Dear all,

I’ve been trying for long to figure out why my code gets divison by zero error. Usually i can’t even start the code without that it goes 1 minute and it shuts down with division by zero error. But on some occasions, dont ask me why, it can start and run, but if i stop and try to run it again it wont work. I’ve narrowed it down to my position sizing calculation, since if i remove this it works fine. But i can figure out how to change the code to have the same position sizing code without causing divison by zero error.

The thought is to not risk more that 0,5% of the Equity by setting a stop in relation to ATR on entry.

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995

MinPositionSize = 1

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

Timeframe (5 minutes)

IF NOT ONMARKET THEN

IF Z1 or Z2 or Z3 or Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 THEN

MyStop = AverageTrueRange[17](close[3])*ATRMult

BUY Positionsize CONTRACTS AT MARKET

endif

endif

IF Z1 or Z2 or Z3 or Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 THEN

MyStop = AverageTrueRange[17](close[3])*ATRMult

SELLSHORT Positionsize CONTRACTS AT MARKET

endif

I would be happy with suggestions that i could try,

Best regards Anders

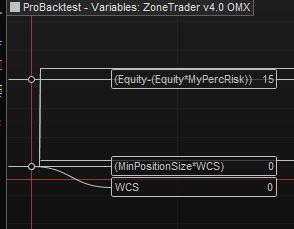

Append these lines to visually detect any cause:

graph ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

graph (Equity-(Equity*MyPercRisk))

graph (MinPositionSize*WCS)

graph WCS //this line could retain 0

Thanks Roberto, i atleast can see that it is due to something in the start. When i change the backtest size it always starts with 0 as you can see in my example pics. I do not know how to solve it though.. 🙂

Tips?

Br Anders

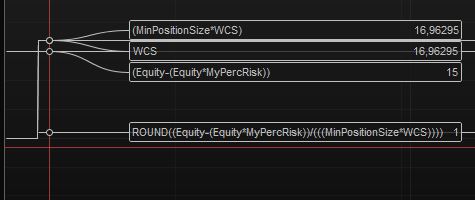

Attached also the values for the different graphs.

Br Anders

What value should MyStop have?

Ciao,

It should be based on AverageTrueRange, but it seems like it cant calculate the ATR directly when i start the system? Below you can see what MyStop should be, i have it embedded in the buying section to avoid that it recalculates on every bar, because i want the initial ATR based upon the entry candle.

IF NOT ONMARKET THEN

IF Z1 or Z2 or Z3 or Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 THEN

MyStop = AverageTrueRange[17](close[3])*ATRMult

BUY Positionsize CONTRACTS AT MARKET

endif

endif

Br Anders

Where can I find variables Z1, Z2, Z3, Z4, Z5, Z6, Z7, Z8, Z9 and Z10?

I think it would be easier if you posted the running code so that I can test it.

Defparam cumulateorders = False

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995 // Max risk, bör ej vara över 2% = 0.98

MinPositionSize = 1//Minsta size

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

ATRMult = 5

SLMult = 1 //1 = ingen multiplier, starta alltid med 1, försämrad risk/reward vid multiplier

MyProfit = 0 //0 är standard

MyStartTrade = 090000

MyEndTrade = 173000

DaytoFilter = 0

Timeframe (Default)

Z1H = 2204

Z1L = 2191

Z2H = 2250

Z2L = 2245

Z3H = 2284

Z3L = 2277

Z4H = 2308

Z4L = 2300

Z5H = 2362

Z5L = 2356

Z6H = 2413

Z6L = 2404

Z7H = 2383

Z7L = 2376

Z8H = 4620

Z8L = 4615

Z9H = 4665

Z9L = 4670

Z10H = 4698

Z10L = 4704

Z1 = Close > Z1L and Close < Z1H

Z2 = Close > Z2L and Close < Z2H

Z3 = Close > Z3L and Close < Z3H

Z4 = Close > Z4L and Close < Z4H

Z5 = Close > Z5L and Close < Z5H

Z6 = Close > Z6L and Close < Z6H

Z7 = Close > Z7L and Close < Z7H

Z8 = Close > Z8L and Close < Z8H

Z9 = Close > Z9L and Close < Z9H

Z10 = Close > Z10L and Close < Z10H

Long = Average[9](close) < Average[20](close)

Short = Average[9](close) > Average[20](close)

Timeframe (5 minutes)

IF NOT ONMARKET THEN

IF CurrentDayOfWeek <> DaytoFilter and Time > MyStartTrade And Time < MyEndTrade THEN

IF Long THEN

IF Z1 or Z2 or Z3 or Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 THEN

MyStop = AverageTrueRange[10](close[1])*ATRMult

BUY Positionsize CONTRACTS AT MARKET

endif

endif

IF Short THEN

IF Z1 or Z2 or Z3 or Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 THEN

MyStop = AverageTrueRange[10](close[1])*ATRMult

SELLSHORT Positionsize CONTRACTS AT MARKET

endif

endif

endif

endif

Timeframe (Default)

SHL = (Close - (Positionprice+(Mystop*2)))

SellHalfL = (SHL > 0.5)

SHS = ((Positionprice-(Mystop*2)) - Close)

SellHalfS = (SHS > 0.5)

SLL = ((Positionprice-(Mystop*SLMult)) - Close)

StopL = (SLL > 0.5)

SLS = (Close - (Positionprice+(Mystop*SLMult)))

StopS = (SLS > 0.5)

BEL = (Close-Positionprice)

BrkEL = (BEL < 1)

BES = (Positionprice-Close)

BrkES = (BES < 1)

BCL = (Close - (Positionprice+(MyStop)))

BeCalcL = (BCL > 1)

BCS = ((Positionprice-(1)) - Close)

BeCalcS = (BCS > 1)

HalfPos = (Positionsize/2)

IF abs(CountOfPosition) = 0 THEN

Count = 0

endif

IF LONGONMARKET THEN

IF SellHalfL AND abs(CountOfPosition) = PositionSize THEN

SELL HalfPos CONTRACTS AT MARKET

elsif StopL THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

elsif BECalcL THEN

Count = Count + 1

IF Count >= 1 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

endif

IF SHORTONMARKET THEN

IF SellHalfS AND abs(CountOfPosition) = PositionSize THEN

EXITSHORT HalfPos CONTRACTS AT MARKET

elsif StopS THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

elsif BECalcS THEN

Count = Count + 1

IF Count = 1 AND BrkES THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

endif

If MyProfit > 0 then

SET TARGET PPROFIT MyProfit

endif

Thanks, i’ve added the full code.

Br Anders

It’s due to WCS being 0 at the beginning(line 2), so that line 7 will immediately result in a “DIVISION BY 0” error.

Code is read and executed sequentially, you need to set a value for MyStop prior to line 2. Or you may want to move lines 2-7 to a line AFTER MyStop is assigned a correct value, other than 0.

Ciao Roberto,

Hope you are well! You solved the divison error for me and i’ve been trading the code for a while. But now i have another “issue”, i’ve tried to build a scaling out system based on how many times my risk im in profit. And i do not want to leave a position in market which would be easier but instead i would like the code to sell based on if the calculation is true.

Issue #1: My self half code works very well when im short. It sells half of the contract and keeps the other half. But when Long, it sell halfs and on next bar sell the other half directly. In my backtest everything looks fine.

Issue #2: When i was in a short pos recently and it scaled out half, it never triggered my other commands to sell remaining half even though it passed well the 2x of profit and should have sold on 1.25 times the entry. I can’t find a reason for why? Everything looks OK in the backtest.

Hope you or someone else could give some guidance, last time you mentioned in which steps the code is read. Could you elaborate this point a bit further?

Code has been traded on: Sverige 30 Cash, 1 min timeframe (if you talk 1k bars back you will have the latest trades i done, which are fine, but not really acc the backtest since it kept the position until i manually closed the short almost 3x of profits)

Br Anders

Defparam cumulateorders = False

ATRMult = 1//4

SellHalf = 1 // 0 = säljer poss till 2:1 RR, 1 säljer halva vid 2:1

BE1 = 1 // 1= BE lyfts in vid 1:1

BEMult = 1 // 1 = ingen multiplier, starta alltid med 1. Vid ex2 ggr måste kurs nå 2 ggr risk innan den flyttar till BE.

BE2 = 1 // 1= BE lyfts in till 1.25:1 vid 2:1

BE3 = 1 // 1= BE lyfts in till 2.5:1 vid 3:1

BE4 = 1 // 1= BE lyfts in till 3.75:1 vid 4:1

SLMult = 1 //1 = ingen multiplier, starta alltid med 1, försämrad risk/reward vid multiplier

MyProfit = 0 //0 är standard

MyStartTrade = 060000

MyEndTrade = 173000

DaytoFilter = 0

Timeframe (Default)

Z1H = 23080 //LONG

Z1L = 23030 //LONG

Z2H = 23000 //LONG

Z2L = 22290 //LONG

Z3H = 22870 //LONG

Z3L = 22770 //LONG

Z4H = 2315 // SHORT

Z4L = 2308 // SHORT

Z5H = 2342 // SHORT

Z5L = 2338 // SHORT

Z6H = 2371 // SHORT

Z6L = 2365 // SHORT

Z7H = 15955

Z7L = 15955

Z8H = 15955

Z8L = 15955

Z9H = 15955

Z9L = 15955

Z10H = 15955

Z10L = 15955

Z11H = 15955

Z11L = 15955

Z12H = 15955

Z12L = 15955

Z13H = 15955

Z13L = 15955

Z14H = 15955

Z14L = 15945

Z15H = 16010

Z15L = 15995

Z16H = 16055

Z16L = 16045

Z17H = 16110

Z17L = 16090

Z18H = 16155

Z18L = 16135

Z19H = 16235

Z19L = 16215

Z20H = 16295

Z20L = 16280

Z21H = 16360

Z21L = 16345

Z22H = 16420

Z22L = 16400

Z23H = 16525

Z23L = 16500

Z24H = 16610

Z24L = 16595

Z25H = 16775

Z25L = 16775

Z1 = Close > Z1L and Close < Z1H

Z2 = Close > Z2L and Close < Z2H

Z3 = Close > Z3L and Close < Z3H

Z4 = Close > Z4L and Close < Z4H

Z5 = Close > Z5L and Close < Z5H

Z6 = Close > Z6L and Close < Z6H

Z7 = Close > Z7L and Close < Z7H

Z8 = Close > Z8L and Close < Z8H

Z9 = Close > Z9L and Close < Z9H

Z10 = Close > Z10L and Close < Z10H

Z11 = Close > Z11L and Close < Z11H

Z12 = Close > Z12L and Close < Z12H

Z13 = Close > Z13L and Close < Z13H

Z14 = Close > Z14L and Close < Z14H

Z15 = Close > Z15L and Close < Z15H

Z16 = Close > Z16L and Close < Z16H

Z17 = Close > Z17L and Close < Z17H

Z18 = Close > Z18L and Close < Z18H

Z19 = Close > Z19L and Close < Z19H

Z20 = Close > Z20L and Close < Z20H

Z21 = Close > Z21L and Close < Z21H

Z22 = Close > Z22L and Close < Z22H

Z23 = Close > Z23L and Close < Z23H

Z24 = Close > Z24L and Close < Z24H

Z25 = Close > Z25L and Close < Z25H

IF NOT ONMARKET THEN

IF CurrentDayOfWeek <> DaytoFilter and Time > MyStartTrade And Time < MyEndTrade THEN

IF Z1 or Z2 or Z3 or Z7 or Z8 or Z9 or Z10 or Z11 or Z12 or Z13 or Z14 or Z15 or Z16 or Z17 or Z18 or Z19 or Z20 or Z21 or Z22 or Z23 or Z24 or Z25 THEN

MyStop = 8*ATRMult

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995 // Max risk, bör ej vara över 2% = 0.98

MinPositionSize = 1//Minsta size

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

BUY Positionsize CONTRACTS AT MARKET

endif

endif

IF Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 or Z11 or Z12 or Z13 or Z14 or Z15 or Z16 or Z17 or Z18 or Z19 or Z20 or Z21 or Z22 or Z23 or Z24 or Z25 THEN

MyStop = 8*ATRMult

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995 // Max risk, bör ej vara över 2% = 0.98

MinPositionSize = 1//Minsta size

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

SELLSHORT Positionsize CONTRACTS AT MARKET

endif

endif

Timeframe (Default)

SHL = (Close - (Positionprice+(Mystop*2)))

SellHalfL = (SHL > 0.5)

SHS = ((Positionprice-(Mystop*2)) - Close)

SellHalfS = (SHS > 0.5)

SLL = ((Positionprice-(Mystop*SLMult)) - Close)

StopL = (SLL > 0.5)

SLS = (Close - (Positionprice+(Mystop*SLMult)))

StopS = (SLS > 0.5)

BEL = (Close-Positionprice)

BrkEL = (BEL < 1)

BES = (Positionprice-Close)

BrkES = (BES < 1)

BCL = (Close - (Positionprice+(MyStop*BEMult)))

BeCalcL = (BCL > 1)

BCS = ((Positionprice-(Mystop*BEMult)) - Close)

BeCalcS = (BCS > 1)

BEL2 = (Close-(Positionprice+MyStop*1.25))

BrkEL2 = (BEL2 < 1)

BES2 = ((Positionprice-MyStop*1.25)-Close)

BrkES2 = (BES2 < 1)

BCL2 = (Close - (Positionprice+(MyStop*2)))

BeCalcL2 = (BCL2 > 1)

BCS2 = ((Positionprice-(Mystop*2)) - Close)

BeCalcS2 = (BCS2 > 1)

BEL3 = (Close-(Positionprice+(MyStop*2.5)))

BrkEL3 = (BEL3 < 1)

BES3 = ((Positionprice-(MyStop*2.5))-Close)

BrkES3 = (BES3 < 1)

BCL3 = (Close - (Positionprice+(MyStop*3)))

BeCalcL3 = (BCL3 > 1)

BCS3 = ((Positionprice-(Mystop*3)) - Close)

BeCalcS3 = (BCS3 > 1)

BEL4 = (Close-(Positionprice+(MyStop*3.5)))

BrkEL4 = (BEL4 < 1)

BES4 = ((Positionprice-(MyStop*3.5))-Close)

BrkES4 = (BES4 < 1)

BCL4 = (Close - (Positionprice+(MyStop*4)))

BeCalcL4 = (BCL4 > 1)

BCS4 = ((Positionprice-(Mystop*4)) - Close)

BeCalcS4 = (BCS4 > 1)

BEL5 = (Close-(Positionprice+(MyStop*4.5)))

BrkEL5 = (BEL5 < 1)

BES5 = ((Positionprice-(MyStop*4.5))-Close)

BrkES5 = (BES5 < 1)

BCL5 = (Close - (Positionprice+(MyStop*5)))

BeCalcL5 = (BCL5 > 1)

BCS5 = ((Positionprice-(Mystop*5)) - Close)

BeCalcS5 = (BCS5 > 1)

BEL6 = (Close-(Positionprice+(MyStop*5.5)))

BrkEL6 = (BEL6 < 1)

BES6 = ((Positionprice-(MyStop*5.5))-Close)

BrkES6 = (BES6 < 1)

BCL6 = (Close - (Positionprice+(MyStop*6)))

BeCalcL6 = (BCL6 > 1)

BCS6 = ((Positionprice-(Mystop*6)) - Close)

BeCalcS6 = (BCS6 > 1)

BEL7 = (Close-(Positionprice+(MyStop*6.5)))

BrkEL7 = (BEL7 < 1)

BES7 = ((Positionprice-(MyStop*6.5))-Close)

BrkES7 = (BES7 < 1)

BCL7 = (Close - (Positionprice+(MyStop*6)))

BeCalcL7 = (BCL7 > 1)

BCS7 = ((Positionprice-(Mystop*6)) - Close)

BeCalcS7 = (BCS7 > 1)

BEL8 = (Close-(Positionprice+(MyStop*7.5)))

BrkEL8 = (BEL8 < 1)

BES8 = ((Positionprice-(MyStop*7.5))-Close)

BrkES8 = (BES8 < 1)

BCL8 = (Close - (Positionprice+(MyStop*7)))

BeCalcL8 = (BCL8 > 1)

BCS8 = ((Positionprice-(Mystop*7)) - Close)

BeCalcS8 = (BCS8 > 1)

HalfPos = (Positionsize/2)

IF abs(CountOfPosition) = 0 THEN

CountSellHalf = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count2 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count3 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count4 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count5 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count6 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count7 = 0

endif

IF abs(CountOfPosition) = 0 THEN

Count8 = 0

endif

IF abs(CountOfPosition) = 0 THEN

HalfPos = 0

endif

IF LONGONMARKET THEN

IF SellHalf = 1 THEN

IF SellHalfL AND abs(CountOfPosition) = PositionSize THEN

SELL HalfPos CONTRACTS AT MARKET

endif

endif

IF SellHalf = 0 THEN

IF SellHalfL AND abs(CountOfPosition) = PositionSize THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF StopL THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BE1 = 1 THEN

IF BECalcL THEN

Count = Count + 1

endif

IF Count >= 1 and BrkEL THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE2 = 1 THEN

IF BECalcL2 THEN

Count2 = Count2 + 1

endif

IF Count2 >= 1 and BrkEL2 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE3 = 1 THEN

IF BECalcL3 THEN

Count3 = Count3 + 1

endif

IF Count3 >= 1 and BrkEL3 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE4 = 1 THEN

IF BECalcL4 THEN

Count4 = Count4 + 1

endif

IF Count4 >= 1 and BrkEL4 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BECalcL5 THEN

Count5 = Count5 + 1

endif

IF Count5 >= 1 and BrkEL5 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcL6 THEN

Count6 = Count6 + 1

endif

IF Count6 >= 1 and BrkEL6 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcL7 THEN

Count7 = Count7 + 1

endif

IF Count7 >= 1 and BrkEL7 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcL8 THEN

Count8 = Count8 + 1

endif

IF Count8 >= 1 and BrkEL8 THEN

SELL abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF SHORTONMARKET THEN

IF SellHalf = 1 THEN

IF SellHalfS AND abs(CountOfPosition) = PositionSize THEN

EXITSHORT HalfPos CONTRACTS AT MARKET

endif

endif

IF SellHalf = 0 THEN

IF SellHalfS AND abs(CountOfPosition) = PositionSize THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF StopS THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BE1 = 1 THEN

IF BECalcS THEN

Count = Count + 1

endif

IF Count >= 1 AND BrkES THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE2 = 1 THEN

IF BECalcS2 THEN

Count2 = Count2 + 1

endif

IF Count2 >= 1 AND BrkES2 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE3 = 1 THEN

IF BECalcS3 THEN

Count3 = Count3 + 1

endif

IF Count3 >= 1 AND BrkES3 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BE4 = 1 THEN

IF BECalcS4 THEN

Count4 = Count4 + 1

endif

IF Count4 >= 1 AND BrkES4 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

IF BECalcS5 THEN

Count5 = Count5 + 1

endif

IF Count5 >= 1 AND BrkES5 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcS6 THEN

Count6 = Count6 + 1

endif

IF Count6 >= 1 AND BrkES6 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcS7 THEN

Count7 = Count7 + 1

endif

IF Count7 >= 1 AND BrkES7 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

IF BECalcS8 THEN

Count8 = Count8 + 1

endif

IF Count8 >= 1 AND BrkES8 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

endif

If MyProfit > 0 then

SET TARGET PPROFIT MyProfit

endif

Issue #1: NO Long trades have been opened, despite trying with 1K, 5K, 10K, 15K, 50K, 100K and 200K units

Issue #2: Backtests seem to work correctly; it’s impossible to spot any real-time failure.

Thanks for supporting,

Issue #1: True, that is due to the fact that it has no levels that creates the buy signal for LONG. But i add those levels manually every week, and just now i did not have any long levels. But when it has an Long position, it scales out differently from short. Can that be due to that i have a certain sequence in the code?

Issue #2: Yes, i have the same conclusion the backtest looks just fine. But in real-time the code acts a bit differently by not respecting all sell calculations.

Is the code read from top to bottom or how does it work?

Br Anders

But when it has an Long position, it scales out differently from short. Can that be due to that i have a certain sequence in the code?

Hi Anders – Indeed it can. For example (and Yes, the code is executed from top to bottom) :

JustEntered = 0 // <<--

IF NOT ONMARKET THEN

If not JustEntered then // <<-- This one is for good habit.

IF CurrentDayOfWeek <> DaytoFilter and Time > MyStartTrade And Time < MyEndTrade THEN

IF Z1 or Z2 or Z3 or Z7 or Z8 or Z9 or Z10 or Z11 or Z12 or Z13 or Z14 or Z15 or Z16 or Z17 or Z18 or Z19 or Z20 or Z21 or Z22 or Z23 or Z24 or Z25 THEN

MyStop = 8*ATRMult

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995 // Max risk, bör ej vara över 2% = 0.98

MinPositionSize = 1//Minsta size

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

BUY Positionsize CONTRACTS AT MARKET

JustEntered = 1 // <<--

endif

endif

endif

If not JustEntered then // <<-- See text in post below.**

IF Z4 or Z5 or Z6 or Z7 or Z8 or Z9 or Z10 or Z11 or Z12 or Z13 or Z14 or Z15 or Z16 or Z17 or Z18 or Z19 or Z20 or Z21 or Z22 or Z23 or Z24 or Z25 THEN

MyStop = 8*ATRMult

WCS = MyStop

InitialEquity = 3000

Equity = InitialEquity+Strategyprofit

MyPercRisk = 0.995 // Max risk, bör ej vara över 2% = 0.98

MinPositionSize = 1//Minsta size

PositionSize = MinPositionSize*ROUND((Equity-(Equity*MyPercRisk))/(((MinPositionSize*WCS))))

SELLSHORT Positionsize CONTRACTS AT MARKET

JustEntered = 1 // <<--

endif

endif

endif

**) Without such an If, the SellShort will cancel out the Buy of the first section if the Buy happened as well.

You should NOT depend on the conditions for entering, no matter that you obviously think they will be mutually exclusive.

I only picked one example from your code, but it is full with these “mistakes”. So all your Sells and ExitShorts – same problem. For each of these commands, check whether you already executed them (e.g. If not JustExited).

IF Count8 >= 1 AND BrkES8 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET

endif

Maye the CountOfPosition is good habit (told by someone), but I would never do that. Your code will be vague (ambiguous) because of it, because you won’t be able to follow (ProRealCode itself won’t have a problem with it). Look at this example :

IF Count6 >= 1 AND BrkES6 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET // Suppose this one triggers ...

endif

IF BECalcS7 THEN

Count7 = Count7 + 1

endif

IF Count7 >= 1 AND BrkES7 THEN

EXITSHORT abs(CountOfPosition) CONTRACTS AT MARKET // ... then CountOfPosition is unchanged here.

endif

Thus while you may think that when not OnMarket CountOfPosition will be 0 and nothing will happen anyway, you yourself won’t be able to check / follow what really will be happening. This is thus indeed because CountOfPosition will remain unchanged during all the lines of your code (this thus too may counteract an earlier command as per my example above). Only at the next call (when the current bar has passed / closed) these kind of “constants” will have been updated. Same with OnMarket and everything.

Notice that if you leave out the number of Contracts, it will also work for your example (not adding position to already existing position). Thus “ExitShort at Marlet” suffices.

When you apply my “hints” it will be an eyeopener for you how

– suddenly the results are wildly different

– you suddenly understand what’s happening everywhere.

Have fun !

Peter

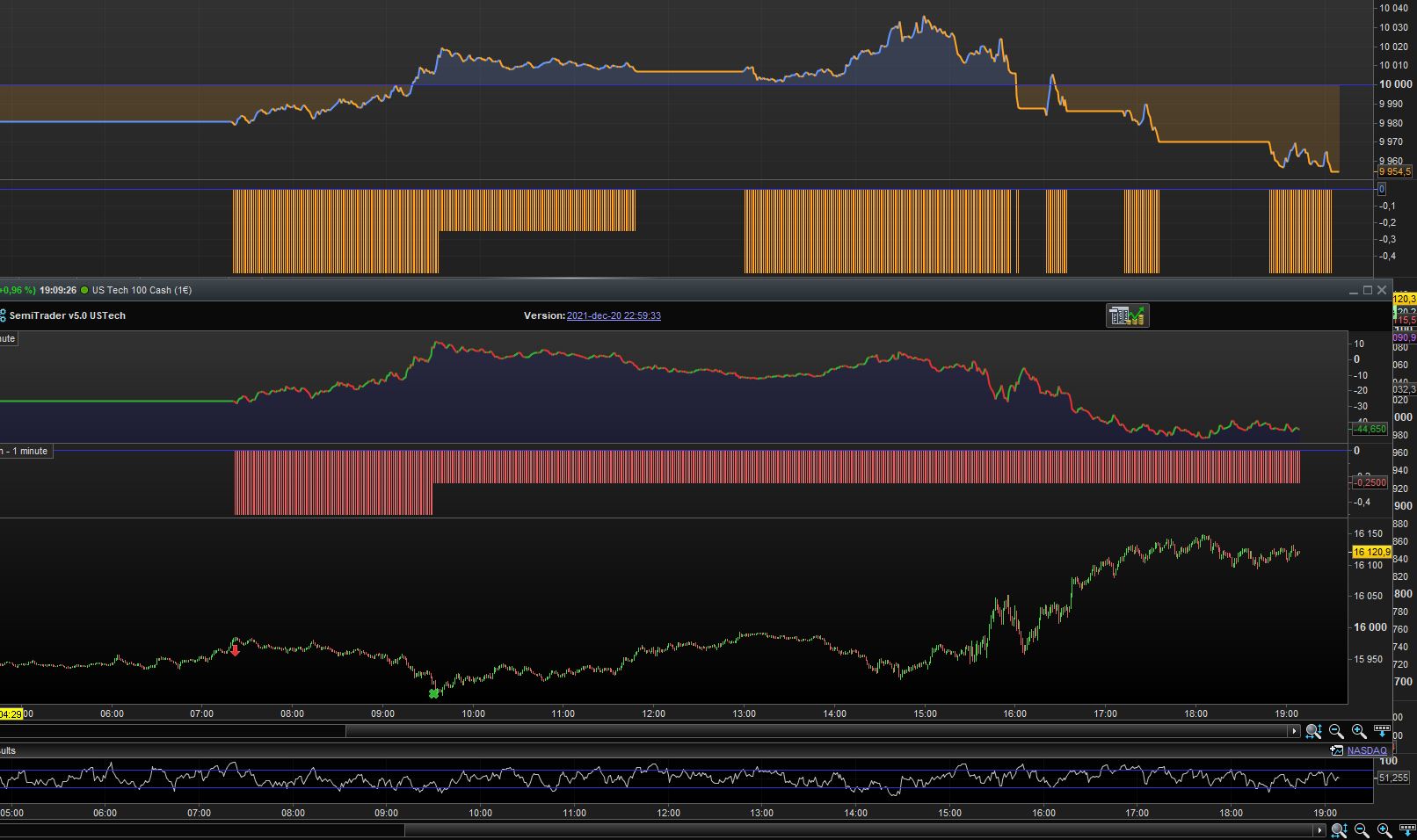

Huge thanks Peter, i will most certainly start working on it. I actually got an new example today, i use the same code but with other levels on USTech, as seen in the image attached where i put the backtest above the actual trade, the position does the first move to halfen the size, but this should in my mind (before adding the wisedom from you Peter) also trigger my other condition to move the SL to BE according to my condition,

I will get on the task to correct my errors, please let me know if there is other vital mistakes i should consider 🙂

BR Anders