With 96.39% wins ? Yeah I could live with that!

You should use the code snippet from here:

https://www.prorealcode.com/topic/average-gain-per-1-code-snippet/#post-94438

It allows us to compare like for like the average gain per 1 position size staked. This way it is easy to see whether accumulating positions is actually a good way to risk your bank running out or not.

Follow it with a good robustness test and you can learn an awful lot about any strategy.

Vonasi, you are a veritable fount of cool ideas – thanks for that!

@GraHal I added Paul’s mods to the trailing stop and ran the WF; there’s good news and not so good. It’s rock steady, only 3 losing trades … but not nearly so profitable. For sure I would run it with MM and cumulate orders.

The good news in that last test is that last test is that the OOS line is at the same angle as the IS line. The WF ratio at 78% also looks positive. The bad news is that not all OOS tests were profitable. Another observation is that 83 trades is not very many to give any great degree of confidence in the results.

Some other observations are that during the data that you are testing on the DOW has been pretty much in a bull rally the whole time with only a few sideways movements and one minor dip. It is very easy to create a strategy that makes money on data that is always going up. How would it cope in a market crash when price is behaving in a very different manner. Perhaps you should consider a very loose fuse stop to shut the strategy down once a loss that you are uncomfortable with has occurred. Yes you lose money and quite a lot of money but not as much as you possibly could do if the market carries on down.

There is also every possibility that by using a trailing stop that you have curve fitted the trailing stop values to the data. You need to test with values either side of your ideal settings and graph the results in Excel or similar to see if the strategy is on a trailing stop cliff edge. You should try to do this with any other variables too to try to prove whether it is a curve fit or not. Once again only 83 trades is your enemy when doing this with this strategy.

I added Paul’s mods to the trailing stop and ran the WF

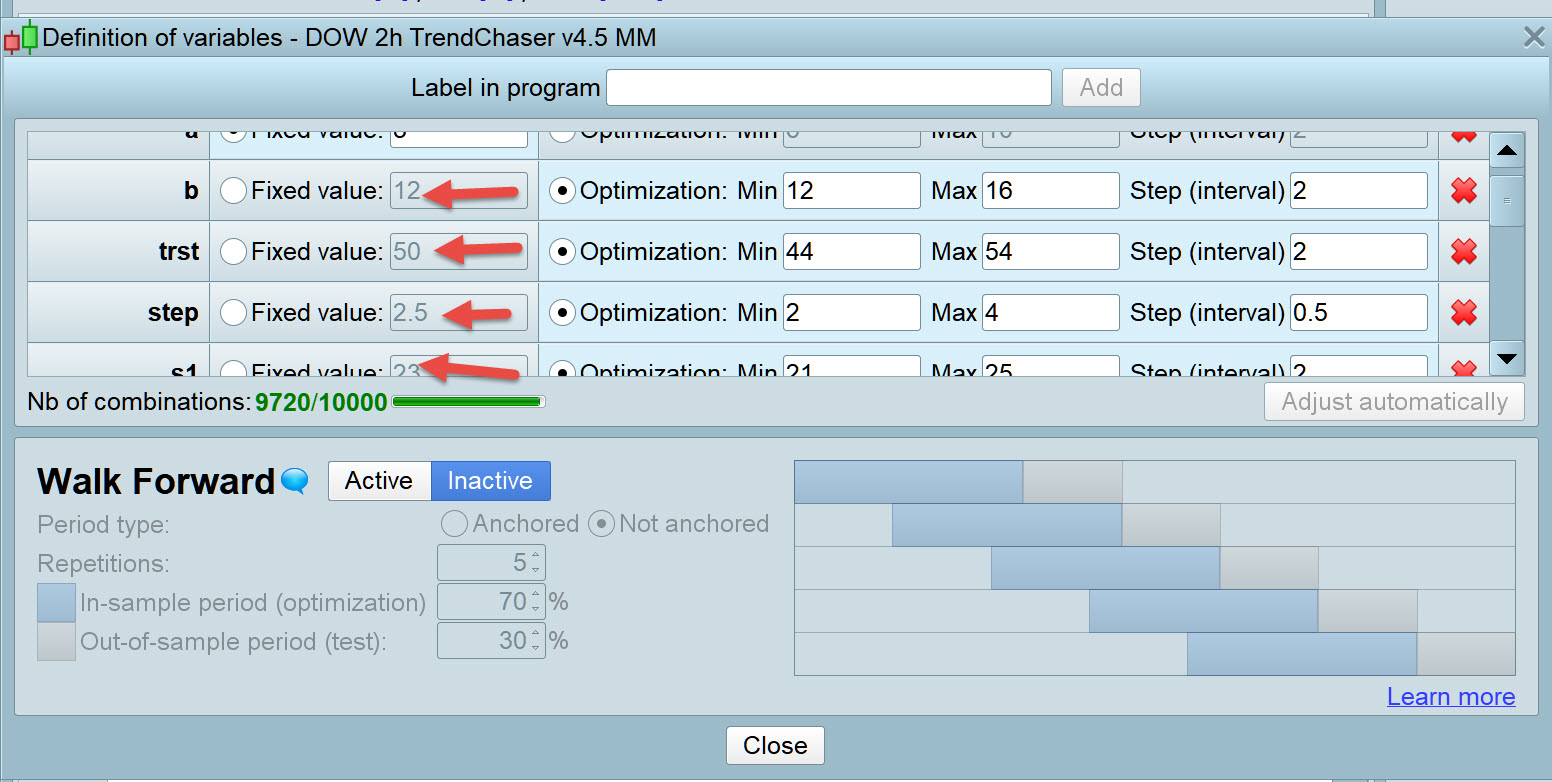

So on v4.5 … are the values at the red arrowheads (on attached) the values after WF that you consider best to go forward with? Or do I need to do the WF again to get WF values for the variables?

I would be setting it going on Demo Forward Test so it’s not critical re the values.

TBH, this is the part I’m least clear about. After doing a WF, we get 5 sets of variables … how to decide which to go with? I think the numbers I put in the fixed box (your red arrows) are an average of the OS results. Is that sensible? The parameters are fairly narrow so prob any of those numbers will ‘work’, but which are best? I still have no idea without just going for a general curve-fit!

On afterthought I ran a 1 x 70/30 optimization and decided to use the values from that. Makes more sense than just averaging the 5 x results.

how to decide which to go with?

Yeah there is no black and white answer in a way! 🙁

The golden rule is to use the set of values for the most recent IS period. This kinda fits in with our re-optimisation MO.

However, I do not always use the most recent IS values … if I judge from the equity curve that there was an exceptional drop, rise or even a prolonged flat period over that most recent IS period.

Reason: WF values would be tuned to an exceptional event period (which could end very soon!).

Conversely, if the most recent OOS period (the period for which the profit / loss figure is shown is exceptional due to sharp rise, drop or flat then I might use the most recent WF values.

Reason: The exceptional OOS period may be the reason for low profit or loss, but the corresponding IS period (over which the WF values were formed) was not exceptional.

And having said above … I probably flick about from one set of rules to another and more in between! 🙂

WF primarily is to see if … in order to show a profit over OOS periods … does this require big variation in values for variables.

If Yes, then probably the Auto-System is not going to be a big winner,

Also the WF Efficiency Ratio needs to be > 50% ish (but with small variation in variable values between IS periods)!

I’ll try to bear all that in mind, but at the mo that level of interpreting results is beyond me!

What about my idea of running a 100k 70/30 and using the values from that? Using the 5xWF to assess robustness, then a separate 1x run to get the numbers? Make sense?

a separate 1x run to get the numbers?

The separate run being the 100K bars WF at 70/30 … Yes?

Thing is though if we use those values to do a Forwad Test (Live trading on Real or Demo) then we would be using values from the 70% IS period. What about the intelligence to be gained from the 30% OOS Period?

IMHO it would be better to do a full optimisation over the full 100K bars (Not using WF) and use the values thus obtained.

Or – after establishing robustness using a 5 period WF – then do a normal optimisation (not using WF) over the most recent 30k bars or 50k bars?

after establishing robustness using a 5 period WF – then do a normal optimisation (not using WF) over the most recent 30k bars or 50k bars?

Yes, that sounds good as a method (I have to have a method or my brain just stalls from having too many possible ways forward). And more in keeping with out experiments in short timeframe optimization… cheers!