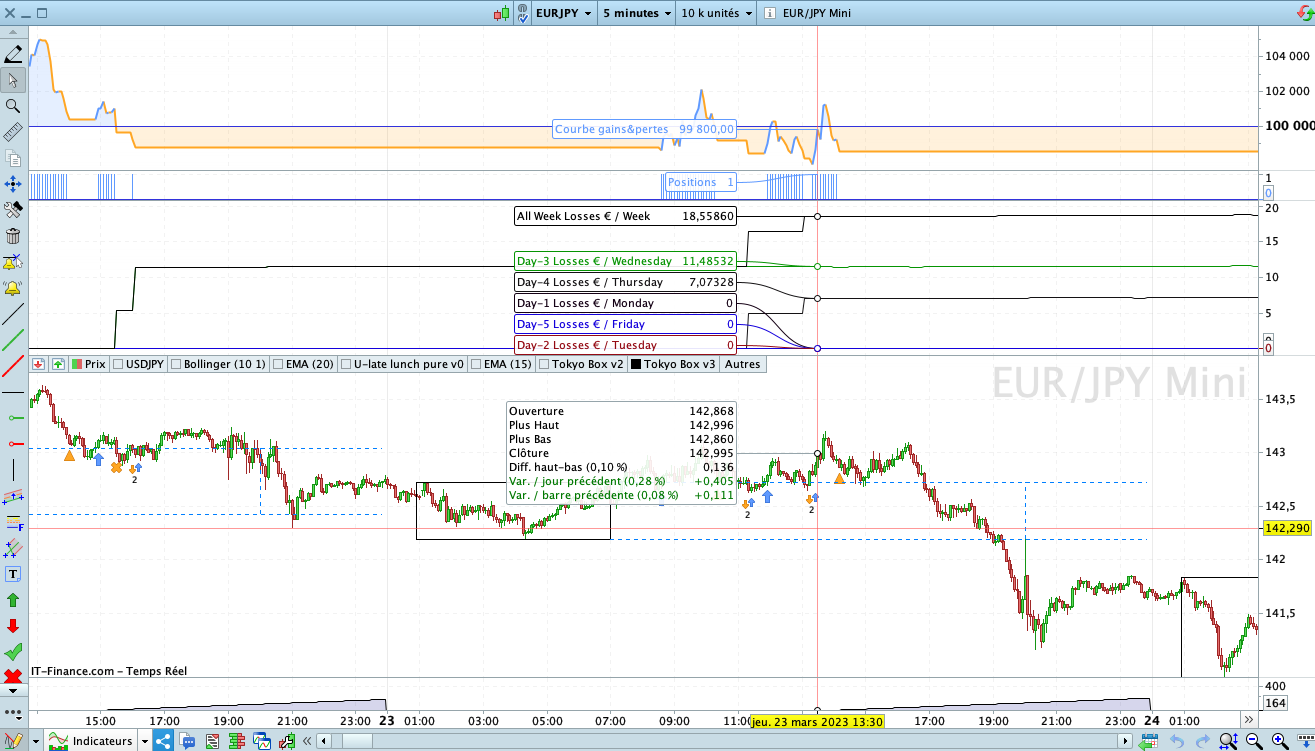

In this code and so I hope it works well anyway I checked several times and it seems to be OK, it’s to calculate the losses generated by the losing trades between 8:05am until 8:05am the next day, so I can count my daily losses and for example put a condition :

– stop buying for the day if I exceed 10€ of loss (C6)

– stop buying for the week if I exceed 40€ of loss (C7)

The next step will be to calculate the losses per month and stop buying if we lose more than 100€.

The other steps will be to calculate the real gain and the latent gain in order to reallocate a part each week for the next week if we are in the positive to allow ourselves to lose more while protecting our realized gains 😊

// Strategy Name : END OF DAY - YEN // Version : 21.0

// Stroks : USD/JPY Mini // indicator associate : Tokyo Box v3

// Time Zone / TF : Paris-France (GTM+2) / M5 // Pip Value : 1 Pip = 100 JPY

// Tokyo Session : 9Am - 3Pm (UTC+9) //

// Spread : 2 //

// Information :

//#******************************************************************#

//# VariableS #

//#******************************************************************#

Once Capital = 100000

Once Equity = Capital

Once TrailinStop = 0 // 1 on - 0 off // Needs to be improved

Once BreakEaven = 1 // 1 on - 0 off

Once BreakRange = 1 // 1 on - 0 off

Once MFE = 0 // 1 on - 0 off // Needs to be improved

Once QuitStrategy = 0 // 1 on - 0 off // Needs to be improved

Once MaxBuyPerDay = 15 // Maximum shares we can buy per day // Z2

Once MaxLostPerDay = 10 // We can buy until we don't lost 10€ per Day // Unit : €

Once MaxLostPerWeek = 40 // We can buy until we don't lost 40€ per week// Unit : €

Once MaxLostPerMonth= 100// Stop Strategy if we Lost 100€ per month // Needs to be improved

Once MaxBuyShare = 10 // Maximum of shares we can buy (Marging math)

Once PercentOfBoxSL = 10 // Percent of Tokyo Box for Initialization the First Stop Loss

Once N = 1 // Buy N Shares

Once Spread = 2 // Spread fees x 2

MedianPriceJPY = Average[10](MedianPrice)

FranceDST = Month=4 OR Month=5 OR Month=6 OR Month=7 OR Month=8 OR Month=9 OR (Month=9 AND Day < 24) // Z5

FranceWinTime = Month=11 OR Month=12 OR Month=1 OR Month=2 OR (Month=3 AND Day < 24) // Z5

IF (DayOfWeek = 1 AND Time > 080500) THEN

MyMondayPeriod = 1

MyFridayPeriod = 0

ENDIF

IF (DayOfWeek = 2 AND Time > 080500) THEN

MyMondayPeriod = 0

MyTuesdayPeriod = 1

ENDIF

IF (DayOfWeek = 3 AND Time > 080500) THEN

MyTuesdayPeriod = 0

MyWednesdayPeriod = 1

ENDIF

IF (DayOfWeek = 4 AND Time > 080500) THEN

MyWednesdayPeriod = 0

MyThursdayPeriod = 1

ENDIF

IF (DayOfWeek = 5 AND Time > 080500) THEN

MyThursdayPeriod = 0

MyFridayPeriod = 1

ENDIF

//#******************************************************************#

//# FonctionS #

//#******************************************************************#

IF FranceDST THEN

EndOfBoxTime = 080500

BeginBoxTime = 020000

ELSIF FranceWinTime THEN

EndOfBoxTime = 070000

BeginBoxTime = 010000

ENDIF

IF Time = EndOfBoxTime THEN

x2 = BarIndex[0]

x1 = BarIndex[73]

yH = Highest[72](High[1])

yL = Lowest [72](Low[1])

os = 4*pipsize

DayRange = (yH - yL) / pipsize

ENDIF

IF NOT OnMarket THEN // Dc

FirstSL = 0

NotOnMArket = 1

ENDIF

//#******************************************************************#

//# Money Management #

//#******************************************************************#

IF Time = 080500 THEN // Ec // #97

LastDayCountOfPosition = CountOfPosition

Flag = 1

ENDIF

MoreMathFlag = LastDayCountOfPosition>0 AND Not OnMArket AND OnMarket[1] AND Flag=1

IF MoreMathFlag THEN // #97

TodayStrategyProfit = StrategyProfit

CountOfMyPosition = CountOfPosition[1] - LastDayCountOfPosition

LastEntryPrice = TradePrice(CountOfPosition[1]+1)

LastExitPrice = TradePrice

DiffEntryExitJPY = (((LastEntryPrice - LastExitPrice )/Pipsize)*PointValue)*CountOfMyPosition

Flag = 0

ENDIF

IF MyMondayPeriod THEN

if LastDayCountOfPosition > 0 AND StrategyProfit <> StrategyProfit[1] then

MondayLossesJPY = DiffEntryExitJPY

DiffEntryExitJPY = 0

LastDayCountOfPosition = 0

MondayLosingTrades = MondayLosingTrades + 1

endif

if StrategyProfit < StrategyProfit[1] AND LastDayCountOfPosition = 0 then

MondayLossesJPY = MondayLossesJPY + (StrategyProfit[1] - StrategyProfit)

MondayLosingTrades = MondayLosingTrades + 1

endif

ENDIF

IF MyTuesdayPeriod THEN

if LastDayCountOfPosition > 0 AND StrategyProfit <> StrategyProfit[1] then

TuesdayLossesJPY = DiffEntryExitJPY

DiffEntryExitJPY = 0

LastDayCountOfPosition = 0

TuesdayLosingTrades = TuesdayLosingTrades + 1

endif

if StrategyProfit < StrategyProfit[1] AND LastDayCountOfPosition = 0 then

TuesdayLossesJPY = TuesdayLossesJPY + (StrategyProfit[1] - StrategyProfit)

TuesdayLosingTrades = TuesdayLosingTrades + 1

endif

ENDIF

IF MyWednesdayPeriod THEN

if LastDayCountOfPosition > 0 AND StrategyProfit <> StrategyProfit[1] then

WednesdayLossesJPY = DiffEntryExitJPY

DiffEntryExitJPY = 0

LastDayCountOfPosition = 0

WednesdayLosingTrades = WednesdayLosingTrades + 1

endif

if StrategyProfit < StrategyProfit[1] AND LastDayCountOfPosition = 0 then

WednesdayLossesJPY = WednesdayLossesJPY + (StrategyProfit[1] - StrategyProfit)

WednesdayLosingTrades = WednesdayLosingTrades + 1

endif

ENDIF

IF MyThursdayPeriod THEN

if LastDayCountOfPosition > 0 AND StrategyProfit <> StrategyProfit[1] then

ThursdayLossesJPY = DiffEntryExitJPY

DiffEntryExitJPY = 0

LastDayCountOfPosition = 0

ThursdayLosingTrades = ThursdayLosingTrades + 1

endif

if StrategyProfit < StrategyProfit[1] AND LastDayCountOfPosition = 0 then

ThursdayLossesJPY = ThursdayLossesJPY + (StrategyProfit[1] - StrategyProfit)

ThursdayLosingTrades = ThursdayLosingTrades + 1

endif

ENDIF

IF MyFridayPeriod THEN

if LastDayCountOfPosition > 0 AND StrategyProfit <> StrategyProfit[1] then

FridayLossesJPY = DiffEntryExitJPY

DiffEntryExitJPY = 0

LastDayCountOfPosition = 0

FridayLosingTrades = FridayLosingTrades + 1

endif

if StrategyProfit < StrategyProfit[1] AND LastDayCountOfPosition = 0 then

FridayLossesJPY = FridayLossesJPY + (StrategyProfit[1] - StrategyProfit)

FridayLosingTrades = FridayLosingTrades + 1

endif

ENDIF

MondayLossesEuro = MondayLossesJPY / MedianPriceJPY

TuesdayLossesEuro = TuesdayLossesJPY / MedianPriceJPY

WednesdayLossesEuro = WednesdayLossesJPY / MedianPriceJPY

ThursdayLossesEuro = ThursdayLossesJPY / MedianPriceJPY

FridayLossesEuro = FridayLossesJPY / MedianPriceJPY

WeekLossesJPY = MondayLossesJPY + TuesdayLossesJPY + WednesdayLossesJPY + ThursdayLossesJPY + FridayLossesJPY // Pc

WeekLossesEuro = WeekLossesJPY/ MedianPriceJPY

WeekLosingTrades = MondayLosingTrades+TuesdayLosingTrades+WednesdayLosingTrades+ThursdayLosingTrades+FridayLosingTrades

IF MyMondayPeriod THEN

DayLossesEuro = MondayLossesEuro

ENDIF

IF MyTuesdayPeriod THEN

DayLossesEuro = TuesdayLossesEuro

ENDIF

IF MyWednesdayPeriod THEN

DayLossesEuro = WednesdayLossesEuro

ENDIF

IF MyThursdayPeriod THEN

DayLossesEuro = ThursdayLossesEuro

ENDIF

IF MyFridayPeriod THEN

DayLossesEuro = FridayLossesEuro

ENDIF

IF DayOfWeek = 0 THEN

MondayLossesJPY = 0

TuesdayLossesJPY = 0

WednesdayLossesJPY = 0

ThursdayLossesJPY = 0

FridayLossesJPY = 0

MondayLosingTrades = 0

TuesdayLosingTrades = 0

WednesdayLosingTrades = 0

ThursdayLosingTrades = 0

FridayLosingTrades = 0

WeekLosingTrades = 0

ENDIF

//#******************************************************************#

//# Long Condition Signals #

//#******************************************************************#

TradingTimeCondition = (Time >= 080500 AND Time <= 200000 AND DayOfWeek < 5) OR (Time >= 080500 AND Time < 170000 AND DayOfWeek = 5) // Tc

C1 = TradingTimeCondition

LongSignal = Close Crosses Over yH

C2 = LongSignal

IF LongSignal Then // Lc

FirstSL = yH - (((yH-yL)/100)*PercentOfBoxSL) // Hc

LastFirstSL = FirstSL

ENDIF

IF Time = 080500 AND CountOfPOsition >= 1 THEN // Condition to force the first purchase even if we are in position since yesterday

NotOnMArket = 1

ENDIF

C3 = NotOnMArket

C4 = CountOfPurchase < MaxBuyPerDay

C5 = CountOfLongShares < MaxBuyShare

DayLostCondition = DayLossesEuro < MaxLostPerDay // Jc & Z7

C6 = DayLostCondition

WeekLostCondition = WeekLossesEuro < MaxLostPerWeek // Qc

C7 = WeekLostCondition

LongSignalAllCondition = C1 AND C2 AND C3 AND C4 AND C5 AND C6 AND C7

IF LongSignalAllCondition THEN

Buy N Contract AT Market

SET STOP PRICE FirstSL

ENDIF

IF LongSignalAllCondition [1] AND NotOnMArket[1] AND CountOfPosition > 0 THEN // can be improved ?

NotOnMArket = 0

ENDIF

IF (OnMarket AND Not OnMarket[1]) OR (ABS(CountOfPosition) > ABS(CountOfPosition[1])) THEN // Wc // // can be improved ?

CountOfPurchase = CountOfPurchase + 1

ENDIF

//#******************************************************************#

//# Trailing & BreakEven & Range Stop Loss & MFE #

//#******************************************************************#

Once trailingstart = 140 // Trailing start after X pips profit

Once trailingstep = 10 // Trailing step to move the "stoploss"

Once StartBERatio = 5 // BE Start for the hole position when the RR(FirstSL) = 5

Once StartBreakRangePercent = 20 // Close > Last entry + 20% of the Tokyo Box

Once PointsToKeep = 2*Spread // Spread to add to BE price

Once TRAILINGMFE = 20 // Trailing stop with the Max Favorable Excursion

// Trailing

if TrailinStop > 0 then // Needs to be improved

IF NOT ONMARKET THEN

NewSL=0

ENDIF

IF LONGONMARKET THEN

// Trailing Start

IF NewSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

NewSL = tradeprice(1)+trailingstep*pipsize

ENDIF

// Trailing Step Move

IF NewSL>0 AND close-NewSL>=trailingstep*pipsize THEN

NewSL = NewSL+trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF NewSL>0 THEN

SELL AT NewSL STOP

ENDIF

endif

// Range Stop Loss

if BreakRange > 0 then // Fc

IF Not OnMarket THEN

BreakRangeLevel = 0

ENDIF

IF LongOnMarket THEN

BreakRangeMath = TradePrice + (((yH-yL)/100)*StartBreakRangePercent)

ENDIF

IF LongOnMarket AND Close Crosses Over BreakRangeMath THEN // Z1

BreakRangeLevel = yH - 2*Pipsize // Gc

//FirstSL = 0

ENDIF

IF BreakRangeLevel > 0 THEN //Z8

SELL AT BreakRangeLevel STOP

ENDIF

endif

// BreakEven Stop Loss

if BreakEaven>0 then

IF Not OnMarket THEN

BreakEvenLevel = 0

ENDIF

yHplusFirstSL = yH + (StartBERatio*(yH-LastFirstSL))

IF LongOnMarket AND Close Crosses Over yHplusFirstSL THEN

BreakEvenLevel = TradePrice + PointsToKeep*pipsize

ENDIF

IF BreakEvenLevel > 0 THEN

SELL AT BreakEvenLevel STOP

ENDIF

endif

if MFE > 0 then // Needs to be improved

if not onmarket then

MAXPRICEMFE = 0

MINPRICEMFE = close

priceexitMFE = 0

endif

if longonmarket then

MAXPRICEMFE = MAX(MAXPRICEMFE,close) //saving the MFE of the current trade

if MAXPRICEMFE-tradeprice(1)>=TRAILINGMFE*pointsize then //if the MFE is higher than the trailingstop then

priceexitMFE = MAXPRICEMFE-TRAILINGMFE*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

if onmarket and priceexitMFE>0 then

SELL AT priceexitMFE STOP

endif

endif

//#******************************************************************#

//# Graph #

//#******************************************************************#

// Blue Azur (0, 127, 255) & Maya (115, 194, 251)

// Green Sinople (20, 148, 20) &

IF 0 THEN

Graph MyMondayPeriod AS "My Monday Period" Coloured (20, 0, 20)

Graph MyTuesdayPeriod AS "My Tuesday Period" Coloured (148, 10, 20)

Graph MyWednesdayPeriod AS "My Wednesday Period" Coloured (5, 148, 2)

Graph MyThursdayPeriod AS "My Thursday Period" Coloured (20, 18, 20)

Graph MyFridayPeriod AS "My Friday Period" Coloured (20, 0, 220)

ENDIF

IF 0 THEN

Graph MondayLossesJPY AS "Day-1 Losses ¥ / Monday" Coloured (20, 0, 20)

Graph TuesdayLossesJPY AS "Day-2 Losses ¥ / Tuesday" Coloured (148, 10, 20)

Graph WednesdayLossesJPY AS "Day-3 Losses ¥ / Wednesday" Coloured (5, 148, 2)

Graph ThursdayLossesJPY AS "Day-4 Losses ¥ / Thursday" Coloured (20, 18, 20)

Graph FridayLossesJPY AS "Day-5 Losses ¥ / Friday" Coloured (20, 0, 220)

Graph WeekLossesJPY AS "All Week Losses ¥ / Week"

ENDIF

IF 1 THEN

Graph MondayLossesEuro AS "Day-1 Losses € / Monday" Coloured (20, 0, 20)

Graph TuesdayLossesEuro AS "Day-2 Losses € / Tuesday" Coloured (148, 10, 20)

Graph WednesdayLossesEuro AS "Day-3 Losses € / Wednesday" Coloured (5, 148, 2)

Graph ThursdayLossesEuro AS "Day-4 Losses € / Thursday" Coloured (20, 18, 20)

Graph FridayLossesEuro AS "Day-5 Losses € / Friday" Coloured (20, 0, 220)

Graph WeekLossesEuro AS "All Week Losses € / Week"

ENDIF

IF 0 THEN

Graph MondayLosingTrades Coloured (20, 0, 20)

Graph TuesdayLosingTrades Coloured (148, 10, 20)

Graph WednesdayLosingTrades Coloured (5, 148, 2)

Graph ThursdayLosingTrades Coloured (20, 18, 20)

Graph FridayLosingTrades Coloured (20, 0, 220)

Graph WeekLosingTrades

ENDIF

//#******************************************************************#

//# Stop Strategy #

//#******************************************************************#

if QuitStrategy then

IF 1 THEN // Nc & Z9

if (StrategyProfit / MedianPrice) < MaxLostPerMonth*(-1) then

Quit

endif

ENDIF

IF 0 Then // Needs to be improved

MaxDrawDownPercentage = 10 // Max DrawDown of x%

Equity = Capital + StrategyProfit

HighestEquity = Max (HighestEquity,Equity) // Save the Maximum Equity we got

MaxDrawdown = HighestEquity * (MaxDrawDownPercentage/100)

ExitFromMarketCond = Equity <= HighestEquity - MaxDrawdown

IF ExitFromMarketCond Then

Quit

ENDIF

ENDIF

endif

//#******************************************************************#

//# Hello ToTo #

//#******************************************************************#

// _ _ _ _ _______ _______

// | | | | | | | |__ __|__ __|

// | |__| | ___| | | ___ | | ___ | | ___

// | __ |/ _ \ | |/ _ \ | |/ _ \| |/ _ \

// | | | | __/ | | (_) | | | (_) | | (_) |

// |_| |_|\___|_|_|\___/ |_|\___/|_|\___/

// GMT : 00H ================== 6H / UTC

// Tokyo : 09H ================== 15H / UTC + 9 / JST (Japan Standard Time)

// Paris : 02H ================== 8H / UTC + 2 / DST (Daylight Saving Time)

// Paris : 01H ================== 7H / UTC + 1 / Winter

// London : 01H ================== 7H / UTC + 1 / DST (Daylight Saving Time)

// London : 00H ================== 6H / UTC + 0 / Winter