Thanks Grahal, I’ll play around with it, load a bunch of variations in demo and see if anything sticks.

@Monochrome or anybody … are you still using the Algo below?

I am getting a ‘negative paramater error message’ (new one from IG?? 🙁 ) anybody got a fix please?

Dj-3min-Dynsuper-v1.2.itf

Here’s the code if anybody can spot the source of the negative parameter please?

//-------------------------------------------------------------------------

// Main code : Dj-3min Dyn/super v1.2

//-------------------------------------------------------------------------

defparam cumulateorders = false

//defparam preloadbars = 10000

DEFPARAM FLATBEFORE = 233000

DEFPARAM FLATAFTER = 210000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

once positionsize = 0.2

//DYNAMIC ZONE ELASTICITY///----/////

once period = 200

once smoothing = 2

once smoothing = max(1, smoothing+1)

once period = max(1, Period)

// Coeficient, change if required

once coef = 0.8

// Signal line

x = std[Period](close)

signam = 1 + (-1* ( ((average[period](close) + (x*2)) - close) / x ) / 2)

// Dynamic Zones

sq = square(signam)

mean = average[period](signam)

vsqrt = sqrt( average[period](sq) - square(mean) )

top = mean + coef * vsqrt

btm = mean - coef * vsqrt

result = average[smoothing](signam)

//DYNAMIC ZONE ELASTICITY///----/////

once period2 = 20

once smoothing2 = 2

once smoothing2 = max(1, smoothing2+1)

once period2 = max(1, Period2)

// Coeficient, change if required

once coef2 = 0.8

// Signal line

x2 = std[Period2](close)

signam2 = 1 + (-1* ( ((average[period2](close) + (x2*2)) - close) / x2 ) / 2)

// Dynamic Zones

sq2 = square(signam2)

mean2 = average[period2](signam2)

vsqrt2 = sqrt( average[period2](sq2) - square(mean2) )

top2 = mean2 + coef2 * vsqrt2

btm2 = mean2 - coef2 * vsqrt2

result2 = average[smoothing2](signam2)

////DYNAMIC ZONE ELASTICITY///----/////

once period4 = 40

once smoothing4 = 2

once smoothing4 = max(1, smoothing4+1)

once period4 = max(1, Period4)

// Coeficient, change if required

once coef4 = 0.8

// Signal line

x4 = std[Period4](close)

signam4 = 1 + (-1* ( ((average[period4](close) + (x4*2)) - close) / x4 ) / 2)

// Dynamic Zones

sq4 = square(signam4)

mean4 = average[period4](signam4)

vsqrt4 = sqrt( average[period4](sq4) - square(mean4) )

top4 = mean4 + coef4 * vsqrt4

btm4 = mean4 - coef4 * vsqrt4

result4 = average[smoothing4](signam4)

////DYNAMIC ZONE ELASTICITY///----/////

once periodx = 80

once smoothingx = 2

once smoothingx = max(1, smoothingx+1)

once periodx = max(1, Periodx)

// Coeficient, change if required

once coefx = 0.8

// Signal line

xx = std[Periodx](close)

signamx = 1 + (-1* ( ((average[periodx](close) + (xx*2)) - close) / xx ) / 2)

// Dynamic Zones

sqx = square(signamx)

meanx = average[periodx](signamx)

vsqrtx = sqrt( average[periodx](sqx) - square(meanx) )

topx = meanx + coefx * vsqrtx

btmx = meanx - coefx * vsqrtx

resultx = average[smoothingx](signamx)

//bollinger////

//bollup = BollingerUp[20](close)

//bolldown = BollingerDown[20](close)

//bollbuy = close< bollup

//bollsell = close > bolldown

//buyboll = bollbuy

//sellboll = bollsell

//STOCHRSI///

//lengthRSI = 5//14 //RSI period

//lengthStoch = 5//14 //Stochastic period

//myRSI = RSI[lengthRSI](close)

//MinRSI = lowest[lengthStoch](myrsi)

//MaxRSI = highest[lengthStoch](myrsi)

//StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)*100

////////////////

//min1stochbuy = stochrsi =>90

//min1stochsell = stochrsi =<10

//timeframe (2 minutes,UPDATEONCLOSE)

////DYNAMIC ZONE ELASTICITY///----/////

//period4 = 20

//smoothing4 = 2

//once smoothing4 = max(1, smoothing4+1)

//once period4 = max(1, Period4)

//// Coeficient, change if required

//once coef4 = 0.8

//// Signal line

//x4 = std[Period4](close)

//signam4 = 1 + (-1* ( ((average[period4](close) + (x4*2)) - close) / x4 ) / 2)

//// Dynamic Zones

//sq4 = square(signam4)

//mean4 = average[period4](signam4)

//vsqrt4 = sqrt( average[period4](sq4) - square(mean4) )

//top4 = mean4 + coef4 * vsqrt4

//btm4 = mean4 - coef4 * vsqrt4

//result4 = average[smoothing4](signam4)

////////////////////

IF RESULT CROSSES UNDER BTM THEN

SNAP = BARINDEX

ENDIF

IF RESULT CROSSES OVER BTM THEN

SNAP = 0

ENDIF

IF RESULT < BTM THEN

H1 = LOWEST[BARINDEX-SNAP](RESULT)

ELSE

H1 = 0

ENDIF

IF RESULT < BTM THEN

H1A = RESULT > H1

ELSE

H1A = 0

ENDIF

IF RESULT CROSSES OVER TOP THEN

SNAP1 = BARINDEX

ENDIF

IF RESULT CROSSES UNDER TOP THEN

SNAP1 = 0

ENDIF

IF RESULT > TOP THEN

H2 = HIGHEST[BARINDEX-SNAP1](RESULT)

ELSE

H2 = 0

ENDIF

IF RESULT > TOP THEN

H2A = RESULT < H2

ELSE

H2A = 0

ENDIF

//IF RESULT < BTM AND RESULT > H1 THEN

//DONTBUY = 1

//ELSE

//DONTBUY = 0

//ENDIF

if result2 crosses over btm2 then

testbuysignal2 = 1

testsellsignal2 = 0

endif

if result2 crosses under top2 then

testsellsignal2 = 1

testbuysignal2 = 0

endif

if testsellsignal2 = 1 and result2 crosses over top2 then

testbuysignal2 = 1

testsellsignal2 = 0

endif

if testbuysignal2 = 1 and result2 crosses under btm2 then

testbuysignal2 = 0

testsellsignal2 = 1

endif

if result4 crosses over btm4 then

testbuysignal4 = 1

testsellsignal4 = 0

endif

if result4 crosses under top4 then

testsellsignal4 = 1

testbuysignal4 = 0

endif

if testsellsignal4 = 1 and result4 crosses over top4 then

testbuysignal4 = 1

testsellsignal4 = 0

endif

if testbuysignal4 = 1 and result4 crosses under btm4 then

testbuysignal4 = 0

testsellsignal4 = 1

endif

if resultX crosses over btmx then

testbuysignal4x = 1

testsellsignal4x = 0

endif

if resultx crosses under topx then

testsellsignal4x = 1

testbuysignal4x = 0

endif

if testsellsignal4x = 1 and resultx crosses over topx then

testsellsignal4x = 0

testbuysignal4x = 1

endif

if testbuysignal4x = 1 and resultx crosses under btmx then

testbuysignal4x = 0

testsellsignal4x = 1

endif

//HAV1 = TESTBUYSIGNAL2 = 1 AND TESTBUYSIGNAL4 = 1 AND TESTBUYSIGNAL4X = 1

//HAV2 = RESULT > RESULT[1]

//HAV3 = HAV1 AND HAV2

IF RESULT CROSSES UNDER TOP THEN

SIGNAL1 = 1

SIGNAL2 = 0

ENDIF

IF RESULT CROSSES OVER BTM THEN

SIGNAL2 = 1

SIGNAL1 = 0

ENDIF

IF RESULT CROSSES OVER TOP THEN

SIGNAL1 = 0

SIGNAL2 = 1

ENDIF

IF RESULT CROSSES UNDER BTM THEN

SIGNAL2 = 0

SIGNAL1 = 1

ENDIF

if signal2 = 1 and result crosses under btm then

signal2 = 0

signal1 = 1

endif

if signal1 = 1 and result crosses over top then

signal1 = 0

signal2 = 1

endif

if signal1 = 1 and result crosses over mean then

signal2 = 1

signal1 = 0

endif

if signal2 = 1 and result crosses under mean then

signal1 = 1

signal2 = 0

endif

//graph signal1

//graph signal2

C1B = RESULT2 CROSSES OVER BTM2 //AND testbuysignal4 = 1

C1S = RESULT2 CROSSES UNDER TOP2 //AND testsellsignal4 = 1

C2B = RESULT4 CROSSES OVER BTM4 //AND testbuysignal4x = 1

C2S = RESULT4 CROSSES UNDER TOP4 //AND testsellsignal4X = 1

C3B = RESULTX CROSSES OVER BTMX

C3S = RESULTX CROSSES UNDER TOPX

/// === CAN ADD MORE PERIODS

timeframe (15 minutes)

//SUPERTREND//

super15 = Supertrend[1,10]

super25 = SUPERTREND[2,11]

super35 = SUPERTREND[3,12]

//ATRSTOP = AverageTrueRange[14](close)

//ATRSTOP1 = ATRSTOP*AA

timeframe (default)

//SUPERTREND//

super1 = Supertrend[1,10]

super2 = SUPERTREND[2,11]

super3 = SUPERTREND[3,12]

superbuy = close> super1 and close>super2 and close>super3

supersell = close<super1 and close<super2 and close<super3

superbuy15 = close> super15 and close>super25 and close>super35

supersell15 = close<super15 and close<super25 and close<super35

//testsuper1 = close > super1

//testsuper2 = close< super1

superbuyx = superbuy and superbuy15

supersellx = supersell and supersell15

abc1 = signal2 = 1 and not h2a

abc2 = c1b or c2b

abc3 = abc2 or c3b

b1 = abc1 and abc3 AND CLOSE>SUPER3 AND not supersellx

asc1 = signal1 = 1 and not h1a

asc2 = c1s or c2s

asc3 = asc2 or c3s

s1 = asc1 and asc3 AND CLOSE<SUPER3 AND not superbuyx

testsuperbuy = b1 and supersell

testsupersell = s1 and superbuy

//graph testsuperbuy

//graph testsupersell

//graph c1b

//graph c2b

//graph c3b

//graph c1s

//graph c2s

//graph c3s

//b1 = (SIGNAL2 = 1 AND (C1B OR C2B )) AND NOT H2A

//s1 = (SIGNAL1 = 1 AND (C1S OR C2S )) AND NOT H1A

//GRAPH testsellsignal4

//GRAPH C2B

//GRAPH C1B

//

//GRAPH RESULT4

////GRAPH TOP

//GRAPH BTM4

////GRAPH SIGNAL1

////GRAPH SIGNAL2

////GRAPH B1

////GRAPH S1

//SET STOP LOSS SATR*AverageTrueRange[NATR](close)

//SET TARGET PROFIT PATR*AverageTrueRange[NATR](close)

if b1 and not daysForbiddenEntry then

buy POSITIONSIZE contract at market

//SET STOP LOSS 3*AverageTrueRange[14](close)

//SET TARGET PROFIT 1*AverageTrueRange[14](close)

set stop %loss 0.2//ATRSTOP1

//set target %profit 0.8

endif

if s1 and not daysForbiddenEntry then

sellshort POSITIONSIZE contract at market

//SET STOP LOSS 3*AverageTrueRange[14](close)

//SET TARGET PROFIT 2*AverageTrueRange[14](close)

set stop %loss 0.2 //ATRSTOP1

//set target %profit 0.8

endif

IF LONGONMARKET AND CLOSE crosses under SUPER3 THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND CLOSE crosses over SUPER3 THEN

EXITSHORT AT MARKET

ENDIF

//IF LONGONMARKET AND SIGNAL1 = 1 AND TESTSELLSIGNAL2 = 1 AND CLOSE < SUPER1 THEN

//SELL AT MARKET

//ENDIF

//IF SHORTONMARKET AND SIGNAL2 = 1 AND TESTBUYSIGNAL2 = 1 AND CLOSE> SUPER1 THEN

//EXITSHORT AT MARKET

//ENDIF

//BREAKEVEN///

//if not onmarket then

//atrtest = AverageTrueRange[14](close[0])

//endif

//

//startBreakeven = atrtest

//PointsToKeep = 5

//

//IF NOT ONMARKET THEN

//breakevenLevel=0

//ENDIF

//

//IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

//ENDIF

//IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

//ENDIF

//if not superbuy then

//IF breakevenLevel>0 THEN

//SELL AT breakevenLevel STOP

//ENDIF

//endif

//if not supersell then

//IF breakevenLevel>0 THEN

//EXITSHORT AT breakevenLevel STOP

//ENDIF

//endif

//closesuper = close crosses under super1

//closesuper1 = close crosses under super2

//closesuper2 = close crosses under super3

//

//closesuper3 = close crosses over super1

//closesuper4 = close crosses over super2

//closesuper5 = close crosses over super3

//

//

//

//close1 = closesuper or closesuper1

//close2 = close1 or closesuper2

//

//close3 = closesuper3 or closesuper4

//close4 = close3 or closesuper5

//

//if longonmarket and positionperf<0.1 and close2 then

//sell at market

//endif

//

//if longonmarket and positionperf<0.1 and close4 then

//exitshort at market

//endif

//if longonmarket and result crosses under btm then

//sell at market

//endif

//if shortonmarket and result crosses over top then

//exitshort at market

//endif

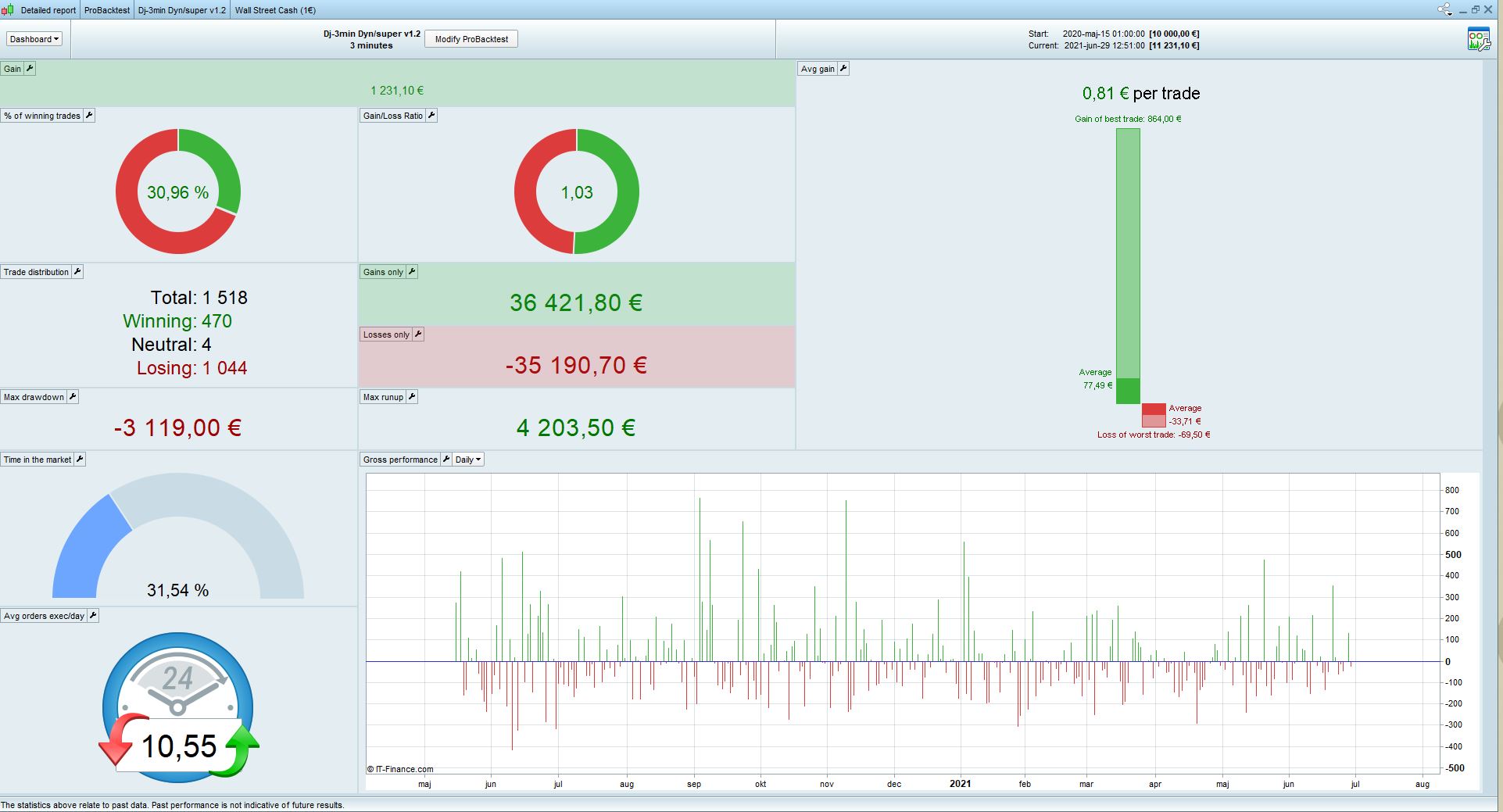

Do u find this algo intressting? Look at attached backtest

Funny you should ask, after my post above, I give it a critical eye and I ditched it in favour of trying None’s version from higher up this thread.

I use Algos different than most anyway … if a trade goes into early profit, I then monitor progress and exit manually at some point, rarely leaving any Algo to exit all on it’s own! 🙂

Try this at line 149:

H2 = HIGHEST[max(1,BARINDEX-SNAP1)](RESULT)

and this at line 132:

H1 = LOWEST[max(1,BARINDEX-SNAP)](RESULT)

Funny you should ask, after my post above, I give it a critical eye and I ditched it in favour of trying None’s version from higher up this thread.

Hey Grahal, thanks for reminding me about this one – could be worth another look. Here’s an fresh take on it, backtest looks good, but unfortunately when I loaded it up got the dreaded div/0 rejection almost immediately.

There’s nothing out of the ordinary apart from the DZE code, and the only division there is x.

I’ve tried fixing this at lines 61,62 but it doesn’t help.

If anyone has a better way of stopping x from ever being zero I’d love to hear it

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 10000

positionsize = 0.5

Ctime = time >=143000 and time <210000

once tradetype = 1 // [1] long/short [2]long [3]short

TIMEFRAME(10 minute)

mx = average[a,t](typicalprice)

c11 = mx > mx[1]

mx1 = average[p3,t](typicalprice)

c12 = mx1 < mx1[1]

indicator2 = SuperTrend[m2,n2]

indicator2a = SAR[q1,w1,e1]

c13 = (close > indicator2) or (close > indicator2a)

c14 = (close < indicator2) or (close < indicator2a)

TIMEFRAME(5 minute)

indicator1 = SuperTrend[m,n]

indicator1a = SAR[q,w,e]

c1 = (close > indicator1) or (close > indicator1a)

c2 = (close < indicator1) or (close < indicator1a)

mx2 = average[p1,t1](typicalprice)

c5 = mx2 > mx2[1]

c6 = mx2 < mx2[1]

//Stochastic RSI | indicator

lengthRSI = lr //RSI period

lengthStoch = ls //Stochastic period

smoothK = sk //Smooth signal of stochastic RSI

smoothD = sd //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c7 = K>D

c8 = K<D

TIMEFRAME(default)

mx3 = average[p2,t2](typicalprice)

c9 = mx3 > mx3[1]

c10 = mx3 < mx3[1]

//Dynamic Zone Elasticity

Period = 20

smoothing = 2

// ----------------

once smoothing = max(1, smoothing+1)

once period = max(1, Period)

// Coeficient, change if required

once coef = 0.8

// Signal line

x = std[Period](close)

if x=0 then

x=x[1]

endif

signam = 1 + (-1* ( ((average[period](close) + (x*2)) - close) / x ) / 2)

// Dynamic Zones

sq = square(signam)

mean = average[period](signam)

vsqrt = sqrt( average[period](sq) - square(mean) )

top = mean + coef * vsqrt

btm = mean - coef * vsqrt

result = average[smoothing](signam)

c3 = result crosses over btm

c4 = result crosses under top

// Conditions to enter long positions

if tradetype=1 or tradetype=2 then

IF Ctime and c1 and c3 and c5 and c7 and c9 and c11 and c13 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

ENDIF

endif

// Conditions to enter short positions

if tradetype=1 or tradetype=3 then

IF Ctime and c2 and c4 and c6 and c8 and c10 and c12 and c14 THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS sls

SET TARGET %PROFIT tps

ENDIF

endif

//trailing stop function

once trailingstop = 1

if trailingstop then

trailingpercentlong = tsl // %

trailingpercentshort = tss // %

stepPercentlong = stl

stepPercentshort = sts

tssensitivity=2 // 1 = close 2 = H,L 3 = l,H 4 = typicalprice

if onmarket then

trailingstartlong = tradeprice(1)*(trailingpercentlong/100) //trailing will start @trailingstart points profit

trailingstartshort = tradeprice(1)*(trailingpercentshort/100) //trailing will start @trailingstart points profit

trailingsteplong = tradeprice(1)*(stepPercentlong/100) //% step to move the stoploss

trailingstepshort = tradeprice(1)*(stepPercentshort/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

if tssensitivity=1 then

tssensitivitylong=close

tssensitivityshort=close

elsif tssensitivity=2 then

tssensitivitylong=high

tssensitivityshort=low

elsif tssensitivity=3 then

tssensitivitylong=low

tssensitivityshort=high

elsif tssensitivity=4 then

tssensitivitylong=typicalprice

tssensitivityshort=typicalprice

endif

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tssensitivitylong-tradeprice(1)>=trailingstartlong THEN

newSL = tradeprice(1)+trailingsteplong

ENDIF

//next moves

IF newSL>0 AND tssensitivitylong-newSL>trailingsteplong THEN

newSL = newSL+trailingsteplong

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-tssensitivityshort>=trailingstartshort THEN

newSL = tradeprice(1)-trailingstepshort

ENDIF

//next moves

IF newSL>0 AND newSL-tssensitivityshort>trailingstepshort THEN

newSL = newSL-trailingstepshort

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

endif

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF longonmarket and barindex-tradeindex(1)>= b1 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex(1)>= b2 and close>positionprice then

exitshort at market

endif

endif

try deleting lines 61 – 63, change line 60 to

x = (std[Period](close)) + 0.1

it’s a dead simple solution but seems to work so far, opened a trade today with no rejections.

I had a divide by zero stoppage this morning so I am trying below at Line 61 to see if it stops the stoppages! 🙂

x = max(1,std[Period](close))

Here’s a thought, has anybody ever sent a Technical Report (on any Algo) to PRT asking “why is my Algo stopping and giving a divide by zeror error message”?

I’m really fed up with divide by zero errors generally … why can’t PRT put some script in the backtest engine to detect the conditions which give divide by zero errors??

Yeah, mine got stopped as well. I’m now running it with

x = std[Period](close) + 0.3

as adding more than that starts to impact performance. Hasn’t been rejected … yet.

Agreed about PRT, shouldn’t be too difficult for them to at least point out where the problem is.

The + 0.3 version took a trade yesterday. Also

x = std[Period](close)

if x=0 then

x=1

endif

seems to work. I’m hoping this might be a generic solution for div/0 rejections, to be inserted wherever you’ve got a problematic division ???

Could be worth trying.

Yeah my idea below worked also and took a trade yesterday and ended in profit!

Below is effectively the same as your code above, i.e. if 0 read 1.

x = max(1,std[Period](close))

Our solutions make me think the divide by zero errors are mainly due to missing bars (bars with no price movement) and PRT must have some script in their backtest engine to produce the same result … if 0 read 1 ??

Would we really want backtests to keep stopping and throw up divide by zero errors??

Maybe we just live with / work around by adding our solution (if 0 read 1) to our strategy codes if / when we get divide by zero errors? I have been doing this for a while anyway.

Trouble is with complex / many lines of codes it is difficult to determine where the divide by zero error originates, but then it would be just as difficult if the error was thrown up in backtest?

On the strength of above discussion with myself 🙂 , I will not send a Contact Form to PRT for the divide by zero error … unless anybody has any other thoughts?

Yes nonetheless, it’s a nice solution as it won’t affect subsequent calculations.

GraHal, your solution can affect calculations as it will never allow divisions by 0.1…0.9 (or smaller decimals) or negative numbers, while nonetheless‘ will only change 0’s.

The Master has spoken, the None’s have it then! 🙂

I’ll change mine to None’s for next week!