Paul

PaulParticipant

Master

@Francesco The code handles both ways, increase & decrease, with either direction and optimisation 0-1 finds out which is best. It’s based on the last trade result.

win -> decrease angle; loss -> increase angle with direction 0

loss -> decrease angle; win -> increase angle with direction 1

I thought about it to be based on ratio mfa/mae, but that’s difficult!

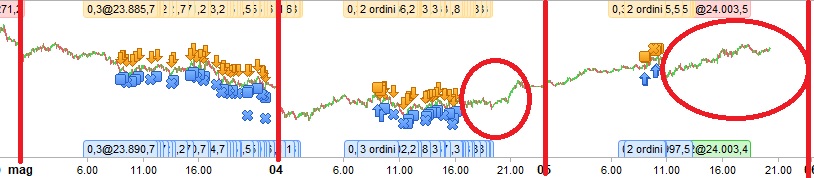

Hey Paul, i’m running a short timeframe system with your dinamic live parameter adjustment with the re-start everyday option. The first 3 days in the backtast it’s everything ok, then these last two days (the system is built to operate since 9 to 22), suddenly the system stop working after some hours.

As you can see from the image, in the first day as the previous 2 everything is normal, then when the days after is restarted it suddenly stops and does not continue where the circle indicates.

I also tried running the system only in the “suspected days” since another hour and it stops anyway. Any clue?

PaulParticipant

Master

Great!

Because of you suggestion francesco I started wondering if there are other ways. How it make it more self learning? Maybe this is a way?

It focus on losses and you still ‘ve to pick a start direction with 0 or 1.

for the boxsize for long (or angle long) it checks performance of the last trade,

if it wins it sticks to the current directions/increments, however if it starts losing and when it reaches the min/max value, it swaps direction to do the opposite and so it’s less depended on a daily reset. Increments are now more important. If the minvalue->maxvalue is big with small increments it takes a while before a swap.

that’s the idea.

// dynamic parameter adjustment [OPPOSITE ON REACH MIN/MAX LEVEL WITH LOSSES)

once periodr = 0 // [0]none;[1]day;[2]week;[3]month;[4]year (reset period)

once directionl= 0 // [0] or [1]opposite

once directions= 0 // [0] or [1]opposite

increment = 4

minvalue = 16

maxvalue = 32

once valuex = (minvalue+maxvalue)/2

once valuey = (minvalue+maxvalue)/2

once startvalueL=24

once startvalueS=24

// main setup

if periodr=0 then

if barindex=0 then

longperf=0

shortperf=0

endif

elsif periodr=1 then

if day<>day[1] then

longperf=0

shortperf=0

endif

elsif periodr=2 then

if dayofweek=0 then

longperf=0

shortperf=0

endif

elsif periodr=3 then

if month<>month[1] then

longperf=0

shortperf=0

endif

elsif periodr=4 then

if year<>year[1] then

longperf=0

shortperf=0

endif

endif

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

if directionl=1 then

if longperf<>0 then

if longperf>longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

directionl=0

endif

endif

else

valuex=startvalueL

endif

anglelong=valuex

else

if longperf<>0 then

if longperf>longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

directionl=1

endif

endif

else

valuex=startvalueL

endif

anglelong=valuex

endif

if directions=1 then

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

directions=0

endif

endif

else

valuey=startvalueS

endif

angleshort=valuey

else

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

directions=1

endif

endif

else

valuey=startvalueS

endif

angleshort=valuey

endif

graph directions coloured(200,0,0)

graph directionl coloured(0,200,0)

graph valuex coloured(0,200,0) as "long value"

graph valuey coloured(200,0,0) as "short value"

I encountered the problem again, I will try to test this new concept … thanks as usual 🙂

PaulParticipant

Master

encountered the problem again

The first thing I think of is that you use used that little snippet and the value for losses is set to 1 (%), so it stops trading after cumulative losses. It could be something else of-course and maybe it’s solved with above code.

The problematic was related to te bullish/bearish detection. Probably the exponential average values reach in some days, through the dynamic adjustment, a certain value that not opens new trades.

Ok, my bad, the problem was not related to a “stuck” in the average values…

I noticed that removing these lines there’s no holes; but it brings the system to more lossess

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

You was right 🙂

Hey Paul or everyone else, i would like to know if and how it’s possible to run an automatic system for a certain time range without using effective money but having it opening positions in “background” (we talked about this time ago in the renk discussion). Then after a time trigger (or a strategyprofit trigger) starting using capital for the position opening.

This is tricky but I have done it before. Basically you need to ‘virtually’ take the positions using the same rules and then keep track of their virtual performance. I use variables called IsLong and IsShort along with variables called LongEntryLevel and ShortEntryLevel

There is also this topic that might be of interest:

Simulated Trading

Francesco, could this be something you’re looking for:

https://www.prorealcode.com/blog/learning/how-to-improve-a-strategy-with-simulated-trades-1/

The very good code of Nicolas is only for short 😉

I was thinking in the case of low tf systems (>30) in order to avoid an hypotetical overfitting of the ML values (max,min,start): what if (using the daily reset mode) we put yesterday’s optimized parameters for tomorrow operativity and going on like this? That reduces the possibility to have ML overfitting based on the fact that the markets does not drastically changes day by day. With this kind of solution we can evolve the ML values in parallel to the changes of the market. Have everyone tried to run a system for a week using last week 200k ML values vs a system for a week with daily optimized values based on yesterday?

I don’t know if i explained myself well, but i hope this can be understandable and interesting 🙂

Sorry if I am clogging this topic continuously but I need a suggestion about an idea.

I would like to know if it’s possible to create a dynamic parameter adjustment like this:

I choose an interval for a parameter of my strategy (for example 10-1000) like the original Paul’s dynamic live parameter adjustment code.

Then, the machine learning algorithm after the closing of the first trade of the day select the most profitable parameter on it between the interval and fix it on the strategy for the rest of the day (so there’s not a continuous fixing trade by trade and not by starting from a parameter and moving following a selected increment value); then there’s the reset for the day after. If it’s possible the first trade of the day should be simulated somehow in order to avoid losses with the vonasi’s simulated trading hint, but it’s not fundamental, I can also achieve a loss starting from a random parameter, the important is having the best one of the first trade fixed for the rest of the day.

Is something like this possible? How? I would be really grateful if you can help me because this could be very important for a strategy that I’m developing 🙂