The distance of 2 moving averages … if both are on top of each other … can I somehow code them in percent?

For example:

SMA20> SMA200

And of that the distance in percent?

There you go:

PerCent = (Sma20 * 100 / Sma200) - 100

And how exactly can I use this calculated number for long or short entries? My idea is to only enter into trades when the two SMAs are not too far apart.

JS

JSParticipant

Senior

If PerCent > x then => Buy

If PerCent < y then => SellShort

x for example 0.5%

y for example -0.5%

Crossing MA’s at x = 0 or y = 0

distance in percent?

Distance in percent of what … the faster average / SMA20?

So where SMA20 > SMA200 …

((SMA20-SMA200)/SMA20)*100

JSParticipant

Senior

Distance in percent of the Close

PerCent is the same as:

S1 = Average[20](Close)

S2 = Average[200](Close)

Dist = S1 – S2

DistPerc = (Dist / Close) * 100

I was always very good at math … I’m trying to understand which formula is better. I’ll just try it out. Thank you very much.

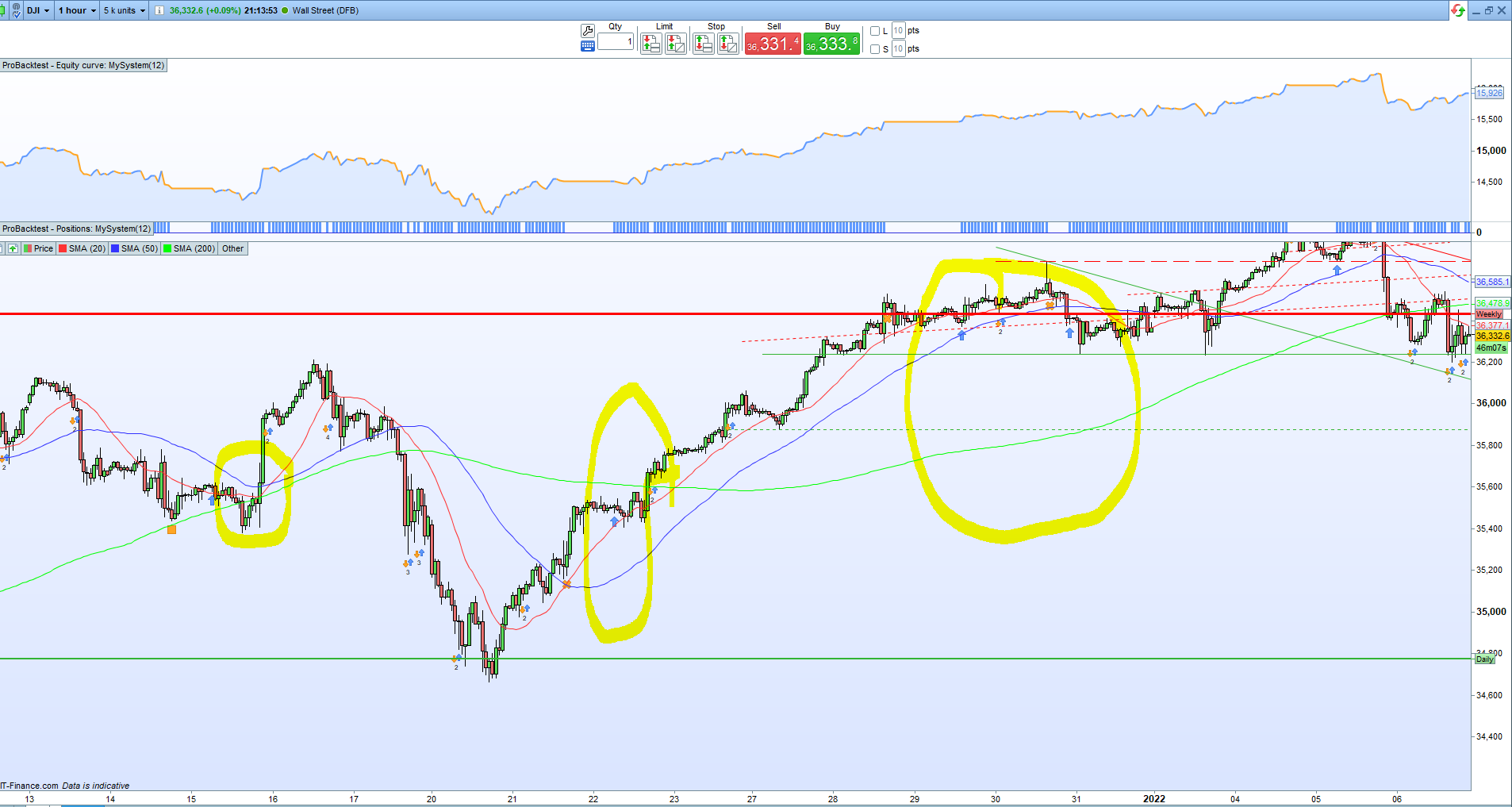

Hi. New to this forum. Such a great comunity.

My firt try with an algo. Inspiration from Phoentzs

Is this someting to build on or what do u think, Too much time in market? How to improve thos without curvefitting?

// Wallstreet 1H - SMA Distance

// SnorreDK @ prorealcode.com

//2022-01-06

//To do - Better entrys - more standard filters?

//Try other trailing

//****************************************** **************************************

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

ONCE sl = 1.5

ONCE sl2 = 1.0

ONCE A1 = 70.0

ONCE A2 = 60.0

ONCE tsm = 4.0

ONCE tst = 4.6

ONCE tst1 = 1.5

ONCE st = 0.28

ONCE A11 = 10.0

ONCE A22 = 20.0

ONCE y1 = -3.1

positionsize = 1

Timeframe(4h, updateonclose)

AA=RSI[14](close)

Timeframe(default)

CB2 = (AA<A1 and AA>A11) //4H RSI filter

CS2 = (AA<A2 and AA>A22) //4H RSI filter

S1 = Average[20](Close)

S2 = Average[200](Close)

Dist = S1 - S2

DistPerc = (Dist / Close) * 100

CB1 = DistPerc > y1

CS1 = DistPerc < y1

If not (DayOfWeek = 2) then

If CB1 and CB2 and not shortonmarket then

BUY positionsize contracts AT MARKET

Endif

If CS1 and CS2 and not longonmarket then

SELLSHORT 1 CONTRACTS AT MARKET

Endif

endif

//****************************************************************************************

// trailing stop atr

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = st // typically between 0 and 0.25

once tsminatrdist = tsm // typically between 1 and 4

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance, set to IG min value

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = tst // ts atr distance, typically between 4 and 10

trailingstopshort = tst1 // ts atr distance, typically between 4 and 10

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

If shortonmarket then

SET STOP %loss SL2

endif

If Longonmarket then

SET STOP %loss SL

endif

Personally, I think it’s been on the market for a long time, maybe too long. I can see that the setup is modeled on my H4 breakout. This type of setup works very well for me. But my little timeframe is M1. At the moment I’m also working on a setup with RSI. But with RSI2 in the H4 as a reversal. Build it yourself with the timeframes like H4 breakout. But it is still in progress.

Sorry. My aproach with sma-distance doesnt make any sense.

MA20 and MA200 are close together buy signal ?, far apart buy signal ??

it’s because distperc never goes above 3 or below -3 so the condition is always true

I’ve put this type of calculation aside for now. Even if it would be nice to calculate it so easily, it somehow doesn’t work that way. I continue to use my classic pullbacks. So MACD pullback or RSI pullback in connection with the MAs. That works pretty well.

JSParticipant

Senior

S1 = Average[20](Close)

S2 = Average[200](Close)

Dist = S1 - S2

DistPerc = (Dist / Close) * 100

CB1 = DistPerc > y1

CS1 = DistPerc < y1

The distance between the MA’s can be positief or negatief and zero for the crossing of the MA’s

For a Long signal use DistPerc > “Positief Value” (for example yl = 0.5)

For a Short signal use DistPerc < "Negative Value" (for example ys = -0.5)

In your code there is only a negative value y1 = -3.1