All,

I have modified the "Quino Statistics Plotter" indicator created last August,

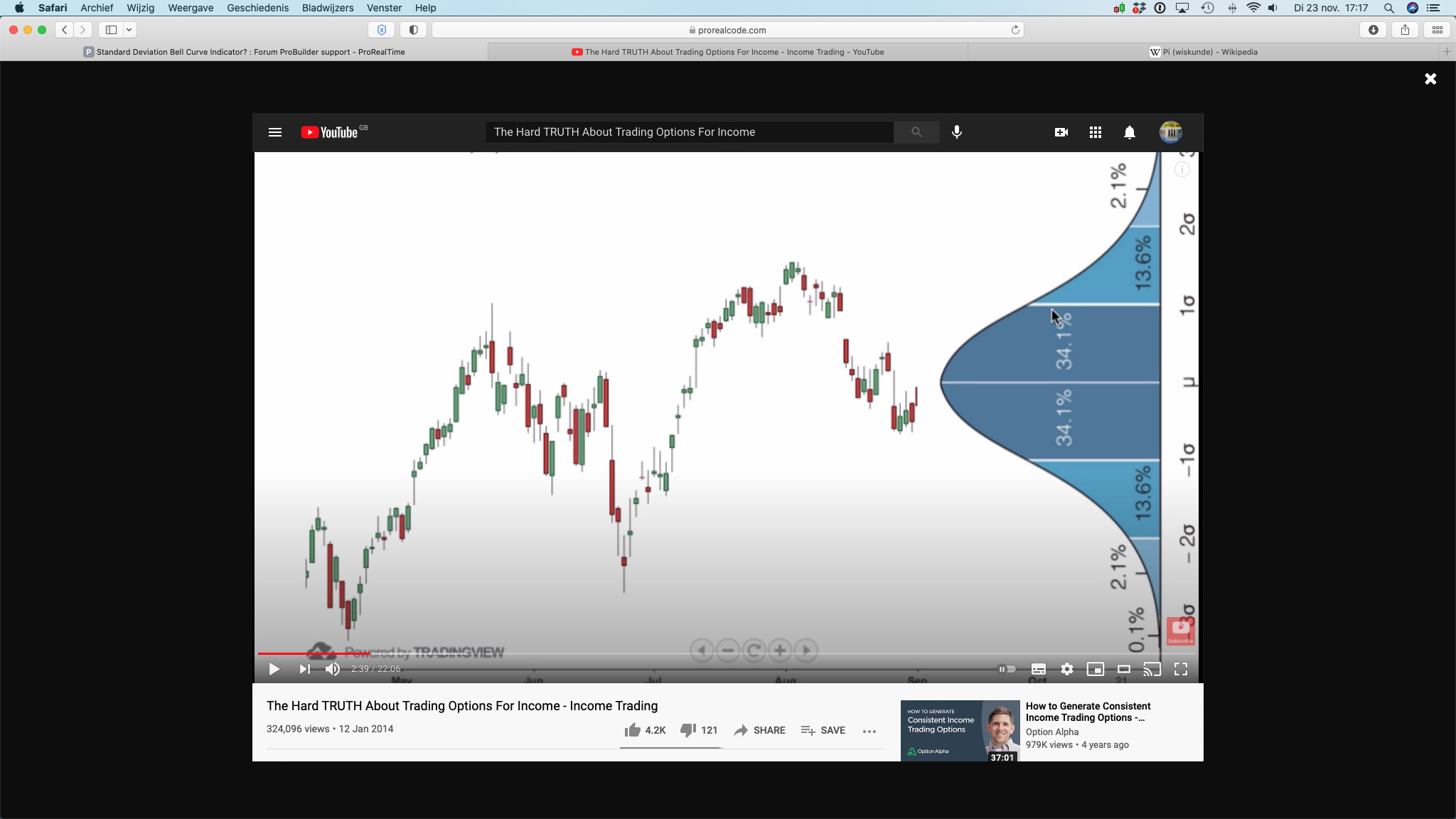

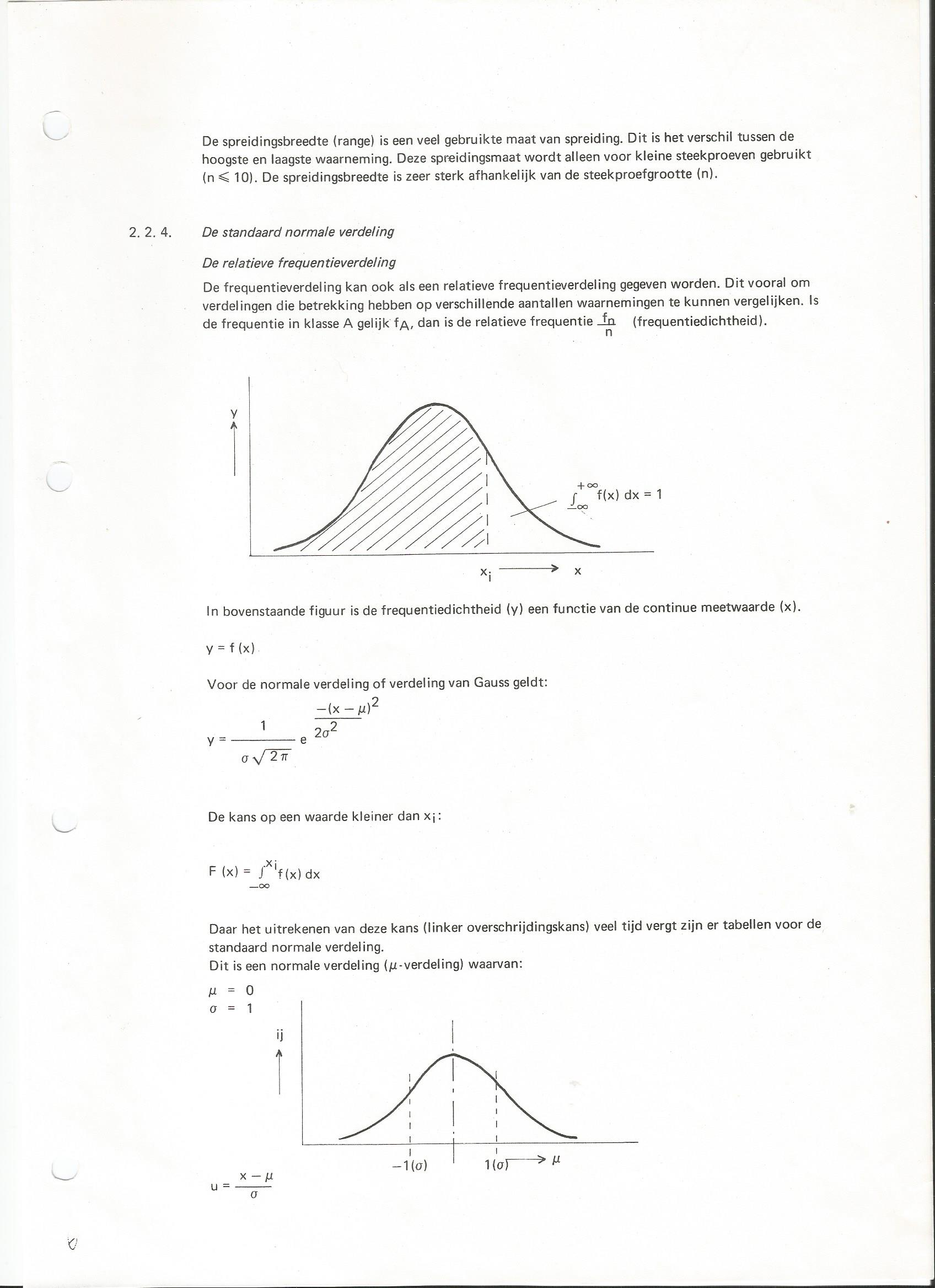

to map the theoretical Gaussian curve to a distribution of "Close" on a defined number of bars.

This allows to have an idea if this distribution (Price) has the contours of a Gaussian curve[attachment file="182879"]

.

See the old version in the indicator library for more information on the other functionalities.

// Quino Statistics Plotter

// By Quino

// version of 05/12/2021

//===================================================================================

// NbrOfSamples : Number of consecutive close

// NbrOfClasses : Number of intervals of values in which we store the values of “close”

// InformationDisplay :

// – false : display of the histogram only

// – true : display of limit values for each class and % of occurrence

// ClassTracer :

// – false : indicator that can be used stand-alone (curve and information)

// – true : indicator usable in the price indicator. By locating the class of the last “close” or another class. Class boundaries are represented by two horizontal lines on the price chart.

// ClassIndex : manual search for the class number corresponding to the last “close” or another class. Alignment of the cue point under the value of the last close (in red)

// GaussianShape

// – false : No Gaussian curve drawn

// – true : Gaussian curve drawn from avrerage and standard deviation of the selected number of consecutive close

//Typical use : NbrOfSamples=150 ; NbrOfClasses=30 (5 samples per class minimum)

//===================================================================================

NbrMaxFrequency=1000 // Number max of occurency per class

AdjustA=30 // Scale calibration

AdjustB=4 // Position calibration

//———————————-

if islastbarupdate then

for k =0 to NbrOfSamples-1 do

$v[k]=close[k]

next

for i= NbrOfSamples-1 downto 0 do

$d[i]=arraymax($v)

for j=NbrOfSamples-1 downto 0 do

if $v[j]=$d[i] then

$v[j]=0

break

endif

next

next

Bin=(arraymax($d)-arraymin($d))/(NbrOfClasses)

For i=0 to NbrOfClasses do

$r[i]=0

next

BinA=arraymin($d)

for j=0 to NbrOfClasses-1 do

Dtemp=0

for i=0 to NbrOfSamples-1 do

if j < NbrOfClasses then

if $d[i]>=BinA+ j*Bin and $d[i] <BinA+(j+1)*Bin then

Dtemp=Dtemp+1

else

if $d[i]>=BinA+ j*Bin and $d[i] =<BinA+(j+1)*Bin then

Dtemp=Dtemp+1

endif

endif

endif

next

$r[j]=Dtemp

next

Vmoy=average[NbrOfSamples](close)

Vect=std[NbrOfSamples](close)

for k =0 to NbrOfClasses-1 do

$Vg[k]=((exp(-0.5*square(((BinA+ k*Bin)-Vmoy)/Vect)))/Vect*sqr(6.18))

next

if GaussianShape Then

Scale=max(arraymax($r),arraymax($Vg))+12

else

Scale=arraymax($r)+12

endif

If scale < AdjustA then

CorrecYY=1

CorrecY=1

endif

For i=1 to (NbrMaxFrequency/AdjustA) do

if scale>=i*AdjustA and scale<(i+1)*AdjustA then

CorrecYY=i+1

CorrecY=(i+1)*AdjustA/AdjustB

endif

next

for i= 0 to NbrOfClasses-1 do

if ClassTracer then

ValCaseMax=(BinA+ClassIndex*Bin)

ValCaseMin=(BinA+(ClassIndex-1)*Bin)

drawsegment(barindex[NbrOfSamples-1-i],ValCaseMax,barindex[NbrOfClasses-i-1],ValCaseMax)coloured (51,153,255)

drawsegment(barindex[NbrOfSamples-1-i],ValCaseMin,barindex[NbrOfClasses-i-1],ValCaseMin)coloured (0,51,153)

if i=ClassIndex then

tag=1

else

tag=undefined

endif

else

drawsegment(barindex[NbrOfClasses-i],$r[i],barindex[NbrOfClasses-i],0)coloured (0,0,0)

drawsegment(barindex[NbrOfClasses-i],$r[i],barindex[NbrOfClasses-i+1],$r[i])coloured (0,0,0)

drawsegment(barindex[NbrOfClasses-i+1],0,barindex[NbrOfClasses-i+1],$r[i]) coloured (0,0,0)

drawpoint(barindex[NbrOfClasses-ClassIndex+1],tag)coloured (0,0,50)

if GaussianShape then

drawsegment(barindex[NbrOfClasses-i+1],$Vg[i],barindex[NbrOfClasses-i],$Vg[i+1])coloured (255,0,0)

endif

if InformationDisplay then

for i= 0 to NbrOfClasses-1 do

temp=round(($r[i]/(NbrOfSamples))*10000)/100

temp1=round((BinA+(i)*Bin),2)

temp2=round((BinA+(i+1)*Bin),2)

drawtext(“%= #temp#”,barindex[NbrOfClasses-i],Scale+CorrecY-2*CorrecYY)coloured (0,0,255)

if close >= temp1 and close < temp2 then

drawtext(“#temp1#”,barindex[NbrOfClasses-i],Scale+CorrecY-6*CorrecYY)coloured (255,0,0)

drawtext(“#temp2#”,barindex[NbrOfClasses-i],Scale+CorrecY-4*CorrecYY)coloured (255,0,0)

else

drawtext(“#temp1#”,barindex[NbrOfClasses-i],Scale+CorrecY-6*CorrecYY)coloured (0,0,0)

drawtext(“#temp2#”,barindex[NbrOfClasses-i],Scale+CorrecY-4*CorrecYY)coloured (0,0,0)

endif

next

drawtext(“Average= #Vmoy#”,barindex-4,Scale-8*CorrecYY)coloured (0,0,0)

drawtext(“STD= #Vect#”,barindex-4,Scale-10*CorrecYY)coloured (0,0,0)

endif

endif

next

endif

if GaussianShape Then

Scale=max(arraymax($r),arraymax($Vg))+12+CorrecY

else

Scale=arraymax($r)+12+CorrecY

endif

if not ClassTracer then

zero=0

else

zero=undefined

Scale=undefined

endif

return Scale as “Vertical Reference”,zero as “Zero”

[attachment file="182879"]