Paul

PaulParticipant

Master

some first code, not sure if it’s correct completely, but it looks the way i’am after.

I want that the code automatically adjust a few parameters of a strategy if it determines that long or short doesn’t work anymore.

It’s like live adjustments within the margins set. First off I needed the data to work with so this is a start.

// period reset

once periodr=1 //0all;1day;2week;3month;4year

if periodr=0 then

if barindex=0 then

longperf=0

shortperf=0

endif

elsif periodr=1 then

if day<>day[1] then

longperf=0

shortperf=0

endif

elsif periodr=2 then

if dayofweek=0 then

longperf=0

shortperf=0

endif

elsif periodr=3 then

if month<>month[1] then

longperf=0

shortperf=0

endif

elsif periodr=4 then

if year<>year[1] then

longperf=0

shortperf=0

endif

endif

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

graph longperf coloured(0,0,255,255) as "long performance"

graph shortperf coloured(255,0,0,255) as "short performance"

Machine learning … great idea! Got to be the way to go Paul?

Did you see the work Leo did on Neural Network Indicators (links below)? Might spark some ideas for you.

I didn’t understand Leo’s code, but I just spotted something I hadn’t appreciated before!

Also now you are doing above, my task today is to read up on the difference between Machine Learning and Neural Networks.

https://www.prorealcode.com/topic/neural-networks-programming-with-prorealtime/

https://www.prorealcode.com/topic/discussion-on-leos-neural-networks/

PaulParticipant

Master

I know the topics, but never realised it could be usefull for my goal. I only need 1 parameter to be adjust while trading, so maybe that will fit the purpose. Thanks for the links!

In meantime, something simple which can be used with code above.

Stop trading, long or short each, when profits are >2% or losses <-2%. It depends when the period-reset is set to start trading again.

// limit & secure profit daily

if longperf>2 or longperf<-2 then

tradelong=0

else

tradelong=1

endif

if shortperf>2 or shortperf<-2 then

tradeshort=0

else

tradeshort=1

endif

//

If longposition and tradelong then

I did a lot of work on a code that adapted an indicator setting to what had worked best recently and the back tests were all fantastic but the forward tests turned out to be terrible. It seems that no matter what we do there is some form of curve fitting when using historical data and so I gave up on the concept. Plus at the time without arrays it was a coding nightmare!

I have developed and refined a ‘plug and play’ self contained heuristics algorithm over the last few years that can dynamically adjust any parameter based on it’s performance. I use it in all of my strategies. Let me know if you are interested.

Sounds interesting Juanj. I’m sure lots of people would like to see how that works.

@Vonasi I would then need to direct your attention to this topic I started in 2017: https://www.prorealcode.com/topic/machine-learning-in-proorder/

This is the early idea and birth place of the strategy. I will post the latest version there

PaulParticipant

Master

hi juanj yes i’am very interested. Thanks for posting that link!

PaulParticipant

Master

I’ve picked up on this. It’s a version of ML in a basic way. It does what I had in mind.

if previous traderesult is positive/negative, it increase (or decrease) the parameter within max/min values

There’s a reset, currently it reset’s the positionperformance for a period, it doesn’t reset the boxsize in a proper way.

And a mention to the snippet above which is optional with below. It calculates the % for the period and if the realised performance exceeds the preset value it stops trading for that period.

if positions have +0.5 +0.2+0.6+1.0 and the total is bigger then i.e. 2%, it won’t take new trades that period. Same for losses. It’s no stoploss, because it looks at realised trade results.

// dynamic parameter adjustment

once periodr = 1 // [0]none;[1]day;[2]week;[3]month;[4]year (reset period)

once direction= dd // [0] or [1]opposite

once valuex = aa

once valuey = bb

increment = 5

minvalue = 15

maxvalue = 40

// main setup

if periodr=0 then

if barindex=0 then

longperf=0

shortperf=0

endif

elsif periodr=1 then

if day<>day[1] then

longperf=0

shortperf=0

endif

elsif periodr=2 then

if dayofweek=0 then

longperf=0

shortperf=0

endif

elsif periodr=3 then

if month<>month[1] then

longperf=0

shortperf=0

endif

elsif periodr=4 then

if year<>year[1] then

longperf=0

shortperf=0

endif

endif

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

if direction=1 then

if longperf>longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

endif

endif

if shortperf>shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

endif

endif

else

if longperf>longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

endif

endif

if shortperf>shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

endif

endif

endif

graph longperf*10 coloured(0,0,255,255) as "long performance (*10)"

graph shortperf*10 coloured(255,0,0,255) as "short performance (*10)"

boxsizes=valuey

boxsizel=valuex

graph valuex coloured(0,200,0) as "boxsize long"

graph valuey coloured(200,0,0) as "boxsize short"

PaulParticipant

Master

quick fix for the valuex/y reset when periodr > 0

optimise direction 0-1 & valuex/y

// dynamic parameter adjustment

once periodr = 0 // [0]none;[1]day;[2]week;[3]month;[4]year (reset period)

once direction= 0 // [0] or [1]opposite

once valuex = 45

once valuey = 45

once startvalueL=valuex

once startvalueS=valuey

increment = 5

minvalue = 10

maxvalue = 50

// main setup

if periodr=0 then

if barindex=0 then

longperf=0

shortperf=0

endif

elsif periodr=1 then

if day<>day[1] then

longperf=0

shortperf=0

endif

elsif periodr=2 then

if dayofweek=0 then

longperf=0

shortperf=0

endif

elsif periodr=3 then

if month<>month[1] then

longperf=0

shortperf=0

endif

elsif periodr=4 then

if year<>year[1] then

longperf=0

shortperf=0

endif

endif

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

if direction=1 then

if longperf<>0 then

if longperf>longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

endif

endif

else

valuex=startvalueL

endif

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

endif

endif

else

valuey=startvalueS

endif

else

if longperf<>0 then

if longperf>longperf[1] then

if valuex-increment >= minvalue then

valuex=valuex-increment

else

valuex=valuex

endif

elsif longperf<longperf[1] then

if valuex+increment <= maxvalue then

valuex=valuex+increment

else

valuex=valuex

endif

endif

else

valuex=startvalueL

endif

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuey-increment >= minvalue then

valuey=valuey-increment

else

valuey=valuey

endif

elsif shortperf<shortperf[1] then

if valuey+increment <= maxvalue then

valuey=valuey+increment

else

valuey=valuey

endif

endif

else

valuey=startvalueS

endif

endif

graph longperf*10 coloured(0,0,255,255) as "long performance (*10)"

graph shortperf*10 coloured(255,0,0,255) as "short performance (*10)"

boxsizes=valuey

boxsizel=valuex

graph valuex coloured(0,200,0) as "boxsize long"

graph valuey coloured(200,0,0) as "boxsize short"

PaulParticipant

Master

a try, up 7 parameters! (vectorial)

it bouches around between min & max value and it checks if it’s better to increase after a win or decrease for each parameter. There is a reset which can be usefull. It only needs to test 0 – 1 except for the reset period if used.

valuex1 ->angle long

valuex2 -> angle short

valuex3-7 for the other parameters from the strategy.

remove once from mma/mmb etc.

// dynamic parameter adjustment

once periodr = pp // [0]none;[1]day;[2]week;[3]month;[4]year (reset period)

once route1 = p1 // [0] or [1]opposite specific for long

once route2 = p2 // [0] or [1]opposite specific for short

once route3 = p3 // [0] or [1]opposite

once route4 = p4 // [0] or [1]opposite

once route5 = p5 // [0] or [1]opposite

once route6 = p6 // [0] or [1]opposite

once route7 = p7 // [0] or [1]opposite

// long angle long

increment1 = 2

minvalue1 = 16

maxvalue1 = 32

// short angle short

increment2 = 2

minvalue2 = 16

maxvalue2 = 32

//

increment3 = 1 //periodea 10

minvalue3 = 8

maxvalue3 = 12

//

increment4 = 1 //nbchandeliera 15

minvalue4 = 13

maxvalue4 = 17

//

increment5 = 1 //periodeb 20

minvalue5 = 18

maxvalue5 = 22

//

increment6 = 1 //nbchandelierb 35

minvalue6 = 30

maxvalue6 = 36

//

increment7 = 1 //lag 5

minvalue7 = 0

maxvalue7 = 6

once valuex1 = (minvalue1+maxvalue1)/2

once valuex2 = (minvalue2+maxvalue2)/2

once valuex3 = (minvalue3+maxvalue3)/2

once valuex4 = (minvalue4+maxvalue4)/2

once valuex5 = (minvalue5+maxvalue5)/2

once valuex6 = (minvalue6+maxvalue6)/2

once valuex7 = (minvalue6+maxvalue7)/2

once startvalue1=valuex1

once startvalue2=valuex2

once startvalue3=valuex3

once startvalue4=valuex4

once startvalue5=valuex5

once startvalue6=valuex6

once startvalue7=valuex7

// main setup

if periodr=0 then

if barindex=0 then

longperf=0

shortperf=0

endif

elsif periodr=1 then

if day<>day[1] then

longperf=0

shortperf=0

endif

elsif periodr=2 then

if dayofweek=0 then

longperf=0

shortperf=0

endif

elsif periodr=3 then

if month<>month[1] then

longperf=0

shortperf=0

endif

elsif periodr=4 then

if year<>year[1] then

longperf=0

shortperf=0

endif

endif

if longonmarket[1] and (not onmarket or shortonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

longperf=longperf+positionperf(1)*100

else

longperf=longperf-positionperf(1)*100

endif

endif

if shortonmarket[1] and (not onmarket or longonmarket) then

if strategyprofit[1]>=strategyprofit[2] then

shortperf=shortperf+positionperf(1)*100

else

shortperf=shortperf-positionperf(1)*100

endif

endif

if route1=1 then

if longperf<>0 then

if longperf>longperf[1] then

if valuex1+increment1 <= maxvalue1 then

valuex1=valuex1+increment1

else

valuex1=valuex1

endif

elsif longperf<longperf[1] then

if valuex1-increment1 >= minvalue1 then

valuex1=valuex1-increment1

else

valuex1=valuex1

endif

endif

else

valuex1=startvalue1

endif

else

if longperf<>0 then

if longperf>longperf[1] then

if valuex1-increment1 >= minvalue1 then

valuex1=valuex1-increment1

else

valuex1=valuex1

endif

elsif longperf<longperf[1] then

if valuex1+increment1 <= maxvalue1 then

valuex1=valuex1+increment1

else

valuex1=valuex1

endif

endif

else

valuex1=startvalue1

endif

endif

if route2=1 then

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuex2+increment2 <= maxvalue2 then

valuex2=valuex2+increment2

else

valuex2=valuex2

endif

elsif shortperf<shortperf[1] then

if valuex2-increment2 >= minvalue2 then

valuex2=valuex2-increment2

else

valuex2=valuex2

endif

endif

else

valuex2=startvalue2

endif

else

if shortperf<>0 then

if shortperf>shortperf[1] then

if valuex2-increment2 >= minvalue2 then

valuex2=valuex2-increment2

else

valuex2=valuex2

endif

elsif shortperf<shortperf[1] then

if valuex2+increment2 <= maxvalue2 then

valuex2=valuex2+increment2

else

valuex2=valuex2

endif

endif

else

valuex2=startvalue2

endif

endif

if route3=1 then //periodea

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex3+increment3 <= maxvalue3 then

valuex3=valuex3+increment3

else

valuex3=valuex3

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex3-increment3 >= minvalue3 then

valuex3=valuex3-increment3

else

valuex3=valuex3

endif

endif

else

valuex3=startvalue3

endif

else

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex3-increment3 >= minvalue3 then

valuex3=valuex3-increment3

else

valuex3=valuex3

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex3+increment3 <= maxvalue3 then

valuex3=valuex3+increment3

else

valuex3=valuex3

endif

endif

else

valuex3=startvalue3

endif

endif

if route4=1 then //nbchandeliera

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex4+increment4 <= maxvalue4 then

valuex4=valuex4+increment4

else

valuex4=valuex4

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex4-increment4 >= minvalue4 then

valuex4=valuex4-increment4

else

valuex4=valuex4

endif

endif

else

valuex4=startvalue4

endif

else

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex4-increment4 >= minvalue4 then

valuex4=valuex4-increment4

else

valuex4=valuex4

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex4+increment4 <= maxvalue4 then

valuex4=valuex4+increment4

else

valuex4=valuex4

endif

endif

else

valuex4=startvalue4

endif

endif

if route5=1 then //periodeb

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex5+increment5 <= maxvalue5 then

valuex5=valuex5+increment5

else

valuex5=valuex5

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex5-increment5 >= minvalue5 then

valuex5=valuex5-increment5

else

valuex5=valuex5

endif

endif

else

valuex5=startvalue5

endif

else

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex5-increment5 >= minvalue5 then

valuex5=valuex5-increment5

else

valuex5=valuex5

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex5+increment5 <= maxvalue5 then

valuex5=valuex5+increment5

else

valuex5=valuex5

endif

endif

else

valuex5=startvalue5

endif

endif

if route6=1 then //nbchandelierb

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex6+increment6 <= maxvalue6 then

valuex6=valuex6+increment6

else

valuex6=valuex6

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex6-increment6 >= minvalue6 then

valuex6=valuex6-increment6

else

valuex6=valuex6

endif

endif

else

valuex6=startvalue6

endif

else

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex6-increment6 >= minvalue6 then

valuex6=valuex6-increment6

else

valuex6=valuex6

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex6+increment6 <= maxvalue6 then

valuex6=valuex6+increment6

else

valuex6=valuex6

endif

endif

else

valuex6=startvalue6

endif

endif

if route7=1 then //lag

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex7+increment7 <= maxvalue7 then

valuex7=valuex7+increment7

else

valuex7=valuex7

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex7-increment7 >= minvalue7 then

valuex7=valuex7-increment7

else

valuex7=valuex7

endif

endif

else

valuex7=startvalue7

endif

else

if shortperf<>0 or longperf<>0 then

if shortperf>shortperf[1] or longperf>longperf[1] then

if valuex7-increment7 >= minvalue7 then

valuex7=valuex7-increment7

else

valuex7=valuex7

endif

elsif shortperf<shortperf[1] or longperf<longperf[1] then

if valuex7+increment7 <= maxvalue7 then

valuex7=valuex7+increment7

else

valuex7=valuex7

endif

endif

else

valuex7=startvalue7

endif

endif

Line 52 should not be

once valuex7 = (minvalue7+maxvalue7)/2

?

PaulParticipant

Master

yes, saw it later after posting. More bugs most likely. Need a reset day/week/month i.e. on 5 min. to make sense, if it does anyway. The min+max/2 value can be replace with a preferred number. I.e. lag, put in 5, with increment 5 and it will switch between 0 and 5. (with minvalue=0/maxvalue=5)

Clear.. btw i was thinking: you can choose 0 and 1 to select the direction of the increment; it’s not possible to have both? The system can handle at the same time the decision of going up and down?

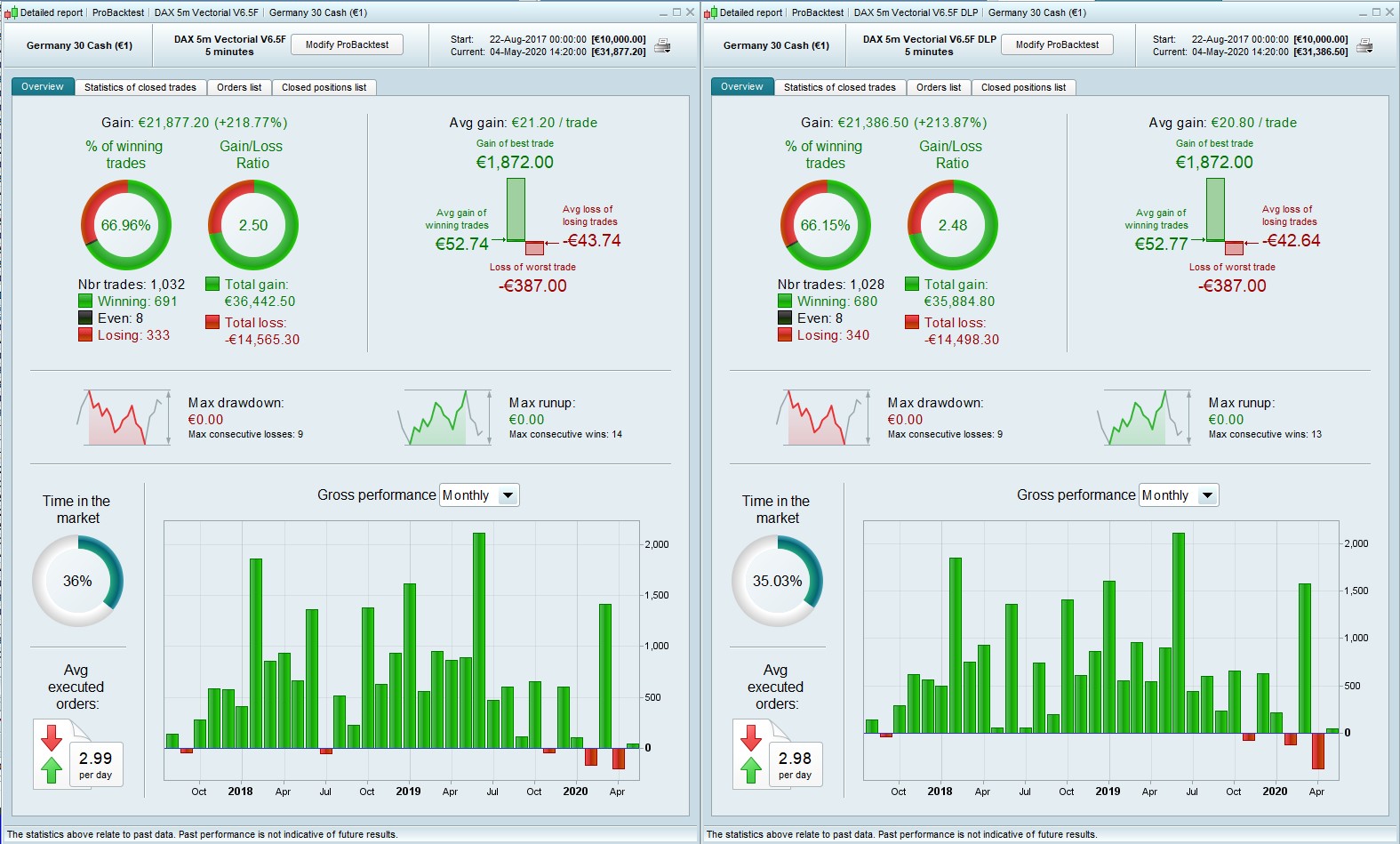

Altered the min/max values and got it to where it’s very close to the non-dynamic version. Tried using a fixed number for startvalue but (min+max)/2 was better. Feels like it needs just another little push to get up into positive territory!

// dynamic parameter adjustment

once periodr = 1 // [0]none;[1]day;[2]week;[3]month;[4]year (reset period)

once route1 = 1 // [0] or [1]opposite specific for long

once route2 = 1 // [0] or [1]opposite specific for short

once route3 = 1 // [0] or [1]opposite

once route4 = 1 // [0] or [1]opposite

once route5 = 1 // [0] or [1]opposite

once route6 = 1 // [0] or [1]opposite

once route7 = 1 // [0] or [1]opposite

// long angle long 45

increment1 = 2

minvalue1 = 37

maxvalue1 = 53

// short angle short 34

increment2 = 2

minvalue2 = 26

maxvalue2 = 42

//

increment3 = 1 //periodea 10

minvalue3 = 8

maxvalue3 = 12

//

increment4 = 1 //nbchandeliera 14

minvalue4 = 12

maxvalue4 = 16

//

increment5 = 1 //periodeb 22

minvalue5 = 20

maxvalue5 = 24

//

increment6 = 1 //nbchandelierb 34

minvalue6 = 32

maxvalue6 = 36

//

increment7 = 1 //lag 4

minvalue7 = 0

maxvalue7 = 6